Introduction

UK small business owners face a persistent challenge: while trying to grow their companies, they're drowning in financial admin. Sage research from May 2025 found that UK SMBs lose 24 days per year to financial administration (the equivalent of working 13 months but getting paid for only 12). Nearly 49% of small business CEOs spend four hours weekly just dealing with payment issues.

The financial cost of poor bookkeeping is direct and measurable. Research from Dext estimates UK SMBs lose an average of £742 every month from incorrect invoicing stemming from poor expense tracking, with 68.6% reporting a direct impact on growth.

Getting the fundamentals right changes that picture entirely. This guide clarifies the difference between bookkeeping and accounting, outlines essential practices and UK tax obligations, helps you choose the right accounting setup, and covers best practices to keep your business compliant and financially healthy.

Key Takeaways

- Bookkeeping captures daily transactions; accounting interprets that data to inform strategy and ensure compliance

- UK businesses must meet HMRC obligations: Corporation Tax, VAT (if applicable), PAYE, and Making Tax Digital requirements

- Choose your setup (software, in-house, or outsourced) based on your business size, complexity, and growth stage

- Consistent record-keeping prevents HMRC penalties, cash flow surprises, and costly gaps that push small businesses to close

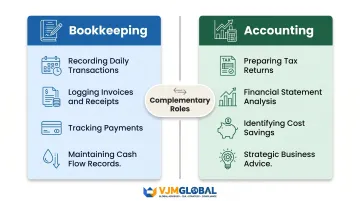

Bookkeeping vs Accounting: Understanding the Difference

Bookkeeping and accounting serve distinct but complementary roles. According to the Association of Accounting Technicians, bookkeeping focuses on recording and organising financial data, while accounting interprets and presents that data.

Here's how the two functions differ in practice:

- Bookkeeping covers day-to-day transaction recording — logging invoices, tracking receipts, recording payments, and maintaining accurate cash flow records

- Accounting takes that raw data and analyses it: preparing tax returns, assessing business health through financial statements, identifying cost-saving opportunities, and providing strategic advice

In your business's early stages, you'll likely handle both functions yourself. As you grow, the roles typically separate — your bookkeeper maintains current records, while your accountant interprets them quarterly or annually and manages compliance filings.

Legal Record Retention Requirements

UK businesses must retain financial records for specific periods based on their structure:

| Entity Type | Retention Period |

|---|---|

| Sole traders | 5 years after the 31 January submission deadline (effectively ~6 years from tax year end) |

| Limited companies | 6 years from the end of the financial year |

Source: GOV.UK record-keeping guidance

Directors who fail to keep adequate accounting records can face fines up to £3,000. Organised, consistent bookkeeping isn't just good practice — it's a legal obligation with real financial consequences.

Essential Bookkeeping Practices for UK Small Businesses

Effective bookkeeping starts with proper foundations. The first critical step is separating business and personal finances from day one.

Limited companies must legally maintain separate banking — your company is a distinct legal entity, and GOV.UK states "there must be a clear division between the company's finances and those of the owners and directors."

Sole traders face no legal requirement for a separate business bank account, but doing so simplifies record-keeping enormously, makes tax preparation straightforward, and prevents the nightmare of sorting through mixed personal and business transactions at year-end.

Maintaining Core Financial Records

Every UK small business must maintain three fundamental records:

- Cashbook — records all money in and out: sales receipts, expense payments, bank transfers, and cash transactions. Every other financial report traces back to this.

- Sales invoice file — tracks everything sold, paid and unpaid. Sequential numbering, clear payment terms, and monitoring outstanding amounts prevent cash flow gaps.

- Purchase invoice file — logs what you've bought and whether it's been paid. Organised purchase records help you claim every allowable deduction and avoid paying suppliers twice.

Bank Reconciliation

Bank reconciliation matches your accounting records to your actual bank statement, ideally monthly. This process catches:

- Timing differences (cheques not yet cleared)

- Bank charges you haven't recorded

- Failed or reversed payments

- Errors in data entry

Regular reconciliation prevents year-end surprises. When your books show £15,000 in the bank but your statement shows £12,000, monthly reconciliation catches the gap before it compounds into a much larger problem.

Tracking Expenses and Claiming Deductions

Tracking allowable business expenses directly reduces your taxable profit. HMRC permits deductions for:

- Office costs (supplies, software, utilities)

- Travel expenses (business mileage, public transport, accommodation)

- Staff costs (salaries, pensions, training)

- Professional fees (accountant, solicitor, membership subscriptions)

- Marketing and advertising

- Insurance and bank charges

Critical requirement: HMRC requires receipts and invoices as evidence for all claimed expenses. Dext research found that 69% of SMB leaders say untracked expenses leave them uncertain about outstanding liabilities. Organising receipts by category throughout the year is far easier than reconstructing months of spending at filing time.

The Three Golden Rules of Bookkeeping

Double-entry bookkeeping rests on three conceptual foundations:

- Debit the receiver, Credit the giver — debit the account receiving value; credit the account giving it

- Debit what comes in, Credit what goes out — assets entering the business are debited; assets leaving are credited

- Debit all expenses and losses, Credit all incomes and gains — costs and losses sit on the debit side; revenue and gains on the credit side

When any of these rules is applied incorrectly, your trial balance won't reconcile — a reliable early warning that something has been recorded wrong. Most accounting software applies these rules automatically, but understanding them helps you spot and fix errors quickly.

UK Tax Obligations Every Small Business Must Know

Missing HMRC deadlines costs money — penalties and interest accumulate fast. While obligations vary by business structure, the requirements below apply to most UK small businesses.

Corporation Tax

Limited companies pay Corporation Tax on taxable profits. Since April 2023, the UK operates a dual-rate structure:

| Profit Level | Tax Rate |

|---|---|

| Under £50,000 | 19% (small profits rate) |

| £50,000 - £250,000 | Marginal Relief applies |

| Over £250,000 | 25% (main rate) |

Source: GOV.UK Corporation Tax rates

Filing deadline: Submit your Company Tax Return (CT600) within 12 months of your accounting period end.

Payment deadline: Pay Corporation Tax within 9 months and 1 day of your accounting period end.

Late filing penalties:

| Time After Deadline | Penalty |

|---|---|

| 1 day | £200 |

| 3 months | Another £200 |

| 6 months | 10% of unpaid tax |

| 12 months | Another 10% of unpaid tax |

If you file late three times in a row, the £200 penalties increase to £1,000 each.

VAT (Value Added Tax)

Businesses must register for VAT once their VAT-taxable turnover exceeds £90,000 over any rolling 12-month period (increased from £85,000 on 1 April 2024).

Main VAT schemes:

| Scheme | Eligibility | How It Works |

|---|---|---|

| Standard VAT Accounting | All VAT-registered businesses | Pay VAT based on invoice dates; file quarterly returns |

| Cash Accounting Scheme | Turnover ≤ £1.35 million | Pay VAT when customers pay you; reclaim when you pay suppliers — improves cash flow for businesses with slow-paying customers |

| Flat Rate Scheme | Turnover ≤ £150,000 (excl. VAT) | Pay a fixed percentage of gross turnover by sector; simpler calculations but no VAT reclaim on most purchases |

VAT penalties: From January 2023, HMRC uses a points-based system. Quarterly filers accumulate penalty points for each late return; reaching 4 points triggers a £200 penalty for each subsequent late return. Late payments incur 3% of outstanding amounts at day 15, plus another 3% at day 30.

PAYE and National Insurance

Businesses with employees must operate PAYE (Pay As You Earn), deducting Income Tax and National Insurance Contributions from wages before paying employees, then remitting these to HMRC monthly.

Critical requirements:

- Register with HMRC before your first payday (you cannot register more than 2 months in advance)

- Report all employee pay and deductions to HMRC on or before each payday using Real Time Information (RTI) via Full Payment Submissions (FPS)

- Use payroll software to calculate and submit returns accurately

Making Tax Digital (MTD)

Beyond payroll reporting, HMRC's Making Tax Digital initiative is extending digital record-keeping requirements across the board.

MTD for VAT — already mandatory for all VAT-registered businesses. You must use MTD-compatible software to file all VAT returns.

MTD for Income Tax Self Assessment (ITSA) — rolling out in stages:

| Start Date | Qualifying Income Threshold |

|---|---|

| 6 April 2026 | Over £50,000 |

| 6 April 2027 | Over £30,000 |

| 6 April 2028 | Over £20,000 |

Affected sole traders and landlords must maintain digital records, send quarterly updates to HMRC using compatible software, and submit a Final Declaration by 31 January following the tax year end.

If you haven't already, selecting MTD-compatible software now avoids a last-minute scramble. Xero, QuickBooks, Sage, and FreeAgent are all HMRC-recognised for both VAT and Income Tax.

Choosing Your Accounting Setup: Software, In-House, or Outsourcing

Accounting Methods: Cash Basis vs Accrual

Two main accounting methods exist:

Cash basis records income when money actually arrives and expenses when you actually pay them. Simpler and better for very small businesses. From the 2024-25 tax year, HMRC removed the £150,000 turnover cap — all eligible sole traders and partnerships can now use cash basis regardless of turnover. Limited companies cannot use this method.

Accrual accounting records income when earned and expenses when incurred, regardless of when money changes hands. Provides a more accurate financial picture, particularly for growing businesses with extended payment terms or inventory.

Many businesses start on cash basis and transition to accrual as they scale and require more sophisticated financial visibility.

Accounting Software Options for UK Small Businesses

Modern cloud accounting software automates record-keeping, ensures MTD compliance, and provides real-time financial visibility. The most popular UK platforms include:

Key features to prioritise:

- MTD compliance for VAT and Income Tax

- Bank feed integration (automatic transaction import)

- VAT return filing capability

- Payroll functionality

- Mobile app access

- Ease of use for non-accountants

Pricing overview (entry-level monthly rates, excluding VAT):

| Platform | Starting From | Mid-Tier | Notes |

|---|---|---|---|

| Xero | £7/mo | £16/mo | Strong SMB features, excellent bank feeds |

| QuickBooks | £10/mo | £14/mo | Intuitive interface, robust reporting |

| Sage | £7/mo | £18/mo | Free plans available for sole traders |

| FreeAgent | £19/mo | £33/mo | Free for NatWest/RBS business account holders |

Sources: Xero pricing, QuickBooks pricing, Sage pricing, FreeAgent pricing

Most platforms offer 50-90% discounts for the first 3-6 months and free trials — test before committing.

Outsourcing Your Bookkeeping and Accounting

As your business grows, time spent on bookkeeping and accounting can outweigh the cost of professional help. An external team handles daily transaction recording, monthly reconciliation, VAT returns, payroll, and tax filings — freeing you to focus on running and growing your business.

VJM Global has supported over 250 UK businesses with outsourced accounting, providing qualified Chartered Accountants, CPAs, and finance professionals experienced in HMRC compliance, UK accounting standards, and IFRS. Services include:

- Daily transaction recording and bookkeeping

- Monthly bank reconciliation

- VAT return preparation and filing

- Payroll processing and PAYE management

- Corporation Tax return preparation

- Financial reporting and management accounts

Businesses typically save up to 50% compared to hiring full-time in-house staff — making outsourcing a practical option once compliance admin starts eating into time you'd rather spend on the business itself.

In-House Management Considerations

In-house management is a viable alternative if you have a team member with accounting knowledge, or if your business is small enough to handle the workload yourself using software.

Key risks to consider:

- Significant time commitment that pulls you from core business activities

- Potential for errors without professional oversight

- You remain fully responsible for accuracy of all HMRC submissions regardless of who prepares them

- Difficulty keeping current with changing tax regulations and compliance requirements

If choosing in-house management, invest in quality accounting software, maintain rigorous monthly routines, and budget for annual accountant review to catch errors before they reach HMRC.

Bookkeeping Best Practices and Common Mistakes to Avoid

Consistent monthly bookkeeping routines prevent errors from compounding. Review and reconcile accounts each month rather than at year-end. Produce at minimum a monthly profit and loss statement and balance sheet to track performance and spot trends early.

Monthly bookkeeping routine:

- Reconcile bank and credit card accounts

- Chase outstanding invoices

- Review expenses and ensure all receipts are captured

- Update VAT records

- Run P&L and balance sheet reports

- Review cash flow forecast

Routine habits keep records clean — but even disciplined businesses fall into predictable traps.

Common Bookkeeping Mistakes

UK small businesses frequently make these costly errors:

Mixing personal and business expenses — creates chaos at tax time and raises red flags with HMRC. Use a dedicated business account even if you're a sole trader.

Falling behind on record updates — letting bookkeeping slip for weeks or months compounds errors. Monthly updates take 2-3 hours; year-end catch-up can take days.

Missing VAT deadlines — the points-based penalty system escalates quickly. Set reminders one week before each deadline.

Failing to save receipts — HMRC can disallow expenses without supporting documentation. Use receipt-scanning apps to capture and categorise in real-time.

Not tracking accounts receivable — money owed but unmonitored becomes cash flow gaps. Without a weekly review of outstanding invoices, overdue accounts slip through unnoticed until the damage is done.

Credit Control as Bookkeeping Discipline

Late payments threaten cash flow more than almost any other factor. FSB research shows 52% of small firms experience late payments, costing up to £5,200 per year in lost productivity — and the FSB estimates 50,000 UK businesses close annually due to the same problem.

Credit control best practices:

- Invoice promptly (within 24 hours of completing work)

- Set clear payment terms upfront (e.g., "Net 30 days")

- Number invoices sequentially for tracking

- Send payment reminders at 7 days before due date, on due date, and 7 days after

- Implement late payment charges where contractually agreed

- Review aged debtor reports weekly and escalate overdue accounts systematically

Treat credit control as a non-negotiable part of your monthly close — not an afterthought when cash runs short.

Frequently Asked Questions

How much does an accountant cost for a small business in the UK?

Typical monthly fees range from £60 to £450, depending on business structure and services required. Sole traders generally pay £100-200 monthly for basic compliance work, while limited companies requiring bookkeeping, VAT, payroll, and Corporation Tax support typically pay £200-400 monthly. Pricing varies based on transaction volume, industry complexity, and whether you need advisory services beyond compliance.

Do I need an accountant for my small business in the UK?

There's no legal requirement to hire an accountant — you can prepare and file your own tax returns. However, most small businesses benefit from professional support, particularly for Corporation Tax filings, VAT management, and strategic tax planning. For many small businesses, outsourced accounting costs less than a full-time hire while providing the same level of qualified expertise.

How much should I pay a bookkeeper in the UK?

Freelance bookkeepers typically charge £10–25 per hour, with annual salaries for in-house bookkeepers ranging from £20,000 to £41,000 depending on location, qualifications, and experience. London rates sit at the upper end of both ranges.

What is the best accounting software for small business in the UK?

The most widely used options are Xero, QuickBooks Online, FreeAgent, and Sage — all MTD-compliant with strong bank feed integration. FreeAgent is free for NatWest and RBS business account holders. Run a free trial before committing to confirm it fits your workflow.

What are the three golden rules of bookkeeping?

The three golden rules underpin double-entry bookkeeping: (1) Debit the receiver, Credit the giver; (2) Debit what comes in, Credit what goes out; (3) Debit all expenses and losses, Credit all incomes and gains. These principles ensure every transaction affects two accounts, keeping your books balanced and creating the audit trail HMRC requires.

What is a bookkeeper not allowed to do?

Bookkeepers are not legally authorised to provide formal tax advisory services, prepare statutory accounts for limited companies, or represent a business before HMRC in disputes or investigations. These tasks require a qualified, regulated accountant (chartered via ICAEW, ACCA, or CIMA). ICB-certified bookkeepers can handle daily transactions, VAT returns, payroll, and management accounts, but complex tax planning and statutory audit work remain outside their scope.