Introduction

Choose the wrong accounting framework and you may not realise it until a funding round stalls or an international expansion hits a wall. UK businesses preparing financial statements follow either UK GAAP (primarily FRS 102) or IFRS — a choice governed by the Companies Act 2006. Listed companies on UK regulated markets must use IFRS for consolidated accounts; others may choose either framework.

The difference matters more than most finance teams expect. It shapes your balance sheet presentation, financial ratios, investor perception, and compliance costs.

The pressure becomes acute at trigger events. Businesses raising external investment, preparing for a listing, or expanding internationally often find their accounting framework creates unexpected friction. International investors struggle to benchmark FRS 102 financials against IFRS-reporting peers. For UK companies entering India specifically, Ind AS (Indian Accounting Standards) is converged with IFRS — so businesses already on IFRS face a significantly smoother transition than those on UK GAAP.

What follows covers the key accounting areas where the two frameworks diverge and how to determine which one fits your business.

Key Takeaways

- FRS 102 applies to private UK companies and SMEs; IFRS is mandated for listed companies and used in 140+ countries.

- Key divergences: lease accounting, revenue recognition, intangible assets, and borrowing cost capitalisation.

- UK GAAP gives more policy flexibility; IFRS is more prescriptive and internationally comparable.

- Companies raising investment, planning a listing, or entering India typically transition to IFRS.

UK GAAP vs IFRS: Quick Comparison

The table below summarises the key accounting differences at a glance — useful when evaluating which framework applies to your entity or when reconciling cross-border financial statements.

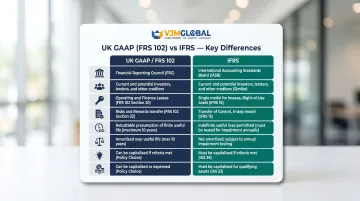

| Aspect | UK GAAP (FRS 102) | IFRS |

|---|---|---|

| Governing Body | Financial Reporting Council (FRC) | International Accounting Standards Board (IASB) |

| Primary Users | Private UK companies, SMEs | Listed UK companies, multinationals, 140+ countries |

| Mandatory for Listed Companies? | No (optional for individual accounts) | Yes (for consolidated accounts, since 2005) |

| Lease Accounting | Finance/operating lease distinction; operating leases off-balance-sheet | Single on-balance-sheet model (IFRS 16) for virtually all leases |

| Revenue Recognition | Risks-and-rewards transfer model | Five-step performance obligation model (IFRS 15) |

| Intangible Assets Useful Life | Finite lives only; maximum 10 years if not reliably estimable | Can have indefinite useful lives |

| Goodwill Treatment | Amortised over finite useful life | Not amortised; tested annually for impairment |

| Development Cost Capitalisation | Accounting policy choice | Mandatory when six criteria met |

| Borrowing Costs | Optional capitalisation | Mandatory capitalisation for qualifying assets |

| Investment Property | Choice between fair value (if reliably measurable) or cost model | Choice between fair value model or cost model (IAS 40) |

Note on UK GAAP variants: FRS 101 and FRS 102 Section 1A are reduced-disclosure frameworks with specific eligibility:

- FRS 101 — applies to subsidiaries within IFRS groups; uses IFRS recognition and measurement with reduced disclosure requirements

- FRS 102 Section 1A — applies to small companies meeting the Companies Act size thresholds

- Core recognition and measurement rules remain consistent across all variants

What is UK GAAP?

UK GAAP is the suite of Financial Reporting Standards issued by the Financial Reporting Council, with FRS 102 being the primary standard for most UK entities. These standards underwent significant revision in 2015, replacing old SSAPs and FRSs with a framework based on the IASB's IFRS for SMEs — making UK GAAP broadly aligned with full IFRS, but distinct in key areas.

That philosophy centres on proportionality. UK GAAP blends rules-based and principles-based guidance, designed to be less burdensome for private and smaller entities while still delivering high-quality, true-and-fair financial information.

Recent updates: On 27 March 2024, the FRC issued major amendments to FRS 102, effective for periods beginning on or after 1 January 2026 (early adoption permitted). These changes introduce IFRS 15-equivalent revenue recognition and IFRS 16-equivalent lease accounting, narrowing the gap between UK GAAP and IFRS.

Who Typically Uses UK GAAP?

Typical users include:

- Privately owned SMEs and owner-managed businesses

- Subsidiaries of larger groups (using FRS 101 for reduced disclosure)

- Small companies eligible for Section 1A reduced-disclosure exemptions

- Businesses not yet seeking external investment from outside the UK

When businesses stay on UK GAAP vs. consider switching:

Companies typically remain on FRS 102 when operations are UK-focused, funding is domestic, and stakeholders understand UK reporting conventions. The conversation shifts to IFRS when trigger points emerge: raising VC or PE funding from international investors, preparing for an IPO, or expanding operations across borders. Each of these scenarios demands the cross-border comparability that only IFRS can reliably provide.

What is IFRS?

IFRS is the set of accounting standards issued by the International Accounting Standards Board, used in more than 140 countries, and designed to create globally comparable, transparent financial statements. UK-listed companies have been required to use IFRS for consolidated financial statements since 2005, following EU Regulation No 1606/2002.

At its heart, IFRS is principles-based — it requires professional judgement and detailed disclosure rather than prescriptive rules. This flexibility comes at a cost: more sophisticated accounting expertise and higher preparation costs compared to UK GAAP.

Post-Brexit context: Following the Brexit transition period ending 1 January 2021, the UK created UK-adopted IFRS (UK IFRS). The UK Endorsement Board (UKEB) now endorses standards for UK use, rather than automatically adopting EU-endorsed IFRS.

In practice, no material divergences exist between UK-adopted IFRS and IASB-issued IFRS. Companies should be aware of this structural distinction, though future divergence remains possible.

Who Typically Uses IFRS?

IFRS users include:

- All UK companies listed on a regulated market (e.g., London Stock Exchange main market)

- Subsidiaries of foreign parent companies reporting under IFRS at group level

- Businesses actively seeking international investment or planning cross-border expansion

India expansion context: UK companies expanding to India should note that India follows Ind AS (Indian Accounting Standards), which is converged with IFRS but not identical. Key Ind AS carve-outs include:

- Investment property must use the cost model only (fair value model not permitted)

- Bargain purchase gains are recognised in Other Comprehensive Income rather than profit or loss

UK businesses already reporting under IFRS will find the transition to Indian group reporting requirements smoother than those on UK GAAP. VJM Global supports UK companies in maintaining accurate, standards-compliant financial reporting across both jurisdictions.

Key Differences Between UK GAAP and IFRS

Lease Accounting

The lease accounting split is fundamental. Under FRS 102, leases are classified as either finance leases (on-balance-sheet) or operating leases (off-balance-sheet, expensed on a straight-line basis).

Under IFRS 16, this distinction disappears for lessees. Virtually all leases over 12 months must be recognised as a right-of-use asset and corresponding lease liability on the balance sheet. Short-term leases (12 months or less) and low-value asset leases are exempt.

Financial impact: Companies transitioning from UK GAAP to IFRS will see significant balance sheet changes:

- Total assets and liabilities increase

- EBITDA improves (lease costs move from operating expenses to depreciation and interest)

- Net profit may be lower in early years of a lease due to front-loaded interest charges

The IFRS Foundation estimated approximately US$2.18 trillion in present-value lease commitments being brought on-balance-sheet globally. Most affected sectors include airlines (22.7% of total assets), retailers (21.4%), and travel/leisure (20.7%). For retailers, 36% of the sample had estimated lease liabilities exceeding 50% of total assets.

For businesses valued on EBITDA multiples, the improved EBITDA metric directly affects valuation discussions with investors or acquirers.

FRS 102 amendments: From 1 January 2026, FRS 102 will introduce an IFRS 16-like model, bringing most leases on-balance-sheet for lessees. Key differences from IFRS 16 include:

- Permission to use an "obtainable borrowing rate" if the implicit rate or incremental borrowing rate is difficult to determine

- Fewer disclosure requirements

- No requirement to restate comparatives (cumulative adjustment to opening retained earnings instead)

Revenue Recognition

FRS 102 uses a risks-and-rewards approach: revenue is recognised when the significant risks and rewards of ownership transfer and the amount can be reliably measured. IFRS 15 uses a control-based five-step model:

- Identify the contract(s) with a customer

- Identify the performance obligations in the contract

- Determine the transaction price

- Allocate the transaction price to the performance obligations

- Recognise revenue when (or as) the entity satisfies a performance obligation

Where timing divergence matters:

Complex multi-element contracts are particularly affected:

- SaaS subscriptions and bundled product-service arrangements: IFRS 15 requires unbundling performance obligations and allocating transaction price based on relative standalone selling prices, not marketing costs

- Long-term construction contracts: Performance obligation satisfaction determines timing under IFRS 15

- Professional services with performance-based fees: Variable consideration must be estimated subject to constraint

- Retail with customer loyalty schemes: Refund liabilities and loyalty points require separate recognition

From 1 January 2026, FRS 102 Section 23 will replace the risks-and-rewards model with a five-step approach closely aligned with IFRS 15, further narrowing the gap.

Intangible Assets and Goodwill

Useful life difference:

- FRS 102: All intangible assets (including goodwill) must have finite useful lives. Where a reliable estimate cannot be made, the amortisation period cannot exceed 10 years.

- IAS 38 and IFRS 3: Intangible assets can have indefinite useful lives (not amortised, but tested annually for impairment). Goodwill is never amortised but tested annually for impairment.

Development cost treatment:

- FRS 102: Accounting policy choice — entities may capitalise or expense development costs, even when capitalisation criteria are met, provided the policy is applied consistently.

- IAS 38: Mandatory capitalisation once six specific criteria are met (commonly remembered by the acronym PIRATE: Probable future economic benefits, Intention to complete and use/sell, Resources available, Ability to use or sell, Technical feasibility, Expenditure reliably measurable).

This affects how R&D-heavy businesses present assets and profitability metrics. A software company expensing all development costs under FRS 102 will show lower assets and lower short-term profits than one required to capitalise under IAS 38.

Other Key Differences

Borrowing costs:

- FRS 102: Accounting policy choice — entities may capitalise borrowing costs directly attributable to qualifying assets, but it's not mandatory

- IAS 23: Mandatory capitalisation of borrowing costs for qualifying assets (those taking a substantial period to get ready for intended use or sale)

Investment property:

- FRS 102: Fair value measurement required with changes through profit or loss (where fair value can be measured reliably without undue cost or effort)

- IAS 40: Choice between fair value model (changes through P&L) or cost model (cost less depreciation less impairment) — giving IFRS preparers more flexibility

Deferred taxes:

- FRS 102: Uses "timing differences" concept (income statement-focused, based on differences between taxable profit and accounting profit)

- IAS 12: Uses "temporary differences" concept (balance sheet-based, comparing carrying amount to tax base)

This can lead to different deferred tax balances, especially in business combinations.

Business combination transaction costs:

- FRS 102: Transaction costs (advisory, legal, due diligence fees) are included in the acquisition cost (capitalised)

- IFRS 3: Transaction costs are expensed as incurred and do not form part of the consideration transferred

Which Framework Is Right for Your Business?

For most UK-based private companies with domestic operations and no external investors, UK GAAP (FRS 102) is the practical default. It is lower cost to prepare, better understood by local accountants and lenders, and sufficient for statutory compliance.

IFRS becomes the more appropriate choice when:

- The business has or plans to have listed securities

- International institutional investors are involved or planned

- Subsidiaries operate in IFRS-adopting countries

- The group parent already reports under IFRS

Four factors should drive your evaluation:

- International investment or IPO plans: IFRS provides better investor comparability. FRS 102 and FRS 101 are not accepted in listing documents.

- Group structure: If the parent reports under IFRS, using FRS 101 for UK subsidiaries is cost-efficient — it applies IFRS recognition and measurement with a reduced disclosure burden.

- Sector-specific reporting needs: Financial services, real estate with complex lease portfolios, and retail are all materially affected by IFRS 16 and IFRS 9.

- Cost of transition and ongoing preparation: IFRS requires more disclosure and specialist expertise, which increases ongoing costs.

With those factors in mind, the decision usually maps to one of three scenarios:

- Choose FRS 102 if your business is owner-managed, privately funded, and UK-focused

- Consider IFRS if you are raising PE/VC capital from international investors, planning a stock exchange listing, or managing a group with subsidiaries across multiple jurisdictions

- Consider FRS 101 if you are a subsidiary within an IFRS group and want to reduce the disclosure burden while maintaining IFRS recognition and measurement

For UK businesses with operations in India or other cross-border jurisdictions, the framework decision carries additional complexity around group consolidation and local statutory requirements. Getting that choice right — and maintaining compliance under it — typically calls for advisory support from a firm experienced in both UK and international standards. VJM Global works with UK businesses and multinationals navigating exactly these decisions, including companies managing operations across the UK and India.

Conclusion

Choosing between UK GAAP and IFRS is a strategic decision shaped by growth ambitions, funding sources, and international footprint. FRS 102 offers simplicity and proportionality for domestic businesses, while IFRS provides the global comparability that investors, regulators, and cross-border partners expect.

The FRC is actively updating FRS 102 to align with IFRS 15 and IFRS 16 equivalents. The January 2026 amendments will introduce comparable revenue recognition and lease accounting models, which means the gap between the two frameworks is narrowing.

Businesses should plan ahead rather than wait for a trigger event to force a rushed transition. Common triggers include:

- Fundraising rounds that attract institutional or international investors

- Listing on a public exchange

- Cross-border expansion or acquisition activity

Engaging an accounting adviser early — well before any of these events — gives you the time to assess the transition cost, prepare staff, and restate comparatives without disruption.

Frequently Asked Questions

Does the UK use IFRS or UK GAAP?

The UK uses both. Listed companies on regulated markets must use IFRS for consolidated financial statements, while most private and smaller UK entities use UK GAAP (primarily FRS 102). Non-listed groups and companies may choose either framework.

What is the difference between UK GAAP and IFRS?

UK GAAP (FRS 102) is a national standard suited to private UK entities, with simpler and more proportionate rules. IFRS is the international standard used in 140+ countries, with stricter requirements on lease recognition, development cost capitalisation, and goodwill treatment — impairment-only under IFRS versus amortisation under FRS 102.

Does IFRS 16 apply to UK GAAP?

IFRS 16 does not directly apply to UK GAAP. FRS 102 historically retained the finance/operating lease distinction with operating leases kept off-balance-sheet. However, FRS 102 amendments effective 1 January 2026 introduce a similar on-balance-sheet model for leases, bringing UK GAAP closer to IFRS 16.

What is the UK equivalent of GAAP?

The UK equivalent is called UK GAAP, a suite of standards issued by the Financial Reporting Council (FRC), with FRS 102 being the primary standard. It replaced old UK GAAP in 2015 and is broadly based on the IASB's IFRS for SMEs.

Is UK GAAP different from US GAAP?

Yes, they are distinct frameworks. US GAAP, issued by the FASB, is a rules-based system used exclusively in the United States. UK GAAP, issued by the FRC, is more principles-based — and unlike US GAAP, both UK GAAP and IFRS prohibit the LIFO inventory method and differ on lease accounting treatment.