Introduction

HMRC requires mandatory registration within 30 days once taxable turnover exceeds £90,000 in any rolling 12-month period. Registration is not automatic — HMRC scrutinises every application, and late registration triggers backdated VAT liability on all sales made since the obligation date, plus potential penalties.

This guide covers UK-based businesses approaching the £90,000 threshold and overseas companies supplying to UK customers. The two groups face different rules: UK businesses benefit from the threshold exemption, while non-established taxable persons (NETPs) must register from their very first taxable supply, regardless of amount.

Here's what this guide covers:

- Eligibility criteria and registration thresholds

- Step-by-step online registration process

- Required documentation and common pitfalls

- VAT scheme selection (Flat Rate, Cash Accounting, Annual)

- Making Tax Digital compliance requirements

- Special rules for non-established foreign businesses

Key Takeaways

- VAT registration becomes mandatory once taxable turnover exceeds £90,000 in any rolling 12-month period

- Overseas businesses have no threshold—registration required from first UK taxable supply

- Register online via HMRC Government Gateway and receive a 9-digit VAT number upon approval

- All registered businesses must use MTD-compatible software to file returns digitally

- Pick a VAT scheme—Flat Rate, Cash Accounting, or Annual Accounting—based on your turnover and cash flow

What Is UK VAT Registration — and Who Needs to Register?

UK VAT registration is HMRC's formal process for authorising your business to charge VAT on taxable sales and reclaim VAT on business expenses. Once registered, you're legally required to collect VAT from customers and file periodic returns with HMRC.

Registration becomes mandatory when your taxable turnover exceeds £90,000 over any rolling 12-month period. You must register within 30 days of the end of the month you crossed that limit. Taxable turnover covers standard-rated, zero-rated, and reduced-rate supplies — but excludes VAT-exempt items like insurance or certain financial services.

If you're below the threshold, voluntary registration is still worth considering. The benefits include:

- Reclaim input VAT on business expenses immediately

- Signal credibility to corporate clients who require VAT invoices

- Streamline international trade processes and cross-border transactions

- Avoid rushed compliance when approaching the threshold

Step-by-Step: How to Register for VAT in the UK Online

Most UK businesses register online through HMRC's Government Gateway portal. Postal registration using form VAT1 is mandatory only for specific scenarios: Agricultural Flat Rate Scheme applicants, overseas partnerships, divisional registrations, or insolvency practitioners.

Step 1: Check Your Eligibility and Registration Trigger

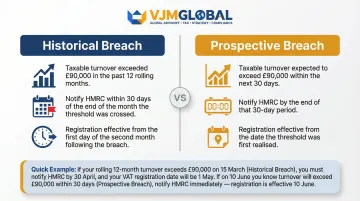

Determine whether registration is mandatory or prospective using these criteria:

| Trigger Type | Condition | Notification Deadline | Effective Date of Registration |

|---|---|---|---|

| Historical Breach | Taxable turnover exceeded £90,000 in last 12 months | Within 30 days of month-end | First day of second month after breach |

| Prospective Breach | Turnover will exceed £90,000 in next 30 days | By end of 30-day period | Date you realised threshold would be exceeded |

Example: If turnover exceeds £90,000 on 15 July, you must register by 30 August. Your effective registration date becomes 1 September.

Late registration consequence: You owe VAT on all taxable sales made from the date registration should have occurred, even if you never charged customers VAT. HMRC applies failure-to-notify penalties calculated as a percentage of potential lost revenue.

Step 2: Create or Sign Into Your HMRC Government Gateway Account

Access HMRC's Government Gateway portal and sign in with existing credentials. If no account exists, create one before beginning the registration. Applications save automatically, allowing you to return later if needed.

Step 3: Gather Your Required Documents

Limited company requirements:

- Company registration number from Companies House

- Unique Taxpayer Reference (UTR)

- Business bank account details

- Annual turnover details and 12-month estimates

- Corporation Tax and PAYE information

Sole trader or partnership requirements:

- National Insurance number

- Valid identity document (passport or driving licence)

- Business bank account details

- UTR if you complete Self Assessment

- Recent payslips or P60

- Partners must submit form VAT2 with full partner details

Overseas natural persons must provide:

- Government-issued photo ID (passport or national ID)

- Two recent correspondence items (bank statement or utility bill from last 3 months)

Step 4: Complete and Submit the Online VAT Application Form

Fill in details about business structure, trading activities, expected taxable turnover, and principal place of business (PPOB).

CRITICAL: HMRC defines PPOB as where essential management decisions occur and central administration takes place—where human and technical resources operate. An accountant's address, PO box, registered office, or virtual office does not satisfy this requirement.

HMRC increasingly uses Google Maps and Street View to verify addresses and check whether multiple VAT registrations share single locations. Applications with unsatisfactory addresses face delays or post-approval deletion without right of appeal.

Step 5: Wait for HMRC's Decision

HMRC reviews applications by verifying business substance and address legitimacy before approval. Processing typically takes 2–6 weeks, though complex or overseas applications may extend longer. HMRC's guidance states: "If you have not heard from us after 40 working days, contact our VAT Registration Service".

Interim invoicing rule: Do not charge VAT on invoices until you receive your VAT number. You may increase prices to account for anticipated VAT liability, but cannot show VAT separately. Once approved, reissue invoices within 30 days showing the full VAT-inclusive amount.

Step 6: Receive Your VAT Certificate and Number

Upon approval, HMRC issues a Certificate of Registration (VAT4) containing:

- 9-digit VAT registration number (format: GB123456789)

- Effective date of registration

- First return deadline and payment information

Sign up for your VAT online account immediately and enrol in Making Tax Digital unless exempt. The certificate can be viewed and printed digitally through the portal.

VAT Schemes and Post-Registration Obligations

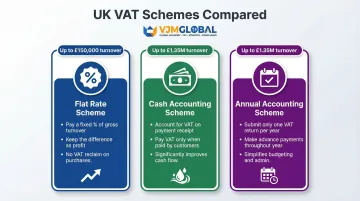

HMRC offers simplified schemes for different business types:

| Scheme | Turnover Threshold | How It Works | |--------|-------------------|--------------|\n| Flat Rate Scheme | £150,000 or less | Pay fixed percentage of gross turnover; keep difference charged to customers; cannot reclaim VAT on most purchases | | Cash Accounting Scheme | £1.35 million or less | Account for VAT when payment received/made; improves cash flow for businesses with payment delays | | Annual Accounting Scheme | £1.35 million or less | Submit one VAT return annually with advance payments; simplifies budgeting |

Core post-registration obligations:

- Charge correct VAT rates on taxable sales (20% standard, 5% reduced, 0% zero-rated)

- Issue VAT-compliant invoices showing VAT number and amount

- File VAT returns quarterly (or annually with Annual Accounting Scheme)

- Pay VAT owed by deadline (typically one month and 7 days after period end)

- Maintain accurate digital records

Making Tax Digital (MTD) Compliance

All VAT-registered businesses must use MTD-compatible software to maintain digital records and submit returns. Manual HMRC portal submissions ceased on 1 November 2022. Any data transfers between software tools must use digital links; manually copying figures between systems is not permitted.

Special Considerations for Overseas Businesses Registering for UK VAT

No registration threshold: Non-established taxable persons (businesses without a UK establishment) must register from their first taxable supply in the UK, regardless of amount. Common triggers include:

- Importing goods into the UK for sale

- Holding inventory in UK warehouses or fulfilment centres

- Selling goods or digital services directly to UK consumers

- Operating ecommerce models delivering goods into the UK

How HMRC determines UK establishment: HMRC determines UK establishment based on where essential management decisions occur and whether permanent physical presence exists with human and technical resources to make or receive supplies.

Principal place of business vs. registered address: The PPOB must be where actual business activities occur. Using an accountant's or solicitor's address does not satisfy HMRC requirements. Applications with invalid addresses risk deletion even after provisional approval.

Additional documentation for overseas applicants:

- Evidence of UK taxable supplies (contracts, invoices, logistics arrangements)

- Details of any UK establishment or confirmation of non-established status

- Power of attorney (form VAT1TR) if appointing a UK tax agent

Foreign companies navigating UK VAT registration often face additional complexity around establishment status, documentation, and agent appointments. VJM Global supports international businesses through this process, from assessing registration obligations to preparing compliant applications.

Common Mistakes to Avoid When Registering for VAT in the UK

VAT registration errors are more common than most applicants expect — and several of them carry real financial consequences. Watch out for these six pitfalls:

- Don't list a registered office as your principal place of business. HMRC requires premises where management decisions actually occur, not a Companies House address or accountant's office.

- Don't assume HMRC will approve quickly. Around 20–25% of applications take longer than 14 days due to incomplete information or missing documents.

- Avoid underestimating taxable turnover. Your figures must include standard-rated, zero-rated, and reduced-rate supplies — not just your headline revenue.

- Submit all required documents upfront. Missing identity documents, bank details, or a VAT2 partnership form will result in immediate rejection.

- Register before you hit the threshold — not after. Late registration triggers backdated VAT liability on all sales from the date you should have registered, and HMRC can demand VAT you never collected from customers.

- Never show VAT as a separate line on invoices until HMRC issues your VAT number. Doing so is treated as unauthorised VAT collection and can attract penalties.

Frequently Asked Questions

Who has to register for VAT in the UK?

UK businesses with taxable turnover exceeding £90,000 in any rolling 12-month period must register within 30 days. Overseas businesses making taxable supplies to UK customers must register from their first supply, with no minimum threshold. You can also register voluntarily below the threshold to reclaim input VAT and build credibility with VAT-registered clients.

How do I apply for a UK VAT number?

Most businesses apply online through HMRC's Government Gateway — sign in, complete the VAT registration form with your business and turnover details, and submit the required documents. Postal registration via form VAT1 applies only to Agricultural Flat Rate Scheme applicants, divisional registrations, and certain partnership structures.

Can a foreign company register for VAT in the UK?

Yes, overseas businesses can and often must register for UK VAT when making taxable supplies to UK customers. Unlike UK businesses, there is no minimum turnover threshold—registration is required from the first taxable supply. Foreign companies may appoint UK tax representatives using form VAT1TR.

Is it worth being VAT registered in the UK?

Key benefits of voluntary VAT registration include:

- Reclaiming input VAT on business expenses

- Enhanced credibility with corporate clients who require VAT invoices

- Smoother international trade processes

- Avoiding last-minute compliance pressure near the threshold

Weigh these against the added admin work: quarterly return filing and MTD-compatible software requirements.

How do I get my VAT certificate in the UK?

After HMRC approves your application, the VAT certificate (VAT4) arrives by post containing your 9-digit registration number, effective date, and first return deadline. You can also access it online through your VAT online account once enrolled.

How much does it cost to become VAT registered in the UK?

HMRC charges no fee for VAT registration. However, if you use an accountant or tax agent to prepare the application, manage ongoing compliance, or handle HMRC correspondence, professional fees will apply.