Introduction

Miss your Company Tax Return deadline and HMRC won't wait — penalties start immediately and escalate fast. Every active UK limited company must file with HMRC after each accounting period, and errors or late submissions can trigger fines, interest charges, and compliance flags that are difficult to reverse.

Understanding the process matters even if you outsource to an accountant. This is especially true for foreign-owned companies and new directors who are unfamiliar with HMRC's filing requirements, deadlines, and format standards.

This guide explains what a Company Tax Return is, who must file, what documents are required, and exactly how to complete the process step by step. With significant changes to penalties and filing methods taking effect in 2026, directors need current, accurate guidance to maintain compliance.

Key Takeaways

- The CT600 form reports taxable profits and calculates the Corporation Tax your company owes HMRC

- All active UK limited companies must file — even with no tax liability or a trading loss

- File online within 12 months of your accounting period end

- Pay Corporation Tax earlier: the deadline is 9 months and 1 day after the period ends

- Late filing triggers automatic penalties starting at £200, doubling from April 2026

What Is a Company Tax Return in the UK?

A Company Tax Return is the formal submission that limited companies use to report profits or losses for Corporation Tax purposes and calculate any tax liability. Built around HMRC form CT600, the terms "corporate tax return" and "CT600" are often used interchangeably, though CT600 is the correct HMRC designation.

A complete Company Tax Return comprises three elements filed with HMRC as a single submission:

- CT600 form — declares taxable profits, reliefs, and the final tax calculation

- Statutory company accounts — includes the balance sheet, profit and loss account, and directors' report

- Tax computations file — shows how accounting profit was adjusted to arrive at taxable profit

Sole traders and partnerships report income through Self Assessment, not a Company Tax Return. This filing obligation applies specifically to incorporated limited companies subject to Corporation Tax.

Who Needs to File a UK Corporate Tax Return?

All active UK limited companies must file a Company Tax Return after every accounting period. This includes:

- Companies that made a loss

- Companies with no Corporation Tax to pay

- Companies that received a CT603 "Notice to Deliver" letter from HMRC

Dormant company exemptions: Dormant companies do not need to file — but only after formally notifying HMRC they have stopped trading and have no income. Once HMRC confirms dormancy in writing, the company must not resume trading without re-registering.

A company qualifies as dormant for Corporation Tax if it:

- Has stopped trading and has no other income

- Is a new limited company that hasn't started trading yet

- Is a flat management company

Non-resident companies: Non-UK incorporated companies with UK-source income or chargeable gains on UK property also have Corporation Tax obligations. These companies must register within three months of starting business activity in the UK.

What Information and Documents Do You Need Before Filing?

Core Credentials Required

Before starting your filing, gather these essential credentials:

| Credential | Purpose |

|---|---|

| Government Gateway user ID and password | Access to HMRC business tax account |

| Companies House authentication code | 6-digit alphanumeric code to authorise online filing |

| Company registration number | Your unique Companies House identifier |

| Unique Taxpayer Reference (UTR) | 10-digit number found on HMRC correspondence |

| Accounting period dates | Start and end dates set by HMRC (may differ from financial year in first year) |

Financial Documents and Format Requirements

Statutory accounts: You must prepare full statutory accounts including balance sheet, profit and loss account, and director's report. These must be formatted in iXBRL (Inline eXtensible Business Reporting Language); standard PDFs or spreadsheets are not accepted.

The iXBRL requirement has been mandatory since April 2011, applying to all UK limited companies regardless of size. Narrow exemptions exist only for unincorporated charities and certain non-resident companies whose accounts are prepared to unsupported accounting standards.

Tax computations: This document reconciles your accounting profit figure with the taxable profit figure used on the CT600. It documents allowable deductions, capital allowances, and reliefs applied to arrive at your final Corporation Tax liability.

Supplementary Pages

Beyond the core documents, your company's activities may require additional CT600 supplementary pages:

- CT600A — Loans to participators by close companies

- CT600C — Group and consortium relief

- CT600L — Research and Development tax relief claims

- CT600H — Cross-border royalties

Most small owner-managed companies only need the first few sections of the main CT600 form.

How to File a Corporate Tax Return in the UK

UK limited companies must file their Corporation Tax return online. Paper filing is only permitted where HMRC accepts a reasonable excuse, or for returns filed in Welsh.

Step 1: Register for Corporation Tax

New companies must register for Corporation Tax with HMRC within three months of starting to trade. Registration generates your company's Unique Taxpayer Reference (UTR), which is essential for all future filings.

Complete registration through HMRC's online portal by adding Corporation Tax services to your business tax account.

Step 2: Prepare Your Statutory Accounts

Finalise your annual accounts first — the profit or loss figures feed directly into the CT600. Accounts must meet Companies House minimum standards and be formatted in iXBRL for HMRC submission.

If your accounts were prepared in standard formats (basic spreadsheets or PDFs), they cannot be submitted directly. You'll need HMRC-compatible accounting software or professional accountant support to generate compliant iXBRL files.

Step 3: Calculate Taxable Profits and Corporation Tax

Your accounting profit requires adjustment before tax is applied. Allowable deductions, capital allowances, and reliefs all reduce your accounting profit down to the taxable figure. Document these adjustments in your tax computations file.

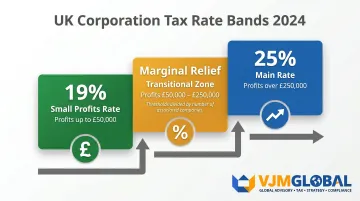

Current Corporation Tax rates (from 1 April 2023):

- 19% small profits rate — profits up to £50,000

- 25% main rate — profits over £250,000

- Marginal relief applies to profits between £50,000 and £250,000

These thresholds are divided by the number of associated companies plus one. Check current rates at the GOV.UK Corporation Tax rates page.

Step 4: Complete the CT600 Form

The CT600 requires the following key information:

- Company details (name, UTR, registration number, company type)

- Return period dates

- Income and profit figures

- Deductions and reliefs claimed

- Final Corporation Tax calculation

Many later sections of the 12-page form apply only to specific industries or grouped companies. Small businesses typically complete only the core sections.

Step 5: Submit Online via HMRC's Service

Critical change from 1 April 2026: HMRC's free joint filing service permanently closed on 31 March 2026. All CT600 returns must now be filed using HMRC-approved commercial software.

Through your chosen software, submit all three documents together:

- CT600 return form

- iXBRL-formatted statutory accounts

- Tax computations file

The integrated HMRC/Companies House filing service no longer exists. Depending on your software, you may need to file separately with each organisation.

Key Deadlines, Corporation Tax Payments, and Penalties

Two Critical Deadlines

| Deadline | Timing | Note |

|---|---|---|

| CT600 filing deadline | 12 months after accounting period end | Return submission |

| Corporation Tax payment deadline | 9 months and 1 day after accounting period end | Payment comes first |

The payment deadline always falls before the filing deadline. You must calculate and pay your Corporation Tax liability before the CT600 is formally due.

First-Year Complications

Because Companies House assigns accounting reference dates to new companies, the first set of accounts often covers more than 12 months. Since a Corporation Tax accounting period cannot exceed 12 months, new companies may need to submit two separate CT600 returns in their first year.

Quarterly Instalment Payments (QIPs)

Large companies with annual profits between £1.5 million and £20 million must pay Corporation Tax in quarterly instalments rather than a single payment. Very large companies with profits over £20 million face even earlier payment schedules.

HMRC divides these thresholds by the number of associated companies plus one. Companies approaching these thresholds should forecast profits carefully to avoid unexpected instalment obligations.

Penalty Structure for Late Filing (from 1 April 2026)

Missing deadlines carries real cost. Late filing penalties doubled from 1 April 2026 — the first increase in nearly 30 years:

- 1 day late: £200 penalty

- 3 months late: Another £200

- 6 months late: 10% of HMRC's estimated tax bill

- 12 months late: Another 10% of unpaid tax

- 3 consecutive late filings: The initial £200 penalty escalates to £1,000 per filing

Late payment interest: HMRC charges 7.75% annual interest on overdue Corporation Tax (rate from 9 January 2026). This is calculated as Bank of England base rate plus 4%.

HMRC Enquiry Window

HMRC can open a formal enquiry into your return within 12 months of the filing date. Retain all supporting documents for at least 12 months after filing — solid records are your first line of defence if HMRC identifies errors and initiates an investigation or requests an amended return.

Common Mistakes and Misconceptions When Filing

Three mistakes trip up even experienced filers — and all three are avoidable with the right preparation:

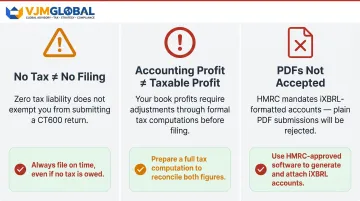

- Assuming no filing is needed when no tax is owed. Filing is still required even with a loss or zero Corporation Tax liability. HMRC explicitly states you must submit a return regardless — skipping it is one of the most common reasons for penalties.

- Copying accounting profit directly onto the CT600. Accounting profit and taxable profit are not the same. Capital allowances, disallowable expenses, and other adjustments must be applied first. The tax computations file exists precisely to document those differences.

- Underestimating iXBRL formatting requirements. Accounts prepared in basic spreadsheets or PDFs cannot be submitted to HMRC directly. You'll need HMRC-compatible accounting software or a professional accountant to handle the conversion.

Each of these mistakes is more common among international businesses filing in the UK for the first time. VJM Global works with foreign-owned UK companies to handle Corporation Tax preparation — from adjusting accounts for taxable profit to ensuring iXBRL-compliant submission. Having served 250+ UK businesses with a 95% client retention rate, the team helps international companies stay compliant without diverting focus from day-to-day operations.

Frequently Asked Questions

When to file a corporate tax return in the UK?

The deadline is 12 months after the end of the accounting period the return covers. This is separate from the Corporation Tax payment deadline of 9 months and 1 day after the same period ends.

How to file a UK Corporation Tax return?

Filing must be done online using HMRC-approved commercial software (as of 1 April 2026). Submit the CT600 form alongside iXBRL-formatted accounts and a tax computations file through HMRC's online service.

What is a company tax return in the UK?

It is the annual submission centred on HMRC form CT600 that UK limited companies use to report their profits or losses for Corporation Tax purposes and calculate their tax liability.

What happens if you file your company tax return late?

Late filing triggers escalating penalties:

- Day 1: £200 immediate penalty

- 3 months: Additional £200

- 6 and 12 months: 10% of estimated unpaid tax each

- Ongoing: Interest on any unpaid tax

Do I need to file a company tax return if my company made a loss?

Yes. All active UK limited companies must file a return regardless of whether they made a profit or loss, or have no tax to pay.

What is the difference between Corporation Tax and a company tax return?

Corporation Tax is the actual tax liability owed on taxable profits. The company tax return (CT600) is the document submitted to HMRC to calculate and report that liability.