Introduction

April 2023 changed the rules for every UK company. HMRC replaced the flat 19% Corporation Tax rate with a tiered structure — and many businesses are still miscalculating which rate applies to them, whether that's the 19% Small Profits Rate, the 25% Main Rate, or the Marginal Relief band in between.

The stakes are real. Late filing penalties start at £200 from day one, and errors in self-assessment can trigger retrospective enquiries reaching back up to 20 years in cases of negligence.

This guide breaks down the principles that keep UK companies compliant — and out of HMRC's crosshairs.

What Is UK Corporate Tax Compliance?

UK corporate tax compliance is the process by which companies meet their legal obligations to register with HMRC, calculate taxable profits accurately, file Corporation Tax returns (CT600), and pay the correct amount of tax on time. This encompasses the entire cycle from notifying HMRC of a new accounting period through to maintaining records for at least six years after the relevant period.

Who Must Pay UK Corporation Tax?

UK-resident companies are taxed on their worldwide profits, regardless of where those profits arise. Non-resident companies with a UK permanent establishment or UK property business are also within scope and must register and file returns for their UK-source income.

A company is UK-resident if either of the following applies:

- Incorporated in the UK under UK company law

- Central management and control is exercised in the UK (regardless of where incorporated)

Non-resident entities must separately assess whether their UK activities constitute a permanent establishment — broadly, a fixed place of business or a dependent agent arrangement that creates a taxable presence in the UK.

Tax Avoidance vs. Legitimate Tax Planning

Understanding where legitimate tax planning ends and abusive avoidance begins is essential for any compliant business. HMRC draws a clear line: legitimate tax planning uses reliefs and allowances as Parliament intended, while abusive tax avoidance involves artificial arrangements designed to exploit loopholes. The General Anti-Abuse Rule (GAAR), introduced in Finance Act 2013, empowers HMRC to counteract tax advantages arising from abusive arrangements.

The GAAR applies when arrangements are "not a reasonable course of action," considering established practice, relevant tax provisions, and whether the arrangement achieves a tax result contrary to the purpose of the legislation.

That's why genuine compliance and transparent record-keeping matter. HMRC has broad powers to challenge arrangements it deems abusive, and penalties plus interest can add significantly to the original liability.

Current UK Corporation Tax Rates: The Tiered Structure

The UK shifted from a single flat 19% rate (in place from 2017 to March 2023) to a two-tier system effective 1 April 2023. Both rates remain unchanged for financial years 2025–26 and 2026–27:

- 19% Small Profits Rate for companies with profits up to £50,000

- 25% Main Rate for companies with profits over £250,000

This structure increases tax revenue from larger companies while shielding smaller businesses — but companies with profits between the two thresholds sit in a tapered band with its own calculation rules.

Marginal Relief for Profits Between £50,000 and £250,000

Companies with augmented profits (taxable profits plus exempt distributions) between £50,000 and £250,000 pay tax at the 25% main rate, reduced by Marginal Relief. This creates a gradual taper between the two rates, avoiding a sudden jump in effective tax.

How Marginal Relief works:

Marginal Relief is calculated using the standard fraction 3/200 applied to the difference between the upper threshold (£250,000) and the company's augmented profits. HMRC provides a Marginal Relief calculator to simplify this computation.

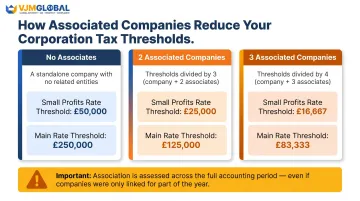

Watch out for associated companies: The £50,000 and £250,000 thresholds are divided by the total number of associated companies plus one (the company itself).

- Two associated companies each face thresholds of £25,000 and £125,000

- Three associated companies reduce those thresholds further to £16,667 and £83,333

- Overlooking associated companies is one of the most common causes of underpayment and HMRC enquiries

Special Corporation Tax Regimes

Certain sectors operate under distinct rules:

Oil and gas ring-fence companies pay a 30% ring-fence Corporation Tax rate plus a 10% supplementary charge (effective from 1 January 2016). An additional 35% Energy Profits Levy on extraordinary profits pushes the combined rate up to 75%.

Real Estate Investment Trusts (REITs) are exempt from Corporation Tax on qualifying property rental income and capital gains, provided they meet distribution and asset requirements.

Banking surcharge: Banks pay an additional 3% surcharge on profits exceeding £100 million, effective 1 April 2023.

Tonnage Tax: Shipping companies can elect into a tonnage-based regime that taxes deemed profits based on fleet tonnage rather than actual accounting profits.

Pillar Two: Multinational Top-Up Tax

The UK implemented OECD Pillar Two rules effective from accounting periods beginning on or after 31 December 2023. Large multinational groups with consolidated revenue of €750 million or more must ensure a minimum 15% effective tax rate in each jurisdiction.

Key obligations:

- Register with HMRC's online portal within six months of the end of the first in-scope accounting period

- Submit a Global Anti-Base Erosion (GIR) Information Return within 18 months for the first period, then 15 months for subsequent periods

- Maintain detailed records to support effective tax rate calculations and top-up tax computations

Groups entering Pillar Two scope for the first time should map their jurisdictional effective tax rates before the first reporting deadline — errors in the GIR can trigger top-up tax charges that are difficult to unwind after the fact.

Corporation Tax Filing and Registration Requirements

Notification and the CT603 Notice

Companies must notify HMRC when they become liable to Corporation Tax—typically when they start trading, receive income, or make a taxable capital gain. HMRC issues a CT603 notice to file, which triggers the formal obligation to submit a Corporation Tax return (CT600).

Filing Deadline: 12 Months After Period End

The CT600 return must be filed within 12 months of the end of the period of account. For a company with a 31 March 2025 year-end, the CT600 is due by 31 March 2026.

Accounting Periods vs. Financial Years

An accounting period is normally the 12-month period for which a company prepares its statutory accounts. A financial year runs from 1 April to 31 March and determines which Corporation Tax rates apply.

When an accounting period straddles two financial years with different rates, profits must be apportioned on a time basis and taxed at the applicable rate for each portion.

Example: A company with a 31 December 2023 year-end has three months (1 January to 31 March 2023) taxed under the old flat 19% rate and nine months (1 April to 31 December 2023) under the new tiered structure.

What Must Be Included in the CT600?

The CT600 return requires:

- Statutory company accounts

- A detailed tax computation adjusting accounting profit to taxable profit

- Supplementary pages for specific reliefs, claims, or regimes (R&D, group relief, Pillar Two, etc.)

The company is legally responsible for the accuracy of its return. Negligent or deliberate errors carry penalties ranging from 15% to 100% of the tax underpaid, plus interest.

HMRC Enquiry Powers

HMRC has 12 months from the filing date (or normal filing deadline, if later) to open an enquiry into a return. In cases of deliberate understatement or fraud, HMRC can reopen cases up to 20 years after the end of the accounting period.

Contemporaneous documentation—retained and organised at the time decisions are made—is your primary defence if HMRC opens an enquiry years after filing.

Allowable Deductions, Reliefs, and Incentives

Taxable profit starts with accounting profit before tax, then adjusts for tax-specific rules. Most direct business expenses—staff costs, rent, utilities, professional fees—are deductible. However, business entertainment costs are explicitly disallowed.

This section covers three key relief categories:

- Capital allowances — deductions for qualifying capital assets

- R&D relief — enhanced credits for innovation expenditure

- Loss relief and group relief — offsetting losses across periods and group structures

Capital Allowances

Capital allowances are the tax equivalent of depreciation, allowing businesses to deduct the cost of qualifying capital assets (plant, machinery, IT equipment, vehicles) against taxable profits.

Annual Investment Allowance (AIA): Permanently set at £1 million per year since 1 January 2019, the AIA allows 100% first-year relief on qualifying expenditure up to the limit.

Full Expensing: Introduced in April 2023 and made permanent by the Autumn Finance Bill 2023, full expensing provides:

- 100% first-year allowance on qualifying new main rate plant and machinery

- 50% first-year allowance on special rate assets (e.g., integral features, long-life assets)

Full expensing is available only to companies (not unincorporated businesses) and significantly enhances cash flow by accelerating tax relief.

Research and Development (R&D) Relief

Qualifying companies can claim enhanced deductions or tax credits on eligible R&D expenditure. From 1 April 2024, the previous SME and RDEC schemes merged into a single scheme offering:

- A 20% Research and Development Expenditure Credit (RDEC) above the line

- A notional tax rate of 19% for loss-making companies claiming payable credits

HMRC scrutinises R&D claims closely. Keep detailed records — captured at the time — that document the scientific or technological uncertainty, the advance being sought, and how each item of expenditure meets HMRC's qualifying criteria.

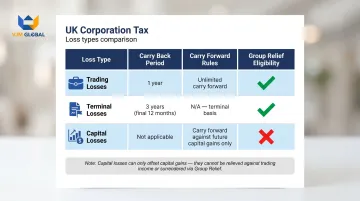

Loss Relief and Group Relief

The table below summarises how different loss types can be used:

| Loss Type | Carry Back | Carry Forward | Group Relief |

|---|---|---|---|

| Trading losses | 1 year (total profits) | Indefinitely (same trade) | Yes — within 75% group |

| Terminal losses | 3 years (total profits) | N/A | No |

| Capital losses | Not applicable | Indefinitely (capital gains only) | No |

Terminal losses apply to the final 12 months of trade and provide meaningful cash flow relief for businesses that are winding down. Capital losses can only offset capital gains — they cannot reduce trading income.

Corporation Tax Payment Deadlines and Penalties

Standard Payment Deadline

Most companies must pay Corporation Tax nine months and one day after the end of their accounting period. For a 31 March 2025 year-end, payment is due by 1 January 2026—before the CT600 return filing deadline.

Quarterly Instalment Payments for Large Companies

Once profits exceed £1.5 million (adjusted for associated companies and short periods), HMRC requires quarterly instalment payments rather than a single year-end payment. The instalment schedule differs by company size:

| Company Type | Profit Threshold | Instalment Months |

|---|---|---|

| Large | Over £1.5 million | Months 7, 10, 13, 16 |

| Very Large | Over £20 million | Months 3, 6, 9, 12 (accelerated) |

Interest on underpaid instalments runs at 6.25% from January 2026. That interest accrues from the instalment due date — not the year-end — so underestimating profits mid-year carries an immediate cost.

Late Filing Penalties

HMRC imposes automatic penalties for late CT600 returns:

- Immediately (day 1): £200 fixed penalty

- 3 months late: Additional £200 penalty

- 6 months late: 10% of unpaid tax (or £500, whichever is greater)

- 12 months late: Further 10% of unpaid tax (or £500, whichever is greater)

Repeated failures (three consecutive late returns) attract penalties of £1,000 per occurrence instead of £200.

Late Payment Interest

Late filing penalties and late payment interest often arrive together — and the payment clock runs independently of any filing extension. HMRC charges interest on late-paid Corporation Tax at 7.75% (from 9 January 2026), accruing daily from the due date. On a £100,000 liability, that amounts to roughly £7,750 in interest per year — a meaningful cost on top of any filing penalties already incurred.

Common Compliance Mistakes UK Businesses Make

Misclassifying Capital and Revenue Expenditure

Confusing capital expenditure (qualifying for capital allowances over time) with revenue expenditure (immediately deductible) leads to incorrect tax computations. Missing the opportunity to claim capital allowances or incorrectly deducting capital items as expenses triggers adjustments and potential penalties.

Failing to Account for Associated Companies

The most frequent error when applying the tiered rate structure is ignoring associated companies. Thresholds (£50,000 and £250,000) are divided by the number of associated companies plus one. A company with two associated companies has thresholds of £16,667 and £83,333—substantially lower than the headline figures.

HMRC defines associated companies broadly: companies under common control (direct or indirect 51%+ ownership) at any point during the accounting period count, even if held for just one day.

Missing Deadlines for Relief Claims and Elections

Many reliefs and elections must be claimed within two years after the end of the accounting period. Missing this window means forfeiting valuable relief permanently. Common time-limited claims include:

- R&D relief claims

- Loss relief elections

- Group relief surrenders (claimed by the first anniversary of the filing date)

- Capital allowance elections

Inadequate Record-Keeping

HMRC requires companies to retain records for at least six years after the end of the accounting period. For Pillar Two, longer retention applies. Poor documentation is the leading cause of failed enquiries, denied claims, and penalties.

Essential records include:

- Invoices, receipts, and contracts supporting all expenditure

- Payroll records and employment documentation

- Bank statements and financial records

- Board minutes evidencing key decisions

- Technical documentation for R&D claims

- Transfer pricing documentation

Cross-Border Complexity

Record-keeping obligations extend further when a UK business has foreign subsidiaries, cross-border transactions, or international group structures. Each layer adds distinct compliance requirements:

- Transfer pricing: Intra-group transactions must be priced at arm's length, with documentation to prove it

- CFC rules: Undistributed profits of foreign subsidiaries may be attributed to the UK parent company

- Diverted Profits Tax: A 25% charge applies to profits artificially diverted from the UK, effective from 1 April 2015

- Pillar Two compliance: Large multinationals face registration requirements, GIR filings, and top-up tax calculations

For businesses managing cross-border structures, specialist support reduces the risk of missed filings or mispriced transactions. VJM Global has worked with 250+ UK businesses on international tax compliance, transfer pricing, and cross-border accounting obligations.

Frequently Asked Questions

What is the corporate tax rate in the UK 2019?

The UK Corporation Tax rate in 2019 was a flat 19% for all non-ring fence company profits. No tiered structure applied — every qualifying company paid the same rate.

What was the UK corporate tax rate in 2020?

The Corporation Tax rate remained at 19% for financial year 2020 (from 1 April 2020). A planned reduction to 17% was cancelled under Finance Act 2020, leaving the rate unchanged.

When did UK corporation tax rise to 25%?

The 25% main rate took effect from 1 April 2023, applying to companies with profits over £250,000. A 19% small profits rate was simultaneously introduced for companies with profits under £50,000.

What is UK tax compliance?

UK tax compliance is a company's legal obligation to register for relevant taxes, accurately calculate taxable profits, and file returns with HMRC on time. It also means paying the correct amount of tax by each statutory deadline.

What is Marginal Relief and who qualifies for it?

Marginal Relief applies when a company's total profits (including dividends from non-group companies) fall between £50,000 and £250,000, tapering the effective rate between 19% and 25%. Both thresholds are divided by the number of associated companies plus one, so having associates reduces the band available to each company.

What are the penalties for filing a Corporation Tax return late in the UK?

Late CT600 filings trigger an automatic £200 penalty from day one, rising to a further £200 after three months. At six and twelve months, tax-geared penalties of 10% of unpaid tax apply — and HMRC charges 7.75% interest on any overdue Corporation Tax.