Introduction

A GST audit notice from Indian tax authorities is not something a Singapore business can handle reactively. By the time the notice arrives, the window for clean, voluntary correction has typically closed. A GST audit is the formal examination of a registered entity's tax records, returns, and financial documents — verifying that turnover, taxes paid, Input Tax Credit (ITC), and refund claims comply with the CGST Act, 2017. For Singapore businesses with Indian operations or subsidiaries, the exposure includes penalties, demand orders, and reputational risk with local partners and regulators.

India's GST enforcement environment has become increasingly data-driven. The Business Intelligence and Fraud Analytics (BIFA) system automatically flags return mismatches, abnormal ITC utilisation, and suspicious transaction patterns. Between FY 2021 and FY 2023, the proportion of planned audits actually conducted jumped from 26% to 70%. That pace of expansion means cross-border entities — including Singapore subsidiaries — are no longer low-priority targets.

This guide covers everything Singapore businesses need to know: the legal framework, what triggers an audit, how the process unfolds, and what penalties apply — plus how to keep your Indian entity audit-ready year-round.

Key Takeaways

- GST audit verifies records, returns, and financial documents for compliance — no CA certification required from businesses

- Mandatory CA/CMA audit (Section 35(5)) was scrapped in 2021; turnover above ₹5 crore now requires self-certification via GSTR-9C

- Two authority-initiated audits remain: Departmental Audit (Section 65) and Special Audit (Section 66)

- Singapore businesses face higher scrutiny over ITC mismatches, RCM on imported services, and cross-border inconsistencies

- Non-compliance carries 18% p.a. interest, penalties up to 100% of tax shortfall, and potential legal proceedings

What Is GST Audit in India?

GST audit is the examination of a taxable person's books of accounts, returns, invoices, and related documents to verify correct reporting of taxable turnover, accurate ITC claims, proper tax payment, and overall compliance with the GST Act.

This is distinct from Singapore's domestic GST framework under the Inland Revenue Authority of Singapore (IRAS). India's GST audit operates with different thresholds, timelines, and penalty structures — and the obligations fall directly on your Indian registered entity.

Current Legal Position

The statutory requirement for a CA/CMA-certified audit under Section 35(5) was removed with effect from 1 August 2021 via Finance Act 2021 and CBIC Notification No. 29/2021-Central Tax. This was replaced by a self-certified reconciliation statement in Form GSTR-9C for businesses exceeding ₹5 crore annual aggregate turnover.

In practice, this means three distinct compliance obligations for Singapore businesses with Indian operations:

- Annual return filing (GSTR-9): Mandatory for turnover above ₹2 crore

- Self-reconciliation (GSTR-9C): Self-certified statement for turnover above ₹5 crore

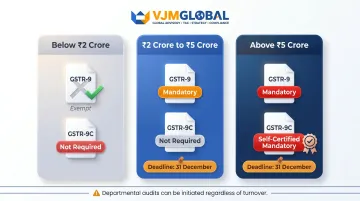

- Ongoing audit risk: Departmental or special audits can be initiated by authorities at any time, regardless of turnover size

This shift from mandatory professional certification to self-certification transfers responsibility and liability directly to the Singapore business or its authorised Indian signatory.

Any errors in the self-certified GSTR-9C — mismatched ITC claims, understated turnover, or incorrect tax payments — can trigger a departmental audit with penalties and interest accruing from the original filing date.

Types of GST Audits Singapore Businesses Should Know

India's GST framework maintains three active audit mechanisms that form a spectrum of scrutiny foreign entities can face. India's GST framework maintains three active audit mechanisms that form a spectrum of scrutiny foreign entities can face. For Singapore businesses — whether operating through a subsidiary, liaison office, or project office — understanding which audit type applies and what triggers it is the first step toward staying compliant.

Departmental Audit (Section 65)

Conducted by the GST Commissioner or an authorised officer, this covers a full financial year or multiple years and is triggered based on risk profiling by the GST authority.

| Procedural Element | Requirement |

|---|---|

| Notice period | Minimum 15 working days via Form GST ADT-01 |

| Completion timeline | 3 months (extendable to 6 months) |

| Findings communication | Form GST ADT-02 within 30 days of conclusion |

| Scope | Verification of turnover, exemptions, tax rates, ITC, and refunds |

| Recovery action | Demand proceedings under Sections 73, 74, or 74A if shortfalls detected |

The departmental audit process requires businesses to make all records available at their place of business. Officers verify documents against filed returns, note discrepancies in audit notes, and provide taxpayers an opportunity to respond before finalising findings.

Special Audit (Section 66)

Initiated by the Assistant Commissioner (with Commissioner approval) when authorities suspect incorrect valuation of supplies or wrongfully availed ITC. This audit is conducted by a CA or CMA nominated by the Commissioner (at government expense) and can be ordered even if a departmental audit was already completed.

- The auditor submits findings via Form GST ADT-04 within 90 days (extendable by another 90 days)

- Can override prior audits, providing no protection from repeat scrutiny

- Commonly triggered by valuation disputes in related-party transactions — a frequent scenario for Singapore subsidiaries transacting with parent entities

Self-Certification and Annual Filing

Turnover-based filing obligations create three tiers:

| Aggregate Turnover | GSTR-9 (Annual Return) | GSTR-9C (Reconciliation) |

|---|---|---|

| Below ₹2 crore | Exempt | Not required |

| ₹2 crore to ₹5 crore | Mandatory by 31 December | Not required |

| Above ₹5 crore | Mandatory by 31 December | Mandatory (self-certified) |

GSTR-9C no longer requires a CA signature. The Singapore business owner or their authorised Indian representative must self-certify it, accepting full responsibility for its accuracy.

Incorrect self-certification attracts penalties up to ₹50,000 under Section 125 of the CGST Act — making accurate reconciliation before filing non-negotiable.

VJM Global's GST compliance services help foreign entities stay audit-ready through ongoing reconciliation, proactive GSTR-9/9C preparation, and internal control reviews that reduce the risk of self-certification errors.

What Triggers a GST Audit: Warning Signs for Singapore Businesses

BIFA Risk Profiling System

The GST portal uses the Business Intelligence and Fraud Analytics (BIFA) system—operated by the Directorate General of Analytics and Risk Management (DGARM)—to identify risky taxpayers through advanced algorithms.

Primary red flags for all businesses:

- GSTR-3B filings show discrepancies against GSTR-2B auto-generated purchase records

- GST-declared turnover differs from income reported in financial statements or income tax returns

- ITC utilisation exceeds 95% of total liability, or ITC claims run 5× higher than cash tax payments

- Turnover spikes or drops sharply without corresponding changes in business activity

These general triggers apply to any registered entity. For Singapore businesses with Indian operations, several additional patterns draw BIFA's attention specifically.

Singapore-Specific Audit Triggers

Reverse Charge Mechanism (RCM) on Imported Services

Under Section 5(3) of the IGST Act, Indian recipients of services from overseas suppliers must pay GST under reverse charge. This applies to common cross-border services:

- Legal and consulting fees from Singapore-based firms

- Software subscriptions and cloud services

- Marketing and advertising services

- Management fees charged by Singapore parent to Indian subsidiary

Gaps in RCM discharge show up immediately when BIFA cross-references service import data against GST filings — making this one of the most commonly flagged issues for foreign-managed entities.

Related-Party Transaction Valuation

Transactions between a Singapore parent and its Indian subsidiary attract heightened scrutiny for transfer pricing and valuation concerns. If management fees, royalties, or service charges appear inconsistent with market rates, authorities may initiate a special audit under Section 66.

ITC Mismatch and the 180-Day Rule

If a Singapore business's Indian entity claims ITC on purchases but the supplier hasn't filed returns, the mismatch is flagged automatically. Under Section 16(2) and Rule 37, ITC must also be reversed if the vendor is not paid within 180 days of invoice date. This rule is frequently missed by foreign-managed entities where intercompany payment cycles run longer than that window.

No Minimum Threshold for Audit Selection

Small subsidiaries and branch offices can be selected for departmental or special audit based purely on data anomalies — aggregate turnover determines annual filing obligations, not audit eligibility. A newly incorporated subsidiary with minimal revenue is just as exposed as a large operation if its return data raises flags.

The GST Audit Process and Documentation Requirements

End-to-End Audit Timeline

- Notice issuance: Form GST ADT-01 with minimum 15 working days' advance notice

- Internal preparation: Reconcile records, identify discrepancies, prepare documents

- Audit examination: At business premises or tax office, typically 3 months (extendable to 6)

- Findings communication: Form GST ADT-02 within 30 days of audit conclusion

- Response period: Taxpayer may submit reply before final demand

- Demand or closure: GST department issues demand under Sections 73/74 for shortfalls, or closes the audit if compliant

Core Documentation Requirements

Singapore businesses must maintain and be ready to produce:

- All GSTR-1, GSTR-3B, GSTR-9, and GSTR-9C filings

- Sales and purchase invoices (including import invoices)

- Input Tax Credit (ITC) claim registers

- Bank reconciliation statements and tax payment challans

- RCM transaction records (especially for imported services)

- E-way bills and stock registers

- Audited financial statements (balance sheet and P&L)

Four Critical Reconciliations

Before any audit, reconcile these four data streams:

- GSTR-1 vs. GSTR-3B: Confirms that sales declared match the tax actually remitted — mismatches here trigger immediate scrutiny

- GSTR-3B vs. GSTR-2B: Validates ITC claims against what suppliers have actually filed — excess claims are a common audit trigger

- GST returns vs. financial statements: Ensures turnover figures are consistent across returns, books, and audited accounts

- E-invoicing data vs. physical invoices: Required for businesses above ₹5 crore turnover — discrepancies signal process gaps

Singapore businesses managing Indian entities remotely are particularly prone to gaps in these reconciliations due to distance, time zones, and reliance on local staff. VJM Global's GST compliance team provides ongoing reconciliation support and monthly return preparation, so records stay audit-ready throughout the year rather than requiring a last-minute scramble before an audit.

Immediate Actions Upon Receiving Audit Notice

- Designate a single point of contact: Appoint a qualified CA or tax advisor in India to manage all communications with the department

- Conduct internal review: Identify and self-correct discrepancies before the audit begins

- Document all responses: Provide written, evidenced replies—not just verbal explanations

- Consider voluntary disclosure: Tax shortfall paid via Form DRC-03 with interest before SCN issuance can eliminate penalties entirely under Section 73

Penalties for GST Non-Compliance in India

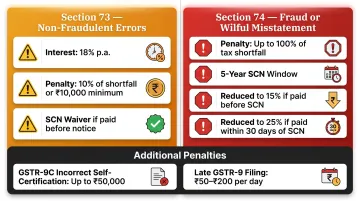

Non-Fraudulent Errors (Section 73)

For genuine mistakes or short payments without intent to evade:

- Tax shortfall: Full amount due

- Interest: 18% per annum from due date until payment

- Penalty: 10% of tax shortfall or ₹10,000 (whichever is higher)

If you pay the shortfall plus interest before a show-cause notice (SCN) is issued, no penalty applies. Payment within 30 days of SCN also waives it.

Fraudulent or Intentional Misreporting (Section 74)

For suppression, fraud, or wilful misstatement:

- Penalty: Up to 100% of tax shortfall plus interest

- SCN timeline: Must be issued at least 6 months before final order deadline (5 years from annual return due date)

- Reduced penalty path: Voluntary payment before SCN reduces penalty to 15%; payment within 30 days of SCN reduces it to 25%

Additional Penalties and Filing Defaults

Beyond Sections 73 and 74, specific filing violations carry their own fixed penalties:

| Violation | Penalty |

|---|---|

| Incorrect GSTR-9C self-certification | Up to ₹50,000 (combined CGST + SGST) — Section 125 CGST Act |

| Late filing of GSTR-9 | ₹50–₹200 per day, capped at 0.04%–0.50% of turnover (size-dependent) — Notification No. 07/2023-Central Tax |

Beyond Financial Penalties: Operational Risk

Singapore businesses face additional consequences:

- GST data flows to the Income Tax Department via Project Insight, potentially triggering follow-on audits

- Your Indian entity's non-compliance disrupts customers' ability to claim ITC on purchases from you

- Poor GST compliance records can block contract approvals, vendor registrations, and regulatory clearances in India

Frequently Asked Questions

What is GST audit in India?

A GST audit is the formal examination of a registered taxpayer's records, returns, and financial documents to verify correct turnover declaration, tax payment, ITC claims, and refund applications under the CGST Act. Three types apply: self-certified (GSTR-9C), departmental (Section 65), or special (Section 66).

What is the procedure for GST audit in India?

The tax authority issues a 15-day advance notice (Form GST ADT-01), examines the taxpayer's books and returns, completes the audit within 3 months (extendable to 6), and communicates findings in Form GST ADT-02. For self-certified compliance, taxpayers file GSTR-9 and GSTR-9C by 31 December of the following year.

What is the GST audit turnover threshold in India?

Businesses with turnover up to ₹2 crore are exempt from filing GSTR-9; those between ₹2–₹5 crore must file GSTR-9 only; those above ₹5 crore must file both GSTR-9 and self-certified GSTR-9C. Departmental or special audits can be initiated for any business regardless of turnover.

Has the GST audit requirement been removed in India?

The mandatory CA/CMA-certified statutory audit under Section 35(5) was removed from 1 August 2021, replaced by self-certification via GSTR-9C. However, departmental audits (Section 65) and special audits (Section 66) can still be initiated by authorities at any time.

What documents does a Singapore business need for a GST audit in India?

Core documents to maintain on an ongoing basis include:

- GSTR-1, GSTR-3B, and GSTR-9/9C filings

- Sales, purchase, and import invoices; ITC registers; RCM records

- Bank statements, tax payment challans, e-way bills, and audited financials

What are the penalties for failing a GST audit in India?

Key penalties include 18% p.a. interest on underpaid tax, a 10% penalty (minimum ₹10,000) for non-fraudulent errors under Section 73, and up to 100% of tax due for fraud under Section 74. Voluntary disclosure before a Show Cause Notice is issued can eliminate penalties entirely.

**Singapore businesses operating in India face real audit exposure** — and the cost of non-compliance compounds quickly through interest, penalties, and regulatory scrutiny. VJM Global has supported foreign entities with Indian GST compliance for over 30 years, from audit-readiness reviews and GSTR-9/9C preparation to representation before tax authorities. Reach out at info@vjmglobal.com or +91-9213397070.