Form 1099 is one of the most consequential yet misunderstood documents in the U.S. tax system. Unlike a W-2, it arrives without any taxes already withheld — which means the financial responsibility lands squarely on you.

This guide covers what Form 1099 actually is, the most common variants you'll encounter, who must issue them, key deadlines and thresholds (including a significant change taking effect in 2026), how 1099 income is taxed, and how it compares to a W-2. Whether you're receiving a 1099 or issuing one to contractors, here's what you need to know.

Key Takeaways

- Form 1099 is an IRS "information return" used to report income earned outside of traditional employment.

- Over a dozen 1099 variants exist, covering freelance pay (1099-NEC), dividends (1099-DIV), retirement distributions (1099-R), and more.

- The $600 reporting threshold for 1099-NEC and 1099-MISC increases to $2,000 starting tax year 2026.

- Unlike W-2 employees, 1099 recipients manage their own tax withholding and owe self-employment tax on net earnings.

- All 1099 income must be reported on your federal return, even if you never receive the form.

What Is Form 1099?

Form 1099 is a family of IRS "information returns," not a single document. A payer — a bank, business, or individual — files a 1099 to report payments made to you that fall outside wages, salaries, or tips. Crucially, the IRS receives a copy directly from the payer at the same time you do.

How the IRS Uses It

The IRS runs an Automated Underreporter (AUR) program that cross-references income reported on your Form 1040 against the 1099s payers submit. If there's a discrepancy, expect a notice. This is why reconciling all your 1099s before filing matters — the IRS already has the data.

No Withholding: The Core Difference

When a company pays a contractor or an investor earns dividends, no federal or state income taxes are withheld from that payment. The recipient gets the full amount and is responsible for:

- Paying federal (and state) income tax on the income

- Paying self-employment tax, if the income comes from freelance or contract work

- Making quarterly estimated tax payments to avoid underpayment penalties

The 2026 Threshold Change

Under the One, Big, Beautiful Bill Act (Public Law 119-21, signed July 4, 2025), the $600 reporting threshold for 1099-NEC and 1099-MISC increases to $2,000 for tax years beginning after 2025, with inflation adjustments starting in calendar year 2027. This change does not apply to Form 1099-K, which operates under separate rules (see below).

Keep in mind: even if you're paid below the reporting threshold and receive no 1099, IRS Publication 525 is clear that you are still legally required to report that income on your tax return.

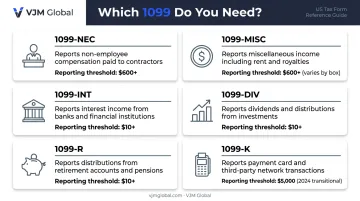

Most Common Types of 1099 Forms Explained

Most taxpayers encounter only a handful of 1099 variants. Which one you receive depends on the nature of the income.

Nonemployee Compensation and Miscellaneous Income

Form 1099-NEC (Nonemployee Compensation)

Reintroduced for tax year 2020, this form reports payments of $600 or more to freelancers, independent contractors, and self-employed individuals. The threshold rises to $2,000 starting tax year 2026. Recipients report this income on Schedule C.

Form 1099-MISC (Miscellaneous Information)

This form covers income outside contractor payments — rents, royalties, prizes, medical payments, and crop insurance proceeds. Most categories carry a $600 threshold; royalties are reportable at just $10. Applicable categories also shift to a $2,000 threshold in 2026.

Investment and Financial Income

Form 1099-INT (Interest Income)

Banks issue this form when interest earned exceeds $10 in a year. It's reported as ordinary income on Form 1040. If your taxable interest tops $1,500, you'll also need to file Schedule B.

Form 1099-DIV (Dividends and Distributions)

Brokerages issue this form for dividends and capital gain distributions of $10 or more. Ordinary dividends are taxed as regular income, while qualified dividends may qualify for the lower long-term capital gains rate. A related form, 1099-B, reports proceeds from stock and security sales and feeds into Form 8949 and Schedule D.

Form 1099-R (Retirement Distributions)

Distributions of $10 or more from pensions, annuities, IRAs, or profit-sharing plans trigger this form. Whether the distribution is taxable depends on the account type and the distribution code shown in Box 7 — so it pays to read that field carefully.

Other Noteworthy Forms

| Form | What It Reports | Key Threshold |

|---|---|---|

| 1099-G | Government payments: unemployment compensation, state tax refunds | $10 or more |

| 1099-K | Payment card and third-party network transactions (PayPal, Venmo, etc.) | More than $20,000 and more than 200 transactions (One Big Beautiful Bill Act) |

| 1099-DA | Digital asset transactions from brokers | Required for transactions on/after January 1, 2025 |

The 1099-K threshold has a recent history worth knowing. The prior IRS roadmap had it dropping to $600 in 2026, which alarmed gig workers and online sellers. The One Big Beautiful Bill Act reversed that direction, restoring the threshold to more than $20,000 and more than 200 transactions for third-party network reporting.

Who Issues and Who Receives a 1099?

Who Receives One

Any individual or entity that earns qualifying non-wage income may receive a 1099, including:

- Freelancers and independent contractors

- Landlords collecting rent

- Investors earning interest, dividends, or capital gains

- Retirees taking distributions from IRAs or pensions

- Gig workers paid through platforms like Uber or Etsy

- Businesses receiving payments through third-party networks

Important exception: Corporations are generally exempt from receiving a 1099-NEC or 1099-MISC — but this exemption does not apply to payments for legal or medical services.

The flip side of receiving a 1099 is knowing when your business is required to send one.

Who Must Issue One

Any business or individual making qualifying payments above the reporting threshold in the course of a trade or business must file the relevant 1099 form. Payer obligations include:

- Completing the appropriate 1099 form accurately

- Furnishing Copy B to the recipient by the applicable deadline

- Filing Copy A with the IRS by the required date

Since tax year 2023, businesses filing 10 or more information returns must file them electronically — a threshold confirmed by Treasury Decision 9972.

VJM Global's CPAs assist U.S. businesses with contractor payment reporting, 1099 filing, vendor reconciliation, and multi-state compliance requirements.

1099 Filing Thresholds and Key Deadlines

Knowing which threshold applies to each form — and when each deadline falls — keeps you out of penalty territory. The table below reflects current IRS rules and proposed changes under the One Big Beautiful Bill Act (OBBBA) for 2026.

Threshold Reference Table

| Form | 2025 Threshold | 2026 Threshold |

|---|---|---|

| 1099-NEC | $600 | $2,000 |

| 1099-MISC | $600 (most); $10 (royalties) | $2,000 (most categories) |

| 1099-INT | $10 | $10 |

| 1099-DIV | $10 | $10 |

| 1099-R | $10 | $10 |

| 1099-K | >$5,000 (2024); >$2,500 (2025) | >$20,000 and >200 transactions (proposed under OBBBA) |

| 1099-B | No single dollar threshold; all reportable sales | No single dollar threshold |

Filing Deadlines

- January 31 — Most 1099s must reach recipients; 1099-NEC is due to both recipients and the IRS by this date

- February 17 — Recipient deadline for 1099-B, 1099-S, and 1099-DA (adjusted for weekend/holiday in 2026)

- February 28 — IRS deadline for paper filers (most forms)

- March 31 — IRS deadline for electronic filers

Miss any of these dates and the IRS penalty clock starts immediately — with per-return charges that compound fast across large filing volumes.

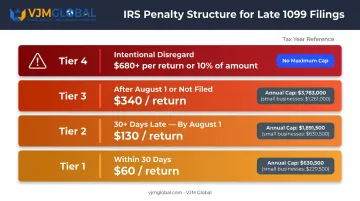

Penalties for Late or Incorrect Filing

Per IRC Sections 6721 and 6722, the IRS imposes penalties per return based on how late the filing is:

| Timing | Per-Return Penalty | Annual Cap (Standard) |

|---|---|---|

| Corrected within 30 days | $60 | $683,000 |

| Corrected 30+ days late, by August 1 | $130 | $2,049,000 |

| After August 1 or not filed | $340 | $4,098,500 |

| Intentional disregard | At least $680 or 10% of amount | No cap |

Small businesses have lower annual caps — but the per-return penalties are identical. A company filing 50 late returns after August 1 faces $17,000 in penalties — before any intentional disregard determination.

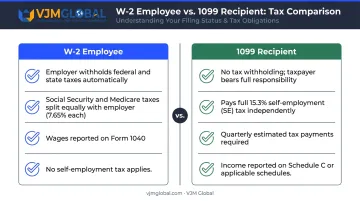

Form 1099 vs. W-2: Key Differences

The distinction comes down to one fundamental question: are taxes being withheld for you, or not?

| Feature | W-2 | 1099 |

|---|---|---|

| Issued by | Employer | Any qualifying payer |

| Reports | Wages, salary, tips | Non-wage income |

| Tax withholding | Federal, state, Social Security, Medicare | None by default |

| Self-employment tax | Employer pays half | Worker pays full 15.3% |

| Filing schedule | Form 1040 wages line | Varies by form type |

Quarterly Estimated Taxes

Because no taxes are withheld from 1099 payments, self-employed individuals and independent contractors must make quarterly estimated tax payments to the IRS. Generally, you're required to pay estimated taxes if you expect to owe $1,000 or more when you file. Missing these payments can result in underpayment penalties.

Self-Employment Tax

1099 workers earning income through freelance or contract work owe self-employment tax of 15.3%, which breaks down as:

- Social Security: 12.4% (employer + employee portions combined)

- Medicare: 2.9%

One upside: you can deduct half of the SE tax as an adjustment to income on Schedule 1, which directly reduces your taxable income.

That 15.3% obligation is one reason worker classification matters — being misclassified as an independent contractor when you're functionally an employee has real financial consequences.

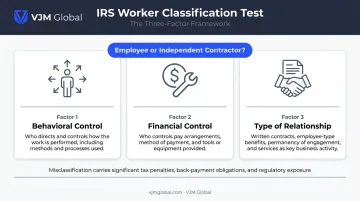

Worker Classification

The IRS evaluates whether a worker is an employee or an independent contractor using a three-factor test:

- Behavioral control — Does the business control how the work is performed?

- Financial control — Does the business control how the worker is paid and what tools they use?

- Type of relationship — Written contracts, employee benefits, and the permanency of the arrangement all factor in here.

Misclassifying an employee as an independent contractor can result in back taxes, interest, and steep penalties for the business.

How 1099 Income Is Taxed

Not all 1099 income is taxed the same way. The form type determines your tax rate, which forms you file, and what deductions you can claim.

Ordinary Income vs. Capital Gains

Ordinary income (1099-NEC, 1099-MISC, 1099-INT, 1099-R) is taxed at your marginal federal bracket. For 2025, those rates range from 10% to 37% depending on your taxable income and filing status.

Capital gains income (1099-B, qualified dividends from 1099-DIV) may qualify for the lower long-term capital gains rate — but only if the asset was held more than one year. Short-term gains (held one year or less) are taxed as ordinary income.

2025 long-term capital gains rates for single filers:

- 0% — up to $48,350

- 15% — $48,351 to $533,400

- 20% — above $533,400

Where 1099 Income Goes on Your Return

| 1099 Form | Report On |

|---|---|

| 1099-NEC | Schedule C |

| 1099-B | Form 8949 + Schedule D |

| 1099-MISC (rents) | Schedule E |

| 1099-R | Form 1040, lines 4a/4b or 5a/5b |

| 1099-INT | Form 1040 interest line; Schedule B if >$1,500 |

| 1099-DIV | Form 1040 dividend lines; Schedule B if >$1,500 |

Deductions That Reduce Your 1099 Tax Bill

Self-employed individuals can deduct legitimate business expenses on Schedule C, directly reducing taxable net income. Deductible expenses include:

- Home office (Form 8829)

- Car and truck expenses

- Equipment and supplies

- Travel and meals (subject to limits)

- Legal and professional services

- Contract labor

Knowing which deductions apply — and documenting them correctly — is where many self-employed filers leave money on the table. VJM Global's tax advisory team works with U.S. business owners to identify applicable deductions and ensure their filings hold up to IRS scrutiny.

Frequently Asked Questions

What is a 1099 form used for?

A 1099 is an IRS information return used to report various types of non-wage income — including freelance payments, interest, dividends, rents, and retirement distributions. The payer sends copies to both you and the IRS, ensuring all income is accounted for on your federal tax return.

How much tax will I pay on a 1099?

Ordinary 1099 income — such as contractor pay or interest — is taxed at your marginal federal bracket. Self-employed individuals also owe 15.3% self-employment tax on net earnings, though deductible business expenses can reduce the taxable amount. The exact amount varies by income type and your overall tax situation.

Is a 1099 the same as a W-2?

No. A W-2 reports wages paid to an employee with federal and state taxes already withheld. A 1099 reports non-wage income with no withholding, placing full tax responsibility — including self-employment tax — on the recipient.

Who is required to file a 1099 form?

Any business or individual that pays a non-corporate recipient $600 or more for services in 2025 must issue a 1099 — most commonly Form 1099-NEC. That threshold rises to $2,000 for tax year 2026. Payments to corporations are generally exempt.

What happens if I don't report 1099 income?

The IRS receives a copy of every 1099 directly from the payer. Unreported income is flagged through automated matching and typically results in a CP2000 notice, additional taxes owed, and penalties plus interest on the unpaid amount.

When are 1099 forms due?

Most 1099s must reach recipients by January 31. Forms 1099-B, 1099-S, and 1099-DA have a February 17 recipient deadline (for 2025 forms). Payers must also file with the IRS — by February 28 on paper or March 31 electronically. Always confirm current deadlines at IRS.gov.