%20(3).jpg)

Whether you're a Singapore startup or a subsidiary of a multinational group, understanding audit exemption rules can help you reduce compliance costs without compromising financial accountability. Under Section 205C of the Companies Act, qualifying "small companies" can skip the mandatory annual statutory audit—but many business owners don't fully understand when exemption applies, what obligations remain, and how recent regulatory changes might affect them.

This guide breaks down Singapore's audit exemption framework: who qualifies, how group structures affect eligibility, what financial obligations stay in place, and what ACRA's 2026 review could mean for your business.

Under Section 205C of the Singapore Companies Act, all incorporated companies are generally required to have their financial statements audited annually. However, qualifying "small companies" are exempt from this obligation, reducing compliance costs without eliminating financial accountability.

What the exemption means:

What it does not mean:

The current framework replaced a much narrower rule. Before July 1, 2015, only Exempt Private Companies (EPCs) with annual revenue under S$5 million qualified for exemption. The Companies (Amendment) Act 2014 replaced this with a broader "small company" concept, introducing quantitative thresholds across revenue, assets, and headcount — a structure that took effect from July 1, 2015 and opened the exemption to significantly more businesses.

To qualify for audit exemption, your company must meet two core conditions:

Public companies are not eligible for this exemption, regardless of size.

Your company qualifies as a "small company" if it meets at least two of the following criteria:

CriteriaThresholdTotal annual revenue≤ S$10 millionTotal assets≤ S$10 million at year-endFull-time employees≤ 50 at year-end

These thresholds must be met across the immediate past two consecutive financial years to maintain exemption status.

Companies incorporated less than two years ago follow a simplified assessment:

Example: If your company is in its first financial year, you check the criteria for that year only. If you meet 2 of the 3 thresholds, you qualify for exemption immediately.

Companies incorporated before July 1, 2015 had a transitional rule:

Unlike the old EPC criteria, the current framework places no restrictions on corporate shareholders. Having a corporate shareholder does not disqualify your company from exemption.

If your company is part of a corporate group, audit exemption becomes more complex. Both the individual company and the entire group must qualify.

What constitutes a "group"?

Dual requirement:

Meeting only one condition is not enough — both must be satisfied simultaneously.

A small group must meet at least two of the following three thresholds on a consolidated basis for the immediate past two consecutive financial years:

Consolidated figures are drawn from:

"My subsidiary qualifies individually as a small company, so it's exempt."

"Our group is a small group, so all subsidiaries are automatically exempt."

When assessing whether a group meets the "small group" criteria, all entities under the group — including those incorporated or based overseas — are counted in the consolidated figures. That said, the audit exemption under Section 205C only applies to Singapore-incorporated companies; foreign subsidiaries remain subject to the audit requirements of their own jurisdictions.

Once qualified, your company continues to be exempt in subsequent financial years unless one of two disqualifying events occurs.

The loss is not immediate. A single bad year does not strip the exemption. The company must fail the criteria for two consecutive years before losing audit exemption status.

Example:

Once disqualification kicks in, the company must take immediate compliance action:

If your company is operating close to the thresholds, track your financials annually so changes in audit status don't catch you off guard. An unexpected shift to non-exempt status can leave you scrambling to appoint auditors under tight deadlines.

Audit exemption does not eliminate your company's fundamental financial obligations. Several requirements remain in place.

Section 199 of the Companies Act requires every company to keep accounting records that:

Failure to maintain proper records is a compliance breach, even for exempt companies.

Exempt companies must still:

The financial statements are unaudited — no external auditor reviews them — but they must still give a true and fair view of the company's performance. That responsibility falls entirely on management. For cross-border businesses handling multiple jurisdictions, outsourced accounting support — such as the services VJM Global provides — can help ensure SFRS-compliant statements and accurate filings.

Even if your company is exempt, shareholders holding at least 5% of the total issued shares retain the right to require the company to conduct a statutory audit. This provides a check on management and ensures minority shareholders can demand accountability when needed.

In February 2026, ACRA announced a formal review of Singapore's audit exemption framework, noting that average company asset values and revenues have grown considerably since the S$10 million thresholds were set in 2015.

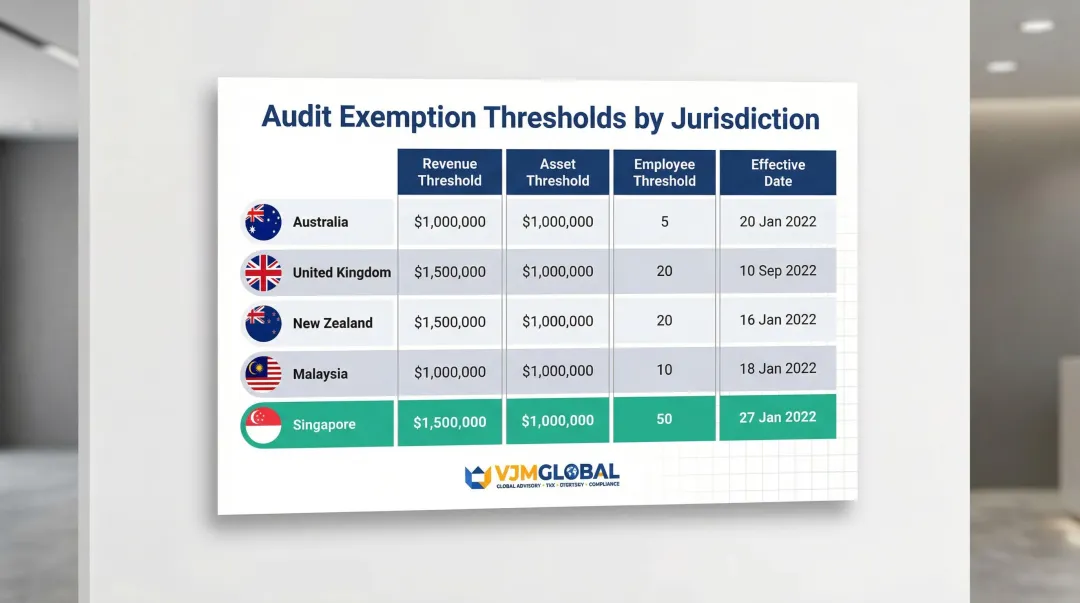

ACRA observed that comparable jurisdictions including Australia, the UK, New Zealand, and Malaysia have raised their audit exemption thresholds in recent years to account for inflation and economic growth.JurisdictionRevenue ThresholdAsset ThresholdEmployee ThresholdEffective DateAustralia≥ A$50 million≥ A$25 million≥ 100 employees1 July 2019United Kingdom≤ £15 million≤ £7.5 million≤ 50 employees6 April 2025New Zealand> NZ$33 million> NZ$66 millionN/A29 September 2025Malaysia≤ RM3 million≤ RM3 million≤ 30 employees1 January 2027

ACRA is focusing on two primary areas:

Targeted industry consultations commenced in March 2026. Companies can track updates and submit feedback directly through ACRA's official review page.

If thresholds are raised, companies currently sitting just above the S$10 million mark — particularly subsidiaries of larger groups — should reassess their eligibility once final guidelines are published.

Audit exemption is a provision under Section 205C of the Singapore Companies Act that allows qualifying "small companies" to skip the mandatory annual statutory audit. This reduces compliance costs while still requiring companies to prepare and file SFRS-compliant financial statements.

Statutory audit is mandatory by default for all Singapore-incorporated companies. However, private companies that qualify as "small companies" (or belong to a "small group") are exempt. Dormant companies may also qualify for a separate exemption under Section 205B.

Private companies qualify if they meet at least 2 out of 3 criteria (revenue ≤ S$10M, assets ≤ S$10M, ≤50 employees) for the past two consecutive financial years. Group companies must additionally satisfy the small group consolidated test.

No formal application or approval from ACRA is required—the exemption is automatic once a company meets the qualifying criteria. Companies should, however, assess their eligibility each financial year and maintain documentation supporting their qualifying status.

Yes. The two-year rule is central to the framework—a company must meet at least two of the three quantitative criteria for the two immediately preceding consecutive financial years to qualify. Similarly, a company must fail those criteria for two consecutive years before losing the exemption.

Internal audit is not mandatory for all Singapore companies under the Companies Act. It is typically required for SGX-listed companies and certain regulated entities. The audit exemption framework discussed in this article relates specifically to statutory (external) audit requirements.

Preparing SFRS-Compliant Financials Without an Auditor?

Qualifying for audit exemption doesn't eliminate your obligation to produce accurate, SFRS-compliant financial statements. VJM Global's team of CPAs and Chartered Accountants supports foreign companies — including USA, UK, and Australian businesses with Singapore operations — in maintaining compliant books and managing cross-border accounting requirements. With 30+ years of experience across international compliance, we can help you stay on track without unnecessary overhead. Contact us to discuss your requirements.