.avif)

Payroll mistakes drain time, trust, and cash. In fiscal year 2024, the U.S. Department of Labor recovered more than $202 million in back wages for nearly 152,000 workers, much of it tied to pay and overtime errors that started as preventable payroll issues. Missed deposit dates also add up quickly, since the IRS applies Failure-to-Deposit penalties that scale with how late a payroll tax payment is.

In this blog, we’ll break down how to fix payroll mistakes, the most common pitfalls that cause them, and the simple controls that keep your next pay run clean in both the U.S. and India.

.avif)

Payroll mistakes may look small, but they create a ripple effect across finance, compliance, and employee trust. Many of these errors come down to human oversight or weak internal controls rather than complex regulations. Understanding what goes wrong is the first step to building a process that stays accurate every month.

1) Misclassifying workers: Treating an employee like an independent contractor leads to wrong tax withholding, benefits, and filings. The IRS stresses that classification depends on the totality of facts and offers Form SS-8 when status is unclear. Getting this wrong can cascade into back taxes and penalties. In the U.S., this affects tax withholdings and benefits under the IRS guidelines, while in India it can trigger issues with PF, ESI, or gratuity compliance.

2) Overtime and hours mistakes: Missing overtime for non-exempt staff, or using the wrong “regular rate,” is a common pain point. Under the FLSA, covered non-exempt employees must receive at least 1.5× the regular rate for hours over 40 in a workweek; state rules may be stricter. Weak timekeeping or manual adjustments often sit at the root of these errors.

3) Late or wrong U.S. payroll tax deposits: Depositor status matters. Monthly depositors must deposit by the 15th of the following month. Semi-weekly depositors follow a Wednesday/Friday schedule, and the $100,000 next-day rule can also apply. Late or wrong deposits trigger penalties and interest.

4) Not correcting U.S. employment tax errors correctly: When mistakes happen, you generally fix Form 941 errors with Form 941-X. There are timing limits for correcting federal income tax withholding, and you must refund or reimburse employees before reducing overcollected tax. Using the right “X” form keeps your correction audit-ready.

5) India payroll compliance slips: TDS, EPF, ESI: On the India side, payroll must reflect TDS under section 192 for salary and be reported in the correct schedules. Employers must deposit EPF contributions and file ECR on or before the 15th of the following month. ESI contributions are also due within 15 days after the close of the wage month. Missing these timelines invites interest and damages credibility with authorities.

6) Poor master data and record hygiene: Wrong PAN or bank details, missing joiner/leaver updates, or unposted pay changes cause repeated errors across cycles. These show up later as reconciliation gaps with ledgers, bank files, EPF/ESI returns, or U.S. payroll tax reports.

7) Skipping monthly reconciliations: When payroll, bank disbursements, and the general ledger are not reconciled every cycle, small mismatches compound. The result is off-cycle adjustments, amended returns, and strained audits.

8) Fragmented processes in cross-border setups: If your workforce or processing spans the U.S. and India, even small differences in overtime rules, deposit calendars, or inventory of statutory returns can produce inconsistencies. Aligning calendars, definitions, and checklists across teams prevents rework and missed filings.

Suggested read: Outsource Tax Preparation from the US to India: A CPA’s 2025 Guide

Now that we’ve looked at what typically goes wrong, let’s move to the next step, understanding how to fix payroll mistakes effectively and prevent them from reoccurring.

Mistakes happen. What matters is catching them fast, correcting them the right way, and closing the root cause so they don’t recur. Use this simple, compliant workflow.

Here are steps to help you correct errors now and build safeguards for the future:

Compare the payroll register, time records, and bank file. Identify who is affected, which pay period is wrong, and whether taxes or social contributions are also off. If overtime is the issue, recheck eligibility and the correct “regular rate” under the Fair Labor Standards Act. Covered, non-exempt employees must receive at least 1.5× their regular rate for hours over 40 in a workweek.

Tell impacted employees what went wrong and when the fix will hit their pay. If you short-paid, process an off-cycle adjustment. If you overpaid, agree on a recovery plan in writing. Where back wages are due under U.S. law, the Department of Labor notes that supervised back-pay resolutions help settle claims and limit later disputes.

Fix the underlying data (rates, hours, tax codes). Rerun net pay and update the payroll register, payslips, and year-to-date balances. Keep an internal memo: what changed, who approved, and which ledgers were touched.

If a previously filed Form 941 is wrong, use Form 941-X to correct federal employment taxes. The IRS provides current instructions and allows e-filing for amended employment returns. When W-2 wage/tax amounts are wrong, file Form W-2c/W-3c with the Social Security Administration and give employees their corrected copy (BSO e-filing is available and required at volume).

For salary TDS, submit a TDS correction statement for Form 24Q via TRACES (online correction or by preparing a correction return) and deposit any shortfall with applicable interest. The Income Tax Department sets out the official correction routes and publishes due-date calendars for deposits.

For EPF, file or revise the ECR and pay dues through the Unified Portal. EPFO guidance states monthly contributions are due on or before the 15th of the following month. For ESIC, contributions are due within 15 days of the last day of the month in which wages fall due; correct and repay any shortfall promptly.

Match corrected payroll to bank payments, GL postings, and statutory returns. Confirm that amended returns were accepted, deposits cleared, and year-to-date totals now tie out.

Add a pre-pay checklist (new hires, rate changes, tax codes), require dual review for payroll changes, and schedule a monthly reconciliation. Where errors involved overtime or status, retrain on FLSA classification rules and your local requirements.

Save reports that show the error, the correction run, revised returns, and employee notices. This file will support internal reviews and external audits later.

At VJM Global, we guide companies through each of these steps, from error detection and employee communication to correction, reconciliation, and preventive controls, across both Indian and U.S. payroll environments.

Also read: Outsourced Tax Services to India: A Guide for US Companies

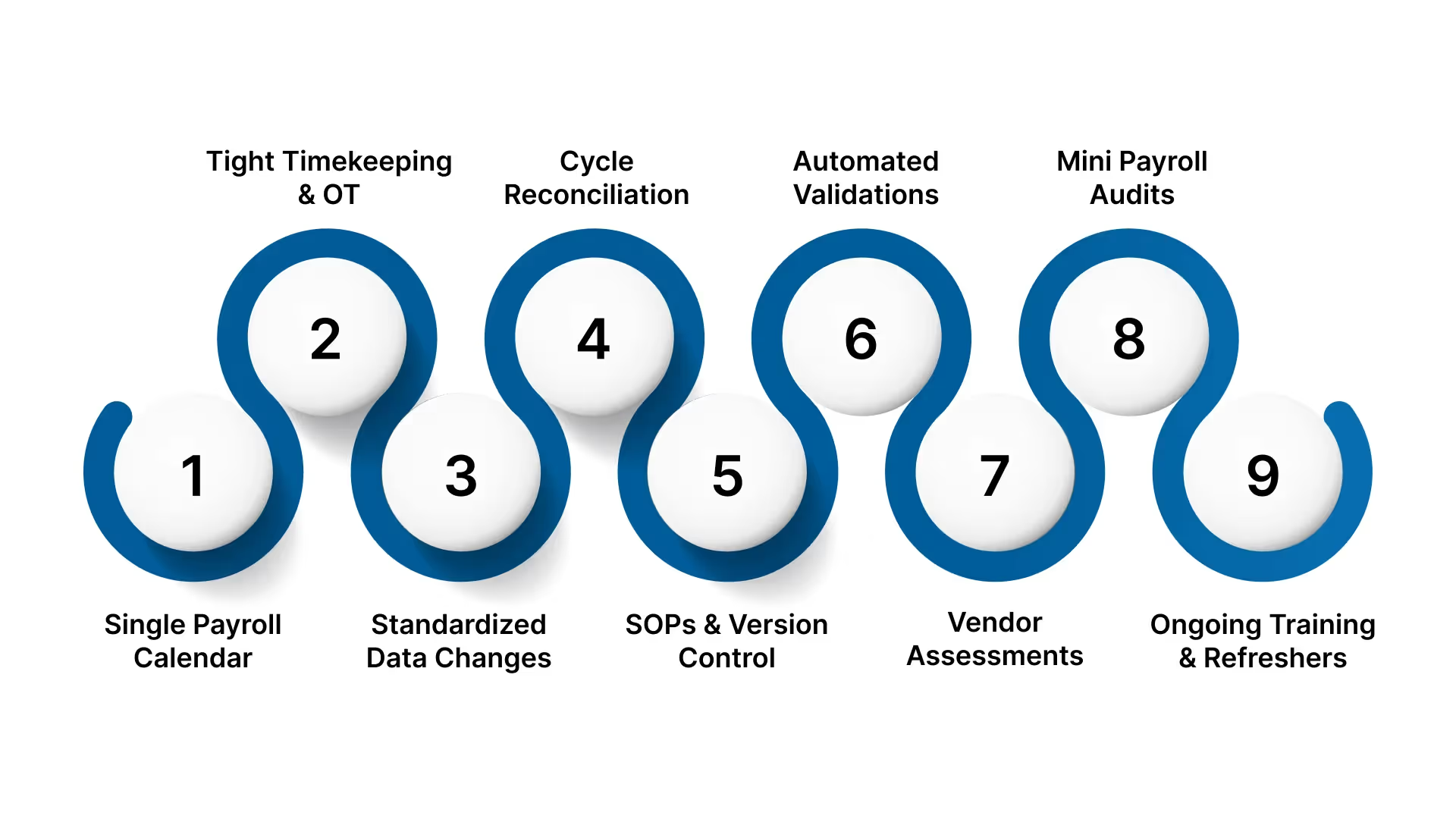

Fixing payroll mistakes restores order, but true efficiency comes from building preventive systems that stop these errors from returning. Let’s look at the best practices that can help you avoid future payroll errors altogether.

Prevention comes from clean data, clear calendars, and controls that run every pay cycle. Here’s a practical playbook that finance and HR teams can follow.

With the right mix of oversight, automation, and external expertise, payroll accuracy becomes less about catching mistakes and more about creating consistency. This mindset leads to long-term stability and compliance confidence.

Great payroll is predictable. When your data is clean, your calendars are clear, and your checks run every cycle, pay is correct, filings land on time, and audits are straightforward. If an error slips through, a documented fix-and-prevent playbook helps you correct it fast, communicate clearly with employees, and close the root cause so it doesn’t return.

At VJM Global, we help businesses simplify payroll across borders. Our specialists handle setup, monthly processing, reconciliations, and statutory compliance for U.S. and Indian entities, ensuring that every cycle runs on time and without errors. Whether you need help correcting past mistakes or building a future-ready payroll system, VJM Global is your trusted partner in accuracy and compliance.

Contact us today to see how we can help you fix payroll mistakes and build a process you can count on.

Start with a review of your last few payroll runs, look for patterns of errors (for example, same job code, same department) and clean your master data. Then implement a checklist to prevent repeat issues.

Yes. Even errors in classification, tax deposits or record-keeping can attract fines, interest and legal claims, especially if they remain unchecked over multiple periods.

A quarterly internal review is ideal for most companies. For organisations with global payroll or hundreds of employees, monthly checks during heavy periods could be beneficial.

Modern payroll platforms combined with integrated time-keeping and error-check logic can reduce error rates significantly, some studies suggest up to a two-thirds reduction.

Yes. Even if payroll remains in-house, outsourced or offshore support from a team familiar with cross-border compliance and documentation adds redundancy, strengthens the control environment and allows your core team to focus on strategy rather than corrections.