This guide is designed for UK limited companies, SMEs, and small business owners who want a structured, step-by-step approach to closing their books accurately and avoiding costly mistakes. You'll learn what year-end accounts are, the key UK deadlines you must meet, a practical checklist of essential tasks, proven tax-saving strategies you can implement before the books close, and the most common pitfalls that trigger HMRC penalties.

Key Takeaways

- UK limited companies must file year-end accounts with Companies House within 9 months and HMRC within 12 months of their financial year-end

- The process includes reconciling accounts, reviewing payroll and VAT, preparing statutory financial statements, and calculating corporation tax

- Year-end presents a strategic opportunity to reduce tax bills through capital allowances, R&D credits, and pension contributions made before the period closes

- Missed deadlines, unrecorded accruals, and overlooked deductions trigger automatic penalties starting at £150 and escalating quickly

- VJM Global, with 250+ UK businesses served, regularly identifies tax-saving opportunities that DIY approaches miss

What Are Year-End Accounts and Why Do They Matter?

Year-end accounts — also called statutory accounts or annual accounts — are a formal summary of your company's financial performance over the past 12 months. Under the Companies Act 2006 Part 15, every UK limited company must prepare these, whether private or public, trading or dormant.

What Statutory Accounts Include

UK year-end accounts typically comprise:

- Profit and Loss Statement (or Income and Expenditure Account for non-profits)

- Balance Sheet signed by a director with printed name

- Notes to the Accounts explaining accounting policies and material items

- Directors' Report (unless the company qualifies as small)

- Strategic Report (required for medium and large companies)

- Auditors' Report (unless the company is audit-exempt)

Small companies benefit from reduced disclosure requirements. From 6 April 2025, the small company thresholds increased significantly:

| Criterion | Previous Threshold | New Threshold (April 2025) |

|---|---|---|

| Turnover | £10.2M | £15M |

| Balance sheet total | £5.1M | £7.5M |

| Employees | 50 | 50 (unchanged) |

Meet at least two of three criteria and you qualify as small — meaning you can file an abridged balance sheet without a profit and loss account at Companies House.

Why These Accounts Go Beyond Compliance

Statutory accounts serve multiple purposes beyond satisfying legal requirements:

- Spot profitability trends and pinpoint where costs can be reduced

- Plan budgets grounded in actual historical performance

- Give investors the audited figures they need before committing capital

- Avoid late-filing penalties — fines start at £150 and escalate to criminal prosecution of directors or company strike-off

- Support credit applications, since lenders routinely require accounts to assess financial health

Key UK Deadlines and Filing Requirements

Primary Filing Deadlines

| Action | Deadline |

|---|---|

| File first accounts with Companies House | 21 months after incorporation date |

| File annual accounts with Companies House | 9 months after financial year-end |

| File Corporation Tax Return (CT600) with HMRC | 12 months after accounting period end |

| Pay Corporation Tax | 9 months and 1 day after accounting period end |

Example: If your financial year ends 31 March 2026, your accounts are due at Companies House by 31 December 2026, and your CT600 is due at HMRC by 31 March 2027. Corporation tax payment is due 1 April 2026.

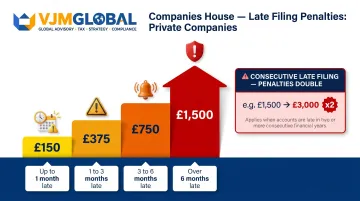

Companies House Late Filing Penalties (Private Companies)

| Delay Period | Penalty |

|---|---|

| Up to 1 month | £150 |

| 1-3 months | £375 |

| 3-6 months | £750 |

| Over 6 months | £1,500 |

Penalties automatically double if you file late in two consecutive financial years. A company filing six months late for the second year in a row faces a £3,000 penalty instead of £1,500.

HMRC Company Tax Return Penalties

HMRC penalties operate separately:

- 1 day late: £200 penalty

- 3 months late: additional £200 penalty

- 6 months late: HMRC estimates your tax bill and adds 10% of unpaid tax

- 12 months late: another 10% of unpaid tax

File late three times in a row and the £200 penalties rise to £1,000 each.

Making Tax Digital (MTD) for VAT

Since April 2022, all VAT-registered businesses must:

- Keep digital VAT business records using MTD-compatible software

- Submit VAT returns via API connection to HMRC (no manual submissions)

- Maintain digital links between software programmes — manual copy-paste breaks the digital chain

- Use bridging software if working with spreadsheets

- Apply to HMRC for an exemption if digital exclusion applies (age, disability, remote location, or religious beliefs) — these cases are rare and assessed individually

The Year-End Accounting Checklist for UK Businesses

This sequential checklist ensures accuracy, compliance, and tax efficiency before you file. Each task builds on the previous one — skipping steps creates errors that cascade through your accounts.

Gather and Organise Financial Records

Collect every financial document for the full financial year:

- Bank statements for all business accounts and credit cards

- Sales invoices (issued and received)

- Expense receipts and supplier bills

- Payroll records including P60s and benefits-in-kind

- Loan agreements and financing documentation

- Fixed asset purchase receipts and disposal records

- VAT returns filed throughout the year

Why it matters: Disorganised records are the primary cause of year-end delays. Missing bank statements or lost receipts force you to reconstruct transactions, wasting days when deadlines are tight.

Reconcile Bank Accounts and Ledgers

Compare your bookkeeping records against bank statements for every business account:

- Match each transaction in your accounting software to the corresponding bank entry

- Identify and correct discrepancies — common culprits include duplicate entries, unrecorded bank fees, and transactions coded to wrong accounts

- Clear outstanding reconciling items from prior periods

- Ensure your trial balance reflects accurate balances before proceeding

Red flag: If reconciliation reveals unexplained differences exceeding 2% of monthly turnover, investigate thoroughly before moving forward.

Review Accounts Receivable and Payable

Accounts Receivable:

- List all outstanding sales invoices at year-end

- Chase overdue payments promptly — unresolved invoices at year-end directly delay your closing process and distort final profit figures

- Write off confirmed bad debts to reflect accurate profit — uncollectable debts left on the books inflate taxable income and increase your tax bill unnecessarily

Accounts Payable:

- Confirm all supplier bills are settled or correctly recorded as liabilities

- Verify amounts match supplier statements

- Identify any disputed invoices requiring resolution

Verify Payroll, PAYE, and Pension Records

Before closing payroll for the year:

- Confirm all employee wages, director salaries, bonuses, and benefits-in-kind are recorded

- Verify PAYE and National Insurance submissions to HMRC match your payroll figures

- Confirm pension contributions were made and correctly recorded

- Submit your final Full Payment Submission (FPS) to HMRC on or before the last payday of the tax year (by 5 April)

- Issue P60s to all employees on the payroll by 31 May

Common mistake: Directors often forget to record their own salaries or benefits-in-kind, creating discrepancies between Companies House accounts and personal tax returns.

Review Fixed Assets, Depreciation, and Stock

Fixed Assets:

- Update your fixed asset register to include new purchases and disposals during the year

- Apply depreciation according to your accounting policy (straight-line or reducing balance)

- Remove fully depreciated assets no longer in use

Inventory (if applicable):

- Conduct a physical year-end stocktake

- Value inventory at the lower of cost and net realisable value under FRS 102 Section 13

- Write off unsellable or obsolete items — overstating stock inflates profits and increases your tax bill

Note: LIFO (last-in-first-out) is prohibited under UK GAAP. Use FIFO (first-in-first-out) or weighted average cost.

Prepare Financial Statements and Account for Accruals

Draft your Profit and Loss Account and Balance Sheet, then make critical adjusting entries:

- Accruals: Record expenses incurred but not yet paid (utilities used in March but billed in April)

- Prepayments: Record costs paid in advance for the next period (annual insurance paid in February covering 12 months)

- Deferred income: Record customer payments received for goods or services to be delivered next year

Once these entries are in place, your statements will accurately reflect the year's true financial position — and you'll be ready to move into tax calculations with reliable numbers.

Year-End Tax Strategies to Maximise Savings

Year-end is your last opportunity to reduce your tax bill before the books close. A few well-timed decisions — on equipment purchases, pension contributions, or loss relief — can save a UK business thousands in corporation tax.

Capital Allowances and the Annual Investment Allowance (AIA)

The Annual Investment Allowance is permanently set at £1,000,000 per 12-month accounting period. This allows you to deduct the full cost of qualifying plant and machinery from taxable profits in the year of purchase.

Qualifying assets include:

- Computers, servers, and IT equipment

- Office furniture and fixtures

- Machinery and manufacturing equipment

- Commercial vehicles (excluding cars)

Strategic timing: If you're planning to purchase equipment early next year, bringing the purchase forward by a few weeks into the current financial year allows you to claim the deduction now, reducing this year's corporation tax bill.

R&D Tax Credits

For accounting periods beginning on or after 1 April 2024, UK companies investing in innovation can claim:

| Scheme | Relief Rate | Eligibility |

|---|---|---|

| Merged RDEC | 20% taxable expenditure credit | All companies (SME and large) |

| ERIS (Enhanced R&D Intensive Support) | 14.5% payable credit | Loss-making SMEs where R&D is ≥30% of total expenditure |

Many businesses underestimate what qualifies. Activities that typically meet HMRC's criteria include:

- Developing new products or significantly improving existing ones

- Creating or refining innovative processes

- Software development and prototype testing

- Advancing science or technology in your field

Note the PAYE cap: claims are limited to £20,000 plus 300% of your company's PAYE and NIC liabilities, so ensure your payroll is sufficient to support larger claims.

Timing of Bonuses, Dividends, and Pension Contributions

Getting the timing right on these three items can shift significant tax liability between periods:

- Bonuses paid before year-end reduce taxable profits in the current period; those accrued but paid later may only be deductible next year (check your accounting policy)

- Employer pension contributions are deductible in the period paid, not when accrued (Finance Act 2004 Section 196) — there's no earnings cap on employer contributions, but contributing more than 210% of last year's amount may spread relief across multiple periods

- Dividends don't reduce corporation tax since they're distributions of post-tax profit, but their timing matters for directors' personal tax planning — only declare dividends where post-tax profits support them, as paying from insufficient profits is illegal and can trigger director liability

Corporation Tax Loss Relief

Where timing strategies aren't enough and the year ends in a loss, HMRC provides several routes to recover tax:

- Current year relief: Offset losses against total profits in the same accounting period

- Carry-back: Carry losses back to the preceding 12 months to reclaim corporation tax paid previously

- Carry-forward: Carry losses forward against future total profits, subject to a 50% restriction on profits exceeding £5 million (for most SMEs, this restriction won't apply)

- Terminal loss relief: Losses in the final 12 months of trading can be carried back three years if you're closing the business

For most SMEs, carry-back delivers the fastest cash benefit — a refund of tax already paid. Carry-forward is the better choice when future profits are expected to be higher and you want to reduce a larger future bill.

Common Year-End Accounting Mistakes to Avoid

Missing Deadlines Due to Poor Date Tracking

With 317,985 penalties issued in one year, missing deadlines is the most common and costly error. Directors often confuse the two filing deadlines:

- Companies House: 9 months after year-end

- HMRC CT600: 12 months after year-end

Solution: Set calendar reminders three months before each deadline to begin preparation, not just a few weeks before.

Failing to Account for Accruals and Prepayments

Recording expenses only when invoices are paid — instead of when costs are incurred — distorts profit figures and can push profits into the wrong tax year. This triggers unexpected tax bills or causes you to miss relief opportunities.

Example: Your March utility bill arrives in April. Without accruing it in March, your year-end profit is overstated, and you pay corporation tax on income that doesn't exist.

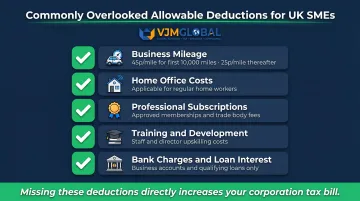

Overlooking Allowable Deductions

Common deductions SMEs miss:

- Business mileage (45p per mile for first 10,000 miles, 25p thereafter)

- Home office costs (if you work from home regularly)

- Professional subscriptions and memberships

- Training and development expenses

- Bank charges and interest on business loans

Leaving Year-End Preparation to the Last Few Weeks

According to FSB research, the average small business spends 52 hours per year on tax administration at an average cost of £4,100. Starting late compounds that cost — rushed reconciliations lead to missing documents and no time to act on tax-saving strategies before the window closes.

The typical accounting close takes several weeks to complete correctly.

When to start: Begin gathering records and reconciling accounts two months before your filing deadline. For complex businesses with multiple entities, international transactions, or VAT complications, start even earlier.

For businesses without in-house expertise, working with a specialist firm like VJM Global — which has supported 250+ UK businesses with year-end compliance — helps catch missed deductions, meet deadlines, and avoid penalties before they occur.

Frequently Asked Questions

What does an accountant need for year-end?

Your accountant requires bank statements, sales invoices, expense receipts, payroll records, VAT returns, fixed asset registers, and loan agreements for the full financial year. Organised records speed up the process and reduce professional fees.

When do year-end accounts need to be filed in the UK?

Limited companies must file with Companies House within 9 months of their financial year-end and submit the Corporation Tax Return (CT600) to HMRC within 12 months. Missing either deadline triggers automatic penalties.

What financial statements are included in UK year-end accounts?

UK statutory accounts include a Profit and Loss Statement, Balance Sheet, Directors' Report, and notes to the accounts. Smaller companies qualifying under FRS 105 need only a simplified balance sheet and minimal notes.

What happens if you miss the year-end accounts filing deadline?

Companies House imposes automatic penalties starting at £150 (up to 1 month late), rising to £1,500 for accounts over 6 months late. Penalties double automatically if you file late in two consecutive years, and directors face potential prosecution.

How can I reduce my corporation tax bill at year-end?

Claim capital allowances, make employer pension contributions, review R&D tax credit eligibility, and record all allowable expenses before year-end. With the small profits rate at 19% (under £50,000 profit) and the main rate at 25% (over £250,000), managing profit around these thresholds can reduce your tax liability by thousands.

Do sole traders need to file year-end accounts in the UK?

Sole traders are not required to file statutory accounts with Companies House (which registers limited companies only). However, sole traders must submit a Self Assessment tax return to HMRC by 31 January each year and should maintain accurate year-end records for tax purposes.