Introduction

Singapore businesses operate under SFRS(I) 16 — a standard aligned with IFRS 16 — but as trade, investment, and cross-border operations with the US grow, many companies find themselves needing to understand or comply with US GAAP's ASC 842. On the surface, both standards brought leases onto the balance sheet, creating the impression of convergence. Look closer, and the differences in lease classification, variable payments, exemptions, and sale-leaseback treatment create real complexity for dual reporters.

Why does this matter? The forthcoming SGX-Nasdaq Global Listing Board (GLB), scheduled to launch mid-2026, will enable companies with market capitalisation of S$2 billion and above to dual-list on both exchanges through a single set of documents. This will substantially increase the number of Singapore companies requiring simultaneous IFRS and US GAAP lease accounting compliance.

Add to that the growing number of Singapore subsidiaries of US multinationals, and the compliance burden becomes concrete.

This article breaks down the key divergences between IFRS 16 and ASC 842 — covering lease classification, variable payment treatment, short-term and low-value exemptions, and sale-leaseback accounting — with a focus on what Singapore businesses specifically need to watch.

Key Takeaways

- Singapore follows SFRS(I) 16, identical to IFRS 16 — all leases use a single on-balance sheet model

- US GAAP (ASC 842) uses a dual model: finance and operating leases produce different income statement impacts

- IFRS 16 remeasures variable lease payments on contractual cash flow changes; ASC 842 requires a separate triggering event

- IFRS 16 allows a low-value asset exemption (USD 5,000 threshold); ASC 842 has no equivalent

- Singapore entities reporting to US stakeholders or listed on US exchanges must maintain parallel processes under both standards

ASC 842 vs IFRS 16: Quick Comparison

Singapore companies reporting under SFRS(I) — which mirrors IFRS 16 — and those with US-listed subsidiaries subject to ASC 842 face nine structural differences between the two standards. The table below maps them side by side.

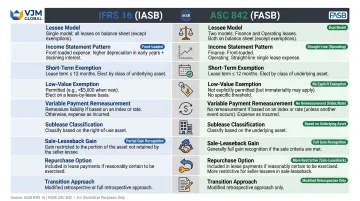

| Feature | IFRS 16 (IASB) | ASC 842 (FASB) |

|---|---|---|

| Issuing Body | International Accounting Standards Board (IASB) | Financial Accounting Standards Board (FASB) |

| Lessee Model | Single model — all leases on-balance sheet | Dual model — finance vs. operating lease classification |

| Income Statement Pattern | Depreciation + interest (front-loaded) | Finance: depreciation + interest; Operating: straight-line expense |

| Short-Term Exemption | ≤12 months, no purchase option at all | ≤12 months, no purchase option reasonably certain to exercise |

| Low-Value Exemption | Yes (~USD 5,000 when new) | No equivalent exemption |

| Variable Payment Remeasurement | When contractual cash flows change | Only when other remeasurement events occur |

| Sublease Classification | By reference to ROU asset | By reference to underlying asset |

| Sale-Leaseback Gain | Limited to rights transferred to buyer | Full gain if qualifying sale and not finance leaseback |

| Repurchase Option | Always fails sale treatment | May allow sale for non-real estate at fair value |

The key practical difference sits in the income statement: IFRS 16's single model inflates EBITDA by reclassifying lease expense to depreciation and interest below the EBITDA line, while ASC 842's operating lease treatment keeps that expense within operating costs, leaving EBITDA unchanged. For Singapore businesses dual-reporting under both frameworks — for example, a SGX-listed company with a US subsidiary — this divergence means the same lease portfolio can produce materially different EBITDA figures depending on which standard applies.

Understanding IFRS 16 — And Why Singapore Already Follows It

Singapore adopted SFRS(I) 16 (substantively identical to IFRS 16) for periods beginning on or after 1 January 2019. This means most Singapore-incorporated companies and SGX-listed entities already apply IFRS 16 principles.

The Accounting Standards Committee (ASC) designed the SFRS(I) framework so companies can provide a "dual statement of compliance" with both SFRS(I) and IFRS, a meaningful advantage for businesses with international investors.

The core IFRS 16 lessee model:

- All leases (above short-term and low-value thresholds) go on-balance sheet as a right-of-use (ROU) asset and corresponding lease liability

- No distinction between "operating" and "finance" leases for lessees

- Expense splits into depreciation of the ROU asset and interest on the lease liability

- This produces a front-loaded expense pattern — higher total expense in early years, lower in later years

Two practical exemptions reduce compliance burden:

- Leases of 12 months or less with no purchase option qualify for the short-term exemption

- Assets worth approximately USD 5,000 or less when new qualify for the low-value exemption (laptops, phones, tablets, small office furniture)

Use Cases for IFRS 16 in Singapore

Knowing which entities fall under IFRS 16 helps clarify where these rules apply in practice:

IFRS 16 applies in these scenarios:

- SGX-listed companies — virtually all of SGX's approximately 615 listed securities apply SFRS(I) 16

- Singapore subsidiaries of multinational groups preparing consolidated financial statements

- Companies raising capital from international investors requiring IFRS-compliant financials

- Entities preparing consolidated statements under SFRS(I)

One important exception applies to lessors: under IFRS 16, lessors still classify leases as finance or operating. This distinction matters for Singapore businesses that own and lease out assets like real estate or equipment.

Understanding ASC 842 — The US GAAP Lease Standard

ASC 842, issued by the FASB, became effective for US public companies in 2019 and US private companies in 2022. Singapore businesses encounter it when they have a US parent, are preparing for a US IPO, have US investors requiring GAAP financial statements, or are acquiring US entities.

ASC 842 retains a dual lessee model. Finance leases follow a pattern similar to IFRS 16 — depreciation plus interest, with front-loaded expense. Operating leases produce a single straight-line lease expense on the income statement, masking the liability build-up visible under IFRS 16.

Finance lease classification criteria (any one triggers finance lease treatment):

- Ownership transfers by lease end

- Purchase option reasonably certain to be exercised

- Lease term covers major part of asset's economic life (generally ≥75%)

- Present value of payments equals substantially all fair value (generally ≥90%)

- Asset has no alternative use to lessor

Use Cases for ASC 842 Among Singapore Businesses

Singapore businesses need ASC 842 when:

- Wholly-owned subsidiaries of US parents filing US GAAP consolidated accounts

- Dual-listed on SGX and a US exchange (NYSE/NASDAQ) — soon to be streamlined via the GLB

- Converting to US GAAP for a US acquisition or capital raise

- US institutional investors requiring GAAP-compliant reporting

With the Global Listing Bridge (GLB) enabling dual-listing for companies with a market cap of S$2 billion and above, more Singapore entities will manage both standards simultaneously.

6 Key Differences Singapore Businesses Need to Know

Difference 1: Single Model vs. Dual Classification

IFRS 16 applies one accounting model for all lessee leases — every lease gets treated like a finance lease.

ASC 842 requires lessees to classify each lease as either finance or operating based on the five criteria above. Operating leases produce straight-line expense — a meaningful income statement difference.

Financial ratio impact:

Research by the CFA Institute documented that bringing operating leases on-balance sheet has measurable consequences:

- Median 13% EBITDA increase across companies studied

- Median 22% increase in reported debt

- Gearing ratios (debt-to-equity) up approximately 30% on average

- Retail sector: debt increases of 40–60%; airlines: 30–50%

For dual reporters, IFRS 16 produces higher EBITDA than ASC 842 for operating leases. Under IFRS 16, all lease expense is removed from above the EBITDA line. Under ASC 842, operating lease expense stays within operating costs.

Difference 2: Variable Lease Payment Remeasurement

For leases with payments tied to an index or rate (e.g., CPI-adjusted office leases — common in Singapore):

IFRS 16 requires the lessee to remeasure the lease liability every time there is an actual change in contractual cash flows (e.g., when the annual CPI adjustment takes effect).

ASC 842 only remeasures the lease liability when another remeasurement event occurs (e.g., a change in lease term). Increases from index adjustments are expensed as incurred.

Practical consequence: Balance sheet figures for the same CPI-linked lease will diverge over time between the two standards — a common source of reconciliation complexity for Singapore dual reporters.

Difference 3: Low-Value Asset Exemption

IFRS 16 permits lessees to keep leases of low-value assets off the balance sheet — assets individually valued at approximately USD 5,000 or less when new. Examples include laptops, tablets, small office furniture, and telephones.

ASC 842 provides no equivalent exemption. Entities rely on their own materiality judgments instead.

Impact: Singapore businesses applying IFRS 16 may have certain leases entirely off-balance sheet that would require on-balance sheet treatment under ASC 842, requiring separate tracking for dual reporters.

Difference 4: Short-Term Lease Definition Divergence

Both standards exempt leases of 12 months or less, but differ on purchase options:

IFRS 16: Any lease containing a purchase option of any kind cannot qualify as short-term — regardless of how unlikely exercise is.

ASC 842: A lease with a purchase option can still qualify as short-term if the lessee is not reasonably certain to exercise it.

This means the population of short-term leases identified may differ between standards for the same portfolio.

Difference 5: Sublease Classification

When a Singapore company acts as an intermediate lessor in a sublease arrangement:

IFRS 16 classifies the sublease by reference to the ROU asset from the head lease. Because the ROU asset has a shorter remaining life, finance lease classification for the sublease is the common outcome.

ASC 842 classifies by reference to the underlying physical asset, which more frequently produces operating lease classification.

This affects how sublease income and the related asset appear on financial statements — particularly relevant for Singapore companies in co-working, office-sharing, or real estate management.

Difference 6: Sale-and-Leaseback Transactions

For Singapore companies monetizing real estate or equipment through sale-leaseback:

Gain recognition:

- IFRS 16: The seller-lessee can only recognize the gain related to the rights transferred to the buyer-lessor. The portion related to the retained ROU is offset against the ROU asset.

- ASC 842: If the transaction qualifies as a sale and the leaseback is not a finance lease, the full gain on the transaction is recognized.

Repurchase options:

- IFRS 16: A repurchase option always results in a failed sale — the transaction is accounted for as a financing arrangement.

- ASC 842: A repurchase option does not automatically preclude sale accounting. For non-real estate assets at fair value with market alternatives available to the buyer, sale recognition may still be permitted.

Singapore companies must model both IFRS 16 and ASC 842 outcomes during transaction structuring. Leaving this analysis until the reporting stage creates avoidable complexity and potential restatement risk.

What This Means for Singapore Businesses Navigating Both Standards

Singapore business profiles most at risk of dual-reporting complexity:

- SGX-listed companies with US institutional shareholders requesting GAAP-compliant reporting

- Singapore entities preparing for US IPO — particularly those targeting the GLB's mid-2026 launch

- Wholly-owned subsidiaries of US multinationals consolidating under US GAAP

- Singapore companies acquiring or integrating US businesses

For these entities, the same lease portfolio will produce different balance sheet values, income statement patterns, and financial ratios under IFRS 16 and ASC 842 — requiring separate ledgers, reconciliations, and disclosures.

The Practical Compliance Burden

Dual reporters must maintain two sets of lease calculations:

- Tracking which leases qualify as operating vs. finance under ASC 842 (but are treated identically under IFRS 16)

- Maintaining separate remeasurement schedules for CPI-linked leases

- Identifying leases that fall within the low-value exemption under IFRS 16 but require capitalization under ASC 842

- Reconciling sublease classifications that differ between standards

- Modeling sale-leaseback transactions under both frameworks before execution

Building Scalable Dual-Reporting Frameworks

The core challenge is not just calculation — it's maintaining audit-ready documentation under two different disclosure regimes simultaneously. Advisors with cross-border accounting experience can map your lease portfolio against both standards, flag divergence points before they create restatement risk, and structure disclosures correctly for each framework.

VJM Global supports multinational clients navigating IFRS 16 and ASC 842 simultaneously, combining Chartered Accountant and CPA expertise to manage the reconciliation work that dual reporting demands.

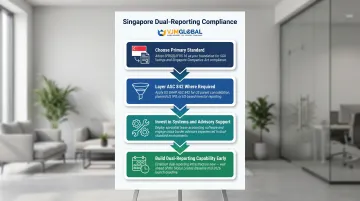

Decision Framework

Singapore businesses should:

- Choose their primary standard based on regulatory requirement — SFRS(I)/IFRS 16 for SGX and Singapore Companies Act compliance

- Layer ASC 842 compliance only where US GAAP financial statements are required (US parent consolidation, US IPO, US investor requirements)

- Invest in lease accounting systems and advisory support capable of handling both simultaneously

- Begin building dual-reporting capability well before initiating a dual-listing process or US capital raise

With the GLB's mid-2026 launch approaching, Singapore growth companies that haven't yet encountered US GAAP requirements will start facing them. Building dual-reporting capability now — rather than under IPO timeline pressure — is the practical move.

Conclusion

IFRS 16 and ASC 842 share the same foundational goal — bringing lease obligations onto the balance sheet — but diverge in ways that affect income statement presentation, balance sheet values, and compliance processes. Singapore businesses that only report under SFRS(I)/IFRS 16 face a relatively straightforward regime; those with US reporting obligations need to understand these six differences and build processes to manage them separately.

The dual classification model under ASC 842, combined with differences in variable payment remeasurement, low-value asset exemptions, and sale-leaseback treatment, creates persistent reconciliation challenges. With the SGX-Nasdaq Global Listing Board expanding the pool of companies requiring dual compliance, building that capability before audit deadlines arrive is far less costly than scrambling to catch up afterward.

Companies that should act sooner rather than later include those:

- Unsure whether their lease portfolio triggers dual-reporting obligations

- Preparing for a US capital raise, IPO, or cross-border acquisition

- Already operating under both SFRS(I) and US GAAP but managing them as a single process

- Approaching an audit cycle without a documented reconciliation framework

Engaging cross-border accounting advisors early — before positions are locked into filed financials — avoids the retroactive adjustments and audit complications that become significantly harder to unwind under time pressure.

Frequently Asked Questions

What is the difference between US GAAP and IFRS for lease accounting?

Both ASC 842 (US GAAP) and IFRS 16 require leases on-balance sheet, but they diverge on lessee classification. IFRS 16 uses a single model treating all leases like finance leases, with front-loaded expense. ASC 842 distinguishes between finance and operating leases — operating leases produce straight-line expense and leave EBITDA unchanged.

What are the specific practical differences between IFRS 16 and ASC 842?

Beyond the single vs. dual model distinction, four differences affect day-to-day accounting:

- IFRS 16 remeasures variable lease payments when cash flows change; ASC 842 only on specific triggers

- IFRS 16 includes a low-value asset exemption (roughly USD 5,000); ASC 842 has no equivalent

- Sale-leaseback gain recognition differs significantly between the two standards

- IFRS 16 applies one depreciation-plus-interest expense pattern; ASC 842 operating leases use straight-line

What is the US GAAP equivalent of IFRS 16 (lease accounting)?

ASC Topic 842, issued by FASB and effective from 2019 for public companies, is the US GAAP equivalent. Both standards bring leases on-balance sheet, but ASC 842 retains a dual classification model (finance vs. operating), creating different income statement impacts compared to IFRS 16's single model.

Which lease accounting treatment is allowed under US GAAP but not under IFRS?

Operating lease classification for lessees is permitted under ASC 842, producing straight-line expense rather than split depreciation and interest. Additionally, US GAAP allows private companies to use a risk-free discount rate as a practical expedient — neither option exists under IFRS 16.

Are leases capitalized under IFRS?

Yes. Under IFRS 16, all leases above the short-term and low-value thresholds are capitalized as a right-of-use asset and lease liability on the balance sheet. This replaced the old off-balance sheet operating lease treatment under IAS 17.

What are the main types of leases under US GAAP and IFRS?

IFRS 16 gives lessees a single lease type: all are treated as finance-type. ASC 842 gives lessees two options — finance or operating. For lessors, both standards distinguish between finance/sales-type leases and operating leases.