Introduction

For NRIs, foreign nationals, and internationally mobile professionals with UK ties, non-domiciled (non-dom) tax status was a cornerstone of cross-border tax planning. It allowed individuals whose permanent home was outside the UK to limit their UK tax liability to income earned or brought into the country — keeping overseas wealth largely out of HMRC's reach.

That changed on 6 April 2025.

According to HMRC statistics, an estimated 73,700 individuals claimed non-domiciled taxpayer status in the 2023/24 tax year. Most of them now face a fundamentally different tax landscape.

Read on to understand what non-dom status was, how the old rules worked, what the 2025 reforms changed, and what steps individuals with cross-border ties should consider now.

Key Takeaways

- Non-dom status let UK residents with a foreign domicile pay UK tax only on UK-sourced or remitted income.

- From 6 April 2025, the remittance basis is abolished — replaced by a 4-year Foreign Income and Gains (FIG) regime for newly arriving residents.

- A Temporary Repatriation Facility (TRF) allows former remittance basis users to bring overseas funds into the UK at 12% (2025–27) or 15% (2027/28).

- UK inheritance tax now follows residence: long-term residents (10+ of the last 20 years) face IHT on worldwide assets.

- Anyone affected should seek professional cross-border tax advice now, not after the window closes.

What Was UK Non-Dom Status?

Non-dom status was a UK tax classification for individuals living in the UK whose permanent home (domicile) was legally considered to be in another country. It had nothing to do with nationality or citizenship.

As HMRC's RDR1 guidance explains, domicile is a legal concept — generally the country where an individual has their permanent home. A person can only have one domicile at any time.

How Domicile Is Established

Domicile works differently from residency:

- Domicile of origin — assigned at birth, typically based on the father's domicile at the time of birth

- Domicile of choice — can only be acquired by physically residing in another country and demonstrating a clear, settled intention to remain there permanently or indefinitely

- Changing domicile — difficult to achieve; moving abroad temporarily or for work does not qualify

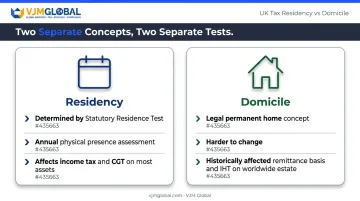

Domicile vs. Residency: A Critical Distinction

These two concepts are separate and affect different tax obligations:

| Concept | How It's Determined | What It Affects |

|---|---|---|

| Residency | Annual physical presence test (Statutory Residence Test) | Income tax, CGT on most assets |

| Domicile | Legal permanent home, harder to change | Historically: remittance basis, IHT on worldwide estate |

It's worth clarifying that non-dom status and non-resident status are not interchangeable. A non-dom lived in the UK but retained a foreign domicile. A non-resident, by contrast, has not met the SRT thresholds at all and is taxed only on UK-source income — a distinct classification with its own set of rules.

How the Old Non-Dom Tax Rules Worked

Under the pre-2025 system, non-dom UK residents had a choice each tax year:

- Arising basis — pay UK tax on all worldwide income and gains (the default)

- Remittance basis — pay UK tax only on UK-source income and any foreign income or gains actually brought into the UK; overseas income left abroad was not taxed in the UK

The remittance basis had to be claimed annually on a Self Assessment return. If no claim was made, the arising basis applied automatically.

The Remittance Basis Charge

The remittance basis was not free for long-term residents. Once an individual had been UK resident for a qualifying period, they had to pay an annual charge to access it:

- £30,000 per year — for those resident in at least 7 of the previous 9 tax years

- £60,000 per year — for those resident in at least 12 of the previous 14 tax years

- Claiming the remittance basis also meant losing the personal income tax allowance and the CGT annual exempt amount

The Deemed Domicile Rule (Pre-2025)

From April 2017, non-doms who had been UK resident for 15 of the previous 20 tax years became deemed domiciled in the UK. At that point, they could no longer claim the remittance basis and became liable to UK tax on worldwide income, gains, and their entire estate for IHT purposes.

Under the old IHT rules, non-doms were only liable on UK-sited assets until they reached that 15-year threshold. This made the UK attractive to wealthy, internationally mobile individuals who managed their UK residence carefully.

The April 2025 Non-Dom Rule Changes Explained

From 6 April 2025, domicile has been removed from the UK tax system as a determining factor for income tax, CGT, and IHT. The remittance basis cannot be claimed for any tax year from 2025/26 onwards. These changes are enacted through the Finance Act 2025.

The system is now entirely residence-based.

The 4-Year Foreign Income and Gains (FIG) Regime

The FIG regime is the replacement for the remittance basis — but it is narrower and time-limited.

Eligibility requirements:

- Must be UK tax resident

- Must be within the first four tax years of UK residence

- Must have been non-UK resident for at least 10 consecutive tax years immediately before arriving

How it works:

- Eligible individuals can elect to pay no UK tax on foreign income and gains for up to four years

- Those funds can be freely brought into the UK without triggering a UK tax charge

- The election must be made for each year it is to apply

For individuals already in the UK on 6 April 2025:

- Resident for fewer than four years (after the required 10-year non-residence period): still eligible for the FIG regime for remaining years

- Resident for more than four years: fully taxable on worldwide income and gains from 6 April 2025

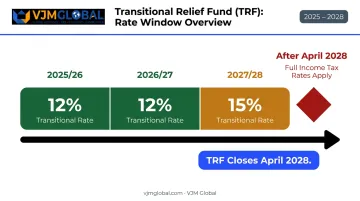

The Temporary Repatriation Facility (TRF)

Former remittance basis users may have accumulated significant untaxed overseas income and gains. The TRF offers a structured window to bring those funds into the UK at reduced rates:

| Tax Year | TRF Rate |

|---|---|

| 2025/26 | 12% |

| 2026/27 | 12% |

| 2027/28 | 15% |

The TRF closes after 2027/28. After that, any previously untaxed foreign income or gains remitted to the UK will be subject to full income tax rates. With the rate rising from 12% to 15% in 2027/28 — and full rates applying after that — those with significant offshore holdings have a limited and narrowing opportunity to act.

Inheritance Tax: From Domicile to Residence

IHT has shifted entirely to a residence-based test. Key points under the new framework:

- UK-sited assets remain subject to IHT regardless of the owner's residence status — this has not changed

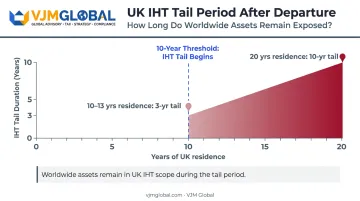

- Non-UK assets are only subject to UK IHT once a person qualifies as a long-term UK resident — defined as being UK resident in at least 10 of the last 20 tax years

- The IHT tail: individuals who leave the UK after meeting the long-term residence threshold can remain within the UK IHT net on worldwide assets for up to 10 years after departure, depending on how many years of UK residence they accumulated

The tail period is tapered based on total UK residence:

- 10–13 years of UK residence → 3-year IHT tail after departure

- 20 years of UK residence → 10-year IHT tail after departure

This tapering is frequently overlooked in departure planning.

Who Is Most Affected and Key Planning Considerations

Three groups face the most immediate exposure:

- Newly arriving high-net-worth individuals — those who previously planned around the remittance basis now have a narrower four-year window under the FIG regime, with no extension

- Long-term UK residents approaching or past the 10-year IHT threshold — worldwide assets are now in scope, and departure no longer immediately ends IHT exposure

- Former remittance basis users with untaxed offshore income — the TRF window is open until April 2028, after which full rates apply

Time-Sensitive Decisions to Address Now

- TRF utilisation — designate and repatriate pre-April 2025 foreign income and gains at 12% before the rate rises and the facility closes

- IHT restructuring — review offshore asset structures before crossing the 10-year long-term residence threshold

- Overseas Workday Relief (OWR) — retained and simplified, OWR applies to qualifying new residents working both in and outside the UK — capped at the lower of £300,000 or 30% of qualifying employment income annually

- Departure planning — anyone considering leaving the UK should map out their IHT tail exposure well in advance, not after the move

Each of these decisions carries a hard deadline — most of the transitional windows close by April 2028 at the latest, and some are already narrowing. VJM Global advises NRIs, foreign investors, and UK-connected businesses on cross-border tax obligations, including DTAA interpretation, FEMA compliance, and multi-jurisdiction structuring. For individuals reassessing their position under the new residence-based framework, specialist input before those windows close is the difference between structured planning and a missed opportunity.

Common Misconceptions About Non-Dom Tax

Several widely held assumptions about non-dom tax are no longer accurate — and acting on them can be costly. Here are three that come up most often.

"The rules were just tweaked." This understates what changed. Domicile no longer determines income tax, CGT, or IHT exposure. From April 2025, simply holding non-dom status provides no tax advantage unless the FIG regime specifically applies to you.

"Non-dom and non-resident are the same thing." They're not, and the distinction matters. A non-dom lived in the UK but held a foreign domicile. A non-resident has not met the Statutory Residence Test thresholds and is taxed only on UK-source income. Separate statuses, separate tests, separate consequences.

"Leaving the UK ends your IHT exposure." Under the new rules, long-term residents remain within the UK IHT net on worldwide assets for up to 10 years after departure. Many people planning to leave are unaware of this tail — and by the time they realise it, the planning window may have already closed.

Conclusion

The UK non-dom regime, which existed for well over a century, has been replaced by a residence-based system that applies uniformly from April 2025. The new 4-year FIG regime provides a structured entry window for newly arriving residents, but after that window closes, worldwide income and gains are fully taxable — the same as any long-term UK resident.

For individuals with international income, offshore assets, or upcoming changes in UK residency status, the decisions that matter most are time-sensitive: the TRF closes in April 2028, IHT exposure builds year by year, and restructuring options narrow with every year of delay.

For NRIs, OCIs, and internationally mobile professionals navigating the India-UK tax intersection, getting the sequencing right — remittances, offshore trusts, residency timing — requires specialist input. VJM Global's international tax team has advised 250+ UK-based clients on exactly these crossover issues. Reach out at info@vjmglobal.com or visit vjmglobal.com/contact-us to discuss your specific situation.

Frequently Asked Questions

Do non-domiciled individuals have to pay UK tax?

Yes. Non-domiciled UK residents always paid UK tax on UK-source income. Prior to April 2025, they could elect the remittance basis so that foreign income and gains were only taxed if brought into the UK. From April 2025, those not eligible for the FIG regime are taxed on worldwide income like any other UK resident.

Do I have to pay tax in the UK if I am a non-resident?

Non-residents are generally taxed only on UK-source income and gains — not on foreign income. The Statutory Residence Test determines residency status each tax year and differs entirely from non-dom status, which relates to domicile rather than physical presence.

How long do you have to stay outside the UK to be considered non-domiciled?

Non-dom status was never determined by time spent outside the UK — it depended on where your permanent home, or domicile, was legally established. For the new FIG regime, eligibility requires at least 10 consecutive years of non-UK residence before arriving in the UK.

What replaced non-dom status in the UK after April 2025?

The domicile-based remittance basis has been replaced by a residence-based system. Newly arriving residents may access the 4-year FIG regime; after that, they are taxed on worldwide income and gains like any other UK resident.

What is the Temporary Repatriation Facility (TRF)?

The TRF is a transitional relief available for three tax years from 6 April 2025, allowing former remittance basis users to bring previously untaxed overseas income and gains into the UK at a flat rate of 12% in 2025/26 and 2026/27, rising to 15% in 2027/28 — rather than paying full income tax rates.

What are the inheritance tax implications for long-term UK residents after the non-dom changes?

Individuals UK resident for at least 10 of the last 20 tax years are now subject to UK IHT on worldwide assets, not just UK assets. This exposure can continue for up to 10 years after leaving the UK, depending on total years of UK residence — so those approaching the 10-year threshold should review their estate position before departing.