Introduction

The 2025-26 financial year brings some of the most complex corporate tax conditions UK businesses have faced in years. The October 2024 Autumn Budget introduced threshold changes, dividend tax adjustments, and capital allowance reductions — all landing alongside full Pillar Two global minimum tax compliance.

For UK-based SMEs, large corporates, owner-directors, finance managers, and multinationals with UK operations, the stakes of getting this wrong are higher than usual.

This guide covers the confirmed rates for 2025-26, key Budget impacts, capital allowance opportunities, Pillar Two obligations, and practical steps to prepare your business.

Key Takeaways

- Main corporation tax rate remains 25% for profits over £250,000; small profits rate stays 19% for profits under £50,000

- November 2025 Budget increased dividend tax by 2 percentage points across all rates

- Autumn Budget also cut writing down allowances from 18% to 14% on the special rate pool

- Permanent full expensing allows 100% first-year deductions on qualifying plant and machinery

- Pillar Two global minimum tax now fully applies to groups with €750M+ revenue, including UTPR from December 2024

- Making Tax Digital (MTD) mandates quarterly reporting for self-employed individuals and landlords from April 2026

UK Corporate Tax Rates for 2025-26: What's Confirmed

The Dual-Rate Structure Continues

The dual-rate structure confirmed for FY2025 (1 April 2025) carries forward unchanged into FY2026, giving businesses a stable baseline for medium-term tax planning.

| Rate | Applies To | Threshold |

|---|---|---|

| 19% (small profits rate) | Companies with augmented profits below £50,000 | Stable since April 2023 |

| 25% (main rate) | Companies with profits exceeding £250,000 | Confirmed for FY2025 and FY2026 |

| 19%–25% (marginal relief) | Companies with profits between £50,000–£250,000 | Sliding scale applies |

HMRC Corporation Tax statistics show approximately 70% of UK companies qualify for the small profits rate — making 19% the effective rate for the majority of small businesses.

The Marginal Relief Band

Companies with profits between £50,000 and £250,000 fall into the marginal relief band, where a sliding scale applies. The effective tax rate gradually increases from 19% to 25% as profits rise through this band.

How marginal relief works:

- Creates an effective marginal tax rate of approximately 26.5% within the band

- Can catch growing businesses off guard as they cross thresholds

- Calculated on "augmented profits" (including dividends from non-group companies)

For businesses approaching the £250,000 threshold, modelling profit forecasts against marginal relief calculations before year-end can avoid a surprise tax bill.

Associated Companies Rule

Both profit limits (£50,000 and £250,000) must be divided by the total number of active associated companies worldwide. Smaller corporate groups often find themselves pushed into the main rate band as a result — even when individual company profits are modest.

Example: A business with three associated companies faces adjusted thresholds of £16,667 (small profits limit) and £83,333 (main rate threshold), significantly reducing the benefit of the lower rate.

Patent Box Relief: An Overlooked Incentive

The Patent Box scheme offers a 10% effective tax rate on profits attributable to qualifying patents. Innovation Tax research shows that Patent Box relief saved businesses over £1.2 billion in 2023-24, yet remains underutilised by many eligible companies.

Key eligibility criteria:

- Company must own or exclusively license qualifying patents

- Must have undertaken qualifying development on the patented invention

- Relief applies to profits from sales of patented products or patent licensing income

Key Changes from the November 2025 Budget

Dividend Tax Rate Increase

Basic rate dividend tax rose from 8.75% to 10.75%, whilst the higher rate increased from 33.75% to 35.75%. This 2 percentage point increase directly impacts owner-directors who use dividend income as part of their remuneration strategy.

Impact example:

- An owner-director taking £50,000 in dividends (after the £500 allowance)

- Higher rate taxpayer now pays £17,700 instead of £16,700

- Additional £1,000 annual tax cost

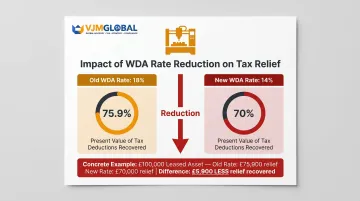

Writing Down Allowance Reduction

The Writing Down Allowance (WDA) on the main rate pool fell from 18% to 14%, reducing the present value of future tax deductions for assets not qualifying for full expensing. The OBR estimates this change will raise approximately £285 million annually by 2029-30.

Government analysis shows the total value of tax deductions falls from approximately 75.9% to 70% of investment cost over the asset's life. Businesses with significant capital asset portfolios will feel this reduction most acutely.

New 40% First-Year Allowance for Leased Assets

The Budget introduced a 40% first-year allowance for qualifying plant and machinery acquired on or after 1 April 2026 that is subsequently leased to third parties. This partially offsets the WDA cut for leasing businesses.

Eligibility:

- Applies to new (not second-hand) plant and machinery

- Asset must be leased to unconnected parties

- Provides upfront relief before reverting to the 14% WDA

Fiscal Drag from Threshold Freeze

The freeze of income tax and National Insurance thresholds through 2031 creates fiscal drag, gradually increasing the effective tax burden on labour. The OBR projects this will raise £40.3 billion cumulatively by 2029-30.

For employers, this has a direct cost implication: as frozen thresholds erode employees' net pay, wage pressure increases. Businesses should factor higher gross salary expectations into workforce planning over the next five years.

Stamp Duty Relief for New Listings

A three-year stamp duty holiday on shares applies to newly listed companies on the London Stock Exchange. Companies listing on or after 1 April 2025 benefit from 0% stamp duty on share transactions for three years, reducing the cost of raising capital through public markets.

Making Tax Digital Expansion

From April 2026, Making Tax Digital for Income Tax applies to a broader group. Affected individuals must use HMRC-compatible software to submit quarterly reports and an annual return.

Who this affects:

- Self-employed individuals with income above £20,000

- Landlords with property income above £20,000

- Contractors and sole traders working with UK businesses

Penalties for late or non-compliant submissions apply from day one of the new regime. Businesses working with self-employed contractors should confirm their partners are set up on qualifying software before April 2026.

Capital Allowances and Full Expensing: Maximising Investment Relief

What Qualifies for Full Expensing

Since Autumn Statement 2023, companies can immediately deduct 100% of qualifying plant and machinery expenditure in the year of purchase. Full expensing is now permanent, removing previous time-limited incentive deadlines that pressured businesses to rush investment decisions.

Key requirements:

- Applies to new (not second-hand) main rate plant and machinery

- Must be used in the business (not leased out)

- Provides immediate cash flow benefit by reducing tax in the year of purchase

Annual Investment Allowance (AIA)

The AIA is permanently set at £1 million, covering plant, machinery, and certain integral features. Smaller businesses that don't require full expensing often find the AIA sufficient for all capital spend.

AIA vs Full Expensing:

- AIA covers second-hand assets; full expensing requires new assets

- AIA applies to a broader range of assets including integral features

- Full expensing applies only to main rate pool items

50% First-Year Allowance for Special Rate Assets

A 50% first-year allowance applies to special rate assets including long-life assets (expected life over 25 years) and integral features such as heating, cooling, and electrical systems. This provides meaningful upfront relief alongside the full expensing regime.

Impact of the WDA Reduction

Not all assets benefit from full expensing. For main rate pool assets that don't qualify — primarily leased equipment — the WDA cut from 18% to 14% directly reduces the real value of tax deductions. The OBR estimates the present value of deductions falls from 75.9% to approximately 70% of investment cost.

Practical impact:

- £100,000 of leased equipment previously generated £75,900 in present-value deductions

- Now generates approximately £70,000 in present-value deductions

- Represents £5,900 less tax relief per £100,000 invested

How to Optimise Your Capital Expenditure Timing

To get the most from the current regime:

- Identify which planned assets qualify for full expensing versus WDA treatment

- Prioritise purchases of new qualifying plant and machinery where possible

- Time purchases strategically ahead of any future changes to the capital allowance regime

Pillar Two and Global Minimum Tax: Who Is Affected?

Scope of Application

UK groups and foreign groups with UK operations face Pillar Two obligations if they have annual consolidated revenue of €750 million or more. This threshold targets large multinationals, but the compliance workload is considerable — and errors carry real financial risk.

Three UK Pillar Two Mechanisms

| Mechanism | Who It Applies To | Purpose |

|---|---|---|

| Multinational Top-up Tax (MTT/IIR) | UK-headquartered groups with low-taxed foreign operations | Ensures foreign profits are taxed at minimum 15% |

| Domestic Minimum Top-up Tax (DMTT/QDMTT) | UK operations taxed below 15% | Ensures the UK collects top-up tax on domestic activity |

| Undertaxed Profits Rule (UTPR) | Groups where other jurisdictions haven't collected minimum tax | Allocates residual tax; effective from 31 December 2024 |

Understanding which mechanism applies to your group is the starting point. From there, all in-scope groups face four categories of compliance obligation.

Compliance Obligations

In-scope groups must:

Registration:

- Register with HMRC within six months of first in-scope accounting period

- Provide details of all group entities and jurisdictions

Annual filings:

- Submit Global Information Return (GIR) within 15-18 months of period end

- File self-assessment return and pay any top-up tax

Recordkeeping:

- Maintain records for nine years

- Document effective tax rate calculations for each jurisdiction

Late or inaccurate filings attract financial penalties, and non-compliance can trigger HMRC enquiries across the entire group.

Special Tax Regimes and Sector-Specific Developments

Energy Profits Levy Update

The Energy Profits Levy (EPL) rate increased to 38% from 1 November 2024 (up from 35%). The 29% investment allowance was removed from the same date, and the levy is extended to 31 March 2030.

An Energy Security Investment Mechanism (ESIM) could end the EPL early if oil and gas prices fall below set trigger levels (£55/barrel for oil, 45p/therm for gas) for two consecutive quarters.

Diverted Profits Tax Repeal

Diverted Profits Tax (DPT) is being repealed for accounting periods beginning on or after 1 January 2026. The replacement is a corporation tax charge on Unassessed Transfer Pricing Profits (UTPP). Key details of the new regime:

- Rate set at 6 percentage points above standard (currently 31%)

- New gateway tests apply — materially different from DPT's existing tests

- Businesses with prior DPT analyses must revisit their positions under the UTPP framework

QAHC Regime Consultation

Beyond the DPT repeal, the Autumn Budget 2025 also flagged structural changes ahead for investment vehicles. The government confirmed it will consult on legislative changes to the Qualifying Asset Holding Company (QAHC) regime.

Fund managers and investors should monitor HMRC updates closely. Proposed changes could affect:

- Tax treatment of capital gains

- Treatment of interest income

- Distribution rules from these vehicles

How UK Businesses Should Prepare for 2025-26

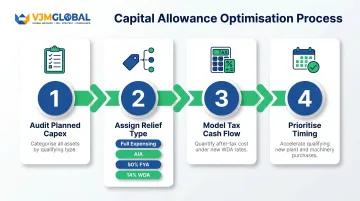

Conduct a Capital Allowance Review

Audit planned capital expenditure to identify assets eligible for full expensing versus main rate pool treatment. Model the tax cash flow impact of the reduced 14% WDA, particularly for businesses with significant leased asset bases.

Action steps:

- Categorise planned purchases by relief type (full expensing, AIA, 50% FYA, or WDA)

- Quantify the after-tax cost difference under the new WDA rate

- Prioritise qualifying new plant and machinery purchases where timing is flexible

Reassess Owner-Director Remuneration Strategy

The 2 percentage point dividend tax increase warrants a review of the salary-dividend mix. Quantify the additional tax cost and explore whether pension contributions or other tax-efficient remuneration options improve overall outcomes.

Consider:

- Increasing salary (subject to National Insurance costs)

- Employer pension contributions (corporation tax deductible, no income tax or NI)

- Timing dividend payments to manage marginal rates

Prepare for Making Tax Digital (April 2026)

Businesses with self-employed directors or connected landlords should identify software readiness gaps and implement compliant reporting systems before April 2026 to avoid penalties.

Preparation checklist:

- Verify which individuals in the business fall under MTD requirements

- Source and test compatible accounting software

- Establish quarterly submission processes

Seek Specialist Cross-Border Tax Advice

For UK businesses with international operations — particularly those expanding into India — domestic tax planning rarely tells the whole story. Cross-border structures require advisors who understand both sides of the equation. VJM Global works with 250+ UK businesses on international tax compliance, India entry strategy, and FDI advisory.

Key areas to address with a cross-border advisor:

- Review treaty positions and transfer pricing obligations under current HMRC guidance

- Assess India entry structure (branch, subsidiary, or LLP) for tax efficiency

- Align UK compliance timelines with Indian regulatory filing deadlines

Frequently Asked Questions

What is the UK corporation tax rate for 2025-26?

The main rate is 25% for companies with profits above £250,000 and 19% for companies with profits below £50,000. Marginal relief applies between those thresholds for the financial year beginning 1 April 2025.

When did the UK corporate tax rate change to 25%?

The 25% main rate took effect from 1 April 2023, announced in the March 2021 Spring Budget by then-Chancellor Rishi Sunak. This ended six years of flat-rate 19% corporation tax that had been in place since April 2017.

How does marginal relief work for 2025-26?

Companies with profits between £50,000 and £250,000 pay an effective rate between 19% and 25%, calculated using HMRC's marginal relief formula. The thresholds are divided by the number of associated companies, so a group with two associates sees limits of £25,000 and £125,000 respectively.

What is the 60% trap?

The 60% trap affects director-shareholders earning between £100,000 and £125,140, where the gradual withdrawal of the personal allowance creates an effective 60% marginal income tax rate. For owner-managed businesses, this makes the salary-versus-dividend split a critical part of annual tax planning — extracting profits via dividends below that threshold can significantly reduce the overall tax burden.

What is permanent full expensing and how does it help businesses?

Permanent full expensing allows companies to immediately deduct 100% of qualifying plant and machinery costs against taxable profits in the year of purchase. This reduces the effective cost of investment and improves cash flow compared to deducting costs gradually via writing down allowances.

Which companies are affected by Pillar Two in the UK?

Pillar Two rules apply to multinational or large domestic groups with consolidated annual revenues of €750 million or more. These groups must pay a top-up tax where their effective tax rate in any jurisdiction falls below 15%.