A Limited Liability Partnership (LLP) occupies a specific and genuinely useful position in that landscape. It combines the personal liability protection of a limited company with the tax transparency of a traditional partnership — making it a natural fit for professional services firms and multi-partner businesses that want protection without Corporation Tax.

This guide covers what a UK LLP actually is, its key benefits, how it compares to limited companies and general partnerships, how taxation works for members, how to register, and what ongoing compliance looks like.

Key Takeaways

- An LLP is a separate legal entity under the Limited Liability Partnerships Act 2000, registered at Companies House

- Members' liability is capped at their capital contribution, protecting personal assets from business debts

- LLPs pay no Corporation Tax — each member files individually through Self Assessment

- At least two members and two designated members are required at all times

- An LLP agreement is not legally required but is strongly recommended; without one, the LLP Regulations 2001 defaults apply

What Is a Limited Liability Partnership in the UK?

An LLP is a legally distinct business entity incorporated under the Limited Liability Partnerships Act 2000. Section 1 of that Act gives the LLP legal personality separate from its members — meaning the LLP can own assets, enter contracts, and sue or be sued in its own name, independent of whoever its members are at any given time.

Minimum requirements for incorporation:

- At least two members (individuals or corporate bodies)

- Carrying on a lawful business with a view to profit

- Registered at Companies House

Non-profit activities are not eligible for LLP status. The profit motive is a statutory requirement — an LLP set up without it risks being treated as invalid at Companies House.

Members vs. Designated Members

Every LLP has two categories of members:

- Ordinary members contribute capital, share profits, and participate in management under the LLP agreement

- Designated members hold the same rights but also carry statutory compliance duties:

- Signing and filing annual accounts

- Submitting the Confirmation Statement

- Notifying Companies House of member changes

Every LLP must have at least two designated members at all times. If the LLP has fewer than two, all members automatically become designated members by default.

Key Benefits of Forming an LLP

Limited Liability Protection

Each member's financial exposure is capped at their capital contribution to the LLP. Creditors cannot pursue a member's home, savings, or personal assets for business debts. This protection is unavailable to sole traders and general partners, both of whom remain personally exposed to unlimited claims.

Tax Transparency

An LLP pays no Corporation Tax. HMRC treats most LLPs as tax transparent — each member is charged Income Tax on their allocated profit share through Self Assessment. This avoids the double-taxation layer that limited company directors face: Corporation Tax on company profits, then dividend tax on any extraction.

Profit-Sharing Flexibility

The LLP agreement can set any profit-sharing ratio the members agree on. This makes it possible to distribute income in a way that makes best use of each member's Personal Allowance and basic rate band — particularly useful where members have different tax positions or income levels outside the LLP.

Operational Flexibility

A limited company must follow statutory governance rules covering directors, shareholders, and board decisions. An LLP sidesteps all of that — its internal management is entirely governed by a private LLP agreement. Members can structure decision-making, responsibilities, and procedures however they choose, and that agreement is never filed publicly at Companies House.

Perpetual Succession

Because the LLP is a corporate body, the departure, retirement, or death of a member does not dissolve it. The LLP continues, can admit new members, and carries on trading. This continuity makes an LLP a more stable vehicle for professional firms or long-term ventures with multiple stakeholders.

LLP vs. Limited Company vs. General Partnership

| Feature | LLP | Limited Company | General Partnership |

|---|---|---|---|

| Legal identity | Separate corporate body (LLP Act 2000) | Separate corporate body | Not a separate legal entity |

| Member/owner liability | Limited to capital contributed | Limited (shareholders) | Joint and unlimited |

| Tax treatment | Tax transparent — members pay Income Tax on profit shares | Company pays Corporation Tax; shareholders pay dividend tax | Tax transparent — partners file Self Assessment |

| Minimum members | 2 | 1 director, 1 shareholder | 2 partners |

| Companies House registration | Required | Required | Not required |

| Public accounts filing | Yes | Yes | No |

| Management flexibility | High — governed by private LLP agreement | Constrained by statutory rules | High — governed by partnership agreement |

| Profit retention | Cannot retain profits without taxing members | Can retain profits in company, deferring personal tax | Cannot retain profits without taxing partners |

Tax Comparison: LLP vs. Limited Company

On full annual profit extraction, an LLP member typically pays less total tax than a limited company director. The LLP has no Corporation Tax layer and no dividend tax — just Income Tax and National Insurance on the profit share.

The key exception is profit retention. A limited company director can retain profits inside the company and defer personal tax across multiple years.

An LLP member is taxed on their full profit share in the year it arises — even if that money stays in the LLP's bank account. For a profitable firm not distributing everything annually, this can mean a meaningful cash-flow disadvantage compared to operating through a limited company.

Liability Comparison: LLP vs. General Partnership

Under the Partnership Act 1890, general partners are jointly liable for firm debts and jointly and severally liable for wrongful acts. Every partner is fully exposed. An LLP removes both risks entirely — members are not personally liable for the LLP's debts or for other members' negligence. For a solicitors' firm or accountancy practice handling high-value engagements, this means a negligence claim against one partner cannot reach another member's personal assets.

Who Should Choose an LLP?

An LLP suits:

- Professional services firms — solicitors, accountants, architects, consultants

- Two or more active partners who want liability protection without Corporation Tax

- Existing general partnerships looking to convert without changing their tax treatment

One structural limitation applies: LLPs do not issue shares. Equity investors and venture capital firms generally prefer limited companies for this reason, so the LLP is a less natural fit for businesses seeking external equity funding.

How LLP Taxation Works in the UK

Self Assessment for Members

HMRC treats each member's allocated profit share as personal income. Every member must register for Self Assessment and file a personal tax return annually. The LLP itself does not pay Corporation Tax but is required to submit a Partnership Tax Return (SA800), filed by the nominated partner, which reports total profits and each member's allocated share.

To register the partnership with HMRC, the nominated partner completes form SA400. Individual members register separately using their own Self Assessment accounts.

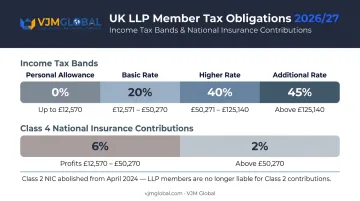

2026/27 Income Tax and National Insurance Rates

Current GOV.UK rates for 2026/27 apply to LLP members' profit shares as follows:

| Band | Income Range | Rate |

|---|---|---|

| Personal Allowance | Up to £12,570 | 0% |

| Basic rate | £12,571 – £50,270 | 20% |

| Higher rate | £50,271 – £125,140 | 40% |

| Additional rate | Above £125,140 | 45% |

Class 4 National Insurance (2026/27):

- 6% on profits between £12,570 and £50,270

- 2% on profits above £50,270

From April 2024, most self-employed people with profits of £7,105 or more no longer pay Class 2 NIC but are treated as having paid it for National Insurance record purposes.

Profit Taxed When Earned, Not When Withdrawn

Unlike a limited company — where retained profits sit untaxed until extracted — an LLP member is taxed on their full profit share in the year it arises, whether or not any money is actually drawn from the LLP.

This rules out profit deferral as a tax strategy, but makes planning more straightforward for members who draw their full share each year.

VAT and PAYE

Two further registrations may apply, both separate from Companies House incorporation and HMRC partnership registration:

- VAT: Required if the LLP's taxable turnover exceeds £90,000 (threshold from 1 April 2024)

- PAYE: Required if the LLP employs staff

How to Register an LLP in the UK

Choosing a Name and Registered Office

The proposed name must:

- End with "Limited Liability Partnership," "LLP," or "llp"

- Not be identical or too similar to a name already on the Companies House register

- Avoid sensitive or restricted words without prior approval

- Correspond to a registered office in the correct UK jurisdiction (England and Wales, Scotland, or Northern Ireland)

Completing Form LL IN01

The incorporation application must include:

- LLP name and registered office address

- Registered email address

- Details of all proposed members and designated members

- People with Significant Control (PSC) information

- Statement of compliance

From 18 November 2025, identity verification is mandatory for all designated members and PSCs under the Economic Crime and Corporate Transparency Act 2023.

Filing Routes and Fees

| Method | Fee | Processing Time |

|---|---|---|

| Digital (software filing) | £100 | Usually within 24 hours |

| Same-day digital service | £156 | Same day |

| Paper filing | £124 | Can take a week or more |

Once Companies House approves the application and issues a Certificate of Incorporation, the nominated partner must separately register the partnership for Self Assessment with HMRC using form SA400. Individual members register for Self Assessment independently.

For international businesses, these post-incorporation steps — drafting the LLP agreement, meeting HMRC deadlines, and managing cross-border reporting obligations — often land simultaneously and can be easy to miss. VJM Global's business setup advisory team has supported 250+ UK businesses through the full registration process. For UK LLPs with international founders or members operating across India, the team also handles international tax structuring and FEMA compliance. Reach out at info@vjmglobal.com to discuss your setup.

Ongoing LLP Compliance Requirements

Annual Filings

Designated members are responsible for two core annual filings:

- Confirmation Statement — must be filed within 14 days of the review period end date. Failure can result in fines of up to £5,000, prosecution, and potential strike-off.

- Annual accounts — prepared and filed at Companies House, publicly available on the register.

Late filing penalties apply on a sliding scale:

| Delay | Penalty |

|---|---|

| Up to 1 month late | £150 |

| 1–3 months late | £375 |

| 3–6 months late | £750 |

| More than 6 months late | £1,500 |

Penalties double if the LLP files late in two consecutive financial years.

Statutory Registers and Member Changes

Every LLP must maintain:

- A register of members

- A register of People with Significant Control (PSC)

Any changes to member details, designated member status, registered office address, or PSC information must be notified to Companies House within 14 days.

LLP Agreement: Governance and Compliance Implications

An LLP agreement is not a legal requirement, but operating without one creates real governance risk. Without a bespoke agreement, the default provisions of the Limited Liability Partnerships Regulations 2001 apply, which include:

- Equal sharing of capital and profits regardless of contribution

- Every member's right to participate in management

- No clear procedures for admitting or removing members

A properly drafted LLP agreement should cover profit-sharing ratios, decision-making procedures, designated member responsibilities, admission and removal of members, and dispute resolution.

Unlike a limited company's articles of association, the LLP agreement is a private document and is never filed at Companies House. This means its terms — including how profits are split and how disputes are resolved — remain entirely confidential to the members.

Frequently Asked Questions

What is an example of a limited liability partnership in the UK?

PricewaterhouseCoopers LLP (Companies House number OC303525) and Deloitte LLP (OC303675) are well-known examples. Law firms, accountancy practices, architectural partnerships, and consultancies commonly use this structure across the UK.

What is the difference between an LLP and an LP in the UK?

An LLP (incorporated under the LLP Act 2000) gives all members limited liability and full management rights. An LP (Limited Partnerships Act 1907) requires at least one general partner with unlimited liability, and limited partners forfeit their liability protection if they take part in management.

What are the tax obligations of an LLP member in the UK?

Each member pays Income Tax and Class 4 National Insurance on their allocated profit share through Self Assessment. The LLP itself pays no Corporation Tax. The nominated partner also files a Partnership Tax Return (SA800) with HMRC each year.

Can a non-resident or foreign national be a member of a UK LLP?

Yes. Members can be individuals or corporate bodies, including overseas persons — form LL IN01 covers both. All designated members must complete identity verification with Companies House, and overseas members should take separate advice on their home-jurisdiction tax position.

Do UK LLPs have to file accounts publicly at Companies House?

Yes. LLPs must prepare and file annual accounts with Companies House, which appear on the public register. This is a key difference from a general partnership, which has no public filing requirement.

Is an LLP agreement legally required, and what happens without one?

An LLP agreement is not a legal requirement but is strongly recommended. Without one, the default rules under the Limited Liability Partnerships Regulations 2001 apply — including equal profit sharing and equal management rights for all members — which may not reflect the members' actual intentions or contributions.