The stakes are particularly high for businesses with profits between £50,001 and £250,000, where the effective marginal rate reaches 26.5%—higher than both the small profits rate and the headline main rate. Add in the associated companies rule, and what looks like a straightforward tax calculation quickly becomes a multi-layered challenge.

This guide covers everything UK businesses need to know for the 2025-26 tax year: the current rates, how marginal relief works, threshold calculations, special regimes, and practical planning strategies to minimise your corporation tax bill legally.

TLDR: UK Corporate Tax Rates 2025-26 at a Glance

- Small Profits Rate of 19% applies to companies with taxable profits of £50,000 or less

- Main Rate of 25% applies to companies with taxable profits above £250,000

- Marginal Relief applies between £50,001 and £250,000, producing a 26.5% marginal rate on profits within that band

- Associated companies reduce both thresholds proportionally — divided by the total number of related entities under common control

- No rate changes are planned for the financial year beginning 1 April 2026 — current rates are safe to use for forward planning

UK Corporation Tax Rates 2025-26: The Complete Rate Breakdown

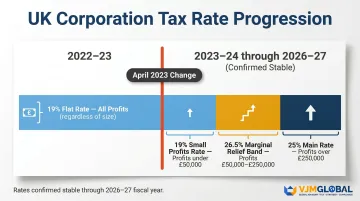

The three-tier rate structure introduced from 1 April 2023 continues unchanged into 2025-26. Companies now pay either 19% (small profits rate), 25% (main rate), or somewhere in between via marginal relief.

"Taxable profits" (also called "augmented profits") includes trading profits, investment income, and chargeable gains after allowable deductions. This figure determines which rate band applies to your company.

Historical Rate Progression

| Rate | 2022-23 | 2023-24 | 2024-25 | 2025-26 | 2026-27 |

|---|---|---|---|---|---|

| Small Profits Rate (under £50,000) | -- | 19% | 19% | 19% | 19% |

| Main Rate (over £250,000) | -- | 25% | 25% | 25% | 25% |

| Flat Rate (all profits) | 19% | -- | -- | -- | -- |

| Lower Limit | -- | £50,000 | £50,000 | £50,000 | £50,000 |

| Upper Limit | -- | £250,000 | £250,000 | £250,000 | £250,000 |

The 2023 shift from a single 19% flat rate to a dual-rate structure is the key reference point for multi-year tax planning — any company crossing the £50,000 profits threshold immediately faced a higher effective rate. Rates are confirmed identical through 2026-27, giving businesses a stable basis for forward planning.

Worked Example: Small Profits Rate

A company with £42,000 in taxable profits (below the £50,000 threshold):

- Taxable profit: £42,000

- Corporation tax rate: 19%

- Corporation tax due: £42,000 × 19% = £7,980

When calculating taxable profit:

- Add back non-allowable costs (client entertainment, depreciation)

- Deduct capital allowances (Annual Investment Allowance, full expensing)

- Include all trading profits, investment income, and chargeable gains

Special Rates for Investment Vehicles and Sectors

The rates above apply to standard UK companies. Certain investment vehicles and regulated sectors operate under separate regimes entirely.

Unit trusts and OEICs pay a fixed 20% rate regardless of profit level.

Ring fence regime for oil and gas extraction combines multiple layers:

- Ring Fence Corporation Tax: 30%

- Supplementary Charge: 10%

- Energy Profits Levy: 38% (increased from 35% in November 2024)

- Total headline rate: 78%

The Energy Profits Levy applies until 31 March 2030, with the investment allowance removed for expenditure from 1 November 2024.

Banking surcharge of 3% applies to profits exceeding £100 million (reduced from 8% with a £25 million threshold in April 2023).

How Marginal Relief Works (and How to Calculate It)

Rather than jumping abruptly from 19% to 25% at the £50,000 threshold, HMRC uses a formula to create a smooth, gradual increase across the £50,001–£250,000 band.

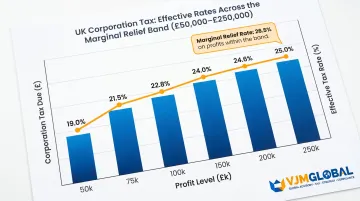

The effective marginal rate within this band is 26.5%—meaning every extra pound of profit in this range is taxed at 26.5%, even though the headline main rate is 25%.

The HMRC Formula

Corporation Tax = (Profits × 25%) − [(3/200) × (£250,000 − Taxable Profits)]

Where:

- 3/200 = Standard fraction (0.015)

- £250,000 = Upper limit

- Taxable Profits = Your company's augmented profits

This 3/200 fraction creates the graduated increase from 19% to 25% across the full £200,000 profit range (£50,001–£250,000).

Detailed Worked Example

Company with £150,000 taxable profits:

- Calculate CT at main rate: £150,000 × 25% = £37,500

- Calculate marginal relief: (3/200) × (£250,000 − £150,000) = (3/200) × £100,000 = £1,500

- Final tax liability: £37,500 − £1,500 = £36,000

- Effective rate: £36,000 ÷ £150,000 = 24.0%

Effective Rates Across the Band

| Taxable Profits | CT at 25% | Marginal Relief | Final CT | Effective Rate |

|---|---|---|---|---|

| £50,000 | £12,500 | £3,000 | £9,500 | 19.0% |

| £75,000 | £18,750 | £2,625 | £16,125 | 21.5% |

| £100,000 | £25,000 | £2,250 | £22,750 | 22.8% |

| £150,000 | £37,500 | £1,500 | £36,000 | 24.0% |

| £200,000 | £50,000 | £750 | £49,250 | 24.6% |

| £250,000 | £62,500 | £0 | £62,500 | 25.0% |

HMRC provides an online Marginal Relief Calculator for precise figures based on your specific profit level and associated company count.

Short Accounting Periods

The limits shown above assume a standard 12-month accounting period. Both the £50,000 lower limit and £250,000 upper limit are proportionately reduced for shorter periods. A six-month period, for example, applies a £25,000 lower limit and £125,000 upper limit.

No Cliff Edge: Higher Profits Always Mean More After-Tax Income

Companies with profits just above £50,000 are not financially worse off than those at exactly £50,000. While the effective rate increases, absolute profit after tax continues to rise—there is no "cliff edge" penalty. That said, careful planning within this band can still reduce your effective rate.

The Associated Companies Rule: How It Affects Your Thresholds

Both the £50,000 lower limit and £250,000 upper limit are divided equally by the total number of "associated companies" a business has.

Under CTA 2010, Section 449, a company is "associated" if one company controls the other or both are under common control. Control encompasses voting power, share capital ownership, or entitlement to assets on winding up.

Concrete Example: Three Associated Companies

If a director controls three companies (including the one being assessed):

- Lower limit: £50,000 ÷ 3 = £16,667

- Upper limit: £250,000 ÷ 3 = £83,333

A company in this group with £90,000 in profits pays the full 25% main rate rather than benefiting from marginal relief. Without the associated companies rule, it would sit comfortably within the marginal relief band.

Dormant Company Exclusion

Under CTA 2010, Section 25(5), a company is excluded from the associated company count if it has not carried on any trade or business during the relevant accounting period.

Key considerations:

- Pure holding companies that merely hold shares and receive/distribute dividends are excluded from the count

- Companies receiving interest on bank accounts or other investment income are treated as carrying on a business and must be included

- Associated companies include UK and overseas entities regardless of tax residence

Planning Implications

Business owners operating multiple companies under a common holding structure should evaluate whether consolidating, restructuring, or separating activities is beneficial. A position that looks like small profits in isolation can become a main rate liability once associated companies are counted.

This is particularly relevant for UK companies with overseas subsidiaries — an Indian entity under common control, for example, counts toward the associated companies total and compresses the thresholds. VJM Global's tax advisory team works with UK businesses that have cross-border or multi-entity structures to assess where they stand and how their group composition affects their corporation tax position.

Special Corporation Tax Regimes to Be Aware Of

Special Corporation Tax Regimes in 2025-26

Five special regimes sit outside the standard 19%/25% structure:

Oil and Gas Ring Fence Companies

| Component | Rate |

|---|---|

| Ring Fence Corporation Tax | 30% |

| Supplementary Charge | 10% |

| Energy Profits Levy (from Nov 2024) | 38% |

| Total headline rate | 78% |

The Energy Profits Levy was raised from 35% to 38% on 1 November 2024, with the sunset clause extended to 31 March 2030. The 29% investment allowance was abolished for expenditure from 1 November 2024, though the decarbonisation investment allowance remains.

Banking Sector Surcharge

Banks pay a 3% surcharge on profits above £100 million in addition to the standard corporation tax rate. This was reduced from 8% (with a £25 million threshold) in April 2023.

Real Estate Investment Trusts (REITs)

UK REITs are exempt from corporation tax on qualifying property rental income and gains. Property Income Distributions carry a 20% withholding tax, rising to 22% from April 2027 when the basic rate of income tax increases.

Patent Box

Companies can apply a 10% effective corporation tax rate to profits from patented innovations. Companies must own or exclusively licence-in patents granted by the UK IPO or European Patent Office, and the company must have undertaken qualifying development.

Beyond these domestic regimes, large multinationals face a separate layer of international rules.

Pillar Two Global Minimum Tax

The UK has implemented OECD Pillar Two legislation for multinational groups with annual revenue of €750 million or more:

| Mechanism | UK Name | Effective Date |

|---|---|---|

| Income Inclusion Rule (IIR) | Multinational Top-up Tax (MTT) | 31 December 2023 |

| Qualifying Domestic Minimum Top-up Tax (QDMTT) | Domestic Top-up Tax (DTT) | 31 December 2023 |

| Undertaxed Profits Rule (UTPR) | Within MTT | 31 December 2024 |

These rules require a minimum effective tax rate of 15%. Groups must file GIR returns within 18 months of the first accounting period end, then 15 months for subsequent periods.

Tax Planning Strategies to Minimise Your 2025-26 Corporation Tax Bill

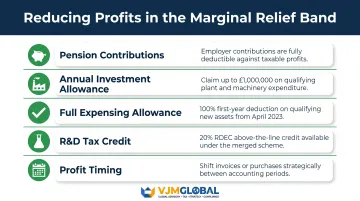

Profit Band Strategy: Maximise Allowable Deductions

Businesses with profits projected to fall within the marginal relief band (£50,001–£250,000) should review their position before year-end.

Allowable deductions that reduce taxable profits:

- Pension contributions (employer contributions are deductible)

- Capital allowances including the £1,000,000 Annual Investment Allowance on qualifying plant and machinery

- Research & Development relief at 20% RDEC rate under the merged scheme

- Timing of invoices or large purchases to shift profits between periods

The 100% full expensing allowance (introduced April 2023) lets companies deduct the full cost of qualifying main rate plant and machinery in the year of purchase. Key conditions: assets must be new and unused, purchased on or after 1 April 2023, and cannot be cars. A 50% first-year allowance applies to special rate assets.

Salary vs Dividend Optimisation

Directors who are also shareholders must weigh the interaction of corporation tax, employer NI, and dividend tax.

2025-26 rates:

- Employer NI: 15% (up from 13.8%) on earnings above £5,000/year (down from £9,100)

- Dividend tax: 8.75% (basic rate), 33.75% (higher rate), 39.35% (additional rate)

- Dividend allowance: £500

Most directors set salary at the secondary NI threshold (£5,000) or personal allowance (£12,570), extracting remaining profits as dividends. The higher 25% corporation tax rate means retained earnings are less tax-efficient than before April 2023 for large-profit companies.

The 60% tax trap affects directors with adjusted net income between £100,000 and £125,140. The personal allowance of £12,570 reduces by £1 for every £2 earned above £100,000, creating an effective 60% marginal income tax rate (40% higher rate + 20% from allowance loss). This makes salary extraction above £100,000 particularly inefficient.

Timing of Capital Expenditure

Companies in the marginal relief band can use large capital purchases before year-end to bring taxable profits below £250,000 (or even below £50,000).

The 100% full expensing allowance makes this particularly powerful. A company with £260,000 projected profit purchasing £50,000 of qualifying equipment before year-end reduces taxable profit to £210,000, moving from the 25% main rate into the marginal relief band—saving approximately £3,250 in corporation tax.

R&D Tax Relief Under the Merged Scheme

The merged R&D expenditure credit (RDEC) scheme provides a 20% taxable above-the-line credit for accounting periods beginning on or after 1 April 2024. This works out to a net benefit of approximately 15% after corporation tax at 25%.

The Enhanced R&D Intensive Support (ERIS) scheme provides additional support for R&D-intensive loss-making SMEs with an intensity threshold of 30% of total expenditure.

Group Relief and Loss Utilisation

UK group companies can surrender trading losses to profitable group members, reducing their corporation tax liability.

Loss restriction: Carried-forward losses can only offset 50% of profits in excess of £5 million (the "deductions allowance"). A single £5 million deductions allowance is available per group.

UTPP Replacing Diverted Profits Tax

The strategies above apply primarily to domestic UK companies. For multinational groups, a separate compliance change takes effect shortly.

The Unassessed Transfer Pricing Profits (UTPP) charge replaces the Diverted Profits Tax for accounting periods beginning on or after 1 January 2026. Multinational groups with UK operations must review transfer pricing compliance ahead of this change.

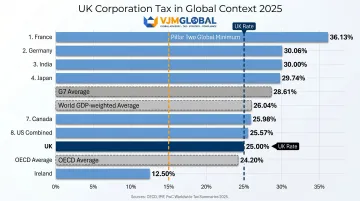

UK Corporate Tax in a Global Context: How Does the UK Rate Compare?

The UK's 25% main rate sits slightly above the global average but remains competitive within the G7.

Global Comparison

| Jurisdiction | Headline Rate |

|---|---|

| Worldwide average (unweighted, 181 jurisdictions) | 23.58% |

| Worldwide average (GDP-weighted) | 26.04% |

| G7 average | 28.61% |

| OECD average | 24.20% |

| France | 36.13% |

| Germany (combined) | 30.06% |

| Japan | 29.74% |

| Canada | 25.98% |

| United Kingdom | 25.00% |

| United States (combined federal + state) | 25.57% |

| India | 30.00% |

| Ireland | 12.50% |

In practical terms, the UK sits roughly in line with the US combined rate (25.57%) while offering a meaningful discount to France, Germany, and Japan — which matters when multinationals are choosing where to locate regional headquarters or IP holding structures.

Competitive Implications for Foreign Investment

The UK's territorial-leaning system means the effective rate for multinational groups is often lower than the headline 25%. Key features include:

- Dividend exemptions for qualifying foreign dividends

- Broad double taxation treaty network (130+ treaties)

- QAHC regime for investment fund holding companies

- Patent Box 10% rate for qualifying IP profits

For UK-India business structures, the UK's 25% rate compares favourably to India's 30% headline rate (or approximately 25.17% effective rate under Section 115BAA for domestic companies opting for concessional treatment). The UK-India Double Taxation Convention provides reduced withholding rates on dividends (10–15%), interest, and royalties (capped at 15%).

For UK businesses looking to use these treaty provisions effectively, structuring the holding entity and profit repatriation route correctly from the outset is critical — this is where specialist cross-border tax advice pays for itself. VJM Global has supported 250+ UK businesses navigating the UK-India corridor, covering entity setup, transfer pricing compliance, and treaty-based profit repatriation.

Frequently Asked Questions

What is the UK corporation tax rate in 2025?

The UK has two main rates for 2025-26: a Small Profits Rate of 19% for companies with taxable profits under £50,000, and a Main Rate of 25% for profits over £250,000. Companies with profits between £50,001 and £250,000 receive marginal relief, creating an effective rate between 19% and 25%.

When did corporation tax increase to 25% in the UK?

The 25% main rate was introduced on 1 April 2023, replacing the previous flat 19% rate that applied to all non-ring fence profits. The change was announced at the Spring Budget 2021 and implemented two years later.

What will the UK corporate tax rate be in 2026?

Both the 19% small profits rate and 25% main rate have been confirmed as unchanged for the financial year beginning 1 April 2026 and continuing through 2026-27, providing stability for business planning.

What are the UK tax changes and thresholds for 2025-26?

There are no new rate changes for 2025-26. The thresholds remain £50,000 (lower limit) and £250,000 (upper limit) for standard companies, divided by the number of associated companies. One notable addition: the Undertaxed Profits Rule (Pillar Two UTPR) became effective for accounting periods beginning on or after 31 December 2024.

How does the UK corporate tax rate compare to the US?

The UK's 25% main rate is broadly comparable to the US combined federal and state corporate tax rate of approximately 25.57% (federal 21% plus average state taxes). Effective rates differ significantly due to each country's specific deductions, credits, and treaty networks.

What is the '60% trap'?

The "60% trap" affects individuals with income between £100,000 and £125,140, where the personal allowance tapers at £1 for every £2 earned — creating an effective 60% marginal rate (40% higher rate plus 20% from allowance loss). Company owner-directors need to account for this when planning salary and dividend extraction.

Need help navigating UK corporation tax for your business? VJM Global's international tax advisory team supports UK businesses with tax planning, compliance, and cross-border structuring — particularly for companies with operations in India. With 30+ years of experience and a 95% client retention rate serving 250+ UK businesses, we help you stay compliant and tax-efficient across borders. Reach us at info@vjmglobal.com or call +91 9213397070 (India office serving UK clients).