Introduction

UK businesses expanding into the US often arrive expecting audit rules similar to those under the Companies Act — turnover thresholds, employee counts, statutory obligations. What they find instead is a system built on entirely different logic. US federal law imposes no blanket audit requirement on private companies, and that gap creates real compliance blind spots.

The practical reality is that audit obligations still arise — just through different channels. Commercial lenders, private investors, government funding programs, and the UK parent's own consolidated reporting requirements can each independently trigger an audit for a US subsidiary.

Failing to recognize these triggers carries concrete consequences: lost financing opportunities, delayed group reporting, and friction with UK group auditors who expect US subsidiaries to meet consolidation standards.

TLDR: Key Takeaways

- Federal US law doesn't require private companies to conduct annual audits—UK-owned subsidiaries included

- Audits become mandatory when triggered by lenders (typically loans above $4–8 million), investors, federal funding exceeding $750,000, or sector regulations

- Required US audits follow GAAS (Generally Accepted Auditing Standards), not PCAOB rules reserved for public companies

- UK parent companies often require US subsidiaries to undergo GAAS audits to satisfy group auditors and consolidated reporting obligations

- Voluntary audits strengthen credibility with US counterparties and prepare businesses for future growth events

Is the US Audit Framework Different for UK-Owned Private Companies?

No Federal Statutory Mandate

The UK Companies Act requires audits for companies exceeding specific size thresholds: from April 2025, companies must be audited if they exceed at least two of the following—annual turnover above £15 million, balance sheet total above £7.5 million, or more than 50 employees. The US has no equivalent federal mandate. Private companies of any size, including UK-owned subsidiaries, face zero federal statutory audit requirement.

This creates immediate confusion for UK business owners accustomed to automatic compliance triggers. A UK-owned US entity—whether structured as a C-Corporation, LLC, or branch office—is classified as a private company under US law. It therefore falls outside SEC and PCAOB audit requirements, which apply exclusively to publicly traded entities.

Entity Structure and IRS Obligations

Entity structure affects audit exposure in specific ways:

- C-Corporations held by UK parents have distinct reporting obligations compared to LLCs

- Disregarded entities (single-member LLCs treated as branches for tax purposes) have simpler federal filings but face the same audit triggers when commercial circumstances demand it

- IRS Form 5472 reporting creates an indirect audit readiness requirement: foreign-owned US entities must file this form annually to report related-party transactions, and maintaining clean, audit-ready records is essential to satisfy IRS scrutiny—even without a formal audit mandate

VJM Global assists UK-owned US entities with Form 5472 preparation and intercompany record-keeping, helping clients avoid the $25,000 penalties for non-compliance while ensuring transaction documentation meets both IRS and potential auditor standards.

State-Level Variation

Certain US states impose audit or financial reporting requirements based on industry or regulated activity:

- California nonprofits receiving gross revenue of $2 million or more must undergo independent audits under Government Code 12586

- New York charitable organizations with revenue exceeding $1 million face audit requirements under the Nonprofit Revitalization Act

- Insurance companies in states adopting the NAIC Model Audit Rule must submit annual audited financial statements regardless of size

UK owners operating in regulated sectors should confirm state-specific obligations with a US-qualified CPA — requirements vary significantly by industry and revenue level.

When Is an Audit Required for a UK-Owned US Private Company?

Lender Requirements

US banks and commercial lenders typically require audited financial statements when loan amounts exceed $4–8 million. This threshold varies by institution, but UK owners seeking US commercial financing should anticipate audit requirements as near-certain above this range. Lenders use audited statements to verify creditworthiness, assess risk, and satisfy their own regulatory obligations.

Investor and Shareholder Conditions

Private equity firms, venture capitalists, and angel investors routinely include audit clauses in shareholder agreements. UK parent companies also frequently require their US subsidiaries to produce annual audited US GAAP financials for inclusion in consolidated group accounts. This internal group requirement—driven by UK Companies Act consolidation rules—is one of the most common and overlooked audit triggers for UK-owned entities.

Mergers, Acquisitions, and Due Diligence

When a UK-owned US company is sold, restructured, or acquiring another business, buyers demand 2–3 years of audited US GAAP financials as standard due diligence. This requirement also applies when the UK parent itself undergoes a transaction requiring verified subsidiary data. Without that audit history, companies face deal delays, valuation write-downs, or collapsed transactions entirely.

Federal Grants and Government Contracts

US entities receiving federal funding of $1,000,000 or more in a fiscal year fall under the Single Audit Act (updated threshold effective October 2024, increased from $750,000). State-level grants may carry lower thresholds. This is particularly relevant for UK-owned US nonprofits, research entities, or contractors engaged in government-funded projects.

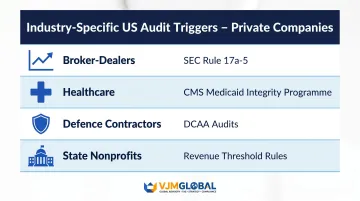

Industry-Specific and Regulatory Triggers

Certain US industries impose sector-level audit requirements regardless of private status:

- Broker-dealers must comply with SEC Rule 17a-5, requiring annual audited financial reports

- Healthcare organisations participating in Medicare or Medicaid programmes face audit requirements under CMS Medicaid Integrity Programme rules

- Defence contractors undergo DCAA (Defense Contract Audit Agency) incurred cost and forward pricing audits

- Nonprofits in regulated states face mandatory independent audits based on revenue thresholds

For UK owners in these sectors, the starting assumption should be that an audit is required — confirming an exemption takes less time than discovering a missed obligation mid-deal or mid-funding cycle.

Applicable Auditing Standards for UK-Owned US Private Companies

Auditing Under GAAS vs. PCAOB

When a US private company audit is required, it's conducted under GAAS (Generally Accepted Auditing Standards) issued by the AICPA's Auditing Standards Board—not PCAOB standards mandated by Congress for publicly traded companies. GAAS audits are generally less exhaustive and less costly than PCAOB audits.

GAAS audits cover:

- Planning and risk assessment

- Internal control evaluation

- Substantive testing of financial statements

- Issuance of an independent auditor's opinion

This provides the assurance that US lenders, investors, and UK parent auditors typically need.

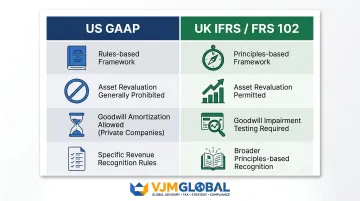

US GAAP vs. UK IFRS/FRS 102: The Reconciliation Challenge

US private companies prepare financial statements in accordance with US GAAP (maintained by FASB), whilst UK parent companies typically report under IFRS or FRS 102. This creates a reconciliation burden: the US subsidiary's GAAP financials must be translated or reconciled for inclusion in UK consolidated group accounts.

Key differences between US GAAP and UK standards:

- US GAAP is rules-based with detailed guidance; UK IFRS/FRS 102 is principles-based

- Asset revaluation is permitted under IFRS but generally prohibited under US GAAP

- Revenue recognition timing and methods differ across frameworks

- Goodwill treatment varies (US GAAP allows amortization for private companies; IFRS requires impairment testing)

The FASB Private Company Council (PCC) offers GAAP simplifications that can reduce compliance costs without affecting audit acceptability. These include:

- Goodwill amortization instead of annual impairment testing

- Simplified treatment of intangible assets in business combinations

- Reduced hedge accounting complexity

UK parent companies should factor these elections into their US subsidiary's accounting setup from the outset.

The Dual Compliance Challenge: Meeting UK and US Requirements Simultaneously

UK Group Reporting Obligations Don't Disappear

Under the Companies Act 2006 (sections 399 and 405), UK parent companies must produce consolidated accounts that include all subsidiaries—including US entities. This means UK auditors will scrutinise the US subsidiary's financials even if those financials weren't independently audited under US GAAS. The result: US subsidiary audits are frequently required not by US law, but by UK group reporting obligations.

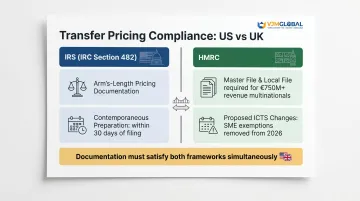

Transfer Pricing and Intercompany Transactions

UK-owned US entities engaged in intercompany transactions—services, royalties, goods, loans—must maintain contemporaneous documentation under both IRS transfer pricing rules (IRC Section 482) and HMRC requirements. These records are central to any audit, and failure to maintain them creates risk on both sides of the Atlantic.

Key compliance requirements:

- IRS: Arm's-length pricing documentation, contemporaneous preparation (within 30 days of filing)

- HMRC: Master file and local file for multinationals with €750 million+ revenue; proposed International Connected Transaction Services (ICTS) changes may remove SME exemptions from 2026

Maintaining audit-ready records that satisfy IRS, HMRC, and auditor expectations simultaneously requires documentation built for both frameworks from the outset — not retrofitted at audit time. VJM Global's transfer pricing documentation services cover both jurisdictions with this dual-standard approach.

Practical Planning Implications

UK businesses should work with advisers who understand both audit frameworks to map out which obligations are triggered and in what sequence. A common mistake is assuming UK-compliant reporting satisfies US lenders — or that US-compliant reporting satisfies UK group auditors. It rarely does. The two frameworks answer to different stakeholders and carry different evidentiary standards, so early planning prevents costly remediation later.

Why UK-Owned US Companies Often Choose Voluntary Audits

Credibility with US Counterparties

Even when not legally required, audited financials strengthen a UK-owned company's position when negotiating with US banks, suppliers, enterprise clients, or joint venture partners. Research from Cogent Business & Management demonstrates that firms with audited statements have better access to formal credit. US counterparties are accustomed to evaluating audited statements and assign higher trust to companies that proactively produce them.

Preparing for Future Growth Events

UK-owned US entities planning to raise US capital, pursue acquisitions, go public, or expand through franchising should treat voluntary audits as an investment in readiness. Buyers and underwriters typically require 2–3 years of audit history—meaning a company that starts auditing early is better positioned when a transaction opportunity arises.

Expert Support for Cross-Border Compliance

Navigating the overlap between US GAAS requirements and UK group reporting obligations is rarely straightforward. Without coordinated guidance, gaps can emerge between what US auditors require and what UK group auditors expect.

VJM Global's team of CPAs and compliance professionals—with experience serving 250+ UK businesses—helps UK-owned entities manage these obligations in parallel. Key areas covered include:

- Transfer pricing documentation aligned to both jurisdictions

- Form 5472 filings and US federal reporting requirements

- Consolidated reporting obligations for the UK parent group

Frequently Asked Questions

Do private companies need to be audited in the USA?

No federal law requires private US companies to undergo annual audits. However, audits are often triggered by commercial lenders, private investors, government funding requirements, or contractual obligations. Most active private businesses encounter audit requirements at some stage as a result.

When must a private company be audited?

Common triggers include bank loans above lender thresholds (typically $4–8 million), investor or shareholder agreement conditions, federal funding exceeding $750,000 under the Single Audit Act, M&A due diligence, and specific industry or state-level regulations.

What auditing standards apply to private companies?

Private company audits in the US are conducted under GAAS (Generally Accepted Auditing Standards) set by the AICPA, and financial statements must be prepared in accordance with US GAAP—distinguishing this from PCAOB standards, which apply only to publicly traded companies.

Does a UK parent company's audit obligation extend to its US subsidiary?

Whilst US law doesn't automatically require the subsidiary to be audited, UK group reporting obligations under the Companies Act typically require consolidated accounts that include the US subsidiary. UK parent auditors will review subsidiary financials as part of this process, which often makes a US GAAS audit a practical necessity.

Can a UK-owned US company use IFRS instead of US GAAP for its US audit?

US private companies are generally expected to use US GAAP for audited statements. Whilst IFRS isn't prohibited, most US lenders and investors require US GAAP — so UK owners typically maintain two sets of financials or prepare a GAAP-to-IFRS reconciliation for group reporting.

What type of auditor should a UK-owned US private company hire?

The auditor must be a licensed CPA registered in the relevant US state and qualified to conduct GAAS audits. For UK-owned entities, a firm with cross-border experience in both US GAAS and UK reporting standards reduces reconciliation complexity and ensures the audit meets requirements on both sides.