Introduction

The US tax system doesn't reward guesswork. Many businesses struggle to keep pace with federal obligations, state-level variations, payroll requirements, and international reporting rules — and a missed deadline or misclassified entity type can trigger audits, penalties, or worse.

According to the IRS Data Book 2025, the IRS collected over $5.3 trillion in gross taxes in FY 2025 alone—and closed nearly 498,000 audits resulting in $26.8 billion in recommended additional tax. Non-compliance isn't abstract risk; it has real financial consequences.

This guide covers what US tax compliance actually means, the major types businesses must manage, critical deadlines and documents, and why compliance matters beyond just avoiding penalties. It also addresses the added complexity for businesses with cross-border operations: specifically, US companies expanding abroad and foreign entities establishing a US presence.

Key Takeaways

- US tax compliance spans federal, state, and international obligations—each with separate filing requirements and deadlines

- Filing the wrong return for your entity type is a common, costly mistake — entity structure determines your form

- Failure-to-file penalties reach 5% of unpaid taxes per month, up to 25%

- FBAR and FATCA reporting apply to US persons with foreign financial accounts above specific thresholds

- Cross-border operations add complexity: transfer pricing rules, foreign VAT/GST, and OECD reporting obligations

What Is Tax Compliance in the US?

Tax compliance means fulfilling all obligations under federal, state, and local tax laws—accurately reporting income, filing returns on time, paying what's owed, and maintaining adequate financial records throughout the year.

Enforcement operates at multiple levels. The Internal Revenue Service (IRS) serves as the primary federal authority under IRC sections 7801 and 7803, while state departments of revenue handle state-level obligations—which vary significantly in scope and structure.

Non-compliance consequences range from financial to criminal:

- Audits — triggered by anomalies in reported income or deductions

- Penalties and interest — accruing immediately on missed or underpaid obligations

- Criminal prosecution — in cases of willful fraud or evasion

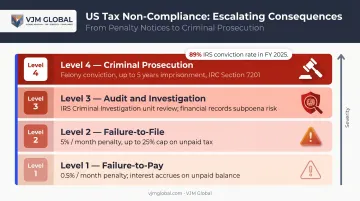

The scale of enforcement reflects how seriously these obligations are taken. The IRS Criminal Investigation unit reported 2,792 investigations initiated and 1,611 convictions in FY 2025, with an 89% conviction rate—spanning businesses and individuals across all income levels.

Types of Tax Compliance in the US

Federal Income Tax Compliance

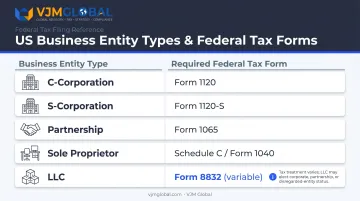

Every US business (except partnerships, which file information returns) must file an annual federal income tax return. The form depends on business structure:

| Entity Type | Tax Form |

|---|---|

| C-Corporation | Form 1120 |

| S-Corporation | Form 1120-S |

| Partnership | Form 1065 |

| Sole Proprietor | Schedule C (attached to Form 1040) |

| LLC | Variable—depends on elections and member count |

LLCs don't have a single default treatment. Multi-member LLCs default to partnership taxation; single-member LLCs default to disregarded entity status. Either can elect corporate treatment through Form 8832.

Tax obligations also differ by taxpayer type. US citizens and resident aliens file Form 1040 and are taxed on worldwide income—regardless of where they live or work. Corporations report income and compute liability on Form 1120.

Estimated tax payments compound this further. Individuals generally must make quarterly estimated payments when they expect to owe $1,000 or more after withholding and credits (IRS Publication 505). Corporations face the same requirement at a $500 threshold (IRS Publication 542).

Quarterly payment schedules differ by taxpayer type:

- Individuals: April 15, June 15, September 15, January 15 (following year)

- Corporations: April 15, June 15, September 15, December 15

Employment and Payroll Tax Compliance

Businesses with employees carry a distinct set of obligations separate from income tax.

Core payroll tax responsibilities:

- Withhold federal income tax based on each employee's Form W-4

- Withhold and match Social Security tax at 6.2% each (up to the $184,500 wage base in 2026)

- Withhold and match Medicare tax at 1.45% each (no wage base cap)

- Withhold an additional 0.9% Medicare Tax on wages exceeding $200,000 per employee

Required filings:

- Form 941 — Quarterly payroll tax return covering federal income tax, Social Security, and Medicare withheld

- Form 944 — Annual alternative for the smallest employers (total annual liability of $1,000 or less)

- Form 940 — Annual Federal Unemployment Tax (FUTA) return; applies when you paid wages of $1,500+ in any calendar quarter or had employees for 20+ weeks in the year

Payroll filings aren't the only reporting obligation. Businesses must also file information returns for independent contractors and other non-payroll payments. Form 1099-NEC covers nonemployee compensation—the threshold is $600 for payments made in 2025, rising to $2,000 for payments made in 2026.

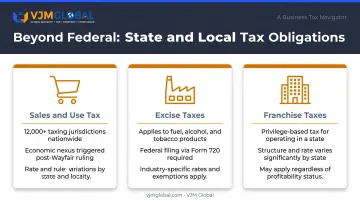

State, Local, and Indirect Tax Compliance

Federal compliance is only part of the picture. State and local obligations create a separate layer of requirements that vary significantly by jurisdiction. The Tax Foundation reports that 44 states levy corporate income taxes in 2026. Alaska, Illinois, Minnesota, and New Jersey impose top marginal rates of 9% or higher. Four states—Nevada, Ohio, Texas, and Washington—impose gross receipts taxes instead.

Beyond income taxes, businesses must navigate:

- Sales and use tax — Over 12,000 sales and use tax jurisdictions exist across the US. Following South Dakota v. Wayfair, states can impose sales tax obligations on remote sellers based on economic nexus, even without physical presence

- Excise taxes — Apply to manufacturers and sellers of fuel, alcohol, tobacco, and certain services; reported on Form 720 (Quarterly Federal Excise Tax Return)

- Franchise taxes — Charged in certain states for the privilege of doing business there, sometimes regardless of profitability

Each state's Department of Revenue sets its own rates, thresholds, and deadlines. There's no universal standard.

Essential Tax Compliance Documents and Deadlines

Core Federal Forms by Entity Type

| Form | Who Files It |

|---|---|

| Form 1040 | Individual US taxpayers |

| Form 1120 | C-Corporations |

| Form 1120-S | S-Corporations |

| Form 1065 | Partnerships |

| Form 941 | Employers (quarterly payroll) |

| Form W-2 | Employers reporting employee wages |

| FinCEN 114 (FBAR) | US persons with qualifying foreign accounts |

| Form 8938 | US taxpayers with foreign financial assets above thresholds |

Filing under the wrong form or entity classification triggers IRS scrutiny and potential penalties — verify your classification before the first return goes out.

Federal Filing Deadlines

- March 15 — S-Corporations and Partnerships (calendar-year filers)

- April 15 — C-Corporations and individual US residents

- June 15 — US citizens and resident aliens living abroad (automatic 2-month extension under IRS Publication 54)

A 6-month extension (Form 4868 for individuals) postpones the filing deadline, but does not extend the payment deadline. Interest accrues immediately on any unpaid balance.

For businesses and individuals with foreign accounts or assets, separate international reporting obligations layer on top of these domestic deadlines.

FBAR and FATCA Reporting

FBAR (FinCEN 114): US persons whose foreign financial accounts exceed $10,000 in aggregate at any point during the year must file electronically via the BSA e-Filing System. The deadline is April 15, with an automatic extension to October 15. This is a Treasury Department requirement, separate from IRS filings.

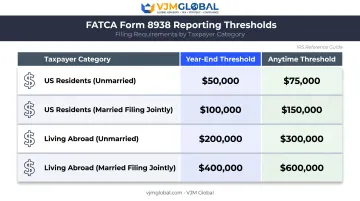

FATCA (Form 8938): US taxpayers holding foreign financial assets above certain thresholds must attach Form 8938 to their annual return. Thresholds vary by filing status and residency:

- US residents (unmarried): More than $50,000 on the last day of the tax year, or more than $75,000 at any time during the year

- US residents (married filing jointly): More than $100,000 on the last day, or more than $150,000 at any time

- Taxpayers living abroad (unmarried): More than $200,000 on the last day, or more than $300,000 at any time

- Taxpayers living abroad (married filing jointly): More than $400,000 on the last day, or more than $600,000 at any time

Failure to file Form 8938 can result in a $10,000 penalty, with additional penalties up to $50,000 for continued non-compliance after IRS notice.

Additional international forms include Form 5471 (US persons with interests in certain foreign corporations) and Form 8865 (US persons with interests in certain foreign partnerships). Missing either carries penalties starting at $10,000 per form per year, making them among the costlier oversights in international tax compliance.

The Importance of Tax Compliance for US Businesses

Financial and Legal Consequences

The numbers make the risk concrete. The IRS projects the annual gross tax gap at $696 billion for tax year 2022—the difference between taxes owed and taxes paid on time. Enforcement has intensified to close that gap.

Specific financial penalties include:

- Failure-to-file: Generally 5% of unpaid taxes per month, up to 25%

- Failure-to-pay: 0.5% of unpaid taxes per month after the due date

- Interest: Accrues on unpaid amounts regardless of whether penalties apply

- Criminal prosecution: Under IRC section 7201, willful tax evasion is a felony carrying fines and up to 5 years imprisonment

Business Credibility and Access to Capital

Those penalties are only the beginning. A clean compliance record also determines whether your business can access capital, win contracts, and close deals:

- Mergers and acquisitions — Tax compliance is routinely examined during due diligence; unresolved liabilities become deal blockers or reduce valuations

- Government contracting — Federal Acquisition Regulation (FAR) 52.209-5 requires offerors to certify delinquent tax status; SAM.gov entity registration includes tax compliance questions

- Banking and lending — Lenders routinely request tax returns as part of credit underwriting

- Licenses and permits — Many states condition business license renewals on confirmed tax standing

The IRS issues compliance status reports (Letters 6201, 6574, and 6575) that government agencies and business partners may review during vetting processes.

Operational and Reputational Risk

Tax non-compliance rarely stays contained to the tax department. An IRS audit can disrupt financial operations for months, divert management attention, and trigger collateral reviews of financial reporting practices.

Publicly disclosed tax issues damage relationships with customers, suppliers, and regulators alike. IRS digital detection tools now identify anomalies faster than before, so the assumption that non-compliance will go unnoticed is no longer a safe bet.

International Tax Compliance Obligations for US Entities

Cross-Border Complexity

US businesses operating abroad—and foreign businesses generating US-source income—face compliance obligations that extend well beyond domestic requirements.

Key areas of additional complexity:

- Transfer pricing — IRC section 482 authorizes the IRS to adjust income between related entities to prevent evasion. Documentation must exist when the return is filed and be provided within 30 days of request to preserve penalty protection

- Country-specific VAT/GST regimes — Operating in multiple jurisdictions means managing distinct indirect tax registrations and filings in each country

- OECD Pillar Two — The global minimum tax framework sets a 15% minimum effective tax rate for multinational groups with revenues exceeding EUR 750 million, with over 140 jurisdictions committed to implementation. US companies with significant international operations need to monitor their effective tax rate across all jurisdictions

FATCA's Impact on Foreign Financial Institutions

FATCA works in both directions. As the US Treasury explains, foreign financial institutions must report information about accounts held by US persons directly to the IRS. This makes undisclosed offshore assets increasingly difficult to conceal—and voluntary compliance considerably more important than it was a decade ago.

For US individuals and businesses with offshore assets, this means the reporting obligation can be triggered from two directions: your own Form 8938 filing and the institution's independent reporting to the IRS.

Working with Cross-Border Compliance Specialists

That dual-reporting structure is one reason why international tax obligations tend to grow more complex as a business scales—not less. For companies navigating the US-India corridor specifically, the requirements compound across entity type, transaction structure, and jurisdiction.

VJM Global's team of CPAs, Chartered Accountants, and international tax specialists works across FATCA and Form 8938 compliance, FBAR filings, transfer pricing documentation, DTAA advisory, and cross-border transaction structuring. For businesses operating between the US and India, that covers everything from initial setup and registration through annual filings and ongoing advisory.

Frequently Asked Questions

What is the FATCA filing requirement in the US?

FATCA requires US taxpayers with foreign financial assets above specified thresholds to report those assets on Form 8938 alongside their annual tax return. Penalties for failing to file start at $10,000 and rise to $50,000 for continued non-compliance.

Which document is used for tax compliance reporting in the US?

The primary form depends on taxpayer type: individuals file Form 1040, C-Corporations use Form 1120, partnerships use Form 1065, and employers file Form 941 for payroll taxes. For international obligations, FinCEN 114 (FBAR) covers foreign account reporting and Form 8938 applies for FATCA.

What are the consequences of failing to meet US tax compliance requirements?

Penalties include a failure-to-file charge of 5% of unpaid taxes per month (up to 25%) and a failure-to-pay charge of 0.5% per month, plus accrued interest. Willful tax evasion under IRC section 7201 is a federal felony carrying fines and potential imprisonment.

What is the difference between tax avoidance and tax evasion in the US?

Tax avoidance is the legal use of deductions, credits, and exclusions under the tax code to reduce liability—entirely permissible. Tax evasion is the deliberate concealment of income or misreporting of tax obligations, which constitutes a criminal offense under IRC section 7201, punishable by fines and imprisonment.

What are the major US federal tax filing deadlines businesses should know?

Three primary deadlines apply: March 15 for S-Corporations and partnerships, April 15 for C-Corporations and individual residents, and June 15 for US taxpayers living abroad. Extensions postpone filing but not payment—unpaid taxes accrue interest from the original due date.

Do foreign companies doing business in the US need to comply with US tax laws?

Yes. Foreign corporations with US-source income or a US business presence generally must file Form 1120-F and may be subject to withholding on certain payments. Specific obligations depend on the entity's structure, applicable tax treaties, and the nature and extent of US-sourced income.