When it comes to strategic taxes, businesses that plan ahead are far more successful in minimizing their tax liabilities and ensuring long-term financial growth. In fact, businesses that implement tax strategies save significant amounts in tax payments, allowing them to reinvest that capital in growth.

In this blog, we will explore how tax planning helps reduce tax burdens, improve cash flow, and foster financial sustainability. From understanding the importance of the right tax structure to maximizing credits and deductions, this blog provides actionable insights that every business owner should know.

Strategic tax planning involves proactively managing your business’s tax obligations to minimize tax liabilities while complying with the law. It goes beyond mere tax filing by focusing on identifying tax-saving opportunities, structuring business activities effectively, and applying deductions, credits, and timing strategies.

Unlike basic tax compliance or standard filing, which ensures you meet tax obligations, strategic tax planning actively seeks to reduce your taxable income through targeted strategies.

Tax planning is crucial for businesses because it directly influences financial growth, scalability, and long-term profitability. By planning strategically, businesses can optimize cash flow, reduce unnecessary tax payments, and allocate resources more efficiently.

While tax planning is legal and necessary for any business to ensure its financial success, tax avoidance is not. Tax planning involves using legal means to reduce tax liabilities by taking advantage of credits, deductions, and exemptions provided by the tax code.

On the other hand, tax avoidance involves manipulating financial activities to evade taxes, often through loopholes or unethical methods, which can lead to penalties and legal consequences.

Now that we understand the basics of strategic tax planning, let’s explore the key components that make up an effective tax strategy.

Must Read: Outsourcing Accounting Services: The Key to Business Growth in 2025

A comprehensive and effective tax strategy is built on understanding your business structure, maximizing deductions, and aligning tax planning with cash flow management. These components work together to help businesses minimize their tax liabilities, improve financial stability, and support long-term growth.

The structure of your business—whether LLC, C-Corp, or S-Corp has significant tax implications.

Maximizing available tax credits and deductions is a critical part of strategic tax planning. Some of the most valuable for startups include:

Aligning tax strategies with cash flow management is essential for minimizing liabilities and ensuring that funds are available when needed. For example, by deferring income recognition to a future tax year, businesses can manage tax payments and maintain liquidity.

Similarly, accelerating deductions or capitalizing on tax credits in the current year can help reduce taxable income and improve cash flow in the short term.

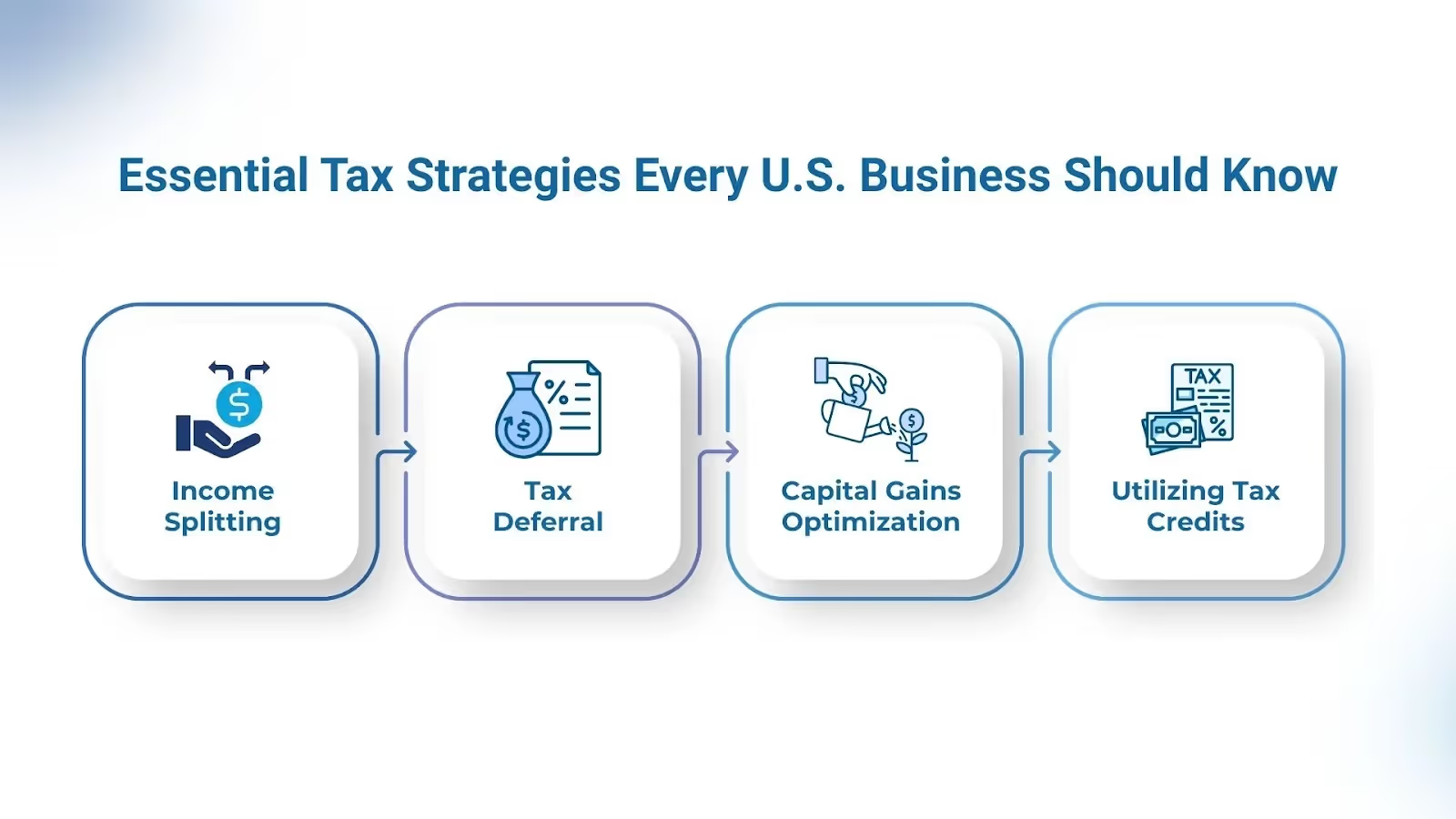

Now that we have a clearer understanding of the key components of tax planning, let's explore some of the most effective tax strategies that U.S. businesses can implement.

For U.S. businesses, strategic tax planning can significantly reduce tax liabilities, increase cash flow, and improve overall financial performance.

Income splitting is a tax strategy where business owners distribute income among multiple individuals such as family members or business partners, who may be in lower tax brackets. This method helps reduce the overall tax burden on the business. It’s particularly beneficial for businesses operating as partnerships or S-corporations, where profits are passed through to the owners’ personal tax returns.

Deferring taxes to future periods allows businesses to retain more capital for current use, which is especially beneficial for startups or those in growth stages. Tax deferral strategies can include postponing income recognition or accelerating business expenses.

For example, a business may defer income by postponing billing until the next tax year, or it can accelerate deductions by purchasing equipment or inventory before the year ends.

Capital gains taxes are typically lower than regular income taxes, and there are strategies that businesses can use to reduce their liability. One of the simplest methods is to hold investments or assets for more than a year before selling them. This qualifies the gains for long-term capital gains rates, which can be significantly lower than ordinary income tax rates.

Tax credits directly reduce the amount of tax owed and can provide a substantial financial benefit. Businesses can take advantage of various credits, such as:

With these strategies in mind, it’s important to understand how tax planning services can help ensure your business remains on track, compliant, and well-prepared for the future. Let’s explore how consulting a tax professional can provide value for your business.

Also Read: Online Accounting Services To Transform Business

Tax planning services provide businesses with expert advice, guidance, and support in structuring their tax affairs to maximize savings and ensure compliance.

Tax planning services provide expert advice to businesses on tax-saving strategies and ensure that their financial operations comply with the latest tax regulations. Tax professionals can identify areas where the business can reduce its tax burden through deductions, credits, and tax-deferred strategies, optimizing overall profitability.

Proactive tax planning can also help businesses prepare for audits. By ensuring that all tax records are accurate, complete, and compliant, tax professionals can reduce the risk of triggering an audit. They can also provide guidance on maintaining documentation, which is essential in the event of an audit, and ensure that the business is fully prepared to respond to any inquiries from tax authorities.

Every business is unique, and so are its tax needs. Tax planning services can create customized solutions that align with a company’s specific industry, size, and operational structure. Whether it’s a startup, a tech company, or a manufacturing firm, tax strategies can be tailored to ensure that businesses maximize their tax benefits while minimizing liabilities.

While effective tax planning is essential, businesses must also avoid certain mistakes that could undermine their tax strategies. Let’s look at some common tax planning mistakes U.S. businesses should avoid to stay compliant and efficient.

When it comes to strategic taxes, many businesses miss out on opportunities to optimize their tax strategy, often due to common mistakes. Avoiding these errors is essential for maximizing savings and ensuring compliance with both federal and state regulations.

Failing to plan taxes throughout the year can result in higher tax liabilities and missed opportunities for deductions. Tax planning should be an ongoing process rather than a last-minute scramble before filing season.

State-specific taxes can vary greatly, and businesses must understand the tax regulations in each state where they operate. Many companies focus on federal taxes but neglect state taxes such as sales tax, payroll tax, and franchise tax.

Many startups and small businesses fail to take full advantage of available tax credits. For instance, the Research and Development (R&D) Tax Credit, Work Opportunity Tax Credit (WOTC), and credits for energy-efficient investments can significantly reduce a company’s tax burden.

Now that we’ve covered common tax mistakes, let’s explore how VJM Global can help your business navigate these challenges and optimize your tax strategy.

VJM Global specializes in helping international businesses optimize their tax strategies, ensuring compliance with international regulations. With deep knowledge of international tax systems, VJM Global helps companies structure their operations to minimize tax liabilities while maximizing savings.

VJM Global offers customized tax planning services that align with the specific needs of your business. Whether you need guidance on choosing the right business structure, restructuring, maximizing deductions and credits, audits, or implementing strategies for tax deferral, VJM Global provides the expert advice necessary to make informed decisions and optimize your tax position.

For businesses expanding to or operating in India, VJM Global offers smooth compliance services. They help companies manage cross-border tax considerations, ensuring adherence to Indian tax regulations while maintaining full compliance with U.S., Australia, Singapore, UK, and UAE laws. Their expertise ensures that your business operations in both countries are tax-efficient and legally compliant.

If you want to ensure that your business is maximizing its tax savings and minimizing liabilities, reach out to us for a consultation today.