Introduction

Thousands of UK small and medium-sized enterprises leave significant R&D tax relief unclaimed every year—not because they're ineligible, but because the enhanced deduction mechanism remains widely referenced yet poorly understood in practice. According to HMRC's latest statistics, SME scheme claims fell 31% to 36,885 in 2023-24, with total relief value dropping 29% to £3.15 billion. Many businesses are simply uncertain about eligibility or put off by the compliance burden introduced through recent reforms.

The SME R&D enhanced deduction scheme lets eligible companies claim additional tax relief on qualifying R&D expenditure — reducing taxable profits for profitable businesses or generating a payable cash credit for loss-making ones.

This guide is written for UK SME owners, finance directors, and startup founders navigating how the scheme works, what rates currently apply, and what changed following HMRC's significant 2023 and 2024 reforms.

Here's what this guide covers:

- Enhanced deduction calculation methodology and current rates

- Eligibility criteria for the SME scheme

- Impact of rate reductions and the merged scheme

- The ERIS carve-out for R&D-intensive SMEs

- Qualifying expenditure categories

- The mandatory Additional Information Form

Key Takeaways

- The SME R&D enhanced deduction scheme lets qualifying UK companies claim extra tax relief on R&D expenditure—now 86% additional deduction from April 2023, down from 130%

- Loss-making SMEs surrender the enhanced loss for a payable 10% cash credit from HMRC

- From April 2024, most SMEs fall under the merged RDEC-style scheme; loss-making R&D-intensive SMEs access higher rates through Enhanced R&D Intensive Support (ERIS)

- Qualifying as an SME requires fewer than 500 employees and meeting turnover/balance sheet thresholds across all linked entities

- All claims since August 2023 require a mandatory Additional Information Form submitted before the tax return

What Is the SME R&D Enhanced Deduction Scheme and Who Qualifies?

The SME R&D enhanced deduction scheme is a UK corporation tax relief allowing SMEs to deduct more than the actual cost of qualifying R&D from taxable profits. The "enhancement" is the additional percentage on top of the standard 100% deduction — currently 86%, reduced from 130% before April 2023.

Profitable companies use this to reduce their corporation tax bill. Loss-making companies can instead claim a payable cash credit directly from HMRC.

This contrasts with the RDEC (Research and Development Expenditure Credit) scheme designed for larger companies. RDEC operates as an "above-the-line" credit that appears as taxable income in accounts; the legacy SME deduction reduces taxable profit below the line.

Since April 2024, most companies — including profitable SMEs — use the merged RDEC-style scheme. The distinction still matters for historical claims and businesses eligible for Enhanced R&D Intensive Support (ERIS).

Qualifying as an SME

HMRC applies EU-derived thresholds to determine SME status. Your company must meet all three criteria:

Core requirements:

- Fewer than 500 employees

- Annual turnover under €100 million OR

- Gross balance sheet assets under €86 million

These thresholds are assessed at group level. If your company is 25% or more owned by or linked to another entity, you must aggregate those entities' figures when calculating eligibility. Companies receiving government grants or performing R&D under contract for another party may be excluded from the SME scheme for those specific projects, though they may qualify under RDEC or merged scheme rules instead.

The 25% ownership trigger catches many businesses off guard — a company that looks like an SME on its own can fail the test once parent or sister company figures are included.

How SME R&D Enhanced Deductions Are Calculated

The enhanced deduction mechanism works by adding a percentage enhancement on top of actual R&D spend, creating "enhanced expenditure" that's deducted from profits. Currently, the enhancement is 86% (reduced from 130% pre-April 2023). On £100 of qualifying R&D spend, you deduct £186 total: the original £100 plus £86 enhancement.

Profit-Making SME Calculation

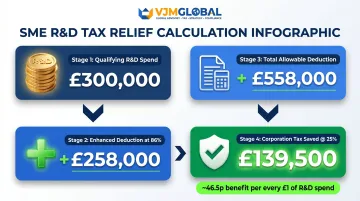

Example: An SME spends £300,000 on qualifying R&D.

- Actual R&D expenditure: £300,000

- Enhancement at 86%: £258,000

- Total deduction: £558,000 (£300,000 + £258,000)

- Corporation tax saved at 25%: £139,500

The company reduces its taxable profit by £558,000, saving approximately £139,500 in corporation tax. That's a net benefit of roughly 46.5p per £1 of R&D spend for profitable companies.

Loss-Making SME Calculation

Loss-making SMEs surrender the enhanced loss for a payable tax credit at 10% (reduced from 14.5% pre-April 2023).

Example: An SME spends £300,000 on qualifying R&D and makes a trading loss.

- Actual R&D expenditure: £300,000

- Enhancement at 86%: £258,000

- Enhanced expenditure added to loss: £258,000

- Surrenderable loss (the loss eligible for conversion to a cash credit): £258,000

- Payable credit at 10%: £25,800

The company receives a £25,800 cash payment from HMRC, approximately 8.6p per £1 of R&D spend. Combined with the original deduction, the total benefit is approximately 18.6p per £1.

PAYE and NIC Cap

For accounting periods beginning on or after 1 April 2021, a cap applies to the payable cash credit. HMRC sets this at £20,000 plus 300% of total PAYE and Class 1 NIC liability. Key rules to know:

- The £20,000 de minimis protects small, genuine claims from being affected by the cap

- Companies with minimal UK payroll face the greatest restrictions under this limit

- Exemption may apply where employees create the IP and the company doesn't extensively subcontract to connected parties

Externally Funded R&D

If a project receives government grants or is performed as a subcontractor for another company, SME relief isn't available for that project. You'd claim under merged/RDEC rules instead. This is assessed project-by-project, so some projects can sit under SME rules while others fall under RDEC simultaneously.

One significant change from April 2024: the subsidised-expenditure restriction was not carried forward into the merged scheme, meaning grant-funded R&D is now fully claimable under the new regime.

Rate Changes and the Shift to ERIS and the Merged Scheme

Rate History and Impact

Before April 2023:

- Enhanced deduction: 130%

- Loss-making payable credit: 14.5%

- Net benefit for loss-making SMEs: approximately 33p per £1

From 1 April 2023:

- Enhanced deduction: 86%

- Loss-making payable credit: 10%

- Net benefit for loss-making SMEs: approximately 18.6p per £1

This reduction from 33p to 18.6p represents a 44% cut in net cash benefit for non-R&D-intensive loss-making SMEs. According to HMRC's published R&D tax relief statistics, SME claim volume fell 31% and relief value dropped 29% in the first year following the rate reductions.

Enhanced R&D Intensive Support (ERIS)

ERIS was created to protect loss-making SMEs spending a disproportionately high share of total expenditure on R&D. Qualifying companies access the 14.5% payable credit rate rather than the reduced 10%, effectively restoring pre-April 2023 benefit levels for the most R&D-heavy businesses.

R&D intensity thresholds:

- April 2023 to March 2024: 40%

- From April 2024 onwards: 30%

To calculate intensity, divide qualifying R&D expenditure (including connected companies) by total relevant trading expenditure (also including connected companies).

Total relevant expenditure includes costs under GAAP, pre-trading costs, and specific deductions. Payments to connected companies are excluded to prevent double-counting.

A one-year grace period applies from April 2024. If your R&D intensity drops below 30% in a given year but you met the threshold and successfully claimed in the previous year, you can continue claiming ERIS, preventing sudden loss of eligibility due to year-on-year fluctuation.

ERIS benefit: Approximately 27p per £1 of R&D spend (186% × 14.5% = 26.97p).

The Merged Scheme (April 2024 Onwards)

ERIS is the exception to a broader restructuring of UK R&D relief. For accounting periods beginning on or after 1 April 2024, most companies, including profitable SMEs, claim under the merged RDEC-style scheme at a 20% above-the-line credit.

R&D relief now appears as taxable income in accounts before tax, with a net benefit of approximately 15p-16p per £1 spent after 25% corporation tax (20% × 75% = 15%). Loss-making R&D-intensive SMEs meeting ERIS criteria are exempt from this merger and continue claiming under SME-style rules.

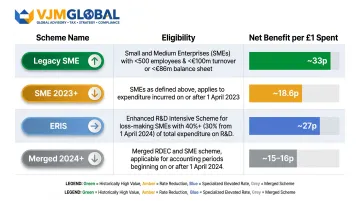

Scheme Comparison

Net benefit per £1 of R&D spend:

| Scheme | Eligibility | Net Benefit per £1 |

|---|---|---|

| Legacy SME (pre-April 2023) | Loss-making SMEs | ~33p |

| Post-April 2023 SME | Loss-making, non-intensive | ~18.6p |

| ERIS (April 2023+) | Loss-making, R&D-intensive | ~27p |

| Merged scheme (April 2024+) | Most companies, all tax positions | ~15p–16p |

The merged scheme's headline rate is lower, but it removed restrictions on subsidised expenditure. For grant-funded SMEs, that change partly offsets the apparent reduction in benefit.

What Costs Qualify for SME R&D Enhanced Deductions?

Core Qualifying Categories

Staff costs:

- Salaries, wages, and bonuses

- Employer National Insurance contributions

- Pension contributions

- Only for employees directly working on R&D activities

Subcontractor costs:

- 65% of payments to unconnected subcontractors qualify

- Connected subcontractors subject to specific rules under merged scheme

- Must relate directly to R&D project work

Consumable items:

- Materials used or transformed in R&D

- Water, fuel, and power consumed

- Revenue expenditure only—capital purchases excluded

Capital expenditure on equipment generally doesn't qualify for R&D relief but may be covered separately by capital allowances.

These core categories cover the majority of qualifying spend for most SMEs. From April 2023, three additional categories expanded the scope significantly.

Expanded Categories from April 2023

HMRC added three new qualifying cost categories for accounting periods starting on or after 1 April 2023:

Cloud computing costs:

- Service fees for cloud infrastructure used in R&D

- Must contribute directly to resolving scientific or technological uncertainty

- Set-up costs likely capital and excluded

Data costs:

- Dataset licence fees used in R&D activities

- Must be used specifically to resolve scientific or technological uncertainty

- Outright data purchases typically capital and don't qualify

Pure mathematics:

- Work relating to pure mathematics now meets R&D definition

- Significant expansion for data science and algorithm-focused businesses

Knowing what qualifies is only half the picture. Understanding what falls outside these categories is just as important for avoiding costly errors.

What Does NOT Qualify

Common exclusions that trip up claimants:

- Routine or incremental improvements without genuine scientific or technological uncertainty

- Market research, consumer behaviour studies, and social science work

- Adapting existing technology for new contexts without overcoming genuine uncertainty

- Creative or commercial innovation that doesn't involve science or technology advance

HMRC estimated a 14.7% error and fraud rate in the SME scheme for 2022-23, totalling £652 million. Overclaiming is the most common trigger for HMRC enquiries and penalties, so accurately mapping costs to qualifying activities before submitting a claim is essential.

Common Misconceptions and HMRC Scrutiny

The Innovation ≠ R&D Misconception

The most common error is assuming any innovative or new product development automatically qualifies as R&D for tax purposes. HMRC's test requires attempting to achieve an advance in science or technology by overcoming genuine uncertainty that a competent professional in the field couldn't readily resolve.

Practical examples:

- Building a new app using existing frameworks = NOT R&D

- Developing a genuinely novel algorithm solving an unresolved technical problem = potentially R&D

- Creating a unique customer experience through design = NOT R&D

- Overcoming technical limitations in data processing no existing solution addresses = potentially R&D

Purely commercial or creative innovation doesn't meet the bar, regardless of how innovative it feels to your business.

Additional Information Form (AIF) Requirement

Since 8 August 2023, all companies submitting R&D claims must file an AIF to HMRC online before or alongside their company tax return. The AIF requires:

- Detailed project descriptions

- Cost breakdowns by category

- Advisor details and involvement

- Senior internal R&D contact information

Failure to submit the AIF results in HMRC rejecting the claim outright. This is a common point of failure for companies filing without specialist support—the AIF isn't optional or discretionary.

HMRC's Increased Enforcement

HMRC has stepped up compliance activity:

- Over 500 compliance staff working on R&D claims (up from approximately 100 in 2021-22)—a five-fold increase

- Thousands of "nudge letters" issued to businesses with potentially non-compliant claims

- £652 million in SME scheme error and fraud identified for 2022-23

- Comptroller and Auditor General qualified HMRC's accounts due to R&D error levels

Critical: Responsibility for claim accuracy lies with your company, not with advisors. Errors can result in repayment of credits plus penalties and interest.

That risk makes thorough documentation and a defensible claim methodology non-negotiable. VJM Global has worked with 250+ UK businesses on tax compliance and advisory, including R&D claims that need to hold up under HMRC review—providing the structured, evidence-backed approach this environment demands.

Frequently Asked Questions

What is RDEC and how is it different from the SME R&D tax relief?

RDEC (Research and Development Expenditure Credit) was designed for large companies and works as an "above-the-line" taxable credit appearing as income in accounts, while the legacy SME scheme reduced taxable profits through enhanced deductions. From April 2024, most companies use the merged RDEC-style scheme, but loss-making R&D-intensive SMEs still access SME-style relief via ERIS.

Who is eligible for UK R&D tax credits?

Eligibility requires being a UK limited company subject to corporation tax, undertaking qualifying R&D activity that resolves genuine scientific or technological uncertainty. SME rules add EU-derived size thresholds: fewer than 500 employees with turnover and balance sheet limits assessed at group level. Sole traders and partnerships don't qualify.

How do R&D tax credits work in the UK?

Companies identify qualifying R&D expenditure and apply the relevant rate to either reduce their corporation tax liability (if profitable) or claim a payable cash credit from HMRC (if loss-making). Since April 2024, the merged scheme uses a 20% above-the-line credit, while ERIS-eligible SMEs retain the SME-style enhanced deduction and payable credit.

What is the SME R&D tax relief (enhanced deductions) and what rates apply?

The SME enhanced deduction allows qualifying small and medium-sized enterprises to deduct an additional 86% (from April 2023) of qualifying R&D expenditure on top of the standard 100% deduction. Loss-making SMEs surrender the enhanced loss for a 10% payable cash credit, while R&D-intensive SMEs qualifying under ERIS access the higher 14.5% rate. Verify current rates at GOV.UK, as these may change following Budget announcements.

How much R&D tax relief can a UK company claim?

The amount depends on scheme, tax position, and qualifying expenditure volume. Under the merged scheme, companies receive a 20% above-the-line credit (approximately 15p net per £1 after tax); under ERIS, loss-making R&D-intensive SMEs receive up to approximately 27p per £1. The PAYE/NIC cap limits maximum payable credits for SMEs.

What documentation does HMRC require when submitting an SME R&D tax credit claim?

Since August 2023, all claims require an Additional Information Form (AIF) submitted online to HMRC before or alongside the company tax return, covering project descriptions, qualifying costs, and advisor details. Companies should also maintain contemporaneous records of R&D activities, staff time allocations, and qualifying expenditure to support the claim and withstand any HMRC enquiry. The AIF is mandatory—no form means no claim.