This guide covers everything UK partnerships need to know: the definition and mechanics of partnership accounting, the different types of partnerships and their implications, the core components of partnership accounts (including the all-important appropriation account), UK tax compliance obligations under the new tax year basis, what happens when partners join or leave, and when professional accounting support becomes essential.

Key Takeaways

- Partnership accounting records income, expenses, capital, drawings, and profit allocations separately for each partner using an appropriation account

- The partnership files an SA800 tax return; each partner reports their share on SA100 + SA104 supplementary pages

- LLPs must file statutory accounts at Companies House within 9 months; general partnerships face no Companies House obligation

- The April 2024 Basis Period Reform moved all partnerships to a tax year basis, requiring those with non-31 March/5 April year-ends to apportion profits across tax years

What Is Partnership Accounting in the UK?

Partnership accounting is the structured system for recording, reporting, and allocating a partnership's financial activity. It ensures profits and losses are shared exactly as set out in the partnership agreement, with separate tracking of each partner's capital contributions, drawings, and profit distribution.

In legal terms, Section 1(1) of the Partnership Act 1890 defines a partnership as "the relation which subsists between persons carrying on a business in common with a view of profit." This remains the legal test for all UK general partnerships.

Most UK partnerships are tax-transparent entities — the partnership itself pays no income tax. HMRC's guidance confirms that "each partner is responsible for paying the tax due on his or her own share of the partnership profits."

There is no joint tax liability. If one partner fails to pay, HMRC pursues that individual alone — not the other partners.

Why partnership accounting is more complex:

- Multiple stakeholders with varying capital contributions and profit-sharing ratios

- Appropriation requirements before profit can be distributed

- Separate partner accounts tracking individual capital, drawings, and profit shares

- Dual compliance obligations: partnership-level filing plus individual partner tax returns

How Partnership Accounting Differs from Sole Traders and Limited Companies

Sole trader:

- Single profit and loss account

- All profit reported directly on the owner's Self Assessment return

- No appropriation account or capital splits required

Limited company:

- Separate legal entity subject to Corporation Tax

- Owners extract value via salaries and dividends, not profit appropriations

- Entirely different compliance framework (Companies House filing, Corporation Tax return, PAYE)

Partnership (general or limited):

- Tax-transparent structure requiring SA800 partnership return

- Each partner reports their share via SA100 + SA104 supplementary pages

- Appropriation account required to allocate profit among partners according to the agreement

Types of UK Partnerships and Their Accounting Implications

General Partnership (GP)

The default structure under the Partnership Act 1890. All partners share unlimited personal liability for business debts and joint management responsibility.

Accounting implications:

- No Companies House registration required

- Accounts prepared for HMRC and shared internally among partners

- Registration with HMRC for Self Assessment is mandatory

- Lower compliance burden than LLPs or Companies House-registered structures

Limited Partnership (LP) and Partnership at Will

An LP separates general partners (unlimited liability, day-to-day management) from limited partners (liability capped at their investment, no operational role). Section 4(2A) of the Limited Partnerships Act 1907 confirms limited partners "shall not be liable for the debts or obligations of the firm beyond the amount so contributed."

Key accounting requirements:

- Must clearly delineate each partner's class, liability, and profit entitlement

- Limited partners who withdraw capital become liable for debts up to the amount withdrawn

- Requires Companies House registration

A related arrangement worth understanding is the Partnership at Will — it has no fixed term and dissolves on notice. Because dissolution can be sudden, continuity planning and up-to-date capital accounts are especially important in this structure.

Limited Liability Partnership (LLP)

An LLP is a separate legal entity that offers limited liability to all members — and it carries the most significant accounting obligations of the three structures. LLPs are incorporated entities registered with Companies House, requiring at least two designated members, and must satisfy both HMRC and Companies House compliance obligations simultaneously.

What this means for your accounts:

- Statutory accounts (Balance Sheet and P&L) must be filed publicly at Companies House within 9 months of year-end

- Members are taxed individually on profit shares (no Corporation Tax for standard trading LLPs)

- Highest compliance burden: both HMRC and Companies House obligations

- Late filing triggers automatic penalties from £150 to £1,500, doubled for successive late years

| Feature | General Partnership | Limited Partnership | LLP |

|---|---|---|---|

| Liability | Unlimited (all partners) | Unlimited (general); capped (limited) | Limited to partnership assets |

| Companies House registration | Not required | Required | Required |

| Public accounts filing | No | Yes | Yes (within 9 months) |

| Minimum members | 2 | 2 (1 general + 1 limited) | 2 (including 2 designated) |

Core Components of Partnership Accounts

Capital Accounts vs. Current Accounts

Capital accounts record each partner's long-term investment — fixed contributions that typically remain stable unless the partnership agreement changes or partners join/leave.

Current accounts track ongoing transactions:

- Profit shares allocated to each partner

- Drawings (money or goods withdrawn for personal use)

- Interest on capital credited

- Interest on drawings charged

- Partner salaries (appropriations, not business expenses)

The sum of both accounts equals a partner's total equity in the business.

Partner Drawings

Money or goods a partner takes out for personal use must be recorded separately for each partner and deducted from their current account. Excessive withdrawals may trigger interest on drawings charges, which serve as a contractual deterrent against taking more than a fair share before final profit allocation.

Profit Sharing Ratio (PSR)

The agreed formula for dividing residual profit after all appropriations. Section 24(1) of the Partnership Act 1890 states that absent a written agreement, "all the partners are entitled to share equally in the capital and profits of the business" — regardless of capital contributed.

A written partnership agreement is essential to override these statutory defaults and reflect each partner's actual contributions and responsibilities.

The Appropriation Account: How Profits Are Distributed

The appropriation account is an additional statement showing how net profit is allocated among partners. It follows a strict sequence:

- Net profit — taken directly from the Statement of Profit or Loss

- Add: Interest on drawings — charged to each partner based on the amount and timing of withdrawals

- Less: Partners' salaries — deducted before residual profit is split; these never appear in the P&L

- Less: Interest on capital — calculated on opening capital balances to reward proportionate investment

- Residual profit or loss — divided between partners using the agreed PSR

Important: Partner salaries are not business expenses — they're treated as a guaranteed part of each partner's profit share and appear only in the appropriation account.

Worked Example: Two-Partner Appropriation Account

Scenario:

- Partner A and Partner B operate a general partnership

- Net profit for the year: £80,000

- Partner A's opening capital: £40,000; Partner B's opening capital: £20,000

- Interest on capital: 5% per annum

- Partner A receives a guaranteed salary: £15,000

- Interest on drawings: Partner A charged £500; Partner B charged £300

- Profit-sharing ratio: 60:40 (A:B)

Appropriation Account Calculation:

| Item | Amount (£) |

|---|---|

| Net profit for the year | 80,000 |

| Add: Interest on drawings (A: £500 + B: £300) | 800 |

| Profit available for appropriation | 80,800 |

| Less: Partner salary (A) | (15,000) |

| Less: Interest on capital (A: £40,000 × 5% = £2,000; B: £20,000 × 5% = £1,000) | (3,000) |

| Residual profit to be shared | 62,800 |

| Allocation by PSR: A (60%): £37,680; B (40%): £25,120 | — |

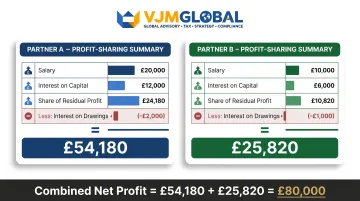

Partner A's Total Share:

- Salary: £15,000

- Interest on capital: £2,000

- Share of residual profit: £37,680

- Less: Interest on drawings: (£500)

- Total: £54,180

Partner B's Total Share:

- Salary: £0

- Interest on capital: £1,000

- Share of residual profit: £25,120

- Less: Interest on drawings: (£300)

- Total: £25,820

Both totals are credited to each partner's current account — a common error is crediting these to capital accounts, which distorts the long-term investment record.

What Happens When a Partner Joins or Leaves?

The appropriation process above assumes a stable partnership — but when the structure changes, additional accounting adjustments apply.

Admission of a new partner:

- Goodwill must be valued and credited to existing partners in the old PSR

- If goodwill is not retained in the accounts, it's immediately written off using the new PSR

- This transfer compensates outgoing partners for the intangible value they built

Retirement or exit:

- The departing partner's capital and current account balances are settled (cash or loan account)

- Remaining partners update their profit-sharing ratios

- Assets may need revaluation to reflect current market values

- Professional accountants ensure all adjustments are legally and financially accurate

UK Partnership Tax Obligations and Filing Deadlines

SA800 Partnership Tax Return

The nominated partner is responsible for filing the SA800 Partnership Tax Return with HMRC. The SA800 reports the partnership's income, expenses, and profit allocation — not to pay tax at partnership level, but to provide HMRC with a cross-reference for each partner's individual return.

Filing deadlines (2024/25 tax year):

| Return Type | Deadline |

|---|---|

| Paper SA800 | 31 October 2025 (11:59pm) |

| Online SA800 | 31 January 2026 (11:59pm) |

Individual Partner Obligations

Each partner must report their allocated profit share on their personal Self Assessment return (SA100) using the SA104 supplementary partnership pages:

- SA104S (short version) — for trading income only

- SA104F (full version) — for complex or mixed income situations

Tax liability rests entirely with each individual partner, not the partnership entity. Payment deadline: 31 January following the tax year.

Miss these deadlines and the penalties multiply fast — because every partner pays separately.

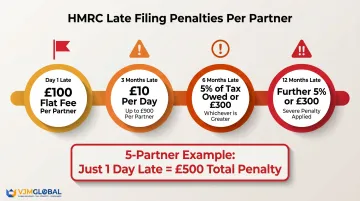

Late Filing Penalties

HMRC's penalty structure charges each partner individually, so a single late SA800 hits the whole firm:

| Delay | Penalty per Partner |

|---|---|

| 1 day late | £100 |

| After 3 months | £10/day (max £900) |

| After 6 months | 5% of tax due or £300 (whichever is greater) |

| After 12 months | Further 5% of tax due or £300 (whichever is greater) |

Critical: All partners are charged penalties if the partnership return is late. A 5-partner firm filing one day late faces £500 in initial penalties (£100 × 5 partners), not just £100.

Basis Period Reform (April 2024)

The Basis Period Reform moved UK partnerships from the Current Year Basis to a Tax Year Basis from 2024/25 onward. Profits are now taxed in the year they arise, regardless of accounting period end date.

Who is affected:

- Partnerships with accounting year-ends other than 31 March or 5 April

- Farming partnerships and seasonal businesses

- Large professional partnerships with non-standard year-ends

Transition year (2023/24):

- All outstanding overlap profits were relieved in full

- Excess transitional profits were automatically spread over 5 years (or accelerated by election)

- Partnership SA800 returns were unchanged; transitional adjustments flowed through to individual partner SA100/SA104 returns

Ongoing impact: Partnerships must now calculate profits for the tax year (6 April to 5 April) rather than their accounting period, requiring apportionment if year-ends don't align.

Compliance Differences: LLPs vs General Partnerships

General partnerships:

- Deal exclusively with HMRC

- No Companies House filing requirement

- Accounts prepared to support SA800 and for partner transparency

- Not publicly disclosed

LLPs:

- Must satisfy two authorities: HMRC (SA800) and Companies House (statutory accounts)

- Statutory accounts (Balance Sheet + P&L) due 9 months after financial year-end

- Late filing triggers automatic penalties: £150 (up to 1 month late), £375 (1-3 months), £750 (3-6 months), £1,500 (over 6 months)

- Penalties double for successive late years

- Designated members can be prosecuted for non-compliance

Making Tax Digital (MTD)

HMRC confirms that "Partnerships will also need to use Making Tax Digital for Income Tax in the future. We'll set out the timeline for this at a later date."

Current status: No mandatory start date for partnerships as of March 2026.

Recommended action now: Move to MTD-compatible software (such as Xero or QuickBooks) and maintain digital records today — the mandate will come with limited lead time once announced.

Why UK Partnerships Need Professional Accounting Support

Accuracy and Dispute Prevention

Professionally prepared accounts — particularly the appropriation account and partner capital schedules — provide an authoritative record that removes ambiguity from profit distributions. This resolves disagreements before they escalate into costly disputes.

The Basis Period Reform has added complexity that increases the risk of under-reporting without expert guidance. Partnerships with non-standard year-ends now require profit apportionment calculations and transitional adjustments that most business owners are unfamiliar with.

Tax Efficiency and Compliance

A specialist accountant ensures:

- Timely SA800 submission (avoiding the £100-per-partner late penalty)

- Correct handling of National Insurance Contributions:

- Class 4 NIC: 6% on profits between £12,570 and £50,270; 2% above £50,270

- Class 2 NIC: £3.45/week, voluntary below £6,725 Small Profits Threshold to protect State Pension entitlement

- Tax planning opportunities such as optimising profit allocation or timing drawings to minimise each partner's tax burden

Specialist Support for UK Partnerships

For UK-based partnerships that need reliable, expert accounting support without the overhead of an in-house team, VJM Global offers specialist accounting outsourcing and compliance services. Having served 250+ UK businesses across 15+ industries with a 95% client retention rate, their team handles everything from bookkeeping and SA800 preparation to LLP statutory accounts and partner tax planning.

Their service is tailored to general partnerships, limited partnerships, and LLPs — covering HMRC compliance, timely filings, and tax planning that keeps liabilities in check.

Frequently Asked Questions

How does partnership accounting work in the UK?

Partnership accounting records all business income and expenses, then distributes profits to partners via an appropriation account based on the partnership agreement. The partnership files an SA800 with HMRC. Each partner then pays tax individually through Self Assessment (SA100 + SA104).

How does a partnership work in the UK?

Two or more people carry on a business together with a view to profit, sharing management responsibilities and liabilities — unlimited in a general partnership, limited for LLPs. They operate under a partnership agreement or, by default, the Partnership Act 1890, which defaults to equal profit sharing.

Do I need an accountant for a partnership in the UK?

LLPs must file statutory accounts, but even general partnerships benefit from professional help. The complexity of profit allocation, SA800 filing, Basis Period Reform adjustments, and individual partner tax returns means professional support is worth the cost for most partnerships.

What is the SA800 and when is it due?

The SA800 is the Partnership Tax Return filed with HMRC by the nominated partner. The paper deadline is 31 October and the online deadline is 31 January following the tax year. Late submission triggers an automatic £100 penalty per partner.

What records must a UK partnership keep for HMRC?

Partnerships must retain:

- Business transaction records (invoices, bank statements, receipts)

- Each partner's capital contributions and drawings

- Copies of the SA800 and all partners' Self Assessment returns

- The partnership agreement

Records must be kept for at least 5 years after the 31 January submission deadline.