Introduction

Most Singapore businesses entering India encounter the same early surprise: audit compliance here isn't a single obligation — it's several, running under different laws, tracked by different authorities, and tied to deadlines that don't align with anything back home.

India's audit ecosystem operates simultaneously under the Companies Act 2013, the Income Tax Act, and GST legislation. Each creates its own reporting requirements, and missing any one of them carries real financial and director-level consequences.

This guide walks Singapore investors through India's audit reporting framework. You'll learn which audits apply to your Indian entity, how to interpret the four audit opinion types, what deadlines to track, and where India's requirements diverge from Singapore's single statutory audit model.

Key Takeaways:

- Every Indian company undergoes statutory audit — no small company exemption exists

- Tax audit and GST reconciliation trigger at specific turnover thresholds (INR 1–10 crore; INR 5 crore)

- Four audit opinions range from clean to disclaimer — each affects consolidation and financial credibility

- Missed deadlines carry penalties from INR 25,000 to INR 5,00,000, plus director-level fines

- India's fixed April–March financial year and mandatory auditor rotation differ fundamentally from Singapore's framework

Why Singapore Businesses Need to Understand India's Audit Framework

Any Singapore company incorporating an Indian subsidiary, branch office, or LLP becomes subject to India's domestic audit obligations from day one — regardless of the parent company's Singapore audit status. Under the Companies Act 2013, the Indian entity is treated as a separate legal entity and must comply independently with all statutory requirements.

Indian Chartered Accountants (CAs) issue audit reports that serve multiple stakeholders beyond the company itself. Each has a distinct compliance trigger:

- The Registrar of Companies (ROC) requires audited financial statements within 30 days of the Annual General Meeting

- Income tax authorities mandate tax audit reports for entities exceeding prescribed turnover thresholds

- Banks scrutinise audit opinions before approving credit facilities

- Foreign investors examine audit reports as primary indicators of financial health and governance quality

These stakeholder obligations intersect with treaty-level requirements. The India-Singapore Double Taxation Avoidance Agreement (DTAA) directly impacts transfer pricing compliance and profit repatriation. Article 9 governs associated enterprise provisions, making clean audit reports essential for supporting arm's length pricing documentation and facilitating dividend remittances without additional scrutiny.

What a qualified opinion costs your Singapore parent: If an Indian subsidiary receives a qualified, adverse, or disclaimer audit opinion, it flows through to the Singapore parent's consolidated financial statements. Singapore auditors will question the reliability of Indian subsidiary figures, potentially requiring adjustments or additional disclosures that affect group-level reporting to shareholders, lenders, or regulators like the Singapore Exchange.

For Singapore companies unfamiliar with these requirements, the compliance calendar alone can create exposure — penalties for late or non-compliant filings can reach INR 5,00,000 for companies, with additional personal fines for directors.

Types of Audits Singapore-Owned Indian Entities Must Undergo

India does not have a single unified audit cycle. Multiple distinct audits run in parallel, each governed by different laws, conducted by different professionals, and submitted to different authorities. Singapore businesses accustomed to one annual statutory audit must budget for and coordinate several simultaneous compliance exercises.

Statutory Audit (Companies Act 2013)

The statutory audit is the primary, mandatory audit of all Indian companies regardless of size or turnover. Section 139(1) of the Companies Act 2013 states categorically: "every company shall, at the first annual general meeting, appoint an individual or a firm as an auditor."

No small-company exemption exists. A private limited company with INR 1 lakh turnover and one with INR 100 crore face identical statutory audit obligations.

Key characteristics:

- Conducted by a licensed Chartered Accountant registered with the Institute of Chartered Accountants of India (ICAI)

- Covers complete financial statements: balance sheet, profit & loss account, cash flow statement, and notes

- Submitted to shareholders and filed with ROC using Form AOC-4 within 30 days of the AGM

- Follows ICAI's Standards on Auditing (SA series), aligned with International Standards on Auditing (ISAs) — making methodology broadly comparable to Singapore's SSAs

VJM Global serves as the appointed CA firm for foreign-owned Indian entities, handling the full statutory audit engagement from planning and risk assessment through final report issuance and ROC filing.

Tax Audit (Section 44AB, Income Tax Act)

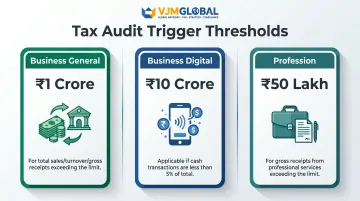

The tax audit is a separate exercise conducted specifically for income tax compliance. It is triggered when an Indian entity's business turnover exceeds prescribed thresholds:

| Category | Threshold | Condition |

|---|---|---|

| Business (general) | INR 1 crore | Total sales/turnover/gross receipts exceed INR 1 crore |

| Business (digital) | INR 10 crore | Cash receipts and cash payments each do not exceed 5% of total |

| Profession | INR 50 lakh | Gross receipts in profession exceed INR 50 lakh |

Source: Income Tax Department, Section 44AB

Most Singapore-owned subsidiaries in IT services or professional services qualify for the INR 10 crore threshold — their predominantly non-cash operations meet the digital transaction criteria.

The output is Form 26 under the Income-tax Act 2025 (effective from tax year 2026-27), which officially replaces legacy Forms 3CA, 3CB, and 3CD. For assessment year 2025-26 and prior years, the old forms still apply.

The tax audit report is filed electronically with the income tax return — it is a separate document from the statutory audit report under the Companies Act.

GST Audit (GSTR-9C)

Indian entities with annual aggregate GST turnover exceeding INR 5 crore must file GSTR-9C, a reconciliation statement certifying that GST returns match audited financial statements. CBIC Circular No. 246/03/2025-GST confirms this threshold. Taxpayers with turnover between INR 2-5 crore may self-certify from FY 2020-21 onwards, removing the mandatory CA certification requirement for this segment.

Singapore companies running manufacturing, trading, or service operations in India commonly cross this threshold. The reconciliation must be filed by December 31 of the following financial year. Late filing attracts penalties of INR 200 per day (INR 100 CGST + INR 100 SGST), capped at 0.50% of turnover in the relevant state.

VJM Global provides GST audit services including thorough examination of GST records, input tax credit verification, and GSTR-9C preparation to ensure error-free compliance.

Secretarial and Internal Audits

Singapore subsidiaries that scale past certain turnover or capital thresholds will trigger two further mandatory audits under the Companies Act — secretarial and internal.

Secretarial Audit (Section 204, Companies Act 2013): Mandatory for:

- All listed companies

- Public companies with paid-up capital ≥ INR 50 crore OR turnover ≥ INR 250 crore

- Private companies with paid-up capital ≥ INR 10 crore

Conducted by a practicing Company Secretary, the secretarial audit reviews compliance with the Companies Act, SEBI regulations (if applicable), and other corporate laws.

Internal Audit (Section 138, Companies Act 2013): Mandatory for:

- All listed companies (no threshold)

- Unlisted public companies with turnover ≥ INR 200 crore OR outstanding loans/borrowings > INR 100 crore OR paid-up capital ≥ INR 50 crore OR deposits ≥ INR 25 crore

- Private companies with turnover ≥ INR 200 crore OR outstanding loans/borrowings > INR 100 crore

Source: Rule 13, Companies (Accounts) Rules 2014

VJM Global coordinates both secretarial and internal audits for foreign-owned entities meeting these thresholds, working with empanelled Company Secretaries and employing system-focused methodologies that provide actionable recommendations beyond compliance tick-boxes.

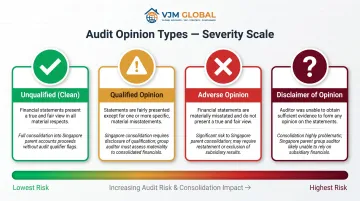

The 4 Types of Audit Report Opinions in India — What They Mean for Your Business

The audit opinion is the bottom-line verdict from the Indian auditor on whether the entity's financials are reliable. Indian audit opinions follow ICAI Standards on Auditing (SA 700, SA 705, SA 706), which map closely to International Standards on Auditing (ISAs).

Unqualified (Clean) Opinion

This is the best possible outcome. The auditor confirms that financial statements present a true and fair view in accordance with Indian Accounting Standards (Ind AS or AS, as applicable) and are free from material misstatement. The auditor obtained sufficient appropriate audit evidence and identified no issues requiring modification.

For Singapore parent companies, this is the expected baseline when consolidating Indian subsidiary financials. A clean opinion provides assurance that the Indian entity's figures can be reliably incorporated into group accounts without adjustment or qualification.

Qualified Opinion

A qualified opinion is issued when the auditor identifies material misstatements or has insufficient evidence on specific issues, but these problems are not pervasive enough to invalidate the entire report. The auditor specifies the exact areas of concern in a "Basis for Qualified Opinion" paragraph.

Common triggers include:

- Inventory valuation discrepancies identified during physical verification

- Incomplete or undocumented related-party transaction disclosures

- Depreciation method changes not properly disclosed

- Tax provisions understated due to disputed positions

For Singapore parent companies, a qualified opinion signals a remediation priority. Your group auditors will scrutinise the qualification and may require consolidation adjustments or additional group-level disclosures.

Banks also treat qualifications seriously. Credit applications from entities with qualified opinions routinely face additional scrutiny or outright rejection.

Adverse Opinion

An adverse opinion is the most serious outcome. It means the financial statements contain pervasive material misstatements and cannot be relied upon. The auditor concludes that the statements do not present a true and fair view of the company's financial position.

Downstream consequences are severe:

- Indian regulators (income tax department, ROC) may initiate scrutiny or investigation

- Banks typically withdraw existing credit facilities or decline new applications

- Singapore parent companies face significant complications consolidating an adverse-opinion entity into group financial reporting

- Listed Singapore parent entities may face SGX or MAS disclosure obligations regarding subsidiary financial irregularities

Disclaimer of Opinion

A disclaimer is the auditor's declaration that they cannot form any opinion due to insufficient access to records or inability to obtain satisfactory evidence. Unlike an adverse opinion, a disclaimer reflects a scope limitation rather than known misstatement.

Disclaimers can arise when:

- Management denies access to related-party transaction records

- Books of account are incomplete or destroyed

- Supporting documentation for major transactions is unavailable

- Inventory physical verification was prevented

Under the Companies Act 2013, cooperation with statutory auditors is a legal obligation. A disclaimer signals serious governance or record-keeping failures that require urgent board-level intervention.

Emphasis of Matter

An Emphasis of Matter paragraph is an addition to an otherwise clean report. It draws attention to significant uncertainties without changing the overall opinion. Common scenarios include:

- Ongoing tax litigation with material potential liability

- Going-concern doubts due to accumulated losses or negative net worth

- Regulatory investigations that could materially impact operations

Worth noting: an Emphasis of Matter does not downgrade the audit opinion. Singapore parent companies can still consolidate the entity's financials, though group-level disclosures about the flagged uncertainty may be appropriate — particularly for transfer pricing disputes or ongoing regulatory inquiries in India.

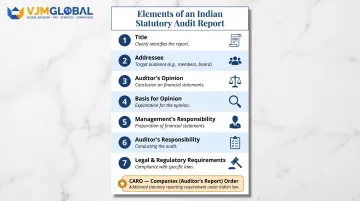

Structure and Key Components of an Indian Audit Report

Indian statutory audit reports follow a standardised structure prescribed by ICAI's Standards on Auditing (SA 700 series). Understanding this structure helps Singapore financial controllers quickly locate critical information.

Standard Report Elements:

- Title: "Independent Auditor's Report"

- Addressee: Shareholders or Board of Directors

- Auditor's Opinion: States whether financial statements present a true and fair view

- Basis for Opinion: Details the audit scope and compliance with Standards on Auditing

- Management's Responsibility: Describes management's role in preparing and presenting financial statements

- Auditor's Responsibility: Explains audit methodology and evidence-gathering approach

- Report on Other Legal and Regulatory Requirements: Includes CARO and other Companies Act reporting obligations

- Signature, Date, and Place: Auditor's credentials and report finalisation details

Key Audit Matters (SA 701): For listed entities and certain unlisted entities, auditors must include a Key Audit Matters section highlighting the most significant areas of audit focus. This typically covers complex accounting estimates, revenue recognition for long-term contracts, impairment assessments, or valuation of investments.

The CARO Requirement: India's Unique Disclosure Framework

Companies (Auditor's Report) Order 2020 (CARO) is an India-specific reporting requirement with no direct Singapore equivalent. For eligible companies, auditors must report on specific matters including:

- Physical verification of fixed assets and inventory

- Title deeds for immovable properties

- Loans granted to related parties and compliance with Section 185/186

- Statutory dues (GST, income tax, customs) payment status

- Default in repayment of borrowings to banks or financial institutions

- End-use of funds raised through debt or equity

- Fraud identified during the audit

- Related-party transaction disclosures

CARO exemptions apply to one-person companies, small companies (paid-up capital ≤ INR 4 crore and turnover ≤ INR 40 crore meeting additional conditions), banking/insurance companies, and Section 8 (non-profit) companies.

For Singapore finance teams reviewing an Indian subsidiary's audit for the first time, CARO is typically the most unfamiliar section — it goes well beyond financial statement presentation to flag operational and regulatory compliance gaps directly.

How to Cross-Read the Audit Report with Financial Statements

When reviewing an Indian audit report, your finance team should cross-reference four key areas against the notes to financial statements:

- Basis of Opinion paragraph: Identifies any qualifications, limitations, or concerns

- CARO report items: Flags compliance gaps or operational irregularities

- Key Audit Matters section: Highlights the highest-risk areas requiring management attention

- Emphasis of Matter paragraphs: Reveals material uncertainties or ongoing disputes

Any qualification in the Basis of Opinion or a CARO flag on statutory dues should prompt immediate follow-up with your Indian subsidiary's management — these are early indicators of compliance risk, not just audit formalities.

Audit Compliance Thresholds, Deadlines, and Penalties

India's multi-layered audit framework comes with distinct deadlines for each compliance stream. Missing these deadlines attracts penalties at both company and director levels.

Triggering Criteria for Mandatory Audits

| Audit Type | Threshold | Notes |

|---|---|---|

| Statutory Audit | All companies | No exemption regardless of size or turnover |

| Tax Audit | Business turnover > INR 1 crore | INR 10 crore threshold if cash transactions ≤ 5% |

| Tax Audit (Professional) | Gross receipts > INR 50 lakh | Applies to professional services |

| GSTR-9C | Aggregate GST turnover > INR 5 crore | Self-certification available below INR 5 crore |

Sources: Section 139, Companies Act; Section 44AB, Income Tax Act; CBIC Circular

Key Compliance Calendar

| Compliance Item | Deadline | Regulatory Basis |

|---|---|---|

| AGM (statutory audit completion) | Within 6 months of FY-end (Sept 30 for March 31 FY) | Section 96, Companies Act |

| ROC filing (Form AOC-4) | Within 30 days of AGM | Section 137, Companies Act |

| Tax audit report (non-TP cases) | September 30 of assessment year | Form 26 FAQ (one month before ITR due date) |

| Tax audit report (transfer pricing) | October 31 of assessment year | Extended deadline for entities with TP compliance |

| GSTR-9C | December 31 of following FY | Rule 80, CGST Rules |

Critical note: India's financial year runs April 1 to March 31 — a structural difference from Singapore's flexible financial year-end options. Singapore companies must align internal reporting cycles with India's fixed FY when planning consolidation timelines.

Penalties for Non-Compliance

| Violation | Penalty Amount | Statutory Reference |

|---|---|---|

| Failure to obtain tax audit | 0.5% of turnover, max INR 1,50,000 | Section 271B, Income Tax Act |

| Companies Act audit default — Company | INR 25,000 to INR 5,00,000 | Section 147(1), Companies Act |

| Companies Act audit default — Director | INR 10,000 to INR 1,00,000 | Section 147(1), Companies Act |

| Companies Act audit default — Auditor | INR 25,000 to INR 5,00,000; imprisonment up to 1 year if willful | Section 147(2), Companies Act |

| Late GSTR-9/9C filing | INR 200/day, capped at 0.50% of turnover | Section 47, CGST Act |

| Late ROC filing (AOC-4) | INR 10,000 + INR 100/day (company max INR 2,00,000; director max INR 50,000) | Section 137(3), Companies Act |

Critical implication: Non-compliance risk extends personally to Indian-resident directors nominated by Singapore parent companies. Foreign investors often appoint local directors without fully appreciating that these individuals face personal penalties and potential disqualification for compliance failures.

For Singapore parent companies, the practical implication is straightforward: build India's fixed compliance calendar into your group reporting schedule well before deadlines arrive. The director liability provisions alone make reactive compliance — catching up after a missed deadline — a significantly more costly approach than staying ahead of them. VJM Global supports foreign companies with compliance calendar management, deadline tracking, and pre-deadline audit readiness reviews to keep Indian subsidiaries consistently on schedule.

How India's Audit Framework Differs from Singapore's

Understanding structural differences between India's and Singapore's audit ecosystems helps Singapore businesses set realistic expectations and budget appropriately.

Core Structural Differences

| Feature | India | Singapore |

|---|---|---|

| Statutory audit exemption | None — mandatory for all companies | Small company exemption if meeting 2 of 3 criteria: revenue ≤ S$10M, assets ≤ S$10M, ≤ 50 employees |

| Financial year-end | Fixed: March 31 (exceptions require Tribunal approval) | Flexible — companies choose any date |

| Auditing standards | ICAI Standards on Auditing (SA series), aligned with ISAs | Singapore Standards on Auditing (SSAs) issued by ISCA, aligned with ISAs |

| Accounting standards | Ind AS (IFRS-converged) for listed/large companies; AS for others | SFRS(I) (identical to IFRS) for listed; SFRS for others |

| Auditor rotation (individual) | Max 5 consecutive years | No mandatory rotation |

| Auditor rotation (firm) | Max 10 consecutive years (two 5-year terms) | No mandatory rotation |

| Tax audit | Separate mandatory audit above thresholds | No separate tax audit concept |

| GST reconciliation | GSTR-9C mandatory above INR 5 crore | No equivalent requirement |

Sources: Singapore Audit Exemption; India Auditor Rotation

Accounting Standards Alignment and Consolidation Implications

Indian companies follow either:

- Indian Accounting Standards (Ind AS): Converged with IFRS, mandatory for listed companies and unlisted companies with net worth ≥ INR 250 crore

- Accounting Standards (AS): Older standards for companies below Ind AS thresholds

Singapore-listed entities follow SFRS(I), which is identical to IFRS. This creates a consolidation gap: an Indian subsidiary following AS (not Ind AS) prepares financials under a different framework than the Singapore parent's SFRS(I) group accounts.

The Indian audit report expresses an opinion based on Indian GAAP, not SFRS(I). Singapore parent companies must convert or reconcile Indian subsidiary financials to SFRS(I) when preparing group accounts — a process that requires working knowledge of where AS and SFRS(I) diverge.

Auditor Appointment and Rotation

In India, statutory auditors are appointed by shareholders at the AGM, with strict rotation requirements:

- Individual auditors: maximum 5 consecutive years

- Audit firms: maximum 10 consecutive years (two 5-year terms)

- Cooling-off period: 5 years after term completion

Singapore has no equivalent mandatory rotation — firms can retain the same auditor indefinitely. For Singapore businesses with long-term India operations, this distinction matters: mandatory audit firm changes every 5-10 years introduce transition costs, re-onboarding time, and potential continuity risks that need to be planned for.

Frequently Asked Questions

What is audit in India?

Audit in India refers to an independent examination of a company's financial records and statements to verify accuracy and compliance with Indian laws and accounting standards. The audit is conducted by a licensed Chartered Accountant registered with ICAI, following Standards on Auditing aligned with international best practices.

Is audit mandatory in India?

Yes. Statutory audit is mandatory for all companies incorporated in India regardless of size, turnover, or ownership — no small company exemption exists. Additionally, tax audit becomes mandatory when business turnover exceeds INR 1 crore (or INR 10 crore for predominantly digital transactions), and GST reconciliation filing (GSTR-9C) is mandatory for entities with aggregate turnover above INR 5 crore.

What are the 4 types of audit report?

The four audit opinion types are:

- Unqualified (Clean) — financial statements are accurate and compliant

- Qualified — specific material issues exist but are not pervasive

- Adverse — financial statements are materially misstated and unreliable

- Disclaimer — auditor cannot form an opinion due to insufficient evidence or scope limitations

What is the cost of audit in India?

Audit fees vary based on company size, transaction volume, and the CA firm engaged. For foreign-owned subsidiaries, fees are negotiated with the appointed CA and approved by shareholders at the AGM. Bundling statutory, tax, and GST audits with one firm often reduces the overall cost.

What is a CAG report in India?

A CAG (Comptroller and Auditor General) report is a government audit issued by India's constitutional auditor under Article 148, covering public sector entities and government-funded organisations. Singapore-owned private Indian entities are not subject to CAG audit — their statutory auditors are appointed by shareholders under Section 139 of the Companies Act 2013.

Final Takeaway: India's audit framework demands significantly more coordination, documentation, and calendar management than Singapore's single statutory audit cycle. Singapore businesses entering India should engage experienced India-based Chartered Accountants early, establish robust record-keeping systems, and build compliance timelines that account for multiple parallel audit streams. VJM Global has supported Singapore, USA, UK, and Australian businesses in navigating India's audit requirements for 30+ years — helping foreign-owned entities maintain clean audit opinions, meet regulatory deadlines, and produce reliable financials for group-level consolidation.

For audit readiness support or to discuss your specific India compliance requirements, contact VJM Global at info@vjmglobal.com or +91 9213397070.