Introduction

From January 2026, FRS 102 amendments will require most leases to be recognised on the balance sheet—ending the era of "off-balance sheet" operating leases for approximately 3.4 million UK businesses. This is the most significant change to UK GAAP lease accounting in a generation, affecting private companies, SMEs, LLPs, and partnerships across the UK.

The practical impact is significant. Lease liabilities and corresponding Right-of-Use (ROU) assets will appear on balance sheets for the first time — with knock-on effects on EBITDA, gearing ratios, and interest cover that could trigger covenant breaches, affect dividend capacity, or push companies over statutory size thresholds.

This guide covers:

- The current UK GAAP lease accounting framework and what's changing

- How the new lessee accounting model works under FRS 102

- The financial statement implications — ratios, covenants, and disclosures

- Practical steps to prepare before the January 2026 effective date

TL;DR: Key Takeaways

- FRS 102 amendments effective from 1 January 2026 bring most operating leases onto the balance sheet

- Lessees must recognise Right-of-Use assets and lease liabilities measured at present value of future payments

- Short-term leases (≤12 months) and low-value assets remain exempt from on-balance sheet treatment

- UK-specific simplifications include the Obtainable Borrowing Rate option and fewer modification triggers than IFRS 16

- FRS 102 changes apply to all preparers — including Section 1A small entities — but not FRS 105 micro-entities

UK GAAP and Lease Accounting: The Framework

UK GAAP refers to the suite of financial reporting standards issued by the Financial Reporting Council (FRC) that UK companies must follow when preparing financial statements. Companies use either UK GAAP or UK-endorsed IFRS depending on their size, listing status, and structure.

Four standards define the landscape, each applying to a different type of entity:

- FRS 102 – The primary standard for most private companies, with Section 20 governing lease accounting

- FRS 101 – Reduced disclosure framework for qualifying subsidiaries of IFRS-reporting groups

- FRS 105 – Micro-entities standard (not subject to the new lease changes)

- UK-endorsed IFRS – Used by UK-listed groups (already subject to IFRS 16, not FRS 102)

The upcoming FRS 102 lease amendments apply to all FRS 102 reporters, including FRS 102 Section 1A small entities. Understanding which standard applies to your entity is the starting point before working through how the amended Section 20 rules affect your lease reporting obligations.

What's Changing Under FRS 102 for Leases in 2026

The Core Shift in Accounting Treatment

Under the current (pre-2026) FRS 102, operating leases remain off the balance sheet with rental expense recognised straight-line through the profit and loss account. Only finance leases are capitalised. The amendments eliminate this dual model for lessees, bringing nearly all leases onto the balance sheet, mirroring the IFRS 16 approach.

New Lease Definition and Embedded Leases

A contract is (or contains) a lease if it conveys the right to control the use of an identified asset for a period in exchange for consideration. Two critical tests apply:

Identified Asset Test:

- The asset must be explicitly or implicitly specified

- The supplier must not have a substantive right to substitute the asset

Control Test:

- The customer must have the right to obtain substantially all economic benefits from the asset

- The customer must have the right to direct how and for what purpose the asset is used

This definition requires businesses to re-examine service contracts, outsourcing arrangements, and equipment agreements for embedded leases—contracts that may not be labelled "lease" but meet the definition.

Transition Approach

The amendments are applied retrospectively using a modified retrospective approach. Key features:

- Comparative information is not restated

- Cumulative effect is recognised as an adjustment to opening retained earnings at the date of initial application

- Practical expedients are available, including use of a single discount rate for similar lease portfolios and treating leases ending within 12 months as short-term

- IFRS group subsidiaries can elect a practical expedient to align with parent group transition

Tax Treatment on Transition

Schedule 14 of the Finance Act 2019 governs the corporation tax treatment. Key points to understand:

- Transitional adjustments are spread over the weighted average remaining lease term, not taxed immediately

- This creates a timing difference between accounting and tax treatment

- Deferred tax obligations arising from that difference must be tracked on a lease-by-lease basis

The ICAEW warns that for very large companies, the first corporation tax payments reflecting these changes could fall due as early as 14 March 2026 for calendar year-end entities.

Lessor Accounting Remains Unchanged

Lessor accounting remains unchanged under the amended standard. Lessors continue to classify leases as operating or finance and account for them accordingly. For most businesses, then, the compliance effort centres on identifying, measuring, and recognising lessee obligations — the focus of the sections that follow.

The New Lessee Accounting Model: ROU Assets and Lease Liabilities

Lease Liability Measurement

At commencement, the lease liability equals the present value of future unpaid lease payments over the lease term. The lease term includes:

- The non-cancellable period

- Extension periods the lessee is reasonably certain to exercise

- Periods covered by termination options the lessee is reasonably certain not to exercise

Variable lease payments linked to an index or rate are included at initial measurement. Usage-based or performance-based variable payments are expensed as incurred.

Discount Rate Options: A UK-Specific Simplification

Once you've determined what goes into the lease liability, the next step is choosing how to discount it. FRS 102 provides three options in a hierarchy:

- Interest rate implicit in the lease (if readily determinable)

- Incremental Borrowing Rate (IBR) – the rate to borrow over a similar term with similar security for an asset of similar value

- Obtainable Borrowing Rate (OBR) – the rate to borrow an amount equal to total undiscounted lease payments over a similar term

The OBR is a UK-specific simplification not available under IFRS 16. It recognises that many UK private companies—particularly SMEs—may not have formal borrowing facilities from which to derive an IBR. The OBR provides a more accessible alternative without requiring access to formal credit facilities.

Discount rate sensitivity example: For a 5-year equipment lease with £50,000 annual payments, a 4.0% discount rate produces a present value of approximately £222,590, while a 7.0% rate produces approximately £205,010—a difference of £17,580.

Right-of-Use Asset Measurement

The ROU asset is initially measured at the amount of the lease liability, adjusted for:

- Lease payments made at or before commencement (less any lease incentives received)

- Initial direct costs incurred (such as legal fees and broker commissions)

- Estimated costs to dismantle, remove, or restore the asset

Subsequently, the ROU asset is depreciated over the shorter of the lease term or the asset's useful life (unless ownership transfers or a purchase option is exercised).

Lessees must also test the ROU asset for impairment under FRS 102 Section 27 at each reporting date.

P&L Impact: Front-Loaded Expense Pattern

The straight-line rental expense is replaced by two charges:

- Depreciation on the ROU asset (typically straight-line)

- Interest on the lease liability (using the effective interest method)

Because the interest charge applies a constant rate to the declining balance of the liability, the interest portion is highest at the start of the lease and reduces over time. This creates a front-loaded expense pattern—total charges in early periods exceed the original straight-line rental cost, with the reverse applying later.

ACCA worked example: A 5-year warehouse lease at £137,500 per annum, discounted at 7%, produces a Year 1 P&L charge of £139,863 (depreciation £111,256 + interest £28,607), compared to £137,500 under straight-line treatment—a £2,363 reduction in profit.

Lease Modifications and Remeasurements

If lease terms change (extension exercised, rent reviews, indexation), the lease liability must be remeasured and the ROU asset adjusted. FRS 102 includes a simplification: certain modification types do not require a revised discount rate, reducing ongoing complexity compared to IFRS 16.

A modification creates a separate new lease if it adds the right to use one or more underlying assets and consideration increases commensurate with the standalone price. Otherwise, it's treated as a modification of the existing lease. Getting this classification right matters practically—only separate new leases require a fresh discount rate to be determined.

Exemptions, Simplifications and Who Is Not Affected

Two Practical Exemptions

Short-term leases:

- Lease term of 12 months or less at commencement

- Cannot contain a purchase option

- Payments expensed straight-line through P&L

Low-value assets:

- Assessed on an absolute basis (not relative to entity size)

- No specific threshold prescribed in FRS 102 (requires judgement)

- Examples that may qualify: tablets, laptops, small office furniture, telephones

- Explicitly NOT low-value: motor vehicles, vans, aircraft, land and buildings

While FRS 102 does not prescribe a monetary threshold, IFRS 16 guidance references approximately $5,000 USD (roughly £5,000) or less based on new asset value, making it a practical reference when applying judgement under FRS 102.

Who Is Not Affected

FRS 105 micro-entities continue using the existing rental expense approach with no additional disclosures or on-balance sheet recognition.

UK-listed groups preparing consolidated accounts under UK-endorsed IFRS are already subject to IFRS 16 (effective from 1 January 2019) and are not impacted by these FRS 102 amendments.

These changes primarily affect private companies, subsidiaries, LLPs, partnerships, and Section 1A small entities preparing under FRS 102.

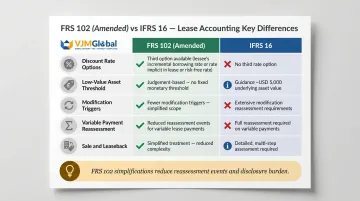

FRS 102 Simplifications vs IFRS 16

| Feature | FRS 102 (Amended) | IFRS 16 |

|---|---|---|

| Third discount rate option (OBR) | Available | Not available |

| Low-value threshold guidance | Judgement-based | |

| Modification triggers requiring revised discount rate | Reduced triggers | More extensive triggers |

| Variable payment reassessment | Fewer reassessment requirements | Reassess when cash flows change |

| Sale and leaseback | Simplified treatment | More detailed requirements |

In practice, these simplifications mean fewer reassessment events, less complex discount rate calculations, and reduced disclosure burden — allowing finance teams to focus effort where lease values are most material.

Financial Statement Impact of the New Lease Standard

Balance Sheet Transformation

Both total assets and total liabilities increase when businesses recognise ROU assets and lease liabilities. The ROU asset depreciates straight-line while the liability unwinds using the effective interest method, creating a timing mismatch that erodes net assets in the early lease years.

For businesses near statutory size thresholds (medium to large entity classification), this gross-up could trigger additional audit requirements or enhanced disclosure obligations.

Scale of impact: When IFRS 16 was introduced globally, the IASB estimated approximately US$2.18 trillion of lease liabilities would be recognised by listed companies worldwide (global IFRS 16 data, used here as a proxy for scale). The long-term financial liabilities to equity ratio increased from 59% to 74% across a sample of 1,022 companies — indicating the order of magnitude UK businesses should expect.

EBITDA and Profit Impact

EBITDA typically increases because the previous operating lease rental expense (within operating costs) is replaced by:

- Depreciation (excluded from EBITDA)

- Interest (a financing cost, also excluded from EBITDA)

RSM notes for private equity portfolio companies: "EBITDA is expected to increase" as "rent costs will be removed from operating expenses."

However, profit is front-loaded negatively in early lease years due to the higher interest charge. Over the full lease term, total expense is identical — the standard shifts when costs hit the P&L, not how much.

Covenant and Credit Risk

Recognising lease liabilities on the balance sheet directly worsens several key lending metrics:

- Gearing ratios (net debt to equity)

- Interest cover (EBITDA to interest expense)

- Net debt metrics

RSM warns that "debt covenants could be impacted by the changes to results" and advises "early conversations with lenders" to plan for covenant reporting post-transition.

Beyond lender covenants, performance-related pay, profit-sharing arrangements, and earnout structures (deferred acquisition payments tied to performance) linked to EBITDA or profit measures may also need renegotiation before the transition date.

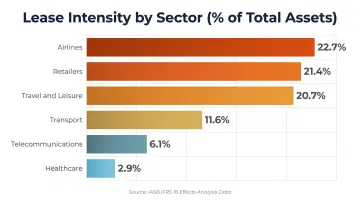

Industry-Specific Exposure

Sectors with large lease portfolios will experience the greatest impact. IASB sector analysis (based on IFRS 16 proxy data) shows lease intensity by sector:

| Sector | Lease Intensity (% of Total Assets) |

|---|---|

| Airlines | 22.7% |

| Retailers | 21.4% |

| Travel and leisure | 20.7% |

| Transport | 11.6% |

| Telecommunications | 6.1% |

| Healthcare | 2.9% |

BDO highlights that professional services firms — law firms, consultancies, and accountancy practices — are also significantly affected. Multi-site office leases sit at the core of their cost base, meaning the balance sheet impact can be material even where lease intensity percentages appear modest.

How to Prepare for FRS 102 Lease Accounting Changes

Immediate Practical Steps

Conduct a lease portfolio audit:

- Identify all lease contracts (including embedded leases in service agreements)

- Review outsourcing arrangements, equipment agreements, and property contracts

- Assess whether contracts meet the new lease definition

Gather lease documentation:

- Extract commencement dates, lease terms, payment schedules

- Identify extension/break options and variable payment clauses

- Document assumptions about reasonably certain exercise of options

Assess exemptions:

- Determine which leases qualify as short-term (≤12 months)

- Identify low-value assets eligible for exemption

- Document exemption elections on a lease-by-lease basis

Determine discount rates:

- Establish methodology for IBR or OBR calculation

- Consider engaging external specialists for discount rate determination

- Document policy choice (IBR vs OBR) and application

For businesses with large portfolios, this preparation can take several months — ideally starting at least six months before your year-end.

Communicating Changes to Stakeholders

Once the internal groundwork is in place, the next priority is managing expectations externally. Engage lenders and investors proactively:

- Explain the mechanical nature of the balance sheet increase

- Emphasise that underlying economics are unchanged

- Seek covenant amendments or waivers before financial statements are prepared

Update internal reporting frameworks:

- Revise KPI definitions to reflect new lease accounting

- Adjust remuneration calculations tied to EBITDA or profit metrics

- Communicate changes to management, boards, and shareholders

Professional Accounting Support

Professional advisors and outsourced accounting support can reduce risk during this transition, covering:

- Impact assessment and materiality analysis

- Discount rate methodology and documentation

- Accounting policy drafting and disclosure preparation

- Systems implementation and ongoing compliance

For UK businesses with multi-site portfolios or cross-border operations, the technical complexity of FRS 102 transition makes specialist support particularly valuable. VJM Global has supported over 250 UK businesses with accounting compliance, including policy drafting, disclosure preparation, and ongoing reporting under UK GAAP.

Frequently Asked Questions

How do you account for leases in the UK?

Under FRS 102 (from January 2026), lessees must recognise a Right-of-Use asset and lease liability on the balance sheet for most leases, measured at the present value of future lease payments. Short-term and low-value leases remain off-balance sheet with rental expense recognised straight-line.

What is the GAAP standard for leases?

FRS 102 Section 20 (amended 2024) governs lease accounting for most UK private companies. UK-listed groups use IFRS 16, while micro-entities follow FRS 105, which retains the simpler rental expense approach without on-balance sheet recognition.

What is the accounting treatment for finance leases?

Under the new FRS 102 model, the previous distinction between finance and operating leases is abolished for lessees. All leases (except exempt ones) are treated similarly to the former finance lease model, with an ROU asset and lease liability recognised on the balance sheet.

Do UK companies use IFRS or GAAP?

UK-listed companies preparing consolidated financial statements use UK-endorsed IFRS. Most private companies, subsidiaries, LLPs, and smaller entities use UK GAAP (FRS 102 or FRS 105), while some subsidiaries of IFRS groups qualify for FRS 101 (reduced disclosure framework).

What is the difference between IFRS 16 and ASC 842?

Both standards require on-balance sheet lease recognition, but ASC 842 (US GAAP) retains an operating vs finance lease distinction — meaning straight-line expense for operating leases. IFRS 16 uses a single lessee model with front-loaded interest and depreciation charges, along with different rules on discount rates and low-value exemptions.