Introduction

If your Singapore-based business has paid UK VAT—on trade fair attendance, imported goods, or a business trip—you may be entitled to a refund. But there's a common trap: many companies waste time pursuing a route that no longer exists.

The first scenario —tourist VAT reclaims— is the Retail Export Scheme (VAT RES) for individuals. Since 1 January 2021, shoppers in Great Britain can no longer reclaim VAT on goods carried home in luggage. Airport VAT desks are closed, and airside tax-free shopping has ended across England, Scotland, and Wales.

The second route applies to Singapore-registered businesses that incur UK VAT on legitimate business expenditure. This route remains open. If your company paid VAT on trade fair attendance, goods imports, or business trip purchases, you can reclaim those costs through HMRC's non-UK business refund scheme under VAT Notice 723A.

This guide covers the business refund route—explaining eligibility, qualifying expenditure, document requirements, and the exact steps to submit a successful claim to HMRC before the strict 31 December deadline.

Key Takeaways

- The UK's tourist VAT refund scheme was abolished on 1 January 2021—visitors cannot claim VAT on retail purchases

- Singapore-registered businesses can still reclaim UK VAT on business expenses via HMRC's VAT Notice 723A

- Singapore-registered businesses can reclaim UK VAT on qualifying business expenses (trade fairs, imports) under HMRC VAT Notice 723A

- Claims use form VAT65A and must reach HMRC by 31 December following the prescribed year (1 July–30 June)

- You'll need an ACRA certificate confirming your Singapore business registration (valid 12 months)

- HMRC processes refunds within 6 months, paid via SWIFT or UK bank transfer

What Is UK VAT and Who Can Reclaim It?

UK VAT (Value Added Tax) is a consumption tax currently set at 20% on most goods and services [4]. Businesses registered for UK VAT reclaim it as input tax, but non-UK businesses without a UK VAT registration cannot use this route—they must use the overseas refund scheme instead.

The Two Refund Routes Explained

There are two distinct routes—only one remains available:

- VAT Retail Export Scheme (Abolished): Tourist shoppers could once reclaim VAT on goods taken home in luggage via airport desks. HMRC abolished this scheme across Great Britain on 31 December 2020 [5][6], with a limited version surviving in Northern Ireland only [7].

- Section 39 Business Refund Scheme (Active): Non-UK businesses can still claim VAT incurred on legitimate business expenditure under Section 39 of the Value Added Tax Act 1994 [2][3]. This route is governed by HMRC VAT Notice 723A [1].

Most Singapore companies miss this route entirely—it never attracted the same attention as the now-defunct tourist scheme.

Why Singapore Businesses Qualify

HMRC requires reciprocity—your home country must allow similar concessions to UK businesses [1]. Singapore operates a Tourist Refund Scheme [8], and HMRC does not publish a list of excluded countries, meaning Singapore-based businesses generally qualify.

Do Singapore-Based Businesses Qualify for UK VAT Refunds?

Not every Singapore business can claim. HMRC applies a strict two-part eligibility test under VAT Notice 723A [1]:

Core Eligibility Conditions

- No UK VAT registration: You must not be registered, liable, or eligible to register for VAT in the UK

- No UK establishment or taxable supplies: You have no place of business or residence in the UK, and you make no taxable supplies there (except narrow exceptions like international transport services or reverse-charge supplies)

What Expenditure Qualifies?

Eligible for reclaim:

- Goods and services purchased in the UK for business purposes

- Goods imported into the UK (if you own them and importing doesn't trigger UK VAT registration)

Practical Singapore examples:

- Attending a London trade exhibition and paying VAT on booth hire, materials, accommodation

- Purchasing machinery or samples during a UK business trip

- Importing UK goods into the UK as part of a supply chain

What's Excluded?

| Expenditure Type | Claimable? | Notes |

|---|---|---|

| Business goods/services | ✅ Yes | Must be for business purposes [1] |

| Imported goods | ✅ Yes | If you own them and no UK VAT liability created [1] |

| Business entertainment | ❌ No | Excluded unless very basic hospitality for overseas customers [1] |

| Ordinary business cars | ❌ No | Only 50% VAT on hired/leased cars for mixed use [1] |

| Goods for resale to travellers | ❌ No | For example, hotel accommodation for direct resale [1] |

| Exempt supplies | ❌ No | VAT used to make exempt supplies outside UK [1] |

Partial Exemption Rule

If your Singapore business makes both taxable and exempt supplies, only the VAT attributable to taxable supplies can be reclaimed [1]. You must apportion costs carefully before filing to avoid HMRC penalties for incorrect claims.

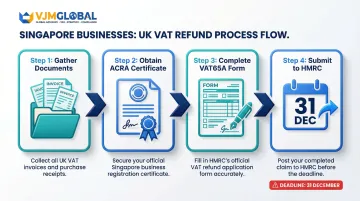

How to Claim UK VAT Refunds from Singapore: Step-by-Step

Each step in this process has specific HMRC requirements—missing a single document field or deadline can result in outright rejection. Work through the steps below in order before submitting your claim.

Step 1: Gather Your Supporting Documents

HMRC requires specific invoice fields. Missing details will result in rejection.

Full VAT invoice (for supplies over £250 including VAT):

- Supplier's name, address, and UK VAT registration number

- Your business name and address

- Identifying invoice number

- Description of goods or services

- Date of supply

- Net cost excluding VAT

- VAT rate applied

- VAT amount charged [1]

Simplified invoice (£250 or less including VAT):

- Supplier name, address, and UK VAT number

- Supply date

- Description

- Total cost including VAT

- VAT rate [1]

For imports:

- VAT copy of the customs import entry (e.g., C79 certificate) showing VAT paid [1]

Keep original documents until claims are fully processed. HMRC may request them even after initial submission [1].

Step 2: Obtain a Certificate of Status from Singapore

First-time applicants must include an original certificate of status from an official Singapore authority [1]. The ACRA (Accounting and Corporate Regulatory Authority) Business Profile confirms your business registration status to HMRC [9].

The certificate must contain:

- Authority name, address, and official stamp

- Your business name and address

- Nature of business

- Business registration number [1]

Validity: 12 months from issue date, covering multiple applications in that period [1]

If your business is not registered with ACRA or you cannot obtain the Business Profile, HMRC form VAT66A is an accepted alternative [10][11].

Step 3: Complete the VAT65A Application Form

Form VAT65A must be completed electronically—HMRC explicitly rejects handwritten schedules at question 9 [1].

Key points:

- The prescribed refund year runs 1 July to 30 June

- You can claim for as little as 3 calendar months or the full year

- Singapore businesses may authorise an agent (such as a tax advisory firm) to submit on their behalf using a Power of Attorney or HMRC-specified letter of authority [1]

Step 4: Submit to HMRC via SDES or Post

You can submit your completed claim electronically or by post—both routes require the same core documents.

Electronic Submission (SDES):

- Register for HMRC's Secure Data Exchange Service by emailing the Overseas Repayment Unit at

newcastle.oru@hmrc.gov.uk[12] with "SDES" in the subject line [1] - Registration deadline: 30 November to meet the 31 December claim deadline [1]

- Upload VAT65A, certificate of status, invoices, and supporting documents

Postal Submission:

- Send to: HM Revenue and Customs, Compliance Centres, VAT Overseas Repayment Unit S1250, Benton Park View, Newcastle upon Tyne, NE98 1YX, United Kingdom [1]

- Include the original certificate of status; copies of other documents are acceptable [1]

Key Deadlines, Minimum Claim Amounts, and Payment

Critical Deadlines

| Deadline | Requirement |

|---|---|

| 31 December | All applications must reach HMRC by this date—no exceptions unless documented exceptional events (pandemics, national emergencies) [1] |

| 30 November | SDES registration requests must be submitted to file electronically by 31 December [1] |

| 1 July–30 June | Prescribed refund year [1] |

HMRC applies the 31 December deadline "strictly" to ensure fair treatment on a first-come, first-served basis [1].

Minimum Claim Thresholds

- 3+ months but less than full year: £130 minimum [1]

- Full prescribed year (or remainder): £16 minimum [1]

Small one-off claims below £130 may not justify the administrative effort — waiting to accumulate a full-year claim is often the practical approach.

Payment Process

HMRC aims to process satisfactory applications within 6 months of receipt [1]. Refunds are paid in pound sterling (£) to your bank account.

HMRC supports payment via SWIFT transfer (recommended for being faster, cheaper, and more secure) or directly to a UK bank account [1].

Required bank details:

- Account number

- Currency (GBP)

- BIC/SWIFT code

- Account name

- Bank name and address [1]

Overpayments are deducted from future refunds. HMRC may impose penalties for false or incorrect applications [1].

Common Mistakes and When a UK VAT Refund May Not Be Worth Pursuing

The Retail Export Scheme no longer exists in Great Britain — VAT cannot be reclaimed on goods purchased in England, Scotland, or Wales and carried home in luggage [5][6]. Only business expenditure claimed under VAT Notice 723A remains available to Singapore-registered businesses.

Document Completeness Traps

HMRC rejects or delays claims when:

- Invoices are missing required fields (especially the supplier's UK VAT number or your business name)

- The certificate of status is a copy rather than the original (for postal submissions)

- The VAT65A schedule at question 9 is handwritten instead of typed [1]

Keep original documents until claims are fully processed and ensure every field is complete before submission [1].

Business-Use Exclusions

Singapore businesses sometimes include VAT on:

- Entertainment expenses

- Hotel bills for personal stays

- Goods used in the UK rather than exported

HMRC explicitly excludes all three categories [1] — including them risks the entire application being queried or rejected.

When Claiming Isn't Worth It

Skip the claim if any of the following apply:

- Total refundable VAT for a period under 12 months falls below £130 (the minimum threshold to file)

- Your UK VAT-bearing expenditure is low — for example, a single small trade show with minimal qualifying costs

- The administrative burden of obtaining the ACRA certificate, completing VAT65A, and coordinating with HMRC outweighs the refund value

In these cases, a better approach is to wait and accumulate a full-year claim (1 July–30 June). The effort is the same regardless of claim size, so consolidating into one larger submission maximises the return on that effort.

Frequently Asked Questions

Can I still get a VAT refund in the UK?

It depends who is asking. Tourists visiting Great Britain can no longer get VAT refunds (scheme ended January 2021). Singapore-registered businesses that incurred VAT on legitimate UK business expenses can still claim refunds via HMRC's non-UK business refund scheme [1][5].

Can I claim VAT back on a UK purchase?

Singapore businesses can claim VAT back on UK purchases made for business purposes—goods, services, and imports—provided they are not UK VAT-registered and have no UK establishment. Personal or tourist purchases do not qualify [1].

How much VAT can you claim back in the UK?

The UK standard VAT rate is 20% [4], so businesses can reclaim 20% of eligible net business expenditure. Minimum claim thresholds apply: £130 for periods under 12 months, £16 for full-year applications [1].

How do I claim a VAT refund in the UK?

Singapore businesses complete form VAT65A, attach an ACRA certificate of status and original VAT invoices, then submit to HMRC via SDES (electronic) or post before the 31 December deadline. Refunds process within 6 months [1].

Can you claim VAT back at the airport when leaving the UK?

No. Airport VAT refund desks for departing travellers no longer operate in Great Britain. The UK government abolished airside tax-free shopping and the Retail Export Scheme on 1 January 2021 [5][6]. A limited scheme exists for Northern Ireland only [7].

Can you get a VAT refund after leaving the UK?

Singapore businesses can claim UK VAT refunds after returning home by submitting the VAT65A application to HMRC remotely—electronically via SDES or by post. There is no requirement to process the claim while in the UK, but all applications must reach HMRC by 31 December of the applicable year [1].

Need help with international tax compliance? VJM Global's team of Chartered Accountants has supported 250+ UK businesses and hundreds of international clients with cross-border tax obligations, including VAT recovery, international taxation, and multi-jurisdiction compliance. With 30+ years of advisory experience, we help businesses recover what they're owed while staying fully compliant. Contact our team to discuss your situation.