According to CFO.com citing Personiv's 2025 Finance and Accounting Talent Outlook, finance-function outsourcing actually fell 25% year-over-year in 2025 — even as 87% of CFOs reported talent shortages. That pullback isn't accidental. CFOs are weighing the risks more carefully.

This article lays out the real disadvantages of outsourcing accounting services: what they are, why they happen, and what smart businesses do to manage them before signing any agreement.

Key Takeaways

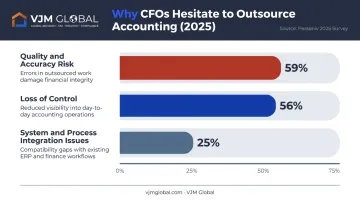

- Loss of control over daily financial processes is the most commonly cited concern — reported by 56% of CFOs in 2025

- Data security risks increase when sensitive financial records move outside your organization

- Hidden costs from scope creep and poorly written contracts can wipe out projected savings

- Communication gaps and staff turnover at outsourcing firms introduce service inconsistency

- Cross-border compliance failures carry financial penalties that catch many businesses off guard at audit time

Loss of Control and Reduced Visibility Into Your Finances

When you hand accounting to an external team, daily financial oversight shifts from inside your business to someone else's workflow. For many owners and CFOs, this is the hardest adjustment — and the data backs it up.

The same Personiv 2025 survey found that 56% of CFOs cited loss of control as a concern with external labour, while 59% cited quality and accuracy risk and 25% cited system and process integration issues. These aren't abstract worries — they translate into delayed reports, missed anomalies, and decisions made on stale data.

The Institutional Knowledge Problem

An in-house accountant builds contextual understanding over time: your seasonal revenue patterns, how you classify certain costs, which clients pay late, where anomalies typically appear. An external provider starts from scratch.

That knowledge gap creates real risk:

- Misclassifications in account coding that distort management reports

- Missed anomalies in cash flow that an insider would have flagged

- Reporting errors during the early months of an engagement, when the learning curve is steepest

- Inconsistent treatment of recurring transactions that require business-specific judgement

What Happens if the Relationship Breaks Down

The institutional knowledge gap compounds if the relationship itself deteriorates. Transitioning back to in-house accounting after a failed outsourcing arrangement is rarely smooth. If the provider maintained your books in proprietary systems or formats that don't export cleanly, you may face a period with limited access to your own financial records — at precisely the moment you need them most.

How to Partially Mitigate This Risk

You can preserve meaningful oversight without managing the books yourself:

- Require real-time or near-real-time access to cloud-based accounting dashboards (QuickBooks and Xero both support this)

- Define reporting cadences contractually — weekly transaction summaries, monthly management accounts

- Set specific KPIs for the outsourcing partner covering accuracy, turnaround, and responsiveness

- Retain a dedicated internal contact point who owns the relationship and reviews all outputs

VJM Global structures client engagements around this model: weekly payment status updates, monthly financial reports with cash flow forecasts, and interactive dashboards giving clients continuous visibility into receivables and key metrics. Clients retain meaningful oversight without carrying the operational burden.

That visibility only holds if someone internally is reviewing the outputs. Active management of the outsourcing relationship — not passive handoff — is what determines whether delegation works.

Data Security, Confidentiality, and Cybersecurity Risks

Outsourcing accounting means sharing payroll records, tax filings, banking credentials, and client payment histories with a third party. That inherently expands your exposure.

The IRS is explicit about this: tax professionals are prime targets for cybercriminals seeking client data to file fraudulent returns. Accounting firms handle financial records for multiple clients simultaneously — which makes them high-value targets. A breach at the vendor level can expose your records without the vendor bearing the full legal consequences.

Your Regulatory Liability Doesn't Transfer

This is the detail businesses frequently overlook. Data protection obligations follow the data controller — not just the processor.

| Jurisdiction | Key obligation |

|---|---|

| UK / EU (GDPR) | Controllers remain responsible for their processors' data handling; international transfers require adequacy or safeguards |

| Australia (Privacy Act) | APP 8 holds the original entity accountable for overseas recipients' handling of personal data |

| US (FTC Safeguards Rule) | Covered financial institutions — including tax preparers — must maintain security programs and oversee service providers |

| California (CCPA/CPRA) | Contracts with service providers must restrict use of personal data; businesses bear compliance responsibility |

A vendor's inadequate data handling can result in penalties for your company, not just theirs. Morgan Stanley paid $35 million to settle SEC charges after a vendor with no data-destruction expertise mishandled decommissioned devices containing data for approximately 15 million customers.

The OCC separately assessed a $60 million penalty for related unsafe practices. The client organization bore the consequences of the vendor's failure — not the vendor itself.

Due Diligence Checklist Before Engaging a Provider

- Request documentation of cybersecurity certifications (ISO 27001 is the international baseline)

- Ask about data encryption standards and where data is physically stored

- Require a signed NDA and a formal data processing agreement before sharing any records

- Confirm that data storage locations comply with your home country's privacy regulations

- Verify the provider's breach notification procedures and incident response timelines

VJM Global works with clients across the US, UK, and Australia handling cross-border financial data, and signs confidentiality agreements before engagement begins. When evaluating any provider, request this documentation upfront — a firm that handles international compliance should produce it without hesitation.

Hidden Costs, Scope Creep, and Budget Overruns

The cost savings that make outsourcing attractive in the first place can erode quickly once the engagement begins. Outsourcing contracts are scoped around defined recurring tasks. Real-world accounting rarely stays within those boundaries.

Where the Extra Costs Come From

According to the 2024 CAS Benchmark Survey by CPA.com and AICPA PCPS, 84% of accounting services practices use fixed-fee billing — and 57% use fixed-price agreements that include regular monitoring specifically for out-of-scope work. The prevalence of that monitoring tells you scope disputes are a recognized, recurring issue.

Common triggers for additional fees that weren't in the original quote:

- Audit support requests outside the standard reporting cycle

- Regulatory changes requiring revised filings or new compliance procedures

- Urgent ad hoc reports for investors, lenders, or board meetings

- Data migration and system integration work during onboarding

- Currency fluctuations on offshore billing — particularly USD/INR, GBP/INR, or AUD/INR exposure when contracts are denominated in the provider's local currency

The Onboarding Cost No One Advertises

Scope overruns aren't the only budget risk. Transitioning to a new outsourcing provider carries its own costs that rarely appear in proposals:

- Staff time to brief the incoming team on your business, systems, and processes

- A learning curve period during which errors are more likely and require more review

- Data migration from your previous system or accounting software

- Potential overlap period if you maintain any internal capability during the transition

How to Protect Yourself Contractually

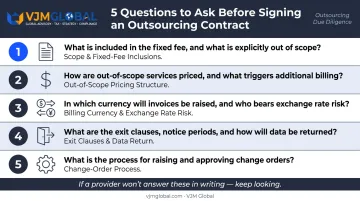

Before signing, ask these specific questions:

- What tasks are explicitly included in the fixed fee, and what triggers an additional charge?

- How are out-of-scope requests priced — hourly rate, fixed add-ons, or renegotiated retainer?

- What currency is billing denominated in, and who bears the exchange rate risk?

- What are the exit clauses, and how is data returned if the engagement ends?

- Is there a defined change-order process before additional work begins?

Any provider worth engaging should answer these questions without hesitation — in writing, before the contract is signed. If they can't or won't, treat that as a red flag and keep looking.

Communication Gaps, Quality Inconsistency, and Overdependence

The Friction of Distance

Time zone differences and the absence of face-to-face interaction create friction that becomes most apparent when something goes wrong. When a cash flow discrepancy surfaces or a tax query needs immediate clarification, the inability to escalate in real time can delay decisions and allow errors to compound.

Harvard Business School research identifies time zone differences as a measurable factor affecting communication quality and outcomes in remote working arrangements — a real risk in accounting, where missed deadlines carry compliance consequences.

Staff Turnover and Knowledge Loss

Communication friction compounds when staff turnover is factored in. The accountant who onboarded your business and learned your account classifications, cost structures, and reporting preferences may not be managing your books six months later.

Each handover introduces:

- A re-learning period during which errors are more likely

- Loss of the contextual knowledge built during earlier months

- Potential inconsistencies in how transactions are classified

Quality and accuracy were cited as concerns by 59% of CFOs in the 2025 Personiv survey — the single most common concern with external labour, above even loss of control.

The Overdependence Problem

Businesses that fully offload their accounting function without retaining any internal financial competence become highly vulnerable if the relationship deteriorates. Finding a replacement provider under time pressure, ensuring records are exported in a usable format, and maintaining continuity during the gap — all of this is costly and disruptive.

The practical fix: retain at least one internal person with enough financial literacy to review outputs, identify anomalies, and manage a transition if needed. Outsourcing should reduce your accounting burden — not eliminate your financial literacy entirely.

Compliance, Regulatory, and Cross-Border Accounting Risks

Tax laws and financial reporting standards are not universal. A provider well-versed in one country's regulations may lack the expertise to handle another's, and errors in tax filings carry direct financial penalties.

The Cost of Getting It Wrong

Cross-border compliance failures are not abstract risks. The IRS imposes a $10,000 penalty for each failure to file a complete and correct Form 5471 by the due date, a filing requirement for US persons with interests in certain foreign corporations. The Australian Taxation Office's guidance specifies that significant global entities can face penalties of 150% of the tax-related liability in specified scheme cases.

These penalties arise not from deliberate non-compliance but from missed filings, misapplied standards, and accounting providers who lacked the jurisdiction-specific expertise to flag the requirement in the first place.

The US GAAP vs. Indian Standards Example

A US company with operations in India must comply with both US GAAP and Indian Accounting Standards (Ind AS) simultaneously. These frameworks diverge meaningfully across revenue recognition, financial instruments, share-based payments, impairment, and business combinations, as detailed in PwC's comparative guide to IFRS, US GAAP, and Ind AS.

A generalist outsourcing provider handling both sets of standards without jurisdiction-qualified professionals may produce financials that satisfy one framework while creating silent compliance failures in the other. Those failures typically surface only during an audit, by which point penalties and interest may already be accruing.

What to Look For in a Cross-Border Provider

When evaluating an outsourcing partner for multi-jurisdictional operations, ask specifically:

- Which jurisdictions do your qualified professionals hold credentials for?

- Do you have CPAs for US compliance and Chartered Accountants for Indian or Australian requirements?

- How do you handle transfer pricing documentation and DTAA applications?

- What is your process when a regulatory change affects one jurisdiction but not another?

VJM Global's team of CPAs and Chartered Accountants specializes in cross-border compliance for businesses operating across the US, UK, Australia, and India, with jurisdiction-specific credentials covering each geography. For companies like Incubit GBS Pvt. Ltd., a US-based company with India operations, this means managing both accounting standards and regulatory obligations through a single coordinated team.

Frequently Asked Questions

Is outsourcing accounting illegal in the US?

Outsourcing accounting services is entirely legal in the US — there is no federal prohibition on engaging domestic or international providers. However, IRS Section 7216 imposes criminal penalties for unauthorized disclosure of tax return information, and offshore tax preparation generally requires written taxpayer consent, making compliance with applicable privacy regulations the business's responsibility regardless of provider.

What are the biggest risks of outsourcing accounting services?

Loss of financial control, data security vulnerabilities, hidden costs from scope creep, communication gaps, and cross-border compliance failures are the most significant risks. All are manageable with thorough provider vetting, a detailed scope of work, and a well-structured contract before the engagement begins.

How can businesses protect their financial data when outsourcing?

Require a signed NDA and a formal data processing agreement before sharing any records. Verify the provider's cybersecurity certifications, confirm where data is physically stored, and ensure storage locations comply with your home country's privacy laws. Maintaining read-only access to your own accounts at all times is also advisable.

Does outsourcing accounting save money, or can it end up costing more?

Outsourcing generally reduces overhead, but hidden costs (onboarding, scope creep, and currency fluctuations for offshore providers) can erode projected savings. Request written answers to billing and scope questions before signing — transparent pricing terms are non-negotiable.

Is outsourced accounting suitable for businesses operating in multiple countries?

Multi-jurisdictional businesses can benefit significantly from outsourcing, but only if the provider has verified, jurisdiction-specific expertise. Generalist providers without qualified professionals in your relevant jurisdictions introduce real compliance risk , particularly for tax filings, transfer pricing, and international information returns where penalties are material.

How do I know if an accounting outsourcing firm is the right fit?

Evaluate the provider's industry experience, credentials by jurisdiction, cybersecurity certifications, client retention rate, and pricing transparency. Ask for references from businesses of similar size and geographic complexity, and press for direct answers on billing, scope changes, and exit clauses before signing — evasiveness at that stage is a red flag.