Introduction

For thousands of UK small businesses, the frustration is real: you invoice a customer today, but won't receive payment for 30, 60, or even 90 days. Yet under standard VAT rules, you owe HMRC that VAT immediately — often before you've collected a single payment. This cash flow squeeze is where the VAT Cash Accounting Scheme steps in: an HMRC-approved method that lets VAT-registered businesses account for VAT based on actual payments received and made, not on invoices issued.

The scheme is designed for small and medium-sized UK businesses, sole traders, and VAT-registered entities whose annual taxable turnover stays within £1.35 million. 61% of UK small businesses say late payments prevent them from reaching their full potential, with nearly half reporting more late payments than a year ago.

When you extend credit to customers or face slow-paying clients, the ability to defer VAT liability until you're actually paid gives businesses meaningful cash flow relief.

This article explains exactly how the Cash Accounting Scheme works, who qualifies, what the real-world trade-offs are, and when businesses should consider leaving or avoiding it altogether.

Key Takeaways

- The VAT Cash Accounting Scheme lets you pay VAT to HMRC only after customers pay you — not when invoices are issued

- Entry threshold: £1.35 million in annual taxable turnover; mandatory exit once turnover exceeds £1.6 million

- Provides automatic bad debt relief and better cash flow alignment for businesses with extended credit terms

- Input VAT reclaims on supplier invoices are delayed until you've actually paid them — and the scheme cannot be used alongside the VAT Flat Rate Scheme or for hire purchase, imports, and reverse charge transactions

What Is the VAT Cash Accounting Scheme?

Under the standard (accrual) VAT method, VAT becomes due (and reclaimable) on the date a VAT invoice is issued or received — regardless of whether money has actually changed hands. HMRC requires you to report these figures and pay any VAT owed even if invoices remain unpaid.

The Cash Accounting Scheme overrides this by tying VAT entirely to actual cash flow.

Core principle:

- Output tax (VAT on sales) is accounted for in the VAT return for the period in which payment is received from the customer

- Input tax (VAT on purchases) is only reclaimed in the period the supplier is actually paid

This means every entry in your VAT return is driven by bank transactions, receipts, and payment records — not invoice dates.

How It Differs from Other VAT Schemes

Not all VAT schemes are compatible with cash accounting. Here's how the two most common alternatives compare:

- VAT Flat Rate Scheme — applies a fixed percentage to gross turnover rather than tracking individual invoices. It cannot be used alongside the Cash Accounting Scheme; you must choose one or the other.

- Annual Accounting Scheme — reduces your VAT returns to one per year. Unlike the Flat Rate Scheme, it can be combined with Cash Accounting, giving you fewer filing deadlines alongside cash flow alignment.

How Does the VAT Cash Accounting Scheme Work?

The scheme replaces the invoice date as the VAT trigger point with the actual payment date. Every entry in your VAT return is based on bank transactions, not when you issue or receive invoices.

Determining the Date of Payment

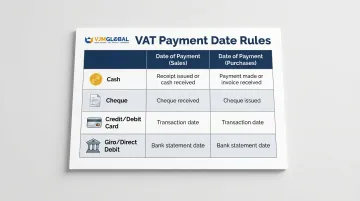

Payment dates vary by method, as defined in HMRC VAT Notice 731:

| Payment Method | Date of Payment (Sales) | Date of Payment (Purchases) |

|---|---|---|

| Cash (coins or notes) | Date you were given the money | Date you gave the money |

| Cheque | Date you receive the cheque, or the date on the cheque (whichever is later) | Date you post or give the cheque to supplier, or the date on the cheque (whichever is later) |

| Credit or debit card | Date you make out the sales voucher (not when the card provider pays you) | Date you authorise the card payment |

| Giro, standing order, or direct debit | Date your bank account is credited | Date your bank account is debited |

Important: If a cheque or card payment is dishonoured, no VAT is due — payment was never received.

Record-Keeping Requirements

You must maintain records that cross-reference:

- Every payment received to the corresponding sales invoice

- Every payment made to the corresponding purchase invoice

- All payments to bank statements, paying-in slips, and cheque stubs

For cash payments (coins or notes), if HMRC asks, you must endorse the customer's copy of the sales invoice with the amount paid and the date.

Output VAT on Sales

When a customer pays an invoice (in part or in full), identify the VAT element within that payment and record it as output tax in the VAT return for the period in which payment was received.

Example: You issue a £1,200 invoice (£1,000 + £200 VAT) on 15 January. The customer pays on 10 March. Under Cash Accounting, you report the £200 output tax in your March quarter VAT return — not January's.

Reclaiming Input VAT on Purchases

Input tax is only claimable once you've paid the supplier. If you buy goods on 60-day credit terms and pay in a later VAT period, the VAT reclaim belongs to that later period.

Example: You receive a supplier invoice for £600 (£500 + £100 VAT) on 5 February with 60-day payment terms. You pay on 10 April. You can only reclaim the £100 input VAT in your April quarter VAT return — not February's, even though you received the invoice then.

This delays recovery compared to standard accounting, where you can reclaim VAT upon receipt of the supplier invoice. Those payment dates — both incoming and outgoing — feed directly into how you complete your VAT return each period.

Completing Your VAT Return

When completing your VAT return:

- All figures for VAT due and VAT deductible are based on payments received and made during the period (not invoice values)

- The "value of outputs" and "value of inputs" boxes show payment amounts exclusive of VAT — not invoice totals

- Your VAT liability is calculated only on actual cash flow, not on invoiced amounts

Eligibility and Entry Conditions

To use the Cash Accounting Scheme, you must meet all the following conditions:

- VAT-registered business

- Estimated taxable turnover for the next 12 months must not exceed £1.35 million (excluding exempt supplies and capital asset disposals)

- All VAT returns up to date

- No outstanding VAT debt with HMRC (or a repayment arrangement in place)

- No VAT conviction, compounded proceedings, or dishonest conduct penalty in the last 12 months

- HMRC has not withdrawn or denied you access to the scheme in the last year

- VAT returns must be in sterling (not a foreign currency)

There's no formal HMRC application required. You simply begin using the scheme from the start of your next VAT accounting period. Make sure transactions already accounted for under standard accounting aren't counted again under the new scheme.

Excluded Transactions

Certain transactions must continue to follow standard VAT accounting rules, even when you're using the scheme:

- Goods bought or sold under hire purchase, conditional sale, or credit sale agreements

- Imported goods or acquisitions from EU member states

- Supplies subject to the VAT domestic reverse charge (construction services, wholesale gas and electricity, mobile phones)

- Supplies where a VAT invoice is issued and payment is not due in full within 6 months

- Supplies where a VAT invoice is issued in advance of making the supply

The hire purchase and advance invoice exclusions catch businesses out most often — if either applies to a transaction, it must be accounted for under standard VAT rules regardless of when cash actually changes hands.

Advantages and Disadvantages of the VAT Cash Accounting Scheme

Benefits of the Scheme

The cash accounting scheme offers three practical advantages for small and growing businesses:

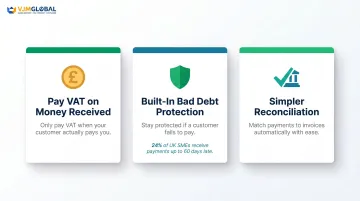

- Pays VAT only on money received — you never remit VAT on unpaid invoices. This matters most for businesses offering 30-, 60-, or 90-day credit terms. According to the 2025 GoCardless/FSB Late Payments Report, 24% of UK SMEs receive payments up to 60 days late, and 45% are experiencing more late payments than a year ago.

- Built-in bad debt protection — if a customer never pays, no VAT liability is triggered. Under standard accounting, you must wait at least 6 months from the payment due date and satisfy multiple conditions before claiming Bad Debt Relief.

- Simpler reconciliation — VAT records map directly to bank transactions. Payments in and out serve as primary evidence, removing the need to match invoices to specific VAT periods and simplifying month-end accounting for businesses with high transaction volumes.

The scheme does have limitations worth weighing before you commit.

Drawbacks of the Scheme

- Slower input VAT recovery — you cannot reclaim VAT on a supplier invoice until you've actually paid it. Under standard accounting, the invoice date triggers the reclaim. For businesses carrying significant purchases on extended credit terms, this timing gap can affect working capital.

- Incompatible with related schemes — the cash accounting scheme cannot be combined with the VAT Flat Rate Scheme. Hire purchase, imports, and reverse charge transactions must all be accounted for outside the scheme, creating a dual-accounting obligation for businesses with mixed transaction types.

- Turnover ceiling limits scalability — once annual taxable turnover approaches £1.35 million, close monitoring is required. Exceeding £1.6 million triggers a mandatory exit, which can force a disruptive accounting transition mid-growth phase.

When the Scheme Is Not the Right Choice — and How to Exit

Scenarios Where the Scheme Provides No Meaningful Advantage

The Cash Accounting Scheme is not beneficial for:

- Businesses paid immediately at point of sale (e.g., retail with card payments) — you receive payment and invoice at the same time, so there's no cash flow gap to manage

- Businesses in a net VAT repayment position — if you regularly reclaim more VAT than you pay (common for exporters or businesses with high capital expenditure), standard accounting processes refunds faster

- Construction sub-contractors subject to domestic reverse charge — these transactions are excluded from the scheme anyway, adding paperwork without any benefit

- Businesses making continuous supplies billed monthly — payment cycles are regular and predictable, so the scheme adds little value

Common Misconceptions About the Scheme

The scheme only changes when you pay VAT, not how much you owe. Businesses that treat it as a reduction in liability risk underpayment when they leave and must account for all outstanding invoices at once.

The scheme also applies to your entire VAT-registered business — not selected transactions. Outside of formally excluded types, you cannot choose which customers or invoices to include.

How to Leave the Scheme

Voluntary exit: You can leave voluntarily at the end of any VAT accounting period. You must then use the standard method of accounting for VAT from the beginning of the next period.

Mandatory exit: You must leave if:

- Taxable turnover exceeds £1.6 million in a rolling 12-month period

- HMRC withdraws use of the scheme

- You're convicted of a VAT offence or assessed to a penalty for VAT evasion involving dishonest conduct

- You cannot comply with record-keeping requirements

One-off capital asset exception: You may stay on the scheme even if you exceed £1.6 million, provided a genuine one-off sale (such as a capital asset disposal) caused it, it hasn't happened before, and you reasonably expect turnover to fall below £1.35 million in the next 12 months.

Exit VAT accounting obligation: On leaving, you must account for VAT on all outstanding sales invoices you haven't been paid for. You may also claim input VAT on all unpaid purchase invoices at the same time.

HMRC typically allows a 6-month window to report this outstanding tax — except where the £1.6 million threshold was breached and supplies in the previous 3 months exceeded £1.35 million.

For UK businesses weighing a scheme exit, VJM Global's VAT compliance team can manage the transition accounting, reconcile outstanding invoices, and ensure nothing falls through the gap between schemes.

Frequently Asked Questions

What is the VAT cash accounting scheme in the UK?

The VAT Cash Accounting Scheme is an HMRC-approved method allowing VAT-registered businesses to account for VAT based on payments actually received and made, rather than invoice dates. It's available to businesses with taxable turnover of £1.35 million or less.

What is the turnover limit for the VAT cash accounting scheme?

The entry threshold is £1.35 million in estimated annual taxable turnover. You can remain on the scheme until taxable turnover exceeds £1.6 million, at which point you must exit at the end of the current VAT period.

What is the difference between the VAT cash accounting scheme and the standard (accrual) VAT scheme?

Under standard VAT accounting, VAT is due and reclaimable on the invoice date regardless of payment. Under Cash Accounting, VAT is only triggered when money actually changes hands, which benefits cash flow but delays input tax recovery on unpaid supplier invoices.

When should I use the VAT cash accounting scheme?

The scheme suits businesses that regularly extend credit to customers, experience slow payment, or face bad debt risk. It's less beneficial for businesses paid immediately at point of sale or those in a net VAT repayment position.

When can or must I leave the VAT cash accounting scheme?

You can leave voluntarily at the end of any VAT period. You must leave if annual taxable turnover exceeds £1.6 million, if HMRC withdraws permission, or if VAT compliance conditions are breached. Any outstanding VAT on unpaid invoices becomes due on exit.

Is the VAT cash accounting scheme legal and available in the UK?

Yes, the scheme is a legitimate HMRC-approved option governed by the VAT Regulations 1995 and detailed in VAT Notice 731. Any eligible VAT-registered business can adopt it from the start of a new VAT accounting period without prior HMRC approval.