IRS audits are standard, but the cost can escalate quickly if your documentation isn’t in order. In 2023 alone, the IRS assessed $7 billion in estimated tax penalties, nearly four times the amount from the previous year. Much of that stemmed from businesses failing to track, file, or support what they reported.

When your return is reviewed, you are responsible for proving its accuracy. This means supplying the right documents, meeting deadlines, and knowing how to manage the audit without widening its scope.

This guide breaks down how IRS audits work, why they happen, and what steps business owners should take before, during, and after an audit to avoid penalties and stay in control.

An IRS audit is a formal review of your tax return, financial statements, and documentation to verify that income, deductions, and credits were reported correctly. While often triggered by discrepancies or patterns in your return, audits may be selected randomly or due to third-party links.

The IRS uses automated systems and peer benchmarks to screen business returns. Triggers often involve outliers, inconsistencies, or aggressive claims that deviate from your size bracket or industry category norms.

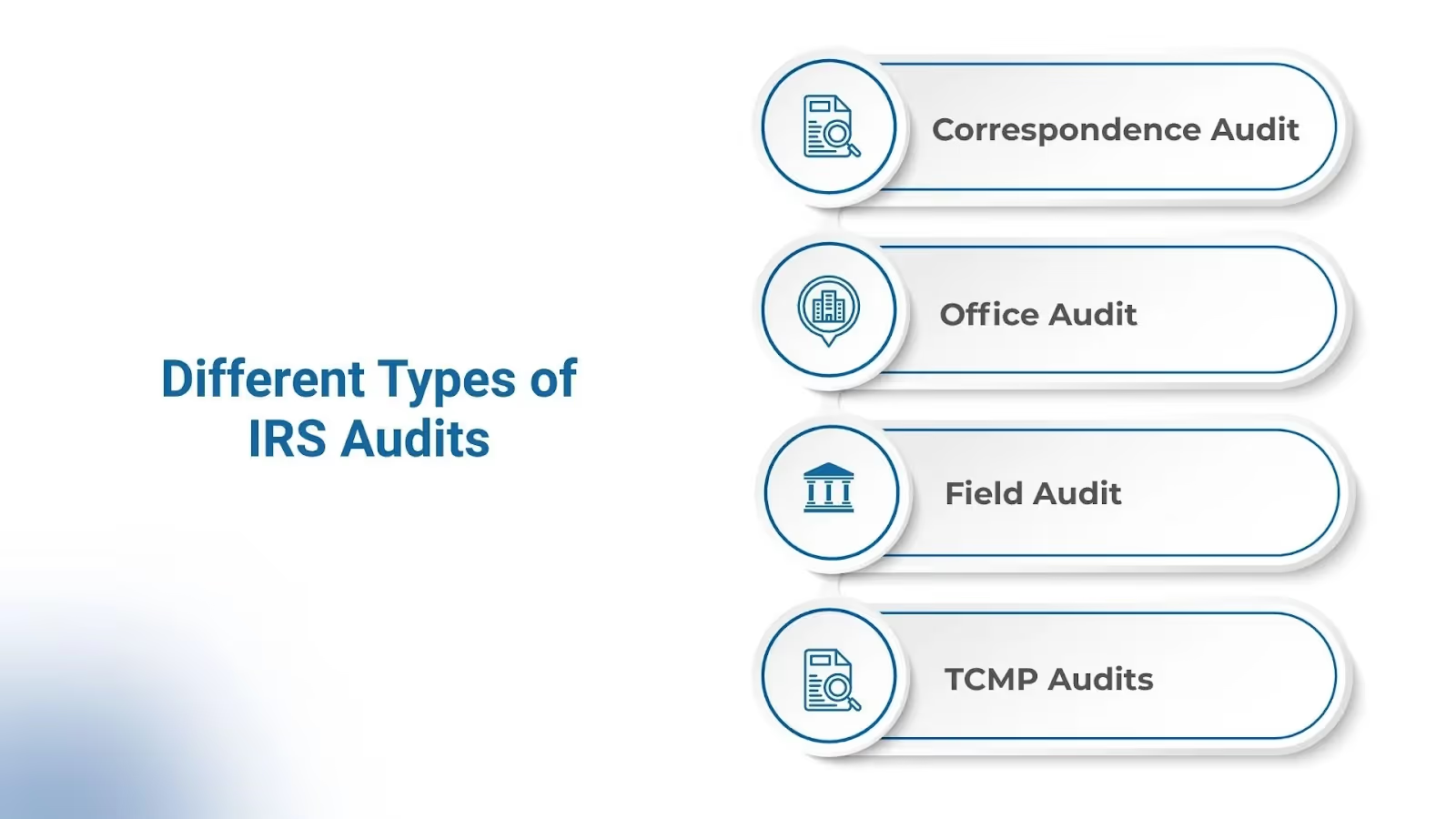

The IRS conducts audits in four main formats. Each one differs in scope and how records are reviewed.

Conducted by mail. The IRS requests documentation for specific line items, such as a deduction or credit. Most are resolved through written responses without meetings.

Held at an IRS office. These reviews cover broader topics, like income, expenses, or employee classification. You’ll be asked to bring organized records for review.

Takes place at your business location or your CPA’s office. IRS agents examine records on-site and may ask operational questions. These are typically used for higher-revenue or complex businesses.

The Taxpayer Compliance Measurement Program (TCMP) is a research-driven audit. If selected, every line of your return must be substantiated. These are rare and not based on red flags.

IRS audits always begin with a mailed notice. Businesses will never be called or emailed without prior written correspondence.

Here’s how the process starts:

Always verify the legitimacy of audit notices and respond promptly to avoid default adjustments.

If you receive an audit notice, don’t panic. Treat it as a process that can be managed with preparation and coordination.

Start by educating your internal team. Anyone involved in finance, payroll, or handling auditor questions should understand what the IRS is reviewing, what documents are in play, and how to communicate accurately.

Once the team is aligned, focus on gathering and reconciling your records. Being audit-ready minimizes disruption and puts you in control of the process.

Preparation steps include:

Tip: These Audit Technique Guides are created for IRS examiners, but they are public and handy for businesses and tax professionals. They outline common audit questions, documentation expectations, and accounting methods, making them a valuable preview of what auditors seek.

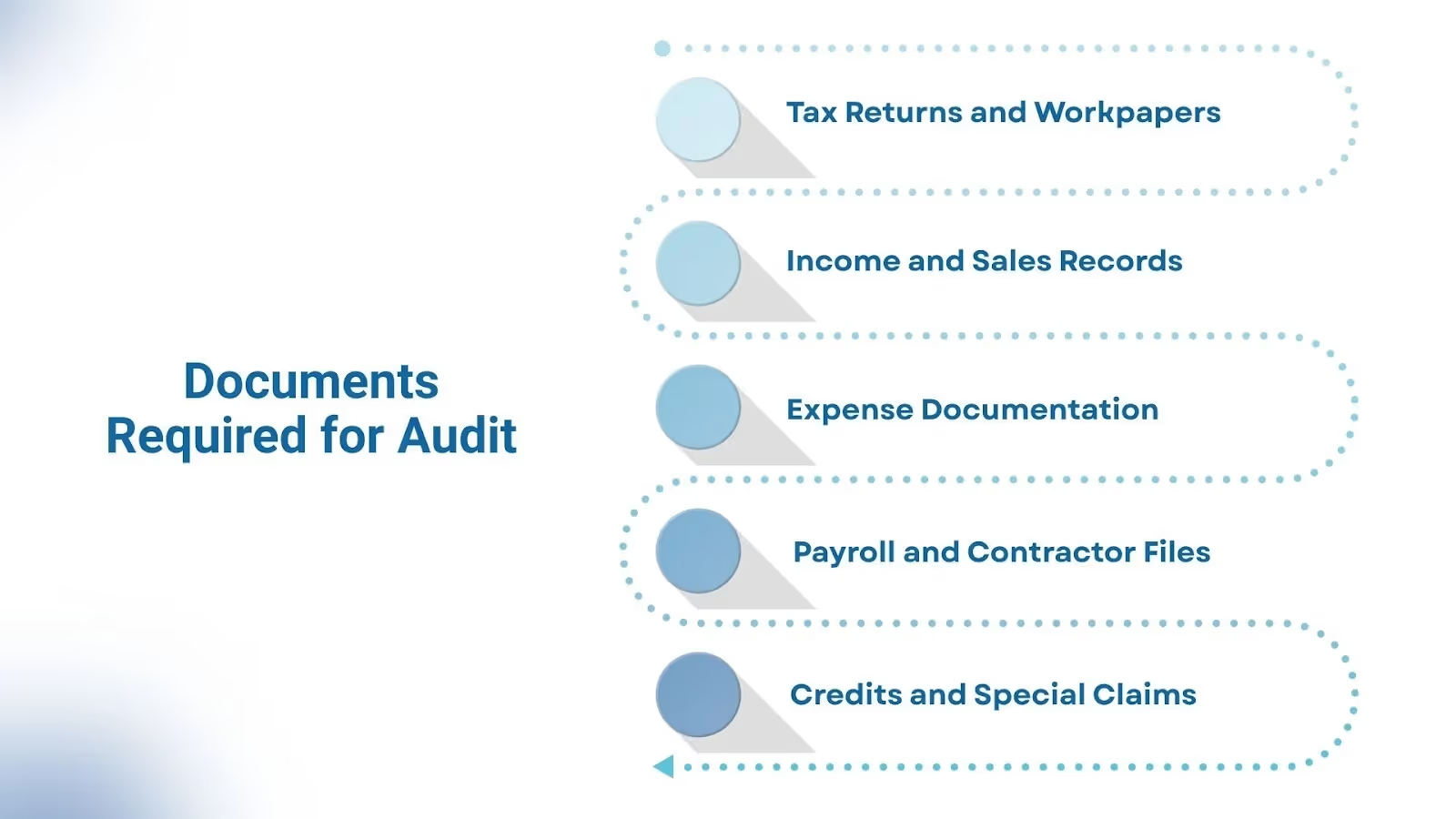

While the IRS generally only audits recent tax returns, they may ask for records dating back to a maximum of six years. As such, any documentation must be filed and preserved correctly for ease of access.

Prioritize these categories:

After you respond to the initial notice, the IRS will issue an Information Document Request (IDR) outlining what records they want to see. This defines the audit scope.

The process unfolds in clear stages:

For office or field audits, the IRS may schedule a conference to confirm timing and locations and clarify expectations. At this point, you can also raise initial questions or concerns.

You’ll have a fixed window, typically 30 days, to organize and submit records listed in the IDR.

Depending on the audit type, this could be by mail (correspondence), at an IRS office (office audit), or your business (field audit). Expect operational questions during field visits.

The IRS will review the documentation and create a Revenue Agent’s Report (RAR). Depending on the complexity of the issues, this may take several months to two years.

You’ll be asked to accept or contest the findings. Acceptance leads to payment or refund instructions. If you disagree, you can file a formal appeal.

In more detailed audits, a closing meeting may be offered to discuss the report and present final clarifications or corrections before resolution.

The audit concludes once adjustments are accepted and settled, or after appeals are exhausted.

Once the audit review is complete, the IRS will issue a formal Revenue Agent's Report (RAR), typically on Form 4549. This report outlines any proposed changes to your return and gives you a chance to respond.

IRS outcomes fall into three categories:

All documentation checks out. The IRS accepts your return as filed and closes the audit with no action required.

The IRS proposes adjustments and you agree. You’ll sign the RAR and receive instructions for paying additional tax or claiming a refund. You may also owe penalties or interest, depending on the issue.

If you disagree with the findings, you can submit a written protest and request a hearing with the IRS Office of Appeals. This must usually be done within 30 days of receiving the report. If no resolution is reached, you can take the matter to the U.S. Tax Court.

Regardless of the outcome, take the time to identify what triggered the audit and update internal processes to prevent repeat issues. This could include revising documentation procedures, bookkeeping systems, or how deductions and credits are substantiated.

The audit may be over, but your work isn't. Post-audit action ensures lasting compliance and protects your business in the future. This is also your chance to fix internal weaknesses, whether it’s recordkeeping, expense tracking, or how you prepare filings, before they cause issues again.

The best defense against audits is consistency. Long-term audit readiness means setting up repeatable habits that reduce your risk and make future audits easier to handle.

In some cases, bringing in a tax professional early can save time, prevent missteps, and protect your business’s position.

Consider hiring a tax pro if:

Note: CPAs, enrolled agents, and tax attorneys can represent you before the IRS, including during appeals. If penalties or legal exposure are on the line, consider working with someone experienced in audit defense.

An IRS audit can be intensive, but it doesn’t have to derail your business or drain your resources if you're prepared. Most audits can be resolved efficiently with accurate records, calm preparation, and the right support. Businesses that prioritize tax hygiene year-round are less likely to be flagged and better equipped to respond when they are.

If your team needs experienced offshore audit support to manage documentation and compliance reviews during peak periods, VJM Global can help. Our team supports audit prep, documentation, and compliance reviews while ensuring alignment with U.S. accounting standards.

Need flexible capacity without compromising accuracy or security? Reach out to VJM Global for scalable audit support tailored to your firm’s needs.