Introduction

Any Singapore company operating in India through a subsidiary, branch office, or other entity structure is subject to Indian tax laws, including the mandatory tax audit requirement under Section 44AB of the Income Tax Act, 1961. Many Singapore companies underestimate this obligation until they face penalties or scrutiny from Indian tax authorities.

The most common missteps include:

- Assuming the statutory audit also satisfies the tax audit requirement

- Missing transfer pricing documentation deadlines tied to the audit cycle

- Believing India-Singapore DTAA protection removes domestic audit obligations

These assumptions can lead to penalties that are entirely avoidable with the right compliance structure in place. This guide breaks down who the tax audit applies to, how the process works, and what practical compliance looks like for Singapore companies with Indian operations.

Key Takeaways

- Tax audit in India is a mandatory CA-conducted examination for entities crossing specified turnover thresholds

- Applies to Indian subsidiaries and branch offices of Singapore companies—not just domestic firms

- Turnover thresholds: ₹1 crore for most businesses, ₹10 crore for digital/low-cash transactions, ₹50 lakh for professions

- Filing deadline is 30th September, extended to 31st October for transfer pricing cases

- Penalty for non-compliance: 0.5% of turnover or ₹1.5 lakh (lower of the two), with potential loss carry-forward disallowance

What Is a Tax Audit Under Indian Law?

A tax audit is a formal examination and verification of a taxpayer's books of accounts and financial statements by a practising Chartered Accountant. It confirms that income, deductions, and tax positions reported in the Income Tax Return are accurate and compliant with Indian law.

Unlike a statutory audit under the Companies Act — which verifies whether financial statements present a true and fair view — a tax audit focuses exclusively on income tax compliance. It covers turnover figures, expense deductions, depreciation claims, TDS adherence, and other tax-relevant disclosures.

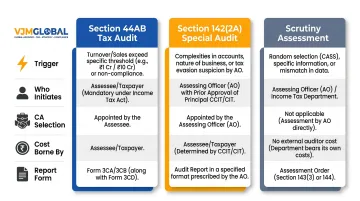

Indian tax law recognizes three distinct proceedings that Singapore companies often confuse with one another:

| Feature | Section 44AB Tax Audit | Section 142(2A) Special Audit | Scrutiny Assessment |

|---|---|---|---|

| Trigger | Turnover/receipts exceed prescribed thresholds | Complexity or doubt about accounts during proceedings | Selection of return for detailed examination |

| Who initiates | Mandatory self-compliance | Assessing Officer (with approval) | Assessing Officer |

| CA selection | Chosen by taxpayer | Nominated by Commissioner | N/A |

| Cost borne by | Taxpayer | Central Government | N/A |

| Report form | Form 3CA/3CB + 3CD | Form 6B | N/A |

The Section 44AB tax audit is a self-initiated compliance requirement triggered by turnover thresholds — not an adversarial or investigative proceeding. For most Singapore companies operating in India through a subsidiary or branch, this is the only audit type they will encounter in routine operations. A special audit or scrutiny assessment only arises if the tax department has specific concerns about a filed return.

Which Singapore Company Structures in India Are Subject to Tax Audit?

Entity Structures and Applicability

Singapore companies typically establish Indian presence through three structures:

Wholly Owned Subsidiary (WOS): Incorporated as an Indian private limited company under the Companies Act 2013. Subject to all Indian tax laws as a domestic company, including Section 44AB. Also requires Companies Act audit under Section 143, meaning Form 3CA applies.

Branch Office: Established with RBI approval under FEMA. Permitted for export/import, professional/consultancy services, research, and IT/software development. Generates taxable income in India and faces identical Section 44AB thresholds as domestic entities. Taxed at 40% plus surcharge and cess (foreign company rate).

Liaison Office: Under FEMA 22(R), expressly barred from commercial, trading, or industrial activity. Cannot earn income in India. Section 44AB is structurally inapplicable to properly operated liaison offices.

Turnover Thresholds

Core thresholds triggering mandatory tax audit:

| Category | Threshold | Condition |

|---|---|---|

| Business (standard) | ₹1 crore | Default for all businesses |

| Business (digital/low-cash) | ₹10 crore | Cash receipts AND cash payments each ≤5% of totals |

| Profession | ₹50 lakh | All professional services |

The 5% cash condition applies only when both receipts and payments in cash do not exceed 5% of total transactions. Non-account-payee cheques or bank drafts are deemed cash transactions under the second proviso.

Singapore companies whose Indian entities engage in consulting, legal, technical advisory, or similar professional services face the significantly lower ₹50 lakh threshold — well below the standard business limit.

Presumptive Taxation Trap

Under Sections 44AD and 44ADA, small entities can opt for presumptive taxation — declaring income at prescribed rates of 8%/6% for business or 50% for professionals, bypassing standard audit requirements.

The trap: if an entity declares profits below these prescribed rates, a tax audit becomes mandatory regardless of turnover. Smaller Singapore-owned Indian entities that try to align reported profits with actual (lower) margins can unknowingly trigger this obligation.

Transfer Pricing Overlay

Indian entities with international transactions — which most Singapore-parented subsidiaries have — fall under transfer pricing provisions (Section 92E). This separately requires a transfer pricing audit with its own requirements:

- Form 3CEB filed by a Chartered Accountant

- Deadline: 31st October (separate from the standard tax audit deadline)

- Documentation covering intercompany service fees, royalties, loans, and any other cross-border transactions

One point that frequently causes confusion: the India-Singapore DTAA (in force since 27 May 1994) contains no exemption from domestic tax audit obligations. Article 25 of the treaty confirms that domestic laws continue to govern taxation. Treaty benefits claimed by a Singapore parent do not relieve the Indian entity of Section 44AB compliance.

How the Indian Tax Audit Process Works: Step by Step

For Singapore companies operating in India, the tax audit follows a defined four-step sequence — and the timeline is tighter than most foreign finance teams expect. Missing any stage can trigger penalties before the October 31 due date.

Step 1: Appoint a Qualified Chartered Accountant

Only a practising CA holding a valid Certificate of Practice can conduct a tax audit. The CA cannot be the same individual or firm that maintains the books of accounts for the entity. Singapore companies should initiate this appointment well before the financial year-end (March 31) to avoid bottlenecks, as most CAs have peak workloads in July–September. Each CA is limited to 60 tax audit assignments per assessment year (excluding presumptive taxation cases).

Step 2: Prepare and Provide Required Financial Records

Core documents required:

- Books of accounts (cash book, ledger, journal, bank statements)

- Sales and purchase invoices

- Stock registers

- TDS returns and reconciliations

- Loan statements

- Fixed asset registers

- Intercompany transaction documentation

For Singapore-owned entities, additionally provide:

- Transfer pricing documentation

- Agreements supporting intercompany pricing

- Master File and Local File (if international transactions exceed ₹1 crore)

- FAR analysis (Functions, Assets, Risks)

Step 3: Conduct the Audit and Reconcile Discrepancies

The CA cross-verifies financial records against filed returns and flags discrepancies for resolution before the report is finalised. Key areas reviewed include:

- GST reconciliation — comparing books against GSTR filings

- TDS compliance — verifying deductions, deposits, and returns

- Advance tax payments — confirming amounts against computed liability

- Disallowable expenses and depreciation — identifying any items requiring adjustment

Any discrepancies are discussed with management for correction or explanation before the report is signed off.

Step 4: Prepare and File the Audit Report

Prescribed forms under current rules:

| Form | Applicability | Content |

|---|---|---|

| Form 3CA | Entities audited under another law (e.g., Companies Act) | Audit report |

| Form 3CB | Entities not audited under another law | Audit report |

| Form 3CD | Accompanies both 3CA and 3CB | Statement of particulars (detailed schedules) |

Singapore WOS entities use Form 3CA because they undergo Companies Act audit. Branch offices use Form 3CB.

Form 26 transition: Under Income Tax Rules 2026, Form 26 replaces Forms 3CA/3CB/3CD for tax years commencing on or after 1 April 2026 (AY 2027-28 onwards). Forms 3CA/3CB/3CD remain applicable for AY 2026-27 and prior.

The CA files the report using their professional login on the Income Tax Portal, after which the taxpayer must accept the report through their own portal login. The date of taxpayer approval is considered the official filing date — making timely internal sign-off as important as the CA's submission itself.

Key Compliance Factors Singapore Companies Must Understand

Due Date Structure

Standard deadlines:

- Tax audit report (Section 44AB): 30th September of the assessment year

- Tax audit report (transfer pricing cases): 31st October of the assessment year

- Income tax return (audit cases): 31st October

- Income tax return (TP cases): 30th November

For entities subject to transfer pricing audit under Section 92E—which applies to virtually all Indian entities of Singapore companies with intercompany transactions—the deadline extends to 31st October. Missing either deadline triggers Section 271B penalties.

Recent extensions: CBDT has extended deadlines in recent years. Plan around statutory deadlines, but factor in that CBDT may grant extensions during technical disruptions or exceptional circumstances.

Financial Year Mismatch

India's financial year runs April 1 to March 31, while Singapore follows a calendar year or company-specific year. Singapore companies must ensure their Indian entity maintains books and closes accounts aligned to the Indian financial year. The Singapore parent's own reporting cycles must not delay provision of intercompany data needed for the Indian audit.

Books of Accounts Requirement

Indian law requires specific books to be maintained in India per Section 44AA. Singapore companies sometimes assume that consolidated accounts prepared under Singapore Financial Reporting Standards are sufficient, but this is incorrect. The Indian entity must maintain India-compliant records independently. The tax auditor reviews these directly — not the Singapore parent's statements.

Required records include:

- Cash book and journal entries

- General ledger

- Bank statements reconciled to Indian accounts

Choosing a Cross-Border Tax Advisor

First-time filers frequently run into missed deadlines, incomplete disclosures, and transfer pricing mismatches — all of which attract penalties. Working with an advisor experienced in Indian compliance for foreign-owned entities, such as VJM Global, helps avoid these pitfalls. VJM Global has supported Singapore and other foreign-owned businesses through Indian tax audit and compliance requirements for over 30 years.

Common Mistakes Singapore Companies Make During Tax Audit

Confusing Statutory Audit with Tax Audit

The most frequent error: assuming the tax audit is the same as or covered by the Indian statutory audit conducted under the Companies Act. While both may be conducted by a CA, they serve different purposes and produce different reports. A Companies Act audit verifies that financial statements present a true and fair view; a tax audit verifies income tax compliance. Both must be completed independently.

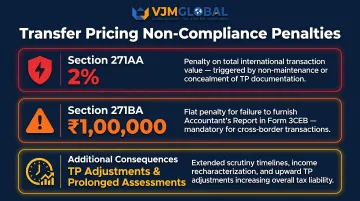

Inadequate Transfer Pricing Documentation

Singapore companies that charge management fees, royalties, or intercompany loans to their Indian entities must maintain an arm's-length pricing study (Form 3CEB) and detailed TP documentation. Tax auditors are required to report on related-party transactions in Form 3CD. Inadequate documentation routinely leads to:

- 2% penalty on transaction value under Section 271AA

- ₹1 lakh penalty for failure to furnish Form 3CEB under Section 271BA

- Prolonged assessment proceedings

- Transfer pricing adjustments

The most common gaps auditors flag include:

- Incomplete FAR (Functions, Assets, Risks) analysis

- Missing benchmarking studies for management fees

- Undocumented intercompany loan terms and interest justification

- Lack of contemporaneous documentation — prepared at the time of the transaction — which must be retained for 8 years

DTAA Misconception

Some Singapore companies assume that India-Singapore DTAA treaty benefits — or the absence of a permanent establishment — exempt their Indian entity from tax audit requirements. They don't. The tax audit obligation is triggered by the Indian entity's own turnover, regardless of any treaty positions taken at the parent level. The DTAA contains no exemption from domestic audit obligations.

Frequently Asked Questions

What is a tax audit in India?

A tax audit is a mandatory examination of a taxpayer's books of accounts and financial statements conducted by a Chartered Accountant under Section 44AB of the Income Tax Act, 1961, to verify the accuracy of income, deductions, and tax compliance reported in the tax return.

What is the purpose of a tax audit in India?

The primary purpose is to verify that financial records are accurate, income and deductions are correctly reported, and the taxpayer complies with Indian tax law. This reduces the scope for errors, misreporting, or fraud in income tax returns.

Who is eligible for a tax audit in India?

Businesses and professionals are the two main categories subject to mandatory tax audit. Entities under presumptive taxation that declare income below the prescribed rate also become liable, regardless of turnover.

How is a tax audit done in India?

The process follows four key steps:

- Appoint a qualified Chartered Accountant and submit books of accounts with supporting documents

- The CA examines, reconciles records, and prepares the audit report (Form 3CA/3CB and Form 3CD, or Form 26 from TY 2026-27)

- The completed report is filed electronically on the Income Tax Portal before the due date

What is the tax audit limit in India?

The turnover threshold is ₹1 crore for businesses — raised to ₹10 crore if cash transactions do not exceed 5% of total transactions. For professionals, the limit is ₹50 lakh in gross receipts.

What is the penalty for tax audit in India?

Under Section 271B, non-compliance attracts a penalty of 0.5% of total turnover or gross receipts, capped at ₹1.5 lakh. Failing to file the audit report can also render the tax return defective, leading to disallowed deductions and potential scrutiny proceedings.