Introduction

UK corporation tax time limits operate as a two-way street: HMRC faces defined windows to pursue underpaid tax, whilst companies must navigate strict deadlines to claim relief, amend returns, and recover overpayments. Missing either side carries real financial consequences—whether it's an unexpected assessment reaching back six years or forfeiting a legitimate £50,000 overpayment claim that expired just weeks ago.

The rules form a tiered system that shifts depending on your company's conduct and the type of issue involved. Key thresholds to know:

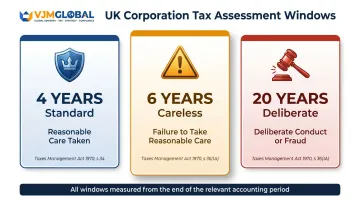

- 4 years — standard HMRC assessment window where reasonable care was taken

- 6 years — applies where HMRC identifies careless behaviour

- 20 years — triggered by deliberate conduct or fraud

- 4 years — the typical window for companies to make most corporation tax claims

- 12 months — the deadline to amend a filed return after the filing date

Understanding both sides of this framework matters: the same rules that protect companies from stale HMRC assessments can also cut off legitimate claims if deadlines are missed.

Key Takeaways

- HMRC has up to four years to assess a tax loss where reasonable care was taken, six years for careless behaviour, and 20 years for deliberate conduct

- Companies have four years from the accounting period end to make most corporation tax claims and overpayment relief claims

- A company can amend its own return within 12 months of the filing deadline—after that, only HMRC can make changes

- Discovery assessments let HMRC reassess outside normal enquiry windows, though taxpayers can challenge both validity and behaviour classification

- Knowing which time limit applies and keeping clear records is essential for defending against HMRC and protecting unclaimed relief

How UK Corporate Tax Time Limits Work: The Three-Tier Assessment Framework

Corporation tax assessment time limits are established under Paragraph 46 of Schedule 18, Finance Act 1998, not the Taxes Management Act 1970 which governs income tax and capital gains tax. These provisions were significantly amended by the Finance Act 2008 to create the current three-tier structure.

All time limits run from the end of the accounting period, not from the filing date. For example, a company with an accounting period ending 31 March 2022 faces a four-year standard window closing on 31 March 2026.

The Three Assessment Windows

| Time Limit | Trigger | Statutory Provision | Measured From |

|---|---|---|---|

| 4 years | Standard / reasonable care taken | Para 46(1) Sch 18 FA 1998 | End of accounting period |

| 6 years | Careless behaviour by company or related person | Para 46(2) Sch 18 FA 1998 | End of accounting period |

| 20 years | Deliberate behaviour, failure to notify chargeability, or DOTAS failures | Para 46(2A) Sch 18 FA 1998 | End of accounting period |

These time limits apply specifically to assessments for underpaid or lost tax — they are separate from HMRC's routine enquiry powers, which operate under a different statutory framework.

Under Paragraph 24 of Schedule 18, HMRC has 12 months from the date the return was delivered to open a formal enquiry, provided the return was filed on or before the filing deadline. Once that enquiry window closes, HMRC can only act through a discovery assessment — and only if certain statutory conditions are met.

Understanding What Drives Each Time Limit: Behaviour and Intent

The applicable time limit depends critically on how HMRC categorises the taxpayer's behaviour. This classification is not always clear-cut, and companies have the right to challenge HMRC's determination—potentially reducing the window and protecting earlier years from reassessment.

| Behaviour | Time Limit | HMRC Standard |

|---|---|---|

| Reasonable care taken | 4 years | Default position |

| Careless (failure to take reasonable care) | 6 years | Balance of probabilities |

| Deliberate or concealed | 20 years | Higher quality of evidence required |

The 4-Year Standard Limit

This applies where the taxpayer or their agent took reasonable care but an error or omission still occurred. It's the default position for most companies with professionally prepared returns. HMRC must prove on the balance of probabilities that a higher standard applies if they wish to extend the window.

The 6-Year Careless Limit

Careless behaviour means a failure to take reasonable care. HMRC's Compliance Handbook (CH53400) defines this as the omission to do something which a reasonable person would do, or doing something which a prudent person would not do—effectively the common law concept of negligence.

Importantly, HMRC acknowledges "people do make mistakes. We do not expect perfection." Repeated inaccuracies may suggest systemic failure, but repetition alone doesn't automatically indicate carelessness.

Example: An agent miscodes a significant expense category and the company lacks adequate review processes — understated profits result. If HMRC can show those review procedures were insufficient, the six-year window applies.

Where carelessness shades into knowing intent, the stakes rise considerably.

The 20-Year Deliberate Limit

This applies where the company—or a person acting on its behalf—deliberately submitted incorrect information or concealed a liability. The key test is whether someone knowingly gave HMRC an inaccurate document — intent to mislead, not merely intent to cause a tax loss.

HMRC distinguishes between two levels:

- Deliberate but not concealed: the person knows the document contains an inaccuracy but hasn't taken active steps to hide it

- Deliberate and concealed: active steps were taken to hide the inaccuracy before or after submission — the most serious level of evasion

The burden of proof rests with HMRC. CH54300 confirms "the onus of proof of careless or deliberate behaviour is on HMRC" on the balance of probabilities, with "the quality of evidence higher for the more serious behaviour."

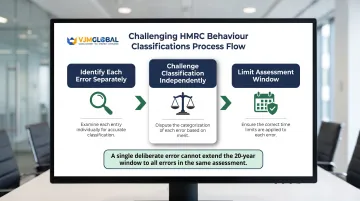

Challenging Behaviour Classification

Case law confirms HMRC must apply behaviour-based time limits to each individual error separately — a single deliberate error cannot be used to extend the 20-year window across all errors in the same assessment. Where an assessment covers multiple errors, challenge each classification independently. Done effectively, this can shield earlier years from reassessment and materially reduce exposure.

Time Limits for Companies Making Tax Claims and Amendments

The time limit framework isn't just about HMRC's powers—companies face statutory deadlines to exercise their own rights, and missing these forfeits relief permanently.

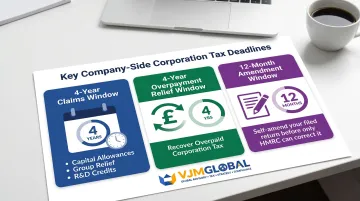

The General 4-Year Claims Rule

Most corporation tax claims must be made within four years of the end of the accounting period under Paragraph 55, Schedule 18, Finance Act 1998 (as amended by Finance Act 2008). This includes:

- Capital allowances elections

- Group relief claims

- R&D tax credit claims

- Most other corporation tax reliefs

This deadline was extended from two years to four years effective 1 April 2010, though certain reliefs retain shorter deadlines — always verify the rules for the specific relief being claimed.

Overpayment Relief Claims

Companies can reclaim overpaid corporation tax within four years of the end of the accounting period under Paragraph 51B, Schedule 18, Finance Act 1998. This matches HMRC's standard assessment window: where reasonable care was taken, both the company and HMRC have four years to correct errors.

Trading Loss Carry-Back Claims

The standard rule under s37 Corporation Tax Act 2010 allows 1-year carry-back of trading losses. A company incurring a trading loss may claim to set it against profits of the preceding 12 months.

The temporary 3-year extended carry-back (Finance Act 2021) has now closed. Key parameters for reference:

- Applied to trading losses in accounting periods ending between 1 April 2020 and 31 March 2022

- Extended carry-back (years 2 and 3) was capped at £2,000,000 per period

- Final claim deadline: 31 March 2024

12-Month Amendment Window

Companies can amend a submitted corporation tax return within 12 months of the filing deadline (not the submission date) under Paragraph 15, Schedule 18. Once this window closes, only HMRC can make corrections through a formal assessment. Any errors discovered after the 12-month mark cannot be self-corrected — they require HMRC to open an enquiry or issue a discovery assessment.

Discovery Assessments: When HMRC Can Reassess Outside Normal Windows

Even after the standard enquiry window has closed, HMRC can raise a further assessment if an officer "discovers" that insufficient tax has been charged. However, this power is constrained by important taxpayer protections.

The Legal Framework: Paragraph 41, Schedule 18

Corporation tax discovery assessments are governed by Paragraphs 41-45, Schedule 18, Finance Act 1998—not s29 TMA 1970, which applies only to income tax and capital gains tax.

An officer may make a discovery assessment if they discover that:

- An amount which ought to have been assessed has not been assessed

- An assessment has become insufficient

- Relief given has become excessive

Two Gateway Conditions

Where a return has been delivered, HMRC can only make a discovery assessment if one of two conditions is met:

Condition 1 - Conduct (Para 43): The situation was brought about carelessly or deliberately by the company, a person acting on its behalf, or a partner.

Condition 2 - Officer Awareness (Para 44): At the time the enquiry window closed or HMRC completed its enquiry, the officer "could not have been reasonably expected, on the basis of the information made available to him before that time, to be aware of the situation."

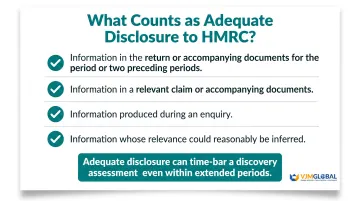

The Taxpayer Protection: Adequate Disclosure

Information is deemed "made available" to HMRC if it is:

- Contained in the return or accompanying documents for the relevant period or the two immediately preceding periods

- Contained in a relevant claim or accompanying documents

- Produced during an enquiry

- Information whose existence and relevance "could reasonably be expected to be inferred" from the above

Adequate disclosure in the original return can time-bar a discovery assessment even within the extended periods. Clearly documenting the basis for material tax positions, reliefs claimed, and any uncertain treatments is one of the most reliable ways to limit HMRC's discovery powers.

Discovery Assessments Remain Subject to Para 46 Time Limits

Even where HMRC clears the gateway conditions above, its power to reassess is not open-ended. Discovery assessments remain subject to the behaviour-based time limits: four years (reasonable care), six years (careless), or 20 years (deliberate) from the end of the accounting period.

Upon receiving a discovery assessment, companies should:

- Check whether the gateway conditions for discovery were genuinely met — both careless/deliberate conduct and officer awareness need scrutiny

- Verify whether adequate information was previously disclosed in the return or accompanying documents, which may time-bar the assessment entirely

- Challenge HMRC's behaviour classification in writing if an extended six- or 20-year window is applied without clear justification

Practical Steps UK Businesses Should Take to Protect Themselves

Maintain Complete Tax Records for the Appropriate Duration

Paragraph 21, Schedule 18 requires companies to keep records for six years from the end of the accounting period—matching HMRC's careless behaviour assessment window exactly.

Companies should retain records longer if they:

- Have offshore connections or complex structures

- Face potential deliberate behaviour allegations

- Show transactions covering multiple accounting periods

- Have bought assets expected to last more than six years

Ensure Adequate Disclosure in Every Return

Clearly document the basis for material tax positions, reliefs claimed, and any uncertain treatments. Where a transaction is complex or the tax treatment uncertain, include:

- The commercial rationale

- The relevant tax provisions relied upon

- The reasoning for your approach

- Any alternative treatments considered

This documentation limits HMRC's ability to raise a discovery assessment after the standard enquiry window closes, even where the ultimate tax treatment is later found incorrect.

Diarise and Track Company-Side Claims Deadlines

Management focus naturally gravitates towards HMRC compliance rather than proactive claim recovery, making these deadlines easy to overlook:

- Four-year claim window for most reliefs (capital allowances, group relief, R&D credits)

- Four-year overpayment relief window

- 12-month amendment window from the filing deadline

Cross-border operations add another layer of complexity here. UK subsidiaries of foreign parents often miss these windows simply because no one in the group has ownership of them. VJM Global works with international groups that include UK entities, helping identify unclaimed relief and keeping compliance deadlines from falling through the cracks of a multi-jurisdiction structure.

Frequently Asked Questions

Is there a statute of limitations in the UK for tax?

Yes. HMRC must raise corporation tax assessments within defined time limits: four years (reasonable care), six years (careless behaviour), or 20 years (deliberate conduct), all measured from the end of the accounting period. Once expired, the tax debt cannot generally be recovered.

How far back can HMRC go for corporation tax?

The standard window is four years where reasonable care was taken. This extends to six years for careless behaviour and 20 years for deliberate conduct. All periods are measured from the end of the relevant accounting period, not the filing date.

What is the 5 year rule for tax in the UK?

There is no "5-year rule" in UK corporation tax law. The term sometimes appears in personal tax discussions, where self-assessment records must be kept for five years after the filing deadline. For corporation tax, the standard assessment limit is four years.

What is the time limit for a company to amend a corporation tax return?

A company can amend its own corporation tax return within 12 months of the statutory filing deadline (not the submission date). After this period, only HMRC can make amendments through a formal assessment.

What happens if HMRC misses the assessment time limit for corporation tax?

Once the applicable time limit expires, HMRC is time-barred from raising an assessment and the company gains finality on that period. HMRC can still challenge this outcome by arguing a longer window applies due to careless or deliberate behaviour.

Can HMRC extend the time limit for a corporation tax enquiry?

HMRC cannot unilaterally extend a time limit. The applicable window is longer where careless or deliberate behaviour is established, or where a valid discovery assessment is raised — and companies can challenge both grounds.