Introduction

Every limited company registered in the UK must prepare statutory accounts at the end of each financial year. Under the Companies Act 2006, directors bear personal responsibility for this requirement—not just administratively, but legally.

Non-compliance carries serious consequences: late filing can trigger criminal prosecution, director disqualification, and strike-off from the register, all of which damage credibility with lenders, investors, and suppliers.

For UK subsidiaries of foreign businesses, the complexity increases significantly. Records held overseas must be mirrored in the UK at six-month intervals, iXBRL tagging is mandatory for tax submissions, and managing dual obligations to Companies House and HMRC demands specialist knowledge.

This guide covers what statutory accounts are, who must file them, what they contain, key deadlines, preparation steps, and when professional support becomes essential.

TLDR:

- All UK limited companies must prepare statutory accounts annually under the Companies Act 2006

- Accounts must be filed with Companies House (9 months) and used for corporation tax returns to HMRC (12 months)

- Late filing penalties range from £150 to £1,500, doubling for consecutive failures—criminal prosecution is also possible

- Company size determines accounting framework (FRS 105/102/IFRS) and disclosure level

- iXBRL tagging is compulsory for HMRC submissions

- Most companies benefit from professional preparation to avoid compliance gaps

What Are Statutory Accounts in the UK?

Statutory accounts are formal financial statements prepared at the end of a company's financial year, as required by Section 394 of the Companies Act 2006. Unlike management accounts (prepared internally for decision-making), statutory accounts carry legal force. They must be distributed to shareholders, filed with Companies House for public record, and submitted to HMRC as part of the corporation tax return.

Dual Filing Obligation

Companies face two separate but linked statutory submissions:

- Companies House filing: Makes financial statements publicly available on the register

- HMRC corporation tax return (CT600): Uses the same accounts to calculate corporation tax liability

The underlying financial data is the same for both, but the deadlines, formats, and submission systems differ. Companies House requires accounts within 9 months of the financial year-end (6 months for public companies), while HMRC requires the CT600 within 12 months. Corporation tax payment falls due 9 months and 1 day after the period end — a separate deadline that frequently catches directors off guard.

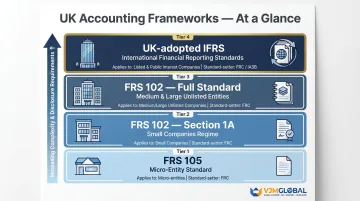

Accounting Frameworks

UK companies must choose one of four accounting frameworks based on their size and listing status:

| Framework | Applies To | Standard-Setter |

|---|---|---|

| FRS 105 | Micro-entities | Financial Reporting Council (FRC) |

| FRS 102 Section 1A | Small companies | FRC |

| FRS 102 (full) | Medium and large unlisted companies | FRC |

| UK-adopted IFRS | Listed companies (mandatory); others (optional) | FRC / IASB origin |

The FRC sets all UK accounting standards. FRS 102 draws from the IASB's IFRS for SMEs standard with UK-specific amendments. Listed companies whose shares trade on a UK regulated market must use UK-adopted IFRS. Whichever framework applies, Section 393 establishes an overriding obligation: directors must not approve accounts unless satisfied they present a truthful and accurate picture of the company's financial position and performance.

Record Retention Requirements

Section 388(4) prescribes minimum retention periods:

- Private companies: 3 years from the date records are made

- Public companies: 6 years from the date records are made

HMRC guidance recommends keeping records for 6 years from the end of the last financial year for broader tax compliance purposes.

Records held outside the UK fall under Section 388(2)-(3) — a provision particularly relevant for UK subsidiaries of foreign companies. Where accounting records are maintained abroad, accounts and returns must be sent to and kept at a UK location. The financial position must be disclosed at intervals not exceeding 6 months, ensuring directors can verify compliance and keep UK-accessible records at all times.

Who Needs to Prepare Statutory Accounts?

Entity Types

Required to prepare statutory accounts:

- All UK limited companies (including dormant companies)

- Limited Liability Partnerships (LLPs)

Exempt from statutory accounts:

- Sole traders (must register for Self Assessment but face no Companies Act filing duty)

- Unincorporated businesses

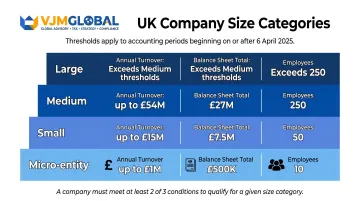

Company Size Categories and Updated Thresholds

The Companies (Accounts and Reports) (Amendment and Transitional Provision) Regulations 2024 (SI 2024/1303) raised thresholds substantially for accounting periods beginning on or after 6 April 2025. A company qualifies for a size category if it meets at least two of three conditions in both the current and preceding financial year.

| Category | Turnover (max) | Balance Sheet Total (max) | Employees (max) |

|---|---|---|---|

| Micro-entity | £1,000,000 | £500,000 | 10 |

| Small | £15,000,000 | £7,500,000 | 50 |

| Medium | £54,000,000 | £27,000,000 | 250 |

| Large | Exceeds medium thresholds | Exceeds medium thresholds | Exceeds medium |

The small company turnover threshold rose from £10.2 million to £15 million, bringing more companies within reach of simplified reporting regimes.

What Each Size Category Means in Practice

Micro-entities:

- May use highly simplified FRS 105 accounts

- Limited disclosure requirements

- No directors' report required

- Generally audit-exempt

Small companies:

- May file abridged accounts

- Can use FRS 102 Section 1A (simplified framework)

- No cash flow statement required

- Generally audit-exempt

- Directors' report required in a simplified form

Medium and large companies:

- Must file full accounts including directors' report

- Must produce cash flow statement

- Large companies must include strategic report

- Generally require statutory audit

UK Statutory Audit Requirement

Size thresholds directly determine audit obligations. Small companies and micro-entities that stay within the limits above are generally exempt from statutory audit.

Exemption is lost if:

- The company is public (unless dormant)

- The company is an authorised insurance, banking, e-money, MiFID investment, or UCITS management firm

- Members holding at least 10% of nominal share capital demand an audit

- The company is a subsidiary of a large group (group membership rules apply)

Medium and large companies generally must have accounts independently audited by a Registered Auditor.

What Do UK Statutory Accounts Include?

The exact documents required vary by company size, but all statutory accounts share core components.

Core Financial Statements

Balance Sheet (Statement of Financial Position):

A snapshot of the company's assets, liabilities, and equity at the financial year-end. The balance sheet distinguishes between:

- Current assets: Convertible to cash within 12 months (e.g., inventory, trade receivables, cash)

- Non-current assets: Long-term holdings (e.g., property, equipment, intangible assets)

- Current liabilities: Due within 12 months (e.g., trade payables, short-term borrowings)

- Long-term liabilities: Due after 12 months (e.g., long-term loans, deferred tax)

Profit and Loss Account (Income Statement):

A record of all income earned and expenses incurred during the financial year, culminating in the net profit or loss figure. This feeds directly into the corporation tax calculation submitted to HMRC.

Cash Flow Statement:

Details inflows and outflows of cash across:

- Operating activities (cash from core business operations)

- Investing activities (purchase/sale of long-term assets)

- Financing activities (loans, equity, dividends)

Required for: Medium and large companies

Exempt: Micro-entities and small companies filing under FRS 102 Section 1A

Beyond the primary statements, statutory accounts require several supporting documents — each with its own rules by company size.

Supporting Documents

Notes to the Financial Statements:

Mandatory for all companies except micro-entities, these provide additional context for line items:

- Depreciation and amortisation policies

- Related party transactions

- Breakdown of debtors and creditors

- Contingent liabilities

- Post-balance-sheet events

Director remuneration disclosure rules differ by size: small companies are not explicitly required to disclose this under FRS 102 (though non-market-terms transactions may still need flagging), while medium and large companies must provide full disclosures under Schedule 5 of SI 2008/410.

Directors' Report:

Required for medium and large companies, this narrative section summarises:

- Business performance and principal activities

- Principal risks and uncertainties

- Future outlook and strategic direction

- Director information and share capital changes

Small companies are generally exempt from a full directors' report but must include basic information.

Auditor's Report:

Where statutory audit is required, an independent Registered Auditor provides an opinion. The ICAEW guidance explains opinion types:

- Unmodified (unqualified) opinion: The auditor considers that accounts give a true and fair view—the standard "clean" opinion

- Qualified opinion: Material but not pervasive misstatement or limitation of scope

- Adverse opinion: Material and pervasive misstatements

- Disclaimer of opinion: Unable to obtain sufficient evidence; effects are material and pervasive

Filing Deadlines and Late Filing Penalties

Key Deadlines

| Scenario | Deadline |

|---|---|

| Private limited company (annual) | 9 months after financial year-end |

| Public limited company (annual) | 6 months after financial year-end |

| First accounts – private company | 21 months from incorporation date, or 3 months from accounting reference date (whichever is longer) |

| First accounts – public company | 18 months from incorporation date, or 3 months from accounting reference date (whichever is longer) |

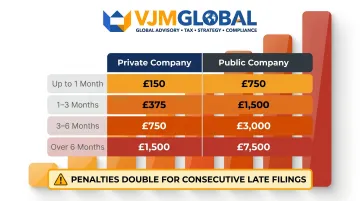

Late Filing Penalty Schedule

| Time After Deadline | Private Company | Public Company |

|---|---|---|

| Up to 1 month | £150 | £750 |

| 1 to 3 months | £375 | £1,500 |

| 3 to 6 months | £750 | £3,000 |

| More than 6 months | £1,500 | £7,500 |

Critical: Penalties double if accounts are late two years in a row. A private company filing more than 6 months late for the second consecutive year faces a £3,000 penalty.

Consequences Beyond the Financial Penalties

The fines are just the beginning. Repeated late filing puts directors and the company itself at serious legal and commercial risk:

- Removes the company from the register entirely (Companies House strike-off)

- Exposes every director to criminal prosecution under Section 451 of the Companies Act 2006 — a strict liability offence with no intent required

- Triggers potential disqualification under the Company Directors Disqualification Act 1986

- Creates a permanent public record that damages credibility with lenders, investors, and suppliers

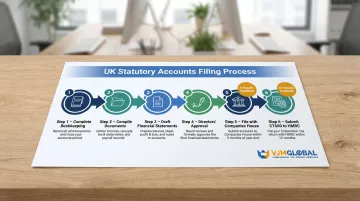

How to Prepare and File Statutory Accounts: A Step-by-Step Overview

Preparation Process

- Ensure bookkeeping is complete and reconciled: Maintain accurate records throughout the year; reconcile bank statements, invoices, payroll records, and loan agreements monthly

- Compile supporting documents: Gather all source documents including contracts, bank statements, VAT returns, payroll records, and fixed asset registers

- Draft financial statements: Prepare accounts in line with the applicable accounting framework (FRS 105, FRS 102 Section 1A, FRS 102 full, or UK-adopted IFRS)

- Directors review and approval: Directors must review accounts and formally approve them, confirming they give a true and fair view

- Submit to Companies House: File via the GOV.UK online filing service or approved software using your Companies House password and authentication code

- File CT600 with HMRC: Separately submit the corporation tax return with iXBRL-tagged accounts attached, due 12 months after the accounting period end

Common Mistakes That Cause Delays

Confusing deadlines:

- Companies House filing: 9 months after year-end (private companies)

- HMRC CT600 filing: 12 months after year-end

- Corporation tax payment: 9 months and 1 day after year-end

These are three distinct deadlines. Missing the payment deadline incurs interest and penalties separate from the late filing penalty.

Applying the wrong accounting framework:

- Using FRS 102 full when FRS 102 Section 1A is appropriate adds unnecessary complexity

- Using FRS 105 when the company exceeds micro-entity thresholds results in under-disclosure and non-compliance

- Verify your size category against the April 2025 thresholds before selecting a framework

iXBRL Requirements Explained

What is iXBRL?

iXBRL (Inline eXtensible Business Reporting Language) embeds machine-readable tags directly into financial statements so HMRC can extract and validate data programmatically. The HMRC XBRL guide confirms iXBRL tagging has been mandatory for Company Tax Returns filed on or after 1 April 2011.

What must be tagged:

- Financial accounts (balance sheet, profit and loss, notes)

- Tax computations

- Detailed profit and loss statements

Which taxonomies apply:

- FRC Taxonomy: For accounts prepared under IFRS, FRS 101, FRS 102, FRS 102 Section 1A, FRS 105, and charity SORP

- CT Computational Taxonomy: For corporation tax computations

Most accounting software handles iXBRL tagging automatically, making this a background process for most companies. Manual preparation is no longer viable in any case: as of 31 March 2026, the HMRC/Companies House joint online filing service closed, and all filings now require commercial software.

Should You Hire a Professional to Prepare Statutory Accounts?

Who Is Qualified to Prepare Statutory Accounts?

While directors have the legal duty to prepare accounts under Section 394, there is no legal requirement for a qualified accountant to prepare accounts for audit-exempt companies (micro-entities and small companies). However, statutory audits must be conducted by a Registered Auditor under Section 1212—an individual or firm that is a member of a Recognised Supervisory Body (RSB).

Recognised professional bodies in the UK:

| Body | Members | Audit Signing Authority |

|---|---|---|

| ICAEW (ACA/FCA) | 151,761 | Yes |

| ACCA | 223,454 | Yes |

| ICAS (CA) | 22,606 | Yes |

| CAI | N/A | Yes |

| CIMA | 115,000 | No |

| CIPFA | 14,000 | No |

Of these, four RSBs — ICAEW, ACCA, ICAS, and CAI — register and supervise statutory auditors. CIMA members are recognised for management accounting but cannot sign statutory audit reports under the Companies Act 2006.

Important for international companies: The US CPA qualification is not recognised as an approved third-country qualification for UK statutory audit purposes. The FRC's international agreements cover only Australia, New Zealand, and Switzerland. US CPAs working in UK subsidiaries cannot sign statutory audits without obtaining a UK-recognised qualification.

The Case for Professional Support

Directors of micro-entities and simple small companies can legally self-prepare accounts. In practice, few do — the combination of iXBRL tagging requirements, dual filing obligations to Companies House and HMRC, and evolving FRC frameworks makes errors costly and time-consuming to fix.

Key benefits of outsourcing:

- Navigates Companies Act 2006 requirements, FRC frameworks, and HMRC iXBRL tagging accurately

- Reduces exposure to penalties, restatements, and criminal prosecution risk under Section 394

- Returns director time to revenue-generating work rather than technical accounting

- Delivers planning and analysis advice that goes beyond filing compliance

Specialist Support for UK Subsidiaries of Foreign Companies

International businesses operating UK subsidiaries face unique challenges:

- Records held overseas must mirror in the UK every six months (Section 388)

- UK-specific accounting frameworks differ from US GAAP, IFRS as issued by the IASB, or other jurisdictions

- iXBRL tagging and dual filings to Companies House and HMRC require local expertise

- Coordination between parent company reporting and UK statutory obligations

VJM Global supports over 250 UK businesses — including subsidiaries of American, Australian, and European companies — with these exact requirements. The firm's UK accounting team provides:

- Statutory accounts preparation under UK GAAP or UK-adopted IFRS

- Companies House filing within the 9-month deadline

- HMRC CT600 submission with iXBRL-tagged accounts

- Accounting overhead reduced by up to 50% compared to in-house UK finance teams

- Chartered Accountants with hands-on UK standards experience

For international companies, this means local compliance coverage without the cost or complexity of building an in-house UK finance function.

Frequently Asked Questions

What are statutory accounts in the UK?

Statutory accounts are legally required financial statements prepared at the end of each financial year under the Companies Act 2006. They must be filed with Companies House for public record and used as the basis for the corporation tax return submitted to HMRC, covering the company's financial position and performance.

What does a statutory accountant do?

A statutory accountant prepares the required financial statements on behalf of a company, ensures compliance with the relevant accounting framework (UK GAAP or UK-adopted IFRS), and liaises with HMRC for corporation tax reporting. They also handle Companies House filings and iXBRL tagging requirements.

How much should I pay for an accountant in the UK?

Costs vary by company size and complexity. Micro-entity accounts preparation typically starts from a few hundred pounds; medium-sized companies may pay several thousand. Key cost drivers include transaction volume, audit requirements, industry-specific reporting, and CT600 preparation — so compare quotes from multiple qualified firms.

Which accounting qualifications are recognised in the UK (CA, ACCA, CPA)?

The primary recognised qualifications for statutory work in the UK are ACA/FCA (ICAEW), ACCA, CA (ICAS or Chartered Accountants Ireland), and CIMA. The US CPA is not recognised for UK statutory audit purposes, though CPAs may assist under the supervision of a UK-qualified principal.

Can a company director prepare statutory accounts themselves?

There is no legal requirement to use a qualified accountant for most companies (except where audit is mandatory). Directors of micro-entities can self-prepare, but iXBRL tagging requirements, accounting standard complexity, and penalty risk make professional help strongly advisable in practice.

UK statutory accounts carry real deadlines and penalties — and for international companies running UK subsidiaries, the compliance picture is more layered than it first appears. Working with advisors who have hands-on experience across both UK regulatory requirements and cross-border structures means fewer surprises at year-end.