Introduction

Picture this: your US-based e-commerce business is expanding into Europe. You've mastered sales tax compliance across multiple states, but suddenly you're encountering VAT on supplier invoices—and your European customers are asking why your prices don't include tax. What's happening?

Many US business owners face this exact scenario when expanding internationally. While the United States relies on a single-stage retail sales tax, most of the world uses Value-Added Tax (VAT). According to the OECD's Consumption Tax Trends 2024, the US is the only OECD member without a federal VAT, while 175 countries worldwide operate VAT or equivalent frameworks.

For businesses crossing borders, understanding both systems directly affects compliance obligations, pricing decisions, and cash flow. This guide breaks down how each system works, where they diverge, and what that means for your operations.

Key Takeaways

- VAT is collected at every supply chain stage; US sales tax applies only at the final sale

- The US has no federal VAT — 45 states impose sales tax across 12,120+ jurisdictions with different rates

- VAT systems include input tax credits for business purchases; US sales tax offers only resale exemptions

- The US is the only major economy without a national VAT — over 170 countries, including all EU members, India, and the UK, operate VAT-based systems

- US companies expanding into VAT jurisdictions such as India, the UK, or the EU must register locally, file periodic returns, and reprice offerings to account for embedded tax

VAT vs. US Sales Tax: At a Glance

Collection Point

VAT is collected at each stage of production and distribution — when raw materials are sold to manufacturers, when finished goods move to wholesalers, and when retailers purchase inventory. Each business in the chain charges VAT, then remits only the net difference to the government — not the full amount collected.

US sales tax is collected only once: at the final point of sale to the end consumer. Business-to-business transactions are generally exempt — buyers provide resale exemption certificates confirming they'll resell the goods.

Governance Level

VAT operates as a national system administered by federal governments. The UK's HMRC and India's GST Council, for example, apply uniform rules across their entire territories.

US sales tax operates at state and local levels with no federal involvement. Each of the 45 states with sales tax sets its own rates and rules, and counties and cities add further layers of complexity. In 2024, the US had 12,120 distinct sales tax jurisdictions — meaning a business selling across multiple states must track dozens of different rate schedules.

Tax Rates

Rather than comparing these systems in prose, the numbers speak for themselves:

| System | Rate Range | Examples |

|---|---|---|

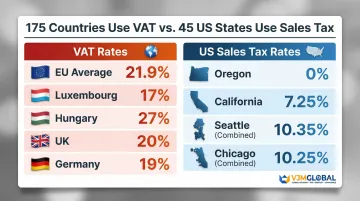

| VAT (EU average) | 17%–27% | Luxembourg 17%, Hungary 27% (OECD, 2024) |

| US State Sales Tax | 0%–7%+ | Oregon 0%, California 7.25% |

| US Combined Rates | Up to 10%+ | Seattle 10.35%, Chicago 10.25% |

Combined US rates in major cities rival standard VAT rates in many countries — a fact that surprises most international businesses entering the US market.

Input Tax Recovery

VAT's defining feature is the input tax credit mechanism. Businesses reclaim VAT paid on purchases by offsetting it against VAT collected on sales, remitting only the net difference. For cross-border operations, this means VAT paid on imported inputs can often be recovered — reducing the real tax burden on compliant businesses.

US sales tax has no equivalent mechanism. Businesses cannot recover sales tax paid on most business expenses. The only exception is resale exemption certificates, which require administrative documentation from buyers proving they'll resell the goods.

Consumer Use Tax

The US employs a companion "consumer use tax" that applies when sales tax wasn't collected at purchase — typically for out-of-state online orders. Buyers must self-report and pay use tax directly to their state.

VAT systems have no equivalent mechanism. Cross-border VAT is handled through reverse charge rules and import VAT at customs — the burden falls on businesses, not individual consumers.

What is VAT?

Value-Added Tax (VAT) is a multi-stage consumption tax levied on the value added to goods and services at each point in the supply chain—from raw materials through manufacturing, distribution, and retail. As of 2025, approximately 175 of 193 UN member countries use VAT or equivalent systems.

How the VAT Mechanism Works

Consider a simple supply chain:

- Raw materials supplier sells steel to a manufacturer for $1,000, charges 20% VAT ($200), collects $1,200 total, and remits $200 to the government

- Manufacturer transforms steel into machinery, sells it to a retailer for $3,000, charges 20% VAT ($600), collects $3,600 total, deducts the $200 VAT paid on steel, and remits $400 net to the government

- Retailer sells machinery to a customer for $5,000, charges 20% VAT ($1,000), collects $6,000 total, deducts the $600 VAT paid to manufacturer, and remits $400 net to the government

- Consumer pays $6,000 total ($5,000 + $1,000 VAT) and cannot reclaim any VAT

Total government revenue: $1,000 (20% of the final $5,000 value). Each business collected VAT but paid only on the value it added.

The Input Tax Credit System

Businesses registered for VAT reclaim the VAT they paid on business purchases (input tax) by offsetting it against the VAT they collect on sales (output tax). This avoids double-taxation and ensures the tax burden falls entirely on final consumers, not businesses.

This is what fundamentally separates VAT from US sales tax:

- Under VAT: A registered business spending $10,000 on equipment with 20% VAT ($2,000) recovers that $2,000 as an input tax credit

- Under US sales tax: That same business pays sales tax on the equipment with no recovery mechanism — the cost is simply absorbed

VAT Rates Across Countries

VAT rates vary by country and product type. Most countries maintain a standard rate alongside reduced rates for essentials:

- EU average standard rate: 21.9% (minimum 15% required by EU law)

- Hungary: 27% (EU's highest)

- United Kingdom: 20% (reduced rates: 5% and 0% for certain goods)

- Germany: 19% (reduced rate: 7%)

In 2022, VAT generated 20.8% of total tax revenue across OECD countries, making it the largest consumption tax category.

Global Reach and Local Variants

Many countries use VAT under different names. India replaced its complex state-level VAT system with a unified Goods and Services Tax (GST) on July 1, 2017, creating a multi-stage tax with rates of 0%, 5%, 12%, 18%, and 28%. Canada operates GST/HST (Goods and Services Tax/Harmonized Sales Tax) systems with similar principles.

For US businesses entering India, the GST framework carries significant compliance obligations — registration thresholds, return filing schedules, and input tax credit rules all differ meaningfully from the US system. VJM Global's Chartered Accountants work specifically with American companies on GST registration and ongoing compliance in India.

Use Cases of VAT

When US businesses encounter VAT:

- Selling products or services in the EU, UK, Canada, India, or other VAT jurisdictions

- Providing digital goods or SaaS to consumers in VAT countries (many now require non-resident sellers to register and charge VAT)

- Importing goods into VAT countries (import VAT applies at customs)

- Operating subsidiaries or branches in countries with VAT systems

VAT registration thresholds:

Most countries require VAT registration only when taxable sales exceed a threshold:

| Country | Threshold | Notes |

|---|---|---|

| United Kingdom | £90,000 | Based on 12-month taxable turnover; increased from £85,000 in April 2024 |

| Germany | €25,000/€100,000 | Small business exemption: ≤€25,000 prior year AND ≤€100,000 current year |

| India (GST) | ₹40 Lakh/₹20 Lakh | ₹40 Lakh for goods (₹20 Lakh in special states); ₹20 Lakh for services |

Below these thresholds, businesses may operate without charging VAT. Above them, immediate registration and tax collection become mandatory.

What is US Sales Tax?

US sales tax is a single-stage consumption tax collected by the seller at the final point of sale to the end consumer. Unlike VAT, it's not imposed at intermediate production or distribution stages—only the end consumer pays.

Jurisdictional Complexity

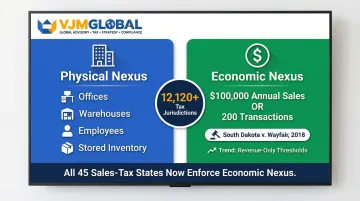

The US has no federal sales tax. Instead, 45 states plus the District of Columbia impose their own sales tax, with counties and cities adding local taxes. The result: more than 12,120 distinct tax jurisdictions across the country.

The rules shift constantly, too. In 2024 alone, there were 588 combined sales tax rate changes and new rates. Businesses operating across multiple states face hundreds of different rates, rules, and filing obligations.

Economic Nexus and Physical Nexus

Businesses must collect and remit sales tax only in states where they have "nexus"—a tax obligation triggered by presence or activity. Two types exist:

- Physical nexus — triggered by a tangible presence in a state: offices, warehouses, employees, or stored inventory.

- Economic nexus — triggered by exceeding sales thresholds, even without physical presence. Following the 2018 South Dakota v. Wayfair Supreme Court ruling, every state with a sales tax now enforces economic nexus.

The most common threshold is $100,000 in annual sales or 200 transactions. However, states are dropping transaction thresholds—South Dakota eliminated its 200-transaction requirement in July 2023, and Utah followed in July 2025. The trend is toward revenue-only thresholds.

Resale Exemption Certificates

Unlike VAT's automatic input credit system, US businesses purchasing goods for resale provide exemption certificates to avoid paying sales tax on those purchases. The seller verifies and retains the certificate, assuming liability if it's invalid.

For sellers, the administrative burden is real. They must collect, verify, and maintain exemption certificates from potentially thousands of wholesale customers.

Invalid certificates don't just create paperwork problems — they expose sellers to back-tax liability plus penalties.

Use Cases of US Sales Tax

Any business selling tangible goods or certain services to US consumers — whether in-store or online — must collect sales tax in states where they have nexus. But the rules vary considerably depending on what you sell:

- Groceries — exempt in most states, but taxed in others

- Clothing — tax-exempt in some jurisdictions, fully taxable elsewhere

- SaaS (Software-as-a-Service) — taxable in some states, exempt in others, and ambiguous in many

When sellers don't collect sales tax — for example, out-of-state online purchases made before economic nexus laws took effect — buyers technically owe "use tax," a parallel obligation they must self-report to their state. In practice, most consumers never do; awareness of use tax remains low even among regular online shoppers.

Key Differences Between VAT and US Sales Tax

Difference 1 — Governance and Uniformity

VAT operates as a centrally administered, nationally uniform tax. One authority sets the rules, one rate applies nationwide, and businesses deal with a single agency.

US sales tax is decentralized across state and local governments with zero harmonization. A business selling in 20 states navigates 20 different tax codes, rate structures, exemption rules, and filing systems. For businesses operating across multiple jurisdictions, US sales tax compliance is structurally more demanding than VAT compliance.

Difference 2 — Collection Stages and Business Burden

VAT: Every business in the supply chain participates in collection. Each business charges VAT on sales and reclaims VAT on purchases, creating a comprehensive paper trail for compliance and auditing. Because buyers need to verify VAT was charged correctly to claim input credits, the system is largely self-policing.

US sales tax: Collection falls entirely on the retailer at the point of sale. Intermediate businesses don't collect tax — they issue exemption certificates instead. This concentrates the compliance burden on retailers and removes any buyer incentive to verify whether tax was correctly applied.

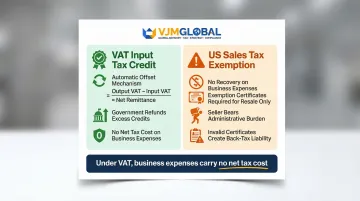

Difference 3 — Input Tax Recovery vs. Exemption Certificates

VAT approach: Registered businesses automatically offset tax paid on purchases against tax collected on sales. If a business pays $10,000 in input VAT and collects $15,000 in output VAT, it remits $5,000 net. If input exceeds output, the government refunds the difference.

US approach: No recovery mechanism exists for sales tax paid on business expenses (office supplies, equipment, utilities). The only exception is resale certificates for inventory purchased for resale — an administrative process requiring documentation from buyers.

The practical impact: under VAT, business expenses carry no net tax cost. Under US sales tax, businesses absorb sales tax on non-inventory purchases with no path to recovery — a real difference in effective tax burden.

Difference 4 — Tax Visibility and Pricing

VAT is often included in the shelf price displayed to consumers (tax-inclusive pricing). A product marked €100 in Germany includes €16.04 net price plus €15.96 VAT (19%). Consumers know exactly what they'll pay before reaching checkout.

US sales tax is added at checkout on top of the listed price. A product marked $100 might cost $107.50 after sales tax, depending on jurisdiction. For e-commerce businesses, this difference affects pricing strategy and consumer price comparison — particularly when US sellers enter international markets where tax-inclusive pricing is the norm.

Difference 5 — Filing and Reporting Obligations

VAT returns are typically filed monthly or quarterly with a single national authority. Businesses report total output VAT collected, total input VAT paid, and remit the net difference. One filing covers all transactions nationwide.

US sales tax filings are made separately to each jurisdiction where a business has nexus, with varying frequencies (monthly, quarterly, annually) and deadlines. Multi-state businesses can file hundreds of returns annually. Avalara, a tax automation provider, processed more than 6 million returns in 2024 for its 43,000 customers.

What This Means for Your Business

For US Businesses Operating Domestically

Your primary obligations center on understanding where you have nexus, tracking rate changes across active jurisdictions, and managing exemption certificates properly.

Action steps:

- Monitor sales in each state against economic nexus thresholds ($100,000 is the common trigger)

- Register for sales tax permits in states where you exceed thresholds

- Implement automated tax calculation software—manual tracking across 12,120+ jurisdictions is impractical

- Maintain valid exemption certificates from wholesale customers

- File returns on time to each jurisdiction (frequencies and deadlines vary)

For US Businesses Expanding Internationally

When entering VAT countries like India, the UK, or EU nations, expect an entirely different compliance model. You'll encounter national tax authorities, input tax credits, tax-inclusive pricing expectations, and registration thresholds.

Critical requirements:

- Registration: Once you exceed country-specific thresholds (£90,000 in UK, ₹40 Lakh for goods in India), you must register for VAT/GST

- Charging tax: Apply the correct rate to sales based on customer location and product category

- Filing returns: Submit monthly or quarterly returns detailing input and output VAT

- Managing credits: Track VAT paid on business purchases to claim input tax credits

- Pricing strategy: Decide whether to show tax-inclusive or tax-exclusive prices based on local norms

For US companies setting up in India specifically, GST registration, monthly return filing, and input tax credit optimization all require local expertise. VJM Global's team of CPAs and Chartered Accountants manages this compliance process for American businesses — covering initial registration, ongoing filing, and audit support — so your team can stay focused on operations.

Decision Guidance

If you sell only in the US: Master sales tax nexus rules, implement robust tax calculation and filing systems, and stay current with the 500+ annual rate changes.

If you sell to customers in VAT countries: Register and comply in those jurisdictions when you cross thresholds. Understand that VAT compliance differs fundamentally from sales tax—input credits, tax-inclusive pricing, and national filing all require system and process adjustments.

If you're establishing a subsidiary abroad: Local tax registration typically becomes a prerequisite before your first sale. Budget time and resources for registration, ongoing compliance, and potential audits in each country where you operate.

Frequently Asked Questions

Is there VAT tax in the USA?

The United States does not have a federal VAT. Instead, it uses a sales tax system administered at the state and local level — making the US the only OECD member country without a national VAT.

What is the VAT rate in the USA?

There is no VAT in the USA. Sales tax rates vary by state and locality, ranging from 0% in the five states with no sales tax to combined state-plus-local rates exceeding 10% in jurisdictions like Seattle and Chicago.

What do the USA use instead of VAT?

The US uses a retail sales tax system, where tax is charged only at the final point of sale to the consumer. Unlike VAT, it's not collected at each production stage, and there is no input tax credit mechanism for businesses.

How much VAT do I pay on $1000?

Americans don't pay VAT on domestic purchases. If buying in a VAT country — for example, the UK at 20% — a $1,000 purchase would include roughly $200 in VAT. Non-residents are often eligible for a VAT refund on qualifying purchases when departing.

Do Americans pay sales tax?

Yes, Americans pay sales tax when purchasing taxable goods and services in states that impose it. The rate depends on state and local jurisdiction. Five states have no state sales tax: Alaska, Delaware, Montana, New Hampshire, and Oregon (though Alaska allows local municipalities to impose sales tax).

Are US tariffs the same as VAT?

Tariffs and VAT are distinct mechanisms. Tariffs are border taxes on imported goods — applied to protect domestic industries or generate trade revenue. VAT is a domestic consumption tax collected at each supply chain stage. That said, many countries calculate import VAT on the customs value including tariffs, freight, and insurance, meaning tariffs and VAT compound on cross-border purchases.