However, navigating Singapore's audit compliance requirements can be challenging, particularly for foreign-owned companies and multinational corporations unfamiliar with local regulations. Many businesses struggle to understand when statutory audits are mandatory, which exemptions apply, and how to meet ACRA (Accounting and Corporate Regulatory Authority) and IRAS (Inland Revenue Authority of Singapore) filing deadlines without incurring penalties.

This guide provides a comprehensive overview of Singapore's audit regulatory framework, covering the Singapore Standards on Auditing (SSAs), statutory audit obligations, exemption criteria, accounting standards, filing requirements, and penalties for non-compliance.

Key Takeaways

- Most Singapore private companies must undergo annual statutory audits unless they qualify for a small company, small group, or dormant company exemption

- Singapore's audit standards (SSAs) are closely aligned with International Standards on Auditing (ISAs), ensuring global consistency

- Small companies qualifying on two of three thresholds (revenue, assets ≤S$10M; ≤50 employees) for two consecutive years may be exempt

- Singapore uses SFRS, which is based on IFRS—not US GAAP—a key distinction for foreign investors

- Non-compliance can mean fines up to S$5,000, director disqualification, and reputational damage with investors and lenders

Singapore's Audit Regulatory Framework

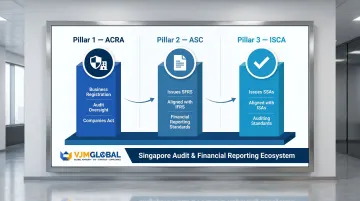

Singapore's audit and financial reporting ecosystem is governed by three primary regulatory bodies working in concert:

ACRA: The Central Regulator

The Accounting and Corporate Regulatory Authority (ACRA) is Singapore's national regulator overseeing business registration, financial reporting, public accountants, and corporate service providers. ACRA's mandate includes administering the Companies Act, Accountants Act, and several other key pieces of legislation.

Only public accountants registered with ACRA can conduct statutory audits in Singapore. ACRA also conducts quality assurance reviews and inspections of audit firms to maintain consistent professional standards.

Since July 2023, ACRA's inspection powers have expanded to include quality control reviews of accounting entities, giving ACRA broader oversight of audit firm practices.

ASC and ISCA: Standards and Professional Guidance

The Accounting Standards Council (ASC), operating under ACRA, has statutory authority to issue Singapore Financial Reporting Standards (SFRS), which are aligned with IFRS Standards.

The Institute of Singapore Chartered Accountants (ISCA) issues the Singapore Standards on Auditing (SSAs), based directly on International Standards on Auditing (ISAs) from the IAASB. Each SSA maps to its ISA equivalent — for example, SSA 700 (Revised) aligns with ISA 700 (Revised).

Together, ASC and ISCA cover the two pillars of Singapore's standards landscape:

- ASC sets financial reporting standards (what companies report)

- ISCA sets auditing standards (how auditors examine those reports)

IRAS: Tax Compliance Partner

The Inland Revenue Authority of Singapore (IRAS) handles tax reporting obligations separately from ACRA. All companies must file Estimated Chargeable Income (ECI) within three months of their financial year-end, unless they qualify for a waiver (annual revenue not exceeding S$5 million and ECI is nil).

Companies must satisfy obligations to both ACRA and IRAS. Failing either can result in penalties, court summons, or director disqualification.

Singapore Standards on Auditing (SSAs): What They Cover

The Singapore Standards on Auditing (SSAs) define how auditors conduct audits of financial statements in Singapore. Because SSAs are based on ISAs, Singapore's auditing practices align with global norms, making it easier for international investors and counterparties to assess audit quality.

Core Principles of SSAs

SSAs are built on three foundational principles:

- Critically evaluate evidence and challenge assumptions rather than accepting information at face value (professional skepticism)

- Form conclusions using knowledge, experience, and understanding of the entity's specific context

- Maintain independence, objectivity, and confidentiality throughout every engagement

Key Areas Covered by SSAs

Risk Assessment

Auditors identify and assess risks of material misstatement by understanding the entity's business environment, internal controls, and industry context. SSA 315 (Revised 2021), effective December 2022, provides detailed guidance on this process — including how auditors should respond when control deficiencies increase risk exposure.

Audit Evidence

SSAs prescribe the nature, timing, and extent of audit procedures required to gather sufficient and appropriate evidence. These procedures include:

- Inspection of records and documents

- Observation of processes and controls

- Inquiry of management and staff

- Confirmation from third parties

- Recalculation and reperformance of transactions

Reporting Standards

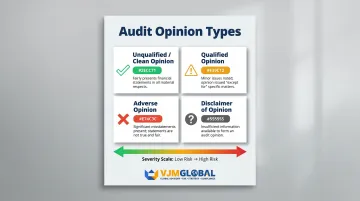

SSA 700 (Revised) outlines the required form and content of the auditor's report, including when modified opinions apply. The type of opinion issued signals the degree of confidence auditors can provide. The four opinion types are:

| Opinion Type | Description |

|---|---|

| Unqualified (Clean) | Financial statements fairly present the company's position in all material respects |

| Qualified | Minor issues exist but don't significantly affect overall accuracy ("except for" opinion) |

| Adverse | Significant misstatements mean financial statements don't present a true and fair view |

| Disclaimer | Auditors couldn't obtain sufficient information to form an opinion |

Enforcement and Updates

ACRA conducts regular quality assurance reviews and inspections to ensure audit firms comply with SSAs. The Audit Regulatory Report 2024 highlights common inspection findings to help firms identify weaknesses and strengthen audit quality.

Staying current with SSA updates is equally important. ISCA regularly revises standards to reflect changes in accounting practices and emerging risks. Recent updates include SSA 315 (Revised 2021), SSA 700 (Revised) updated in July 2022 and December 2023, and SSA 805 (Revised) issued in May 2026.

Who Is Required to Be Audited in Singapore?

Statutory Audit Mandate

Under Section 201(8) of the Companies Act, all private limited companies must have their financial statements audited by a qualified public accountant annually, unless they qualify for an exemption. All public companies are subject to mandatory audit regardless of size—exemptions apply only to private companies.

Auditor Appointment Requirements

Section 205 of the Companies Act requires directors to appoint an ACRA-registered auditor within three months of incorporation. The auditor's role is to examine the financial statements and express an opinion on whether they give a true and fair view of the company's financial position and comply with applicable financial reporting standards.

Scope of Statutory Audits

Auditors examine:

- Balance sheet and statement of financial position

- Income statement (profit and loss)

- Cash flow statement

- Notes to the accounts

- Internal controls and risk management processes

The auditor's report required under Section 207 must state whether the financial statements give a "true and fair view" and comply with the Companies Act and applicable Financial Reporting Standards.

Foreign-Owned Companies

Foreign-owned companies incorporated in Singapore are subject to the same statutory audit obligations as locally owned entities. As of 2022, there were approximately 60,300 majority foreign-owned companies registered in Singapore, employing 1.2 million Singaporeans.

For multinationals, this means Singapore audit obligations must align with reporting requirements in their home jurisdiction — making it important to understand how local standards interact with group-level consolidation or parent company filings.

Audit Exemptions in Singapore

Singapore's Companies Act provides three statutory exemption categories that relieve qualifying companies from mandatory audit requirements. Understanding which applies to your structure can significantly reduce compliance overhead.

Small Company Exemption

Section 205C of the Companies Act provides an audit exemption for companies that qualify as "small companies." To qualify, a company must be a private company throughout the financial year and meet at least two of the following three criteria for the immediate past two consecutive financial years:

- Total annual revenue ≤ S$10 million

- Total assets ≤ S$10 million

- No more than 50 full-time employees

Small Group Exemption

If a company is part of a corporate group (holding company and subsidiaries), the individual company must qualify as a small company and the entire group must qualify as a small group using the same two-of-three thresholds on a consolidated basis for two consecutive years.

This prevents large groups from claiming exemptions for individual subsidiaries that happen to fall below the thresholds.

Dormant Company Exemption

Section 205B exempts companies that have been dormant since incorporation or since the end of the previous financial year. A company is dormant when no accounting transactions occur (excluding prescribed transactions such as appointment of company secretary or filing fees).

Additionally, dormant companies whose total assets do not exceed S$500,000 at any time during the financial year are exempt from preparing and filing financial statements.

Disqualification Triggers

A company loses audit exemption status if:

- It ceases to be a private company at any point during the financial year

- It fails to meet two of the three qualifying criteria for two consecutive financial years

Annual eligibility reviews are advisable — the revenue and total assets thresholds are the criteria most commonly breached as businesses scale, and a breach in one year starts the two-year clock toward losing exempt status.

Obligations of Exempt Companies

Even without a statutory audit, exempt companies must:

- Prepare unaudited financial statements (unless qualifying as a dormant relevant company with assets ≤S$500,000)

- Maintain proper accounting records

- Lodge annual returns with ACRA within prescribed timelines

- Fulfill all IRAS tax filing obligations, including ECI and Form C-S/C

Accounting Standards and Filing Obligations

Singapore Financial Reporting Standards (SFRS)

Singapore follows the Singapore Financial Reporting Standards (SFRS), issued by the ASC and fully aligned with IFRS Standards. The 2026 volume contains 43 individual standards covering areas such as revenue recognition, inventory, financial instruments, and leases, plus 20 SFRS Interpretations.

Because SFRS aligns with IFRS rather than US GAAP, international investors can compare Singapore financial statements directly with those from other IFRS-aligned jurisdictions — a practical advantage for cross-border operations.

SFRS for Small Entities

The SFRS for Small Entities is a simplified reporting framework for qualifying entities. To qualify, an entity must:

- Not be publicly accountable

- Meet at least two of three criteria: revenue ≤S$10 million, assets ≤S$10 million, ≤50 employees

XBRL Filing Requirements

Most companies must file financial statements with ACRA in XBRL (eXtensible Business Reporting Language) format:

| Company Type | Filing Requirement |

|---|---|

| Public companies; non-EPC private companies (revenue or assets >S$5M) | Full XBRL + PDF |

| Non-EPCs with revenue ≤S$5M and assets ≤S$5M | Simplified XBRL + PDF |

| Solvent Exempt Private Companies (EPCs) | Declaration of Solvency only |

| Dormant companies (assets ≤S$500K) | Exempt from filing FS |

Annual Return Deadlines

Under Section 197 of the Companies Act, companies must lodge annual returns with ACRA within:

- 5 months after financial year-end for listed public companies

- 7 months after financial year-end for all other companies

If an Annual General Meeting (AGM) is held, the annual return must be filed within one month following the meeting.

Penalties and Deadlines for Non-Compliance

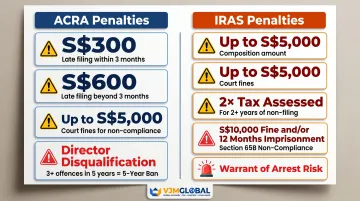

ACRA Late Filing Penalties

ACRA applies a two-tier penalty framework for late annual returns:

- S$300 if filed within 3 months after the due date

- S$600 if filed more than 3 months after the due date

For persistent non-compliance, ACRA may offer a composition sum or prosecute in court, with potential fines up to S$5,000 per offence.

IRAS Tax Penalties

Late or non-filing of Corporate Income Tax Returns carries significant consequences:

- Composition amounts up to S$5,000 per offence

- Court conviction fines up to S$5,000 per offence

- Failure to file for 2+ years: Penalty of twice (2x) the tax assessed, plus fines up to S$5,000 per offence

- Directors may receive Section 65B(3) notices requiring information submission; non-compliance can result in fines up to S$10,000 and/or 12 months' imprisonment

- Failure to attend court may result in a warrant of arrest

Director Disqualification

Under Section 155A of the Companies Act, ACRA will disqualify directors who:

- Are convicted of three or more filing offences within five years

- Were directors of three or more companies struck off under Section 344 within the preceding five years

Disqualification lasts five years and prevents the individual from acting as a director of any Singapore company.

Broader Consequences

Beyond financial penalties, non-compliance damages a company's credibility with banks, investors, and regulatory bodies. This makes it harder to:

- Secure loans or credit facilities

- Attract investors or venture capital

- Expand operations or win contracts

- Maintain professional relationships with partners and clients

Companies should regularly review eligibility thresholds and monitor filing deadlines across both ACRA and IRAS. This is especially critical for fast-growing businesses that may cross statutory exemption thresholds mid-cycle, where engaging a qualified audit or advisory professional can prevent costly oversights.

Frequently Asked Questions

Does Singapore use IFRS or GAAP?

Singapore uses the Singapore Financial Reporting Standards (SFRS), which are based on IFRS (International Financial Reporting Standards)—not US GAAP. This alignment makes it easier for international investors to compare Singapore financial statements with those from other IFRS-aligned countries.

What is an SSA in Singapore?

SSA stands for Singapore Standard on Auditing. These are official auditing standards issued by ISCA that guide how auditors conduct audits of financial statements in Singapore. SSAs are closely aligned with International Standards on Auditing (ISAs) issued by the IAASB.

Who is required to conduct a statutory audit in Singapore?

All public companies and private companies that do not qualify for the small company, small group, or dormant company exemption must undergo a statutory audit annually. The audit must be conducted by an ACRA-registered public accountant.

What are the criteria for small company audit exemption in Singapore?

A private company qualifies for audit exemption if it meets at least two of three thresholds for two consecutive financial years: annual revenue ≤S$10 million, total assets ≤S$10 million, and no more than 50 full-time employees.

What happens if a company fails to comply with audit requirements in Singapore?

Non-compliance carries serious consequences:

- Fines up to S$5,000 and court summons from ACRA

- Personal liability and potential director disqualification

- Reputational damage affecting financing and investor confidence

How does the Singapore audit framework apply to foreign-owned companies?

Foreign-owned companies incorporated in Singapore face the same statutory audit and financial reporting obligations as locally owned entities. This includes SSA-compliant audits, ACRA filings, and SFRS-based financial statement preparation.