Introduction

Singapore businesses expanding into the UK market often encounter an unexpected compliance hurdle: UK VAT obligations can arise from the very first sale—even without a physical presence in the United Kingdom. Unlike Singapore's straightforward 9% GST framework, UK VAT operates with multiple rates, complex registration rules, and a first-supply trigger that trips up many foreign sellers before they've had time to plan.

This guide covers what Singapore businesses need to know to get it right: UK VAT rates and categories, registration rules for non-UK sellers, how the input/output tax mechanism works, cross-border transaction treatment, and ongoing filing obligations.

Whether you're shipping physical goods to UK customers, operating a UK fulfilment centre, or selling digital services to British consumers, getting ahead of these obligations prevents penalties and keeps your expansion on track.

Key Takeaways

- Singapore businesses must register for UK VAT from the first taxable supply — no threshold applies

- UK VAT runs three active rates: 20% standard, 5% reduced, and 0% zero-rated

- Digital services sold B2C to UK consumers are taxable from the very first sale

- All UK VAT returns must be filed via Making Tax Digital (MTD)-compatible software

- Postponed VAT Accounting (PVA) lets registered importers defer import VAT to their return

What is UK VAT and How It Differs from Singapore GST

UK VAT (Value Added Tax) is a consumption tax administered by HMRC and levied at each stage of the supply chain. Businesses collect and remit VAT to HMRC, but the economic cost falls on the end consumer — the same indirect tax structure as Singapore's GST.

Both systems share input tax recovery mechanisms, but the operational rules for foreign businesses differ considerably.

Brief Comparison to Singapore's GST

Both UK VAT and Singapore GST are consumption taxes with input tax recovery mechanisms, but several key differences exist:

- Rates: Singapore GST is currently 9% flat, while UK VAT operates at 20% standard, 5% reduced, and 0% zero-rated

- Revenue significance: VAT is projected to raise £179.6 billion in 2025-26, representing 14.6% of all UK government receipts — making it the second-largest revenue source

- History: UK VAT was introduced on 1 April 1973, predating Singapore's GST framework by over two decades

Of these differences, one has the most immediate operational impact for Singapore businesses selling into the UK.

The Critical Difference for Singapore Businesses

The most important structural difference: foreign businesses making taxable supplies in the UK must register for VAT from the very first sale. No minimum threshold applies.

This is a direct contrast to Singapore's GST regime, where registration is only required once turnover exceeds S$1 million. A Singapore software firm making its first UK sale of £500 is immediately liable to register — the obligation begins at sale one, not after crossing a revenue threshold. Understanding this from the outset prevents unexpected penalties and compliance gaps.

UK VAT Rates: Standard, Reduced, Zero-Rated, and Exempt

Understanding which VAT rate applies to your products or services is critical for pricing and compliance.

Standard Rate: 20%

The standard rate of 20% applies to most goods and services, including:

- Electronics and technology products

- Adult clothing and footwear

- Restaurant meals and hot takeaways

- Hotel accommodation

- Professional services (consulting, legal, accounting)

Calculation example: A £500 consulting fee attracts £100 VAT (£500 × 20%), making the total invoice £600.

Reduced Rate: 5%

The reduced rate of 5% covers a narrow range of goods and services:

- Domestic fuel and power

- Children's car seats

- Eligible energy-saving materials and approved health products

HMRC defines this rate narrowly, so always verify eligibility against official guidance before applying it.

Zero-Rated Supplies: 0%

Zero-rated supplies attract 0% VAT but remain taxable supplies:

- Most food (but not restaurant meals or hot takeaways)

- Children's clothing and footwear

- Books, newspapers, and magazines

- Prescription medicines

- International freight transport

Critical distinction: Zero-rated is NOT the same as exempt. Businesses making zero-rated supplies must still register for VAT once they cross the threshold and can reclaim input VAT on related costs.

The zero-rated vs. exempt distinction catches many Singapore businesses off guard — the table below clarifies how each category works in practice.

Exempt vs. Zero-Rated: A Comparison

| Feature | Zero-Rated (0%) | Exempt |

|---|---|---|

| VAT charged | 0% | None |

| Taxable supply? | Yes | No |

| Input VAT recovery | Yes—fully reclaimable | No—generally blocked |

| Registration required | Yes (if threshold met) | Only if making other taxable supplies |

| Common examples | Food, books, children's clothing | Insurance, finance, healthcare, education |

Exempt supplies—such as financial services, insurance, healthcare, and education—generate no output VAT but also block input VAT recovery on related costs. For Singapore businesses selling into the UK with a mix of exempt and taxable supplies, this means only a proportion of input VAT may be recoverable — and that proportion needs careful calculation each period.

Outside the Scope

Certain transactions fall entirely outside the UK VAT system:

- Statutory fees (MOT testing, public authority charges)

- Freely given charitable donations where nothing is received in return

These need not appear on a VAT return.

Who Must Register for UK VAT: The Critical Rule for Singapore Businesses

UK-Established Businesses: £90,000 Threshold

For businesses established in the UK, the VAT registration threshold is £90,000 taxable turnover in any rolling 12-month period (increased from £85,000 on 1 April 2024). This threshold is measured on taxable turnover—including zero-rated sales—not profit.

Singapore Businesses: No Threshold—Register from First Sale

Non-UK established businesses making taxable supplies in the UK have NO registration threshold. They must register for UK VAT from the very first taxable supply and notify HMRC within 30 days.

This applies to any business without a UK establishment—including Singapore companies—and is a common compliance trap for foreign sellers.

What Counts as "Making Taxable Supplies in the UK"

For Singapore businesses, taxable UK supplies typically include:

- Selling physical goods located in the UK at the point of sale — if your products are stored in UK warehouses or fulfilment centres (including third-party logistics providers like Amazon FBA), you're making UK supplies

- Fulfilling orders from UK-based inventory — even if the sale originates from your Singapore website

- Providing services with a UK place of supply — subject to specific place-of-supply rules

Digital Services: UK VAT from the First Sale

The rules above cover physical goods and general services. Digital products follow a different logic. For Singapore SaaS companies, app developers, and digital content platforms, the place of supply for B2C digital services (streaming, software, e-books) is where the consumer is located, not where the seller is based. This means:

- UK VAT at 20% must be charged from the first sale to a UK consumer

- The UK is not part of the EU's One Stop Shop (OSS) scheme post-Brexit, so a separate UK VAT registration is required

- B2B digital services typically fall under the reverse charge mechanism (see Cross-Border Transactions below)

Voluntary Registration

Singapore businesses whose UK taxable turnover is below the threshold may still choose voluntary registration to:

- Reclaim input VAT on UK business costs (importing goods, professional fees, marketing spend)

- Enhance credibility with UK business partners who prefer VAT-registered suppliers

- Prepare for anticipated growth into the UK market

Whether mandatory or voluntary registration applies to your situation depends on your sales model and UK activity. VJM Global works with Singapore businesses to determine their UK VAT obligations and handles the HMRC registration process end-to-end.

How UK VAT Works: Charging, Recovering, and Filing Returns

For Singapore businesses selling into the UK, VAT isn't just a tax to collect — it affects your pricing, cash flow, and compliance obligations at every stage of the supply chain. Here's how the mechanism works in practice.

Output Tax vs. Input Tax: A Supply Chain Example

Scenario: A Singapore manufacturer sells goods to a UK distributor (£1,000 net), who sells to a UK retailer (£1,500 net), who sells to a UK consumer (£2,000 net). All transactions are standard-rated at 20%.

- Singapore manufacturer → UK distributor: £1,000 + £200 VAT = £1,200 total. Manufacturer collects £200 output VAT and remits it to HMRC.

- UK distributor → UK retailer: £1,500 + £300 VAT = £1,800 total. Distributor collects £300 output VAT, deducts £200 input VAT (paid to manufacturer), and remits £100 net to HMRC.

- UK retailer → UK consumer: £2,000 + £400 VAT = £2,400 total. Retailer collects £400 output VAT, deducts £300 input VAT (paid to distributor), and remits £100 net to HMRC.

Total VAT collected by HMRC: £200 + £100 + £100 = £400 (which equals 20% of the final consumer price). Each business remits only the incremental VAT at its stage of the supply chain.

VAT Return Filing: Frequency and Deadlines

The default VAT return filing frequency is quarterly. If you expect regular VAT refunds — common when input tax consistently exceeds output tax — you can apply for monthly returns to recover cash faster.

Key requirements:

- Returns must report total output VAT charged and total input VAT recoverable

- The business pays (or claims a refund of) the difference

- Returns and payments are due one month and seven days after the reporting period ends

Making Tax Digital (MTD): Mandatory Software Requirement

UK VAT returns must be filed digitally through MTD-compatible software — there is no paper or manual filing option. For Singapore businesses managing UK compliance remotely, this means selecting and configuring a compliant platform before you file your first return.

Compatible platforms include:

- Xero

- QuickBooks

- Sage

- Other HMRC-approved MTD software providers

Subscription costs typically range from £12–£35/month depending on the platform and plan. Budget for this alongside your UK VAT registration setup.

Postponed VAT Accounting (PVA): Cash-Flow Relief for Importers

Postponed VAT Accounting lets you account for import VAT on your VAT return instead of paying it upfront at the UK border. For Singapore exporters shipping goods regularly into the UK, this avoids tying up working capital at customs — sometimes weeks before the goods are even sold.

How it works:

- Select PVA on your customs declaration and provide your VAT registration number and EORI number

- Download monthly postponed import VAT statements from the Customs Declaration Service

- Declare the import VAT on your VAT return as both output tax (owed) and input tax (reclaimable), resulting in a net-zero position if the goods are used for taxable supplies

- Hold valid UK VAT registration and proper customs documentation — both are required to use PVA

UK VAT on Cross-Border Transactions: What Singapore Exporters Need to Know

Cross-border trade introduces additional VAT complexity.

Exporting Goods from the UK

Goods exported from the UK can be zero-rated, meaning no VAT is charged to the overseas customer. Strict conditions apply:

- Goods must be exported within specific time limits (typically three months)

- The supplier must obtain and retain official or commercial proof of export

- If evidence is unsatisfactory or missing, the standard 20% VAT rate becomes due

Importing Goods into the UK

When Singapore businesses ship goods to UK customers, the importer of record becomes liable for UK import VAT at the border. Singapore exporters should clarify contractual responsibility for this cost before shipment:

- Delivered Duty Paid (DDP): the seller covers import VAT

- Delivered Duty Unpaid (DDU): the buyer bears the import VAT burden

B2B Reverse Charge for Services

When a Singapore business provides services to a UK VAT-registered business, the reverse charge mechanism applies. The UK customer accounts for VAT under the reverse charge, meaning the Singapore supplier does not charge UK VAT. The UK business acts as both supplier and recipient, reporting the VAT on its own return.

For B2C services (to UK consumers), UK VAT rules apply and the Singapore supplier must register and charge VAT.

Post-Brexit Context

Since 1 January 2021, the UK operates its own independent VAT framework, separate from EU VAT rules. Singapore businesses that previously relied on EU VAT registrations to cover UK sales must now maintain a separate UK VAT registration — the two systems are no longer interchangeable. Reviewing your registration status and supply chain structure against the current UK rules is a practical first step.

UK VAT Compliance: Invoicing Requirements and Penalties

UK VAT invoices must meet strict HMRC-defined requirements — and they differ meaningfully from Singapore's GST invoicing norms. Getting this right protects your input VAT claims and keeps you clear of penalties.

What a Valid UK VAT Invoice Must Contain

A valid VAT invoice must include:

- Supplier name, address, and VAT registration number

- Invoice date and unique sequential invoice number

- Customer name and address

- Description sufficient to identify the goods or services

- Quantity of goods or extent of services

- VAT rate applied to each line item

- VAT amount charged for each rate

- Total amount payable excluding VAT

- Total VAT chargeable (in GBP)

- Unit price (where applicable)

- Rate of any cash discount offered

Non-compliant invoices can invalidate an input VAT claim, so every field matters. VAT records must also be retained for at least six years — a requirement worth building into your document management process from the start.

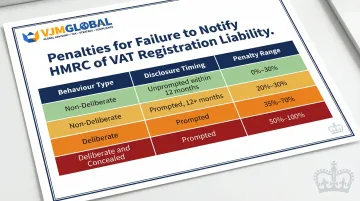

Key VAT Penalties for Singapore Businesses

Failure to notify HMRC of registration liability carries penalties from 0% to 100% of potential lost revenue, scaled by behaviour and disclosure timing:

| Behaviour Type | Disclosure Timing | Penalty Range |

|---|---|---|

| Non-deliberate | Unprompted (within 12 months) | 0%–30% |

| Non-deliberate | Prompted (12+ months) | 20%–30% |

| Deliberate | Prompted | 35%–70% |

| Deliberate and concealed | Prompted | 50%–100% |

For late VAT return submissions, a points-based penalty system has applied since 1 January 2023:

- Quarterly filers: 4 points threshold → £200 penalty

- Monthly filers: 5 points threshold → £200 penalty

- A further £200 penalty for each subsequent late submission while at threshold

Late VAT payments accrue interest at the Bank of England base rate plus 4%, running from the first day overdue until paid in full.

Managing UK VAT Compliance from Singapore

Handling UK VAT compliance remotely adds operational complexity:

- Time zone differences complicate HMRC correspondence

- Unfamiliarity with HMRC systems and processes creates risk

- MTD software requirements demand technical setup

- Ongoing return preparation and reconciliation consume internal resources

Working with a specialist in cross-border tax compliance — one familiar with both HMRC's systems and the practicalities of managing obligations from outside the UK — reduces this burden significantly and lowers your exposure to avoidable penalties.

Frequently Asked Questions

What is VAT and how does it work in the UK?

VAT (Value Added Tax) is an indirect consumption tax charged at each stage of the supply chain, currently set at a standard rate of 20%. Businesses collect VAT on behalf of HMRC, and the end consumer ultimately bears the economic cost.

What are the different VAT rates in the UK?

The UK operates three rates: 20% standard (most goods and services), 5% reduced (domestic fuel, certain health products), and 0% zero-rated (food, children's clothing, books). Exempt and outside-the-scope categories also exist but are not taxable supplies.

Who must register for VAT in the UK and what is the registration threshold?

UK-established businesses must register when taxable turnover exceeds £90,000 in a rolling 12-month period. Non-UK businesses, including those from Singapore, have no threshold and must register from their first taxable supply made in the UK.

How much VAT is charged on £500 in the UK?

At the standard 20% rate, VAT on £500 (net) is £100, making the VAT-inclusive total £600. If £500 is the VAT-inclusive price, the VAT element is £83.33 (calculated as £500 ÷ 1.2 × 0.2).

Are prices in the UK shown with VAT included?

Retail prices displayed to consumers in the UK must include VAT by law. B2B invoices typically show the net price and VAT amount separately—a key distinction to understand when handling UK supplier or customer invoices.