Introduction

The United States remains the world's most lucrative consumer market, with GDP exceeding $28 trillion in 2024 (roughly £22 trillion). For UK businesses seeking growth beyond domestic borders—particularly in the post-Brexit landscape—establishing a US subsidiary has become an increasingly strategic move. UK outward FDI stock in the US reached £529.9 billion at the end of 2024, representing 28.5% of total UK overseas investment.

This guide is for UK business owners, directors, and expansion managers exploring a permanent, legally structured US presence. Getting your setup right from the start determines whether you'll enjoy liability protection, favourable tax treaty treatment, and seamless US banking access — or face costly restructuring later.

We cover structural choices between C-Corporations and LLCs, a step-by-step incorporation process tailored to UK businesses, and the dual-jurisdiction tax obligations that require specialist planning.

TL;DR

- A US subsidiary is a separate legal entity incorporated in the United States and owned by your UK parent company

- C-Corporations are typically preferred for UK ownership — LLCs can create tax transparency mismatches under the UK-US treaty

- Setup spans 4-8 weeks, covering state incorporation, EIN, registered agent, US banking, and tax registration

- UK parent companies face dual obligations: US federal/state filings and HMRC's Controlled Foreign Company (CFC) reporting

- Transfer pricing documentation is required from day one — intercompany transactions between the UK parent and US subsidiary must be at arm's length

What Is a US Subsidiary and Why UK Businesses Open One

A US subsidiary is a distinct legal entity registered in the United States, majority-owned or wholly owned by your UK parent company. It operates under US law and is treated separately from the parent for both legal and tax purposes. This separation creates what's known as a "corporate veil," shielding your UK assets from any US liabilities.

Several practical advantages drive UK businesses toward this structure rather than simpler alternatives:

- US customers and partners strongly prefer dealing with US-registered entities over foreign branches

- Hiring American staff, sponsoring visas, and running US payroll all require a domestic legal entity

- Most US banks won't open business accounts without a locally registered company

- Creditors of the US entity cannot pursue the UK parent's assets, limiting your exposure to capital invested in the subsidiary

- The UK-US Double Taxation Convention reduces withholding tax on dividends from 30% to 5–15% depending on your ownership percentage

Subsidiary vs. Branch Office

A branch is not a separate legal entity. It is an extension of your UK parent company, which means the parent bears direct liability for all branch obligations and any US litigation can expose UK assets. A subsidiary creates legal separation, limiting your risk to the capital invested in the US entity. For most UK businesses, this liability shield makes subsidiaries the preferred structure despite the additional compliance requirements.

LLC vs. C-Corp: Choosing the Right Business Structure

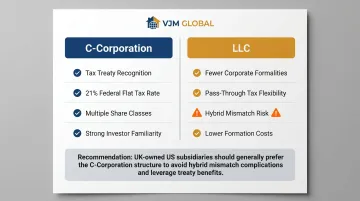

UK-owned US subsidiaries typically choose between two entity types: the C-Corporation (C-Corp) and the Limited Liability Company (LLC). S-Corporations are unavailable because IRS rules prohibit non-resident alien shareholders.

C-Corporation

Why C-Corps dominate for UK ownership:

- Explicitly recognised under the UK-US tax treaty, enabling straightforward dividend repatriation with reduced withholding rates (5% or 15% depending on shareholding)

- Familiar to US investors, lenders, and partners—governance expectations are well understood

- Federal corporate tax sits at 21%; dividends to the UK parent face a statutory 30% withholding rate, reduced by the treaty

- Supports multiple share classes, making future fundraising or equity restructuring straightforward

The tax flow is predictable: net profits taxed at 21% federally, then dividends taxed at 30% statutory rate (reduced to 5% under the treaty if the UK parent holds 10%+ voting shares, or 15% for portfolio holdings).

Limited Liability Company (LLC)

LLC advantages:

- Fewer governance formalities (no board of directors required)

- Pass-through taxation flexibility in the US

- Lower formation and annual compliance costs

The critical UK-US mismatch risk:

Under US tax law, most LLCs are treated as "transparent" entities—profits pass through to owners without entity-level tax. However, HMRC may not recognise this transparency, potentially treating the LLC as an opaque foreign company. This creates a hybrid entity mismatch where:

- The US doesn't tax the LLC at entity level

- HMRC treats it as a taxable foreign company

- You face unexpected double taxation or lose treaty benefits entirely

An LLC can still work — for example, if the UK parent elects to treat the LLC as a corporation for UK tax purposes. Without that election, the hybrid mismatch risk is real. Model both scenarios with a cross-border tax adviser before committing to this structure.

Choosing Your State of Incorporation

Incorporation is a state-level process. The two main options are:

Delaware:

- More than 66% of Fortune 500 companies and 81.4% of US-based IPOs in 2024 chose Delaware

- Predictable corporate law via the Court of Chancery (225+ years of case precedent)

- Privacy-friendly filings and low formation costs (typically $90 filing fee plus $175 minimum annual franchise tax)

- Established infrastructure for foreign-owned entities

If you'll operate in a single US state from day one, incorporating there directly may be simpler.

Operating state (e.g., California, Texas, New York):

- Incorporate where you'll physically operate to avoid "foreign qualification" (registering in two states)

- May face higher taxes (California charges $800/year minimum franchise tax) but simplifies compliance

If you incorporate in Delaware but operate in California, you must foreign qualify in California—filing certificates of authority, appointing a registered agent, and paying fees in both states. For most UK businesses, Delaware incorporation makes sense only if you plan multi-state operations or future venture funding.

How to Open a US Subsidiary: Step-by-Step for UK Businesses

The process typically takes 4-8 weeks from board resolution to operational bank account. UK-side authorisations and US-side filings run in parallel, so starting both tracks simultaneously keeps the timeline on schedule.

Step 1: Pass a Board Resolution in the UK

Before any US registration begins, your UK parent company's board must formally authorise the creation of the US subsidiary. Document this in a board resolution that includes:

- The purpose and strategic rationale for the subsidiary

- Authorised capital investment

- Appointed directors or officers for the US entity

- Authority to execute formation documents

Review your UK company's articles of association to confirm this authority exists and complies with UK Companies Act requirements.

Step 2: Choose Entity Type and State, Then File Formation Documents

Submit your formation documents to the Secretary of State in your chosen state:

- For C-Corps: Articles of Incorporation (also called Certificate of Incorporation) containing:

- Company name (must include "Corporation," "Incorporated," "Corp.," or "Inc.")

- Registered agent name and in-state address

- Authorised share structure (number and class of shares)

- Incorporator details

- For LLCs: Articles of Organisation containing:

- Company name (must include "Limited Liability Company" or "LLC")

- Registered agent details

- Management structure (member-managed or manager-managed)

Delaware processing typically completes within 24-48 hours for standard filings. Most states offer expedited processing for additional fees.

Step 3: Appoint a Registered Agent

Every US state requires a registered agent with a physical in-state address to receive legal and government correspondence. For UK businesses without a US address, commercial registered agent services are available in every state:

- Budget providers: from £40/year

- Typical market range: £80-£240/year

- Premium services: up to £240+/year

Your registered agent ensures you receive important notices (tax forms, compliance deadlines, and legal summons) without maintaining a permanent US office.

Step 4: Obtain a Federal Employer Identification Number (EIN)

The EIN is a 9-digit number issued by the IRS, required for tax filings, hiring employees, and opening a US bank account.

UK companies without a US-based "responsible party" cannot apply for an EIN online. You must apply by one of three methods:

- Telephone: Call 267-941-1099 (Monday-Friday, 6am-11pm ET) for immediate issuance

- Fax: Send Form SS-4 to 304-707-9471—takes approximately 4 business days

- Mail: Post to IRS Cincinnati—takes approximately 4 weeks

The phone route is fastest, though you'll need to call during US business hours. Start this step early — EIN delays push back every step that follows.

Step 5: Open a US Business Bank Account

This step presents the biggest challenge for UK businesses. US banks enforce strict Know Your Customer (KYC) requirements under FinCEN's Customer Due Diligence Rule, and most require at least one company officer to appear in person at a US branch.

Required documentation typically includes:

- EIN confirmation letter

- Articles of Incorporation

- Operating agreement or bylaws

- Beneficial ownership information (any individual owning 25%+ of the entity)

- Two forms of photo ID for beneficial owners

- Personal proof of address

- US business address

Alternatives for remote account opening:

- International banks with US presence: HSBC and Barclays US may enable remote onboarding for existing UK clients

- Online banks and neobanks: Emerging fintech providers accept non-resident applications with EIN and passport verification

- Multi-currency platforms: Some offer business accounts without traditional branch requirements

Bank account opening typically takes 3 weeks after EIN receipt. Schedule any required in-person visits alongside initial US site visits to avoid separate trips.

Step 6: Register for State and Local Taxes and Obtain Licences

After securing banking, complete these registrations:

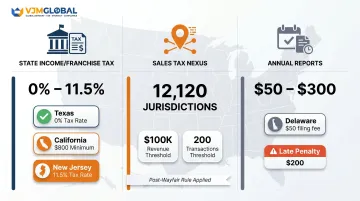

State income/franchise tax: Register with your state's Department of Revenue. California, for example, charges $800/year minimum franchise tax regardless of profitability.

Sales tax: If selling goods or services to US end-users, register for sales tax collection. Post-Wayfair, economic nexus rules apply in all 46 states with sales tax—even without physical presence, exceeding revenue or transaction thresholds triggers registration obligations.

Payroll taxes: If hiring US staff, register for federal and state payroll tax withholding, unemployment insurance, and workers' compensation.

Industry licences: Healthcare, finance, food service, and technology sectors often require additional federal or state licences. Consult a US attorney for industry-specific requirements.

Tax and Compliance Obligations for UK-Owned US Subsidiaries

Managing a UK-owned US subsidiary means running two parallel compliance tracks simultaneously. Your US subsidiary faces federal and state-level obligations, while your UK parent carries its own HMRC reporting duties—and the two interact directly through transfer pricing rules, CFC provisions, and treaty claims.

US Federal Tax Obligations

Corporate income tax:

- 21% flat rate on net taxable income

- Filed annually on Form 1120, U.S. Corporation Income Tax Return

- Due by the 15th day of the 4th month after year-end (April 15 for calendar-year corporations)

Dividend withholding tax:

- Default statutory rate: 30% on dividends paid to foreign shareholders

- UK-US treaty rate: 5% if UK parent holds 10%+ voting shares; 15% for portfolio holdings

- Treaty claims filed via IRS Form W-8BEN-E (for entities)

Transfer pricing compliance:

IRS Section 482 requires that all intercompany transactions—royalties, service fees, loans, goods—be priced at "arm's length" as if between unrelated parties. You must:

- Document the methodology used to price intercompany transactions

- Maintain contemporaneous transfer pricing studies (prepared at the time of the transaction, not retroactively)

- File Form 5471 (Information Return of U.S. Persons With Respect to Certain Foreign Corporations) if applicable

VJM Global supports OECD-aligned transfer pricing documentation—including Master Files and Local Files—for audit readiness across both IRS and HMRC standards.

State-Level Tax Obligations

Each state where your subsidiary has "nexus"—meaning physical presence or surpassing economic thresholds—triggers separate obligations:

- State income/franchise taxes: Rates vary from 0% (Texas, Nevada) to 11.5% (New Jersey). California imposes an $800 minimum franchise tax annually, even on loss-making companies.

- Sales tax collection: With 12,120 sales and use tax jurisdictions across the US, foreign sellers must assess economic nexus state-by-state. Typical thresholds are $100,000 in annual sales or 200 transactions.

- Annual reports: Most states require annual reports with fees ranging from $50–$300. Delaware charges $50 for domestic corporations with a $200 penalty for late filing.

UK-Side Obligations (HMRC and CFC Rules)

When a UK company owns a foreign subsidiary, HMRC's Controlled Foreign Company (CFC) rules may apply. These anti-avoidance provisions target profit diversion to low-tax jurisdictions.

Practical application for US subsidiaries:

The US federal rate of 21% is close to the UK's 25% main corporation tax rate. In practice, a US subsidiary paying 21% federal tax (plus applicable state taxes) generally avoids punitive CFC charges, provided:

- The subsidiary has genuine commercial substance (real operations, employees, assets)

- Profits are not artificially diverted from the UK through transfer pricing manipulation

- The UK parent documents the commercial rationale for the US structure

Ongoing UK reporting:

- Report the subsidiary's existence to HMRC

- Include in consolidated UK accounts if applicable

- Claim foreign tax credit relief for US taxes paid to avoid double taxation

- Maintain documentation supporting treaty claims

VJM Global's international tax team works with UK parent companies on CFC compliance, treaty claim documentation, and cross-border financial reporting.

Ongoing Compliance Requirements

To maintain your subsidiary's legal standing and liability protection:

Corporate formalities:

- Hold and document annual board meetings

- Maintain separate bank accounts (never commingle UK and US funds)

- Document all intercompany agreements in writing

- Update registered agent and state filings when addresses change

Each of these formalities ties directly to a set of recurring filing deadlines:

Recurring filings:

- Federal Form 1120 (annual corporate tax return)

- State income/franchise tax returns (annual or quarterly)

- State annual reports (typically due at incorporation anniversary)

- Payroll tax returns (quarterly federal Form 941 if hiring US staff)

- Sales tax returns (monthly or quarterly in registered states)

Failure to maintain formalities can result in "piercing the corporate veil"—courts may hold the UK parent directly liable for subsidiary debts, eliminating your liability protection.

Common Mistakes UK Businesses Make When Setting Up in the USA

Mistake 1: Choosing LLC Without Cross-Border Tax Advice

Many UK owners assume an LLC is simpler and therefore better, without realising the tax transparency mismatch between UK and US treatment. The US treats most LLCs as pass-through entities (no entity-level tax), but HMRC may not recognise this transparency under UK law. This creates hybrid entity treatment where:

- The US doesn't tax the LLC

- HMRC treats it as an opaque foreign company

- The UK parent faces unexpected tax exposure

Solution: Always obtain specialist cross-border tax advice before assuming an LLC is the right structure. VJM Global's international tax practitioners can map out UK and US implications for your specific ownership structure and profit repatriation plans.

Mistake 2: Underestimating the Bank Account Timeline

Because most US banks require in-person verification, UK businesses that don't plan for this step often delay their entire operational launch. The EIN-to-banking timeline averages 3 weeks, but can extend to 6-8 weeks if documentation is incomplete or multiple bank rejections occur.

Solution: Schedule your bank account visit early, ideally coordinating it with an initial US site visit or market research trip. Prepare all KYC documentation in advance and consider online bank alternatives if in-person visits aren't feasible.

Mistake 3: Ignoring State Nexus and Sales Tax Obligations

UK businesses often focus on federal compliance and overlook the patchwork of state-level obligations. Following the Wayfair Supreme Court decision, economic nexus rules mean that selling remotely into a state—even without physical presence—can trigger sales tax registration.

With 12,120 sales tax jurisdictions and 588 rate changes during 2024 alone, compliance complexity escalates rapidly for businesses selling across multiple states.

Failure to register and collect sales tax exposes you to back-tax assessments, penalties, and interest—often with no statute of limitations.

Solution: Conduct a nexus study before launching sales operations to identify registration obligations state by state. Working with a cross-border tax team to monitor nexus thresholds and manage multi-state filings — as VJM Global's US compliance specialists do for UK clients — significantly reduces the risk of costly back-assessments.

Frequently Asked Questions

How to open a subsidiary in the USA?

UK businesses typically incorporate as a C-Corp, file Articles of Incorporation, obtain an EIN from the IRS, open a US bank account, and register for federal and state taxes. The full process—from board resolution to operational readiness—takes 4-8 weeks.

Do subsidiaries pay taxes?

Yes, US subsidiaries pay 21% federal corporate income tax on net profits, state taxes (which vary by state), and withholding tax on dividends remitted to the UK parent. The UK-US tax treaty reduces dividend withholding from 30% to 5-15% depending on the parent's ownership percentage.

Can an LLC own a subsidiary?

Yes, but UK parent companies face significant tax complications. The UK and US treat LLC transparency differently, which can result in double taxation or loss of treaty benefits. Specialist cross-border tax advice is essential before choosing this structure.

What is a US subsidiary?

A US subsidiary is a separate legal entity incorporated in the United States and owned by a foreign parent company. It shields the parent from US liabilities while enabling a permanent local presence, US banking access, and the ability to hire local staff under US employment law.

What is the difference between a branch office and a subsidiary in the USA?

A branch is an extension of the UK parent company (not a separate legal entity), meaning the parent bears direct US liability for all branch obligations. A subsidiary is a distinct legal entity offering liability protection—creditors generally cannot pursue the UK parent's assets—and provides a more credible local presence for US customers and partners.

How long does it take to open a US subsidiary from the UK?

Basic incorporation takes 1-2 weeks, but the full process—covering EIN issuance, bank account opening, and state tax registration—typically runs 4-8 weeks. Non-US applicants should account for longer IRS processing times.

Have questions about cross-border compliance for your US expansion? VJM Global's team of CPAs and international tax professionals has supported 250+ UK businesses with multi-jurisdiction tax filings, HMRC reporting, and international compliance over 30+ years.

Contact VJM Global at info@vjmglobal.com or call +91 9213397070 to discuss your requirements.