Managing year end accounts is a critical process for businesses of all sizes. Proper preparation ensures accurate financial reporting, regulatory compliance, and a clear understanding of your company’s financial health.

According to a 2023 SAPinsider report, 20% of top-performing companies have reduced their financial close duration to an average of just 3 days, down from 4 days in 2022.

This guide provides a complete checklist to help you navigate the essential steps involved in closing your year end accounts efficiently and correctly.

Year-end closing for accounting is the process of finalizing a company’s financial records at the close of the fiscal year. This includes reconciling accounts, resolving discrepancies, making necessary adjustments, and preparing the financial statements for the year.

The goal is to ensure accurate financial reporting to stakeholders such as investors, regulators, and tax authorities.

This process involves a thorough review of all financial transactions and ledgers from the past fiscal year to create a complete and accurate financial record.

Year-end closing can be complex and time-consuming, often requiring collaboration among finance, operations, accounting, and IT teams within the organization.

Also Read: Outsourced Accounting as a Service Benefits

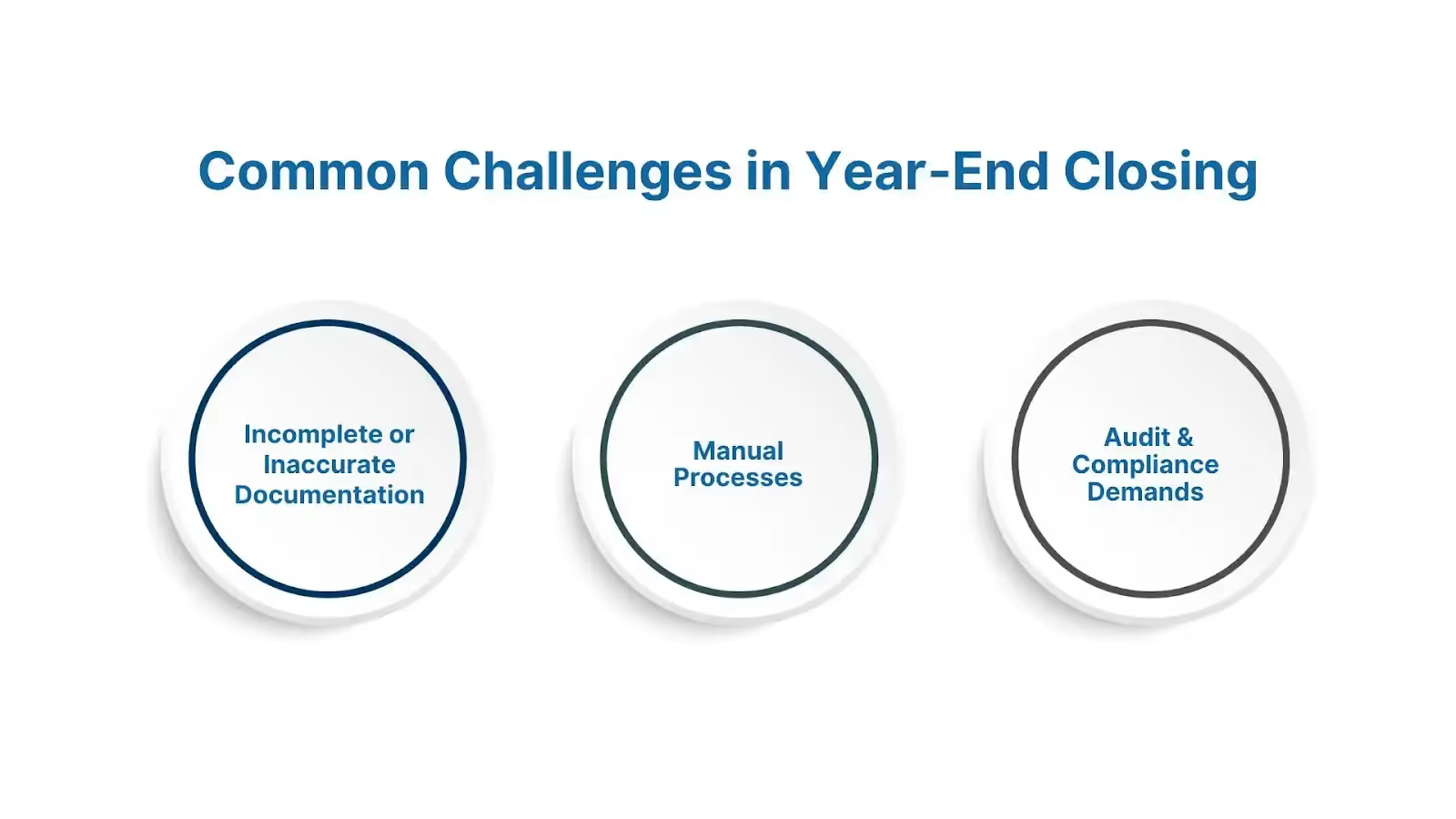

While the year-end closing process is essential, it can also present several challenges that many businesses face.

Year-end closing can be tough, especially when you’re managing financial transactions across multiple entities or dealing with complex transactions.

If you’re a small to mid-sized U.S. company using cloud software, you may still face challenges like inconsistent processes, manual tasks, and strict compliance requirements. Here are some common hurdles you might encounter:

If your financial records aren’t complete or well-organized, it becomes harder to close your year-end accounts smoothly. As your business grows, keeping track of every invoice and receipt can get overwhelming, leading to missing documents that delay your reconciliations and push back your closing deadlines.

Even with cloud software, relying on manual steps in your accounting workflow can slow you down and increase the risk of errors. This makes the year-end closing process longer and more stressful than it needs to be.

If your business undergoes audits, preparing audit-ready records on tight timelines can be a big challenge. Plus, staying compliant with accounting standards adds pressure, which can affect your team’s efficiency and make the closing process more difficult.

Having a clear and organized plan is key to effectively tackling these challenges; this is where a year-end accounting checklist comes in.

Year-end accounting can be overwhelming, especially when there’s a lot to do in a limited amount of time. Having a clear and organized process is essential to close your books faster and with less stress.

Here’s why a year-end accounting checklist is important:

In short, a year-end checklist helps organize the entire financial close process and ensures no task is left unfinished when wrapping up your year-end accounts.

Moving on, let’s break down the essential tasks you need to complete for a smooth and efficient year-end close.

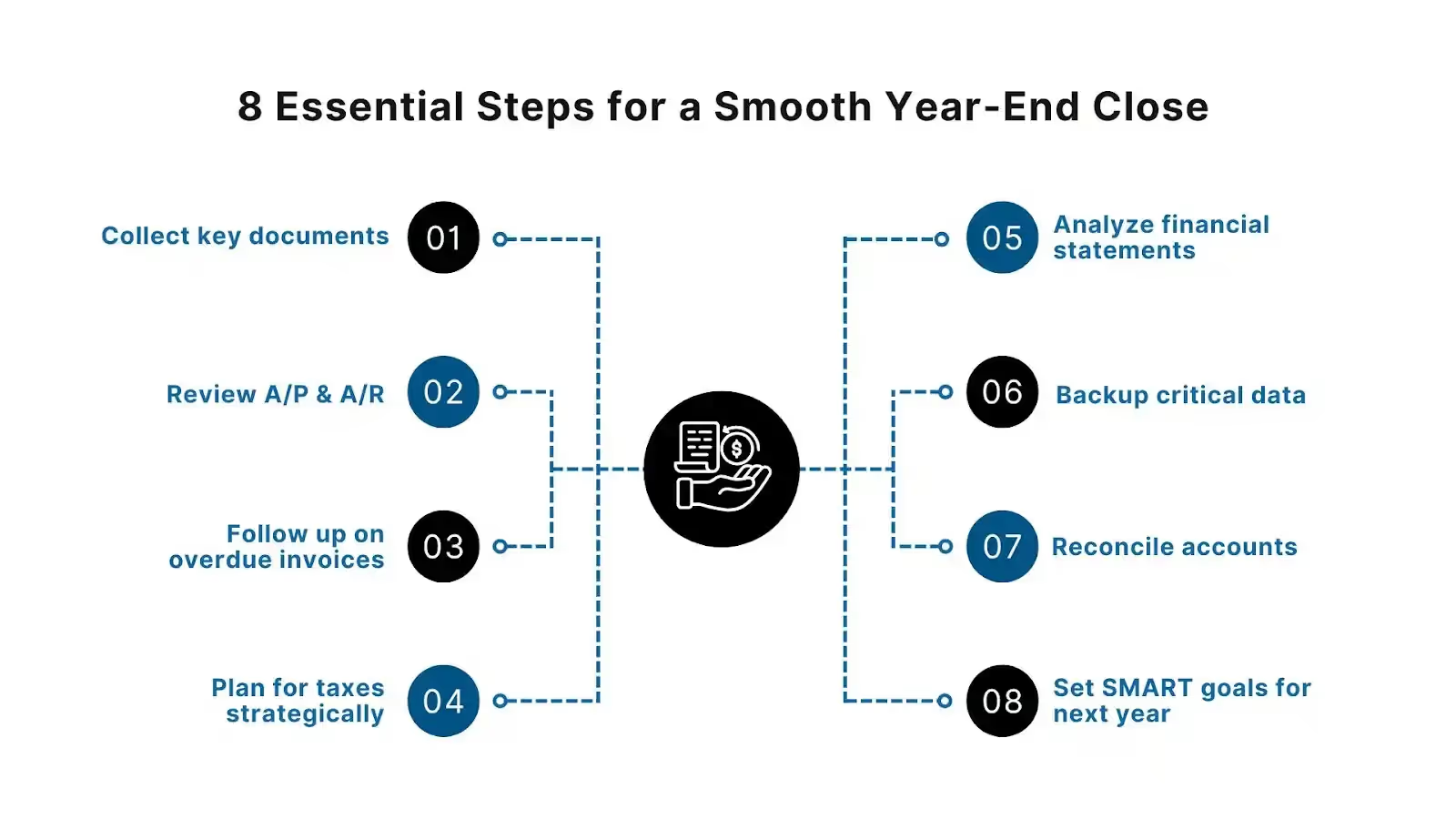

Getting ready for year-end accounting can feel overwhelming, but having a clear plan will make the process manageable and efficient. Here’s a comprehensive checklist to guide you through the essential steps for a smooth year-end close:

Start by collecting all necessary financial documents well before the deadline. This includes:

Having these documents on hand will streamline your review process and avoid last-minute scrambles.

Carefully review outstanding invoices and bills. Confirm that all supplier invoices are recorded and that payments are scheduled or completed.

On the receivables side, identify any unpaid customer invoices and prioritize collections. Use your aging reports to track overdue accounts and initiate follow-ups promptly to avoid cash flow issues.

Collecting overdue payments will maximize your cash inflows. When reaching out to customers, maintain professionalism and empathy.

Set clear payment deadlines and, if necessary, offer flexible payment plans that encourage timely settlement. Document all communications to keep a clear record of your collection efforts.

Tax planning is key to optimizing your business’s financial position. Review your income and expenses to identify tax deductions and credits available.

Collaborate with tax professionals to explore strategies that minimize your tax liability while ensuring compliance with federal and state tax laws.

Prepare comprehensive financial statements, including income statements, balance sheets, and cash flow statements.

Analyze these to assess your business performance over the year. This insight is invaluable for making informed decisions and communicating financial health to stakeholders and investors.

Protect your accounting data by backing up all records in a secure and reliable system. Cloud backups are highly recommended as they safeguard your data from hardware failures, accidental deletions, or cyber threats.

Regular backups ensure that your financial information is accessible and recoverable at any time.

Reconcile your bank and credit card accounts against your accounting records. This helps detect any discrepancies, such as unrecorded transactions or errors. Adjust your books accordingly to maintain accurate and trustworthy financial statements.

Plan ahead by setting clear goals that are Specific, Measurable, Attainable, Relevant, and Time-bound. These goals should focus on improving financial processes, enhancing cash flow, and addressing areas where the business may have struggled during the past year. Breaking goals into quarterly or monthly targets helps maintain focus and momentum.

This checklist can help you organize your year-end accounting process, reduce errors, and close your books on time. Following these steps will set your business up for a successful financial year ahead.

In addition to following the checklist, there are practical strategies you can use to speed up your year-end accounting process.

Year-end closing sets the foundation for your company’s financial accuracy and strategic planning for the year ahead. To avoid unnecessary delays and stress, it’s important to streamline this process. Here are some practical steps you can take to speed up your year-end accounting:

1. Plan Ahead

Don’t wait until the last month to start closing your books. Develop a clear plan well in advance to spread out the workload. This will reduce pressure on your finance team and minimize errors.

2. Perform Regular Account Reconciliations

Reconcile your accounts monthly or quarterly throughout the year. Keeping up with reconciliations regularly will significantly reduce the year-end burden and make closing smoother.

3. Use Accounting Software

Use reliable accounting software to automate routine tasks and manage large volumes of financial data. Automation not only speeds up processes but also lowers the risk of manual errors.

4. Create a Year-End Close Checklist

Document all the steps needed to complete the year-end close. Assign responsibilities clearly and track progress using your checklist. This helps ensure nothing is missed and keeps everyone accountable.

Ready to simplify your year-end accounting and close your books faster? Partner with VJM Global for expert support tailored to your business needs. Contact us today to learn how we can help you streamline your financial close and improve overall efficiency.

Once you’ve wrapped up your current year-end close, it’s equally important to prepare your accounting firm for success in the next fiscal year.

Here’s how you can prepare your accounting firm for a strong start to the next fiscal year. Taking the time now to review, plan, and improve will set you up for smoother operations and better results.

Use the SMART method to create goals that are:

This keeps your team focused and helps turn plans into action.

These steps help maintain steady cash flow and reduce payment delays.

Modern technology saves time and improves your client experience.

Managing your year-end accounts effectively is crucial for maintaining accurate financial records, ensuring compliance, and setting a solid foundation for future growth.

By following a structured checklist, planning ahead, and continuously improving your processes, you can streamline your year-end close and reduce stress for your team.

A smooth year-end closing not only reflects well on your business but also empowers you with the insights needed to make smarter financial decisions in the year ahead.

If you want to simplify your year-end accounting process and boost efficiency, VJM Global is here to help. Our expert team offers tailored solutions designed to meet your unique business needs so you can close your books faster and focus on what really matters: growing your business.