Mergers and acquisitions continue to dominate boardroom strategies, with a 2024 survey revealing that 72% of executives expect their next M&A deal to occur by the first half of 2025 18% before the end of 2024, and 54% in early 2025.

With deal activity accelerating, accurate valuation has never been more important, and so ASC 805 (Business Combinations) becomes essential.

ASC 805, issued by the Financial Accounting Standards Board (FASB), provides the framework for recognizing and measuring assets, liabilities, and goodwill during business combinations. For U.S. businesses expanding globally or acquiring offshore entities, understanding these rules ensures accuracy, compliance, and transparency in financial reporting.

If you’re managing an acquisition, VJM Global can support you in applying ASC 805 valuations correctly, ensuring your reports meet both U.S. and international expectations.

Key Takeaways:

ASC 805 governs business combinations and ensures that mergers and acquisitions are reported accurately under U.S. GAAP.

The acquisition method is mandatory, requiring identification of the acquirer, fair value measurement of assets and liabilities, and recognition of goodwill.

Purchase Price Allocation (PPA) is critical for assigning fair value to acquired assets and liabilities, with ASC 820 guiding valuation techniques.

Transparency builds investor confidence, and engaging third-party valuation experts helps ensure compliance, accuracy, and audit readiness.

Early preparation is key, aligning with valuation specialists before closing a deal can help avoid costly mistakes.

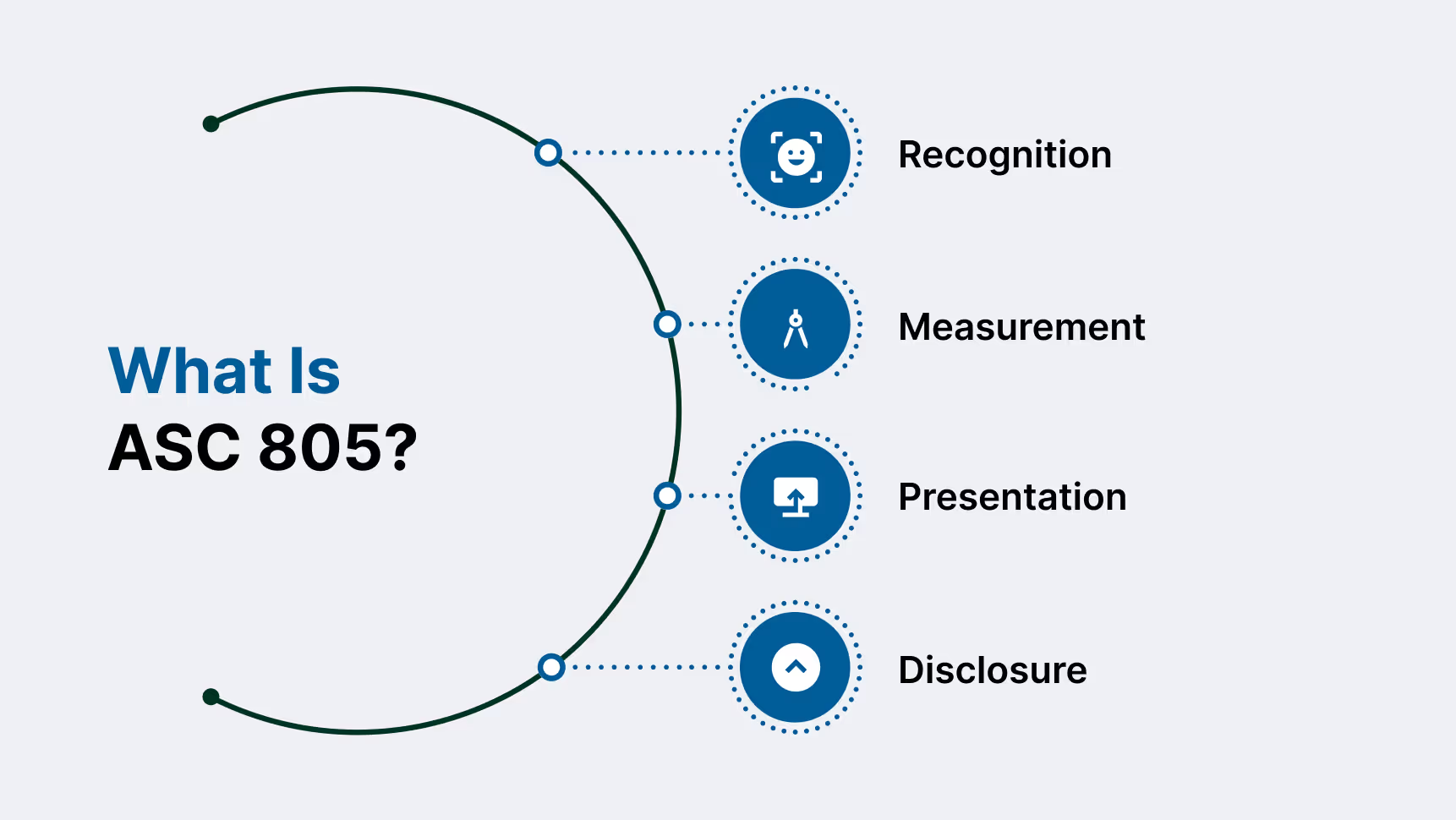

What Is ASC 805? (Definition and Purpose)

ASC 805 is the U.S. GAAP framework for accounting for business combinations. In simple terms, it establishes how companies recognize, measure, and disclose the assets, liabilities, and goodwill arising from mergers and acquisitions.

By standardizing M&A accounting, ASC 805 ensures that stakeholders see a clear, consistent, and transparent picture of how acquisitions affect a company’s financial position. It covers the following:

Recognition: Identifying whether a transaction qualifies as a business combination and which entity is the acquirer.

Measurement: Determining the fair value of acquired assets, assumed liabilities, and any resulting goodwill.

Presentation: Showing the impact of the acquisition on consolidated financial statements.

Disclosure: Providing investors and regulators with details about the transaction, valuation methods, and assumptions used.

ASC 805 gives businesses a structured approach to handling the complexities of acquisitions, making valuations more reliable and financial reporting more credible.

Outsource your bookkeeping and save time without compromising accuracy. Let us handle the books.

Once you understand what ASC 805 is, the next step is recognizing why it plays such a crucial role in financial reporting, especially in today’s deal-driven environment.

Why ASC 805 Matters for Your Financial Reporting

Accurate valuation in business combinations is more than just a technical requirement; it is a cornerstone of financial transparency and credibility.

Here’s why ASC 805 is important:

Investor Confidence: Proper valuation ensures stakeholders can trust that assets, liabilities, and goodwill are presented at fair value.

Audit Readiness: Clear purchase price allocations (PPA) reduce disputes with auditors and avoid costly restatements.

Regulatory Compliance: ASC 805 aligns reporting with U.S. GAAP standards, lowering the risk of SEC scrutiny or penalties.

Strategic Insights: Accurate valuation helps management evaluate the long-term impact of acquisitions, from asset performance to goodwill impairment.

Who Does ASC 805 Apply To?

Understanding which entities must comply with ASC 805 Valuations for Business Combinations is essential for accurate financial reporting in mergers and acquisitions:

Public companies reporting under U.S. GAAP must follow ASC 805 for all mergers and acquisitions. This ensures consistent treatment of fair value, goodwill, and disclosure requirements.

Private companies preparing GAAP-compliant financial statements are also subject to ASC 805, though certain disclosure requirements may be simplified compared to public entities.

Multinational corporations and foreign subsidiaries that report under U.S. GAAP (e.g., overseas entities of U.S.-listed firms) must apply ASC 805 when acquiring or merging with other entities.

Special-purpose acquisition companies (SPACs) and entities involved in reverse mergers are also directly impacted, as ASC 805 provides guidance on identifying the acquirer and applying the purchase method.

Entities outside GAAP reporting (e.g., small partnerships or firms using cash accounting) may not be required to adopt ASC 805 unless they transition to GAAP standards.

Pro Tip: Even smaller private companies should understand ASC 805 basics. During M&A, compliance is not optional, and missteps in purchase price allocation or goodwill valuation can lead to costly restatements and investor concerns.

It’s essential to understand the core components that make up ASC 805 valuations. These elements set the foundation for accurate and transparent financial reporting in business combinations.

Core Components of ASC 805 Valuations for Business Combinations

To apply ASC 805 effectively, businesses need to understand its core components. Each plays a vital role in ensuring that mergers and acquisitions are accounted for accurately and consistently under U.S. GAAP.

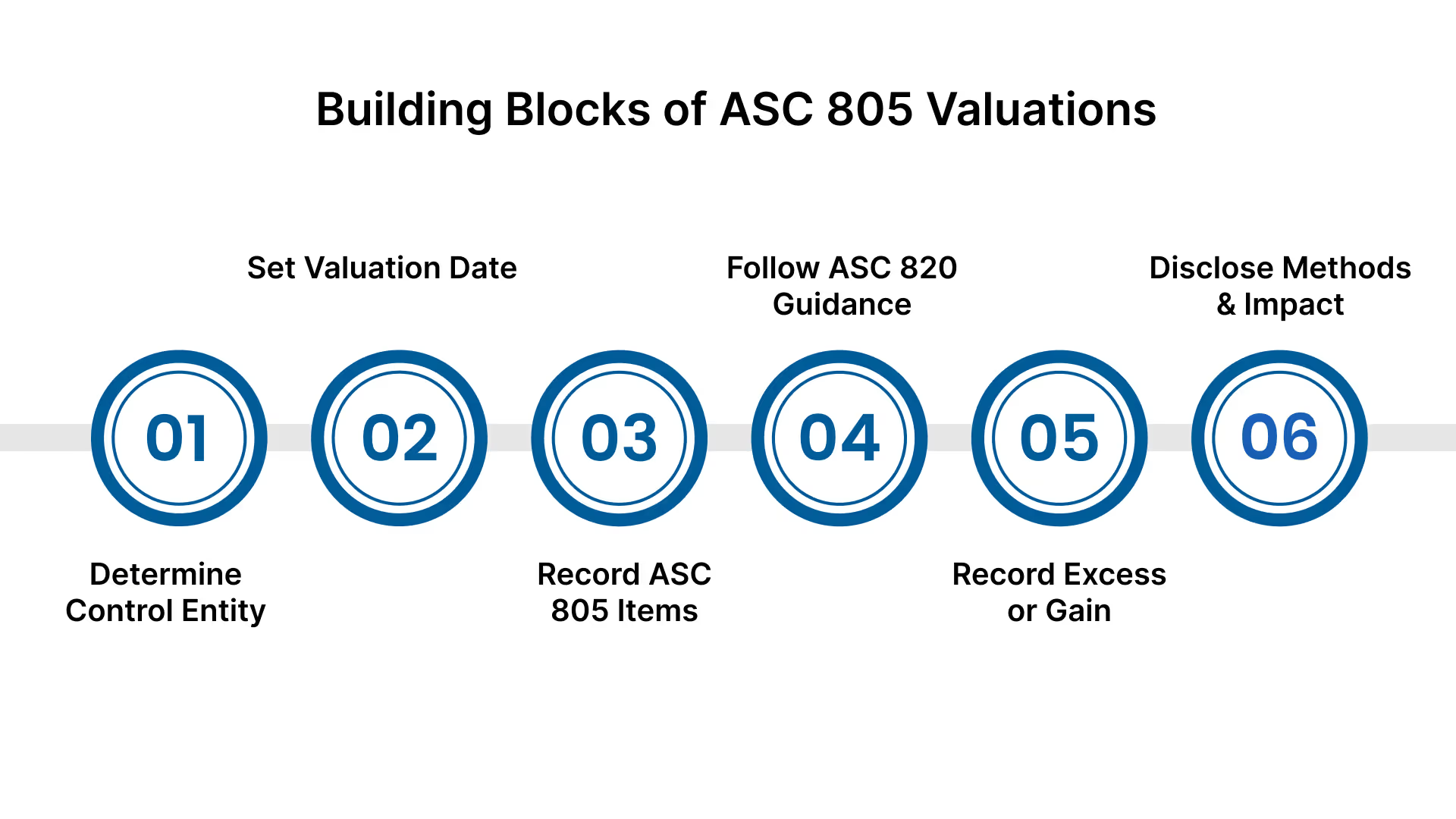

Identification of the Acquirer: The first step is determining which entity is the acquirer, as this dictates how the transaction is recorded. The acquirer is usually the entity that gains control of the other business.

Acquisition Date: Establishing the exact date of acquisition is critical because it defines when the assets, liabilities, and goodwill are measured and recorded at fair value.

Recognition of Assets and Liabilities: All identifiable assets acquired and liabilities assumed must be recognized at the acquisition date, provided they meet ASC 805’s recognition criteria.

Fair Value Measurement: Assets and liabilities are measured at their fair value as of the acquisition date. This ensures consistency and aligns with the broader fair value guidance in ASC 820.

Goodwill and Bargain Purchase: Any excess of the purchase price over the fair value of net assets is recognized as goodwill, while a bargain purchase (where the fair value exceeds purchase price) is recorded as a gain.

Disclosure Requirements: Transparency is a key principle. Companies must disclose details of the transaction, including valuation methods, assumptions, and the impact on financial statements.

Together, these components form the backbone of ASC 805 valuations, ensuring that business combinations reflect economic reality and provide clarity to investors and regulators alike.

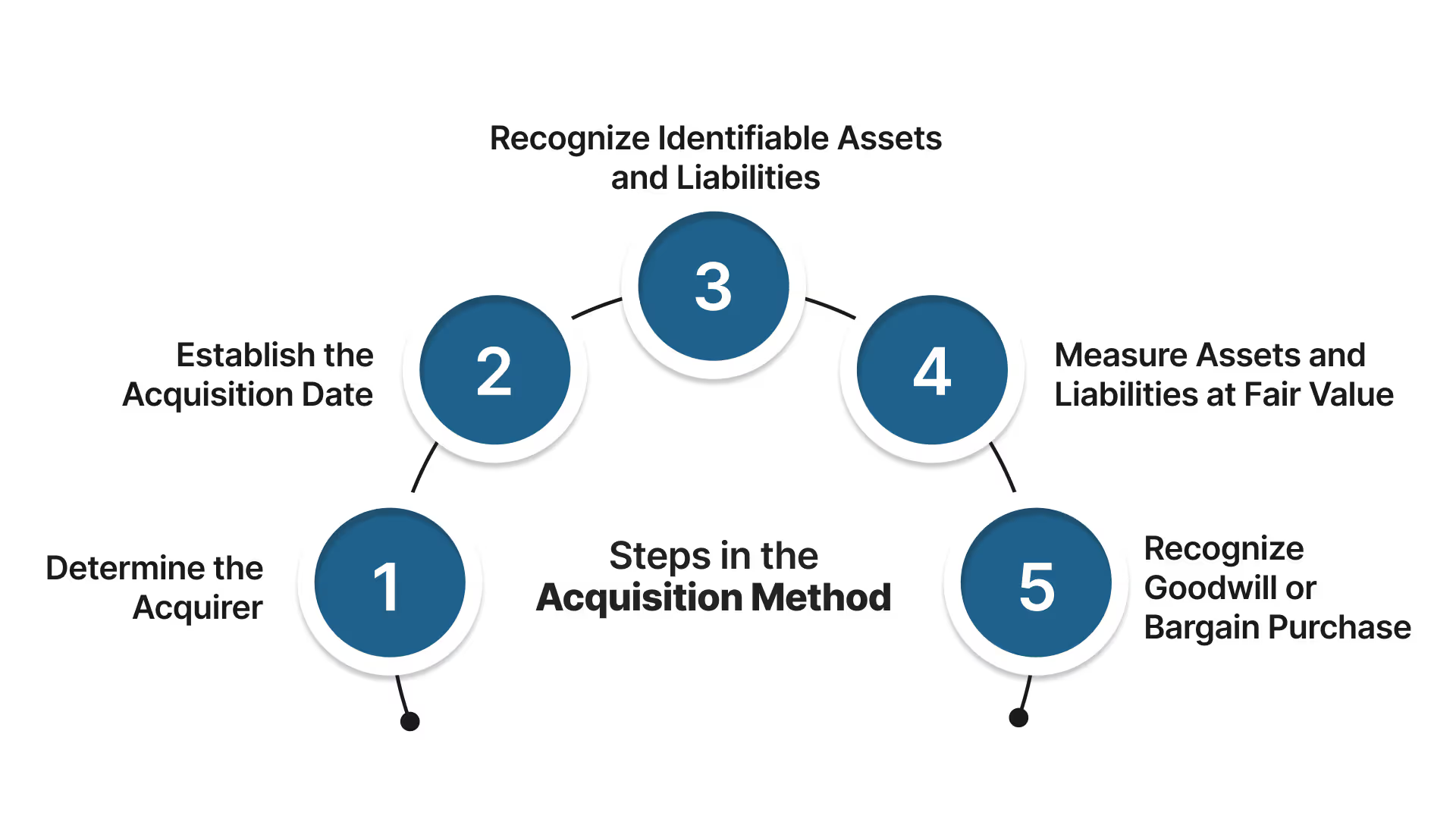

ASC 805 outlines a structured process for applying the acquisition method to business combinations. Each step ensures that the transaction is recorded fairly and consistently, reflecting the true economic impact of the deal.

Step 1: Determine the Acquirer: The process begins by identifying which entity obtains control over the other. This is critical because only the acquirer recognizes the assets and liabilities of the target company.

Step 2: Establish the Acquisition Date: The acquisition date is the point when control is transferred. All assets, liabilities, and goodwill are measured as of this specific date, making it a key milestone for valuation.

Step 3: Recognize Identifiable Assets and Liabilities: The acquirer must recognize all assets acquired and liabilities assumed, provided they meet the recognition criteria outlined in ASC 805.

Step 4: Measure Assets and Liabilities at Fair Value: Every recognized item is measured at fair value on the acquisition date. This ensures consistency with ASC 820 and provides an accurate picture of the transaction.

Step 5: Recognize Goodwill or Bargain Purchase: If the purchase price exceeds the fair value of net assets, the difference is recorded as goodwill. Conversely, if the net assets exceed the purchase price, the acquirer records a bargain purchase gain.

From bookkeeping to audit prep, we handle it all. Discover how outsourcing can work for you.

By following these steps, businesses ensure their acquisitions are accounted for in line with GAAP, building trust with investors and regulators while maintaining transparency in financial reporting.

Once the acquisition method steps are clear, the next critical phase is allocating the purchase price. This process, known as Purchase Price Allocation (PPA), ensures that all assets and liabilities are properly valued and reflected in the financial statements.

Purchase Price Allocation (PPA)

Purchase Price Allocation (PPA) is one of the most critical steps in applying ASC 805. It ensures that the cost of acquiring a business is distributed appropriately among the acquired assets and liabilities, providing transparency and accuracy in financial reporting.

What It Is: PPA is the process of assigning the purchase price paid in an acquisition to the target company’s identifiable assets and liabilities, based on their fair values.

How It Works: After determining the acquisition date, the acquirer evaluates all tangible and intangible assets, as well as liabilities, and assigns fair value to each. The process also involves referencing ASC 820 for fair value measurement standards to ensure consistency.

Why It Matters: Accurate PPA allows companies to present a true financial picture post-acquisition. It prevents overstatement or understatement of asset values, ensures goodwill is calculated correctly, and provides transparency for investors and regulators.

Key Benefits

Enhances financial statement credibility by reflecting true asset values.

Provides clarity for auditors and regulators during reviews.

Strengthens investor trust through transparent reporting.

Helps management make better decisions about post-acquisition integration and asset utilization.

Ultimately, PPA bridges the gap between the acquisition price and the fair value of the acquired business, making it a cornerstone of ASC 805 compliance.

Beyond valuing assets and goodwill, ASC 805 also emphasizes the importance of transparency and expert involvement to build investor trust and ensure compliance.

Why Transparency and Expert Support Matter in ASC 805 Valuations

For investors, transparency shows exactly what a company is worth. For businesses, having the right experts involved ensures that valuations are fair, consistent, and audit-ready.

Accurate Asset Value: Investors gain a clear picture of what the business truly owns and owes.

Fair Market Clarity: Helps avoid confusion by showing the real value of assets at the time of acquisition.

Third-Party Expertise: Independent valuation experts bring objectivity, reduce errors, and align reports with U.S. GAAP requirements.

Early Preparation: Engaging advisors before finalizing deals ensures smoother processes, fewer surprises, and better decision-making.

How VJM Global Helps Businesses with ASC 805 Valuations

Managing ASC 805 valuations for business combinations can be complex, but VJM Global makes the process smooth, accurate, and fully compliant. We help U.S. businesses and global companies handle every aspect of ASC 805 reporting with expert precision.

Here’s how we support you:

Acquisition Method Guidance: Step-by-step assistance in applying the acquisition method, from identifying the acquirer to recognizing goodwill or bargain purchases.

Fair Value Measurement: Expert support in valuing tangible and intangible assets according to ASC 805 and ASC 820 standards.

Purchase Price Allocation (PPA): Transparent allocation of purchase consideration across acquired assets and liabilities to ensure accurate reporting.

Goodwill Analysis: Assistance in calculating, recording, and testing goodwill for impairment, keeping your financials audit-ready.

Regulatory Compliance: Ensuring your M&A transactions align with U.S. GAAP and global reporting standards for smooth audits and investor confidence.

Third-Party Valuation Support: Collaboration with valuation professionals to provide independent, credible reports that satisfy auditors and regulators.

By managing the technical requirements of ASC 805 valuations, VJM Global helps you avoid costly errors, maintain transparency, and present reliable financials to stakeholders. Schedule a consultation with us today to ensure your business combinations are handled with accuracy and confidence.

Frequently Asked Questions (FAQs)

1. What is ASC 805 and why is it important?

ASC 805 is the U.S. GAAP standard for accounting for business combinations, including mergers and acquisitions. It ensures that all acquired assets and liabilities are recorded at fair value, providing transparency and consistency in financial reporting.

2. What does Purchase Price Allocation (PPA) mean under ASC 805?

PPA is the process of assigning the total purchase price of an acquisition to the acquired company’s assets and liabilities based on their fair values. Any remaining amount after this allocation is recorded as goodwill.

3. How is goodwill treated in ASC 805 valuations?

Goodwill represents the excess purchase price paid over the fair value of net assets acquired. Under ASC 805, it must be tested periodically for impairment rather than amortized, ensuring it reflects true business value over time.

4. What role do third-party valuation experts play in ASC 805 compliance?

Independent valuation experts provide objective and credible fair value assessments of acquired assets. Their reports help companies reduce compliance risks, streamline audits, and strengthen investor trust.

5. How does ASC 805 differ from ASC 820?

ASC 805 focuses on business combinations, while ASC 820 provides the framework for fair value measurement. Essentially, ASC 820 guides how fair value should be determined, and ASC 805 explains when and where it applies in acquisitions.

VJM Global

Explore expert insights, tips, and updates from VJM Global

%20(1).avif)