Introduction

The UK ecommerce market generated approximately £128.97 billion in 2024, cementing its position as the 4th largest ecommerce market globally. Yet behind this explosive growth lies a challenge many online sellers struggle with: managing finances across multiple sales channels while staying compliant with HMRC obligations.

If you're selling on Amazon, eBay, Shopify, and Etsy simultaneously, you're juggling different fee structures, payout timings, VAT thresholds, and reporting formats that all need reconciling into one accurate set of books.

Add post-Brexit VAT rules, Making Tax Digital (MTD) mandates, and inventory tracking complexities, and the burden adds up fast. The average UK small business spends 44 hours and £4,500 per year on tax compliance alone.

This guide covers what makes ecommerce bookkeeping unique, what to track, UK VAT and tax rules, software options, common mistakes, and when to seek professional help.

Key Takeaways

- Ecommerce bookkeeping means recording sales, expenses, refunds, and fees across every platform you sell on

- VAT registration is mandatory once taxable turnover exceeds £90,000; MTD rules require compatible software

- Track five core pillars: sales revenue, cost of goods sold (COGS), operating expenses, inventory, and returns

- Cloud-based accounting software integrated with your sales platforms cuts manual data entry and reduces errors

- Outsourcing to specialists like VJM Global, which has supported 250+ UK businesses, ensures compliance and frees time for growth

Why Ecommerce Bookkeeping is Different from Traditional Bookkeeping

Multi-Channel Complexity

Unlike a traditional business with one income stream, ecommerce sellers receive payouts from Amazon, eBay, Shopify, Etsy, and other platforms. Each has its own:

- Fee structure (listing fees, transaction fees, referral fees)

- Payout timing (weekly, biweekly, monthly)

- Reporting format (different CSV exports, APIs, settlement reports)

Shopify leads UK ecommerce adoption with 239,051 websites, compared to 174,183 using WooCommerce. Sellers on three or more platforms can face hundreds of transactions each month — all of which need reconciling into one clean set of books.

Unique Financial Events

Ecommerce transactions include events rarely seen in traditional businesses:

- Platform seller fees deducted before payout

- Payment processor charges from Stripe, PayPal, Klarna

- Frequent returns and refunds that affect both revenue and VAT

- Multi-currency transactions requiring exchange rate tracking

These complexities mean spreadsheet-based approaches quickly become unmanageable. The sections below cover the tools, processes, and compliance requirements that keep UK ecommerce books accurate and audit-ready.

What to Track in Your UK Ecommerce Books

What to Track in Your UK Ecommerce Books

Accurate books start with knowing exactly what to record — and where. These five categories cover the core of what UK ecommerce sellers need to track consistently.

Sales Revenue

Record every sale across every channel, capturing gross sales value rather than just the net payout. Each transaction should include:

- Date of sale

- Platform (Amazon, Shopify, eBay)

- Amount (before fees)

- Payment method

Many sellers mistakenly record only what hits their bank account, but HMRC requires gross revenue reporting for accurate VAT calculations.

Cost of Goods Sold (COGS)

COGS = Opening Inventory + Purchases – Closing Inventory

Track COGS separately from operating expenses to calculate true gross profit. For businesses holding physical stock, getting this right directly affects:

- Profit margin visibility

- Tax liability calculations

- Pricing decisions

Operating Expenses

Most day-to-day running costs qualify as tax-deductible expenses — but only if they're correctly categorised. Common UK ecommerce examples include:

- Platform subscription fees (Shopify, Amazon Professional)

- Advertising spend (Google Ads, Facebook, TikTok)

- Shipping and packaging materials

- Warehousing and fulfilment costs

- Software tools (inventory management, A2X, email marketing)

- Professional services (accounting fees, legal advice)

Miscategorising these — or lumping them under a catch-all — is one of the most common triggers for HMRC queries.

Inventory

Track inventory by:

- Quantity on hand at any given time

- Purchase cost per unit (including shipping and import duties)

Accurate inventory records are needed for:

- Correct COGS calculation

- Cash flow management (avoiding overstock and stockouts)

- VAT compliance (stock values affect Balance Sheet reporting)

Once your core records are in order, you also need a consistent approach to adjustments and deductions.

Returns, Refunds, and Platform Fees

For returns and refunds:

- Deduct from revenue (not recorded as expenses)

- Update inventory quantities accordingly

- Adjust VAT liability on your VAT return

For platform fees:

- Record separately from sales — don't just net them off the payout

- Categorise by fee type (referral fees, FBA fees, subscription fees)

- Accurate fee records are essential for true margin analysis

VAT and Tax Compliance for UK Ecommerce Businesses

VAT rules, post-Brexit cross-border obligations, and the rollout of Making Tax Digital (MTD) make compliance one of the most layered challenges for UK ecommerce businesses. Here's what you need to know.

VAT Registration Threshold

The UK VAT registration threshold is £90,000 in taxable turnover over the previous 12 months, effective since 1 April 2024. The deregistration threshold is £88,000.

How it works:

- You must register if turnover in the last 12 months exceeds £90,000

- You must also register if you expect turnover to exceed £90,000 in the next 30 days alone

- Registration must occur within 30 days of the end of the month in which the threshold was exceeded

- Voluntary registration below the threshold allows you to reclaim input VAT

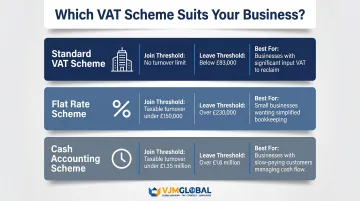

VAT Accounting Schemes

| Scheme | Turnover to Join | Turnover to Leave | Best For |

|---|---|---|---|

| Standard | Any | Any | Larger businesses, high input VAT costs |

| Flat Rate | £150,000 or less | Over £230,000 | Smaller sellers with low input costs |

| Cash Accounting | £1.35 million or less | Over £1.6 million | Businesses with longer payment cycles |

Flat Rate Scheme: Pay a fixed percentage of gross turnover (varies by sector). Simpler but limits input VAT recovery.

Cash Accounting Scheme: Account for VAT when you receive or make payment — not when the invoice is issued. This eases cash flow for businesses that invoice ahead of receiving funds.

International VAT and Post-Brexit Rules

Import One Stop Shop (IOSS)

UK sellers can register for IOSS to report and pay VAT on goods imported in consignments valued at £135 or less sold to EU or Northern Ireland consumers.

Key requirements:

- Must be registered for UK VAT first

- Submit monthly IOSS VAT returns to HMRC

- Receive unique 12-digit IOSS VAT identification number for customs declarations

- Watch for: The EU plans to remove the €150 IOSS consignment limit by approximately March 2028, after which all import B2C consignment VAT must be charged at point of sale

Postponed VAT Accounting (PVA)

Any UK VAT-registered business can use PVA to declare and recover import VAT on the same VAT Return, rather than paying upfront at the border.

How it works:

- Elect PVA on the customs declaration (no prior approval needed)

- Download your Monthly Postponed Import VAT Statement (MPIVS) from the Customs Declaration Service

- Enter on VAT Return: Box 1 (import VAT due), Box 4 (input VAT reclaimed if eligible), Box 7 (value of imports excluding VAT)

Export Zero-Rating

Goods exported from the UK are zero-rated for VAT, provided you hold acceptable evidence of export obtained within 3 months of the time of supply.

Acceptable evidence includes:

- Official export declarations via Customs Declaration Service (with Movement Reference Number)

- Commercial transport documents (air waybills, bills of lading, CMR notes)

Retain all records for 6 years.

Beyond VAT mechanics, HMRC's Making Tax Digital programme is reshaping how UK businesses handle record-keeping and reporting across the board.

Making Tax Digital (MTD)

MTD for VAT

All VAT-registered businesses must keep digital VAT records and submit returns through MTD-compatible software:

- Mandatory since April 2019 for businesses above the VAT threshold

- Extended to all VAT-registered businesses (including voluntary registrations) from April 2022

MTD for Income Tax Self Assessment (ITSA)

From April 2026, sole traders and landlords earning over £50,000 must submit quarterly income tax updates digitally.

| Income Threshold | Mandation Date |

|---|---|

| Over £50,000 | April 2026 |

| Over £30,000 | April 2027 |

| Over £20,000 | April 2028 |

Ecommerce sole traders should confirm their accounting software supports quarterly digital submissions to HMRC — and check which threshold applies to their income level before each mandation date.

Setting Up Your Ecommerce Bookkeeping System

Choose the Right Accounting Software

Compare the leading MTD-compatible platforms for UK ecommerce sellers:

| Software | Entry Plan | Mid Plan | MTD VAT | Multi-Currency | Key Strength |

|---|---|---|---|---|---|

| Xero | £7/mo | £37/mo | Yes | Yes (from £50/mo) | Strong Shopify, Amazon, WooCommerce integrations |

| QuickBooks Online | £16/mo | £33/mo | Yes | Yes (all plans, 145+ currencies) | User-friendly, excellent bank feeds |

| FreeAgent | £33/mo | £330/year | Yes | Limited | Suits micro-businesses, sole traders, free for NatWest customers |

Key criteria:

- Multi-currency support (essential for cross-border sellers)

- VAT compliance and MTD readiness

- Integration capability with sales platforms

- A2X compatibility for automated reconciliation

A2X is a popular add-on that automates reconciliation of Amazon and Shopify payouts. It transforms payout data from Amazon, Shopify, eBay, Etsy, and Walmart into organised summaries that reconcile with Xero, QuickBooks Online, and NetSuite.

Once you've chosen your software, the next step is connecting it to your sales channels.

Connect Sales Channels and Payment Gateways

Integrate each sales platform (Amazon, Shopify, eBay, WooCommerce) and payment processor (Stripe, PayPal, Klarna) directly with your accounting software. This ensures:

- Gross sales recorded automatically

- Platform fees categorised correctly

- Net payouts reconciled to bank deposits

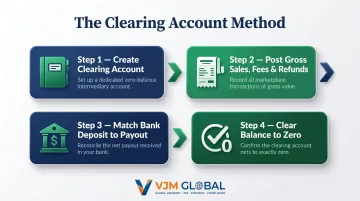

The clearing account method:

A clearing account holds funds between the point of sale and the bank deposit. Set one up for each platform using these steps:

- Create a clearing account in your chart of accounts (e.g., "Amazon Clearing")

- Post gross sales, fees, and refunds to the clearing account

- When the payout arrives, match the bank deposit against the clearing account balance

- The clearing account should reach zero after reconciliation

This method ensures your general ledger reflects gross sales rather than net deposits, critical for accurate VAT reporting. With reconciliation in place, the foundation for compliant bookkeeping is set.

Separate Business and Personal Finances

Open a dedicated business bank account from day one. It:

- Simplifies bookkeeping and audit trails

- Supports Making Tax Digital compliance

- Keeps personal and business transactions cleanly separated

Set up a custom chart of accounts that maps to ecommerce-specific categories:

- Revenue by platform (Amazon sales, Shopify sales, eBay sales)

- Shipping and fulfilment costs

- Advertising by channel (Google Ads, Facebook Ads)

- Platform-specific fees

Establish a Recurring Bookkeeping Routine

Weekly review:

- Import transactions

- Categorise expenses

- Flag anomalies (duplicate charges, incorrect fee deductions)

Monthly reconciliation:

- Match bank deposits to platform payouts

- Reconcile clearing accounts to zero

- Review P&L, Balance Sheet, and Cash Flow statements

Monthly reviews surface margin trends, flag underperforming channels, and give you a clear cash position — the data you need to plan inventory and manage VAT obligations on time.

Common Bookkeeping Mistakes UK Ecommerce Sellers Make

Recording the Net Platform Payout as Revenue

Many sellers record only what Amazon or eBay deposits into their bank account. This overlooks that gross sales, platform fees, and refunds must be recorded separately to get accurate:

- Revenue figures

- Expense totals

- VAT calculations

Always record gross sales and fees separately using the clearing account method — it creates a temporary holding account that reconciles what the platform reports against what actually hits your bank.

Ignoring VAT Deadlines and Misclassifying Transactions

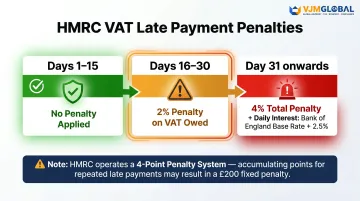

HMRC's points-based penalty system (from January 2023) imposes a £200 penalty once quarterly filers accumulate 4 late submission points.

Late payment penalties:

- Days 1-15 late: No penalty if paid in full or payment plan agreed

- Days 16-30 late: 2% of VAT owed at day 15

- Day 31+ late: 4% total penalty plus daily interest at Bank of England base rate + 2.5%

Misclassifying transactions—such as treating a refund as an expense rather than a sales reversal—distorts financial reports and VAT returns, triggering HMRC investigations.

Waiting Until Year-End to Update Records

Leaving bookkeeping until the end of the tax year makes it nearly impossible to:

- Spot errors in time to correct them

- Reconcile platforms accurately

- File on time without last-minute stress

Regular updates throughout the year keep you compliant and show exactly where your business stands month to month — so you can make tax decisions based on current numbers, not rushed estimates. If time is the constraint, bringing in a bookkeeper or outsourcing the function is far cheaper than the penalties and missed deductions that come from year-end scrambling.

When to Consider Outsourcing Your Ecommerce Bookkeeping

Inflection Points That Signal It's Time

Consider outsourcing when you:

- Sell on three or more platforms

- Are approaching the £90,000 VAT threshold

- Handle multi-currency sales

- Spend several hours a week on admin instead of growing the business

The average UK small business owner spends 44 hours and £4,500 per year on tax compliance—equating to roughly 51 minutes per week on tax compliance alone, before accounting for day-to-day bookkeeping. That's time most ecommerce owners can't afford to lose.

Benefits of Outsourcing to a Specialist

Outsourcing provides:

- Accurate reconciliation of Amazon, Shopify, eBay, and Etsy payouts by specialists who understand how each platform calculates them

- MTD-ready processes that keep VAT deadlines and quarterly ITSA submissions on track

- Scales with your transaction volume — no recruitment delays or hiring costs as you grow

- Monthly P&L, Balance Sheet, and Cash Flow statements delivered within 5–10 business days of month-end

VJM Global has worked with 250+ UK businesses across more than 15 industries. A 95% client retention rate reflects the kind of consistent, hands-on support — dedicated account management, secure data handling, transparent pricing — that ecommerce owners tend to stick with.

What to Look for in a Bookkeeping Partner

When choosing a bookkeeping partner, prioritise:

- Hands-on experience with Amazon, Shopify, WooCommerce, and eBay — not just general bookkeeping

- Working knowledge of IOSS, PVA, and export zero-rating under UK VAT and MTD rules

- Clear pricing structure — monthly retainers or transaction-based, with no hidden fees

- Monthly reports delivered within 5–10 business days after month-end

Frequently Asked Questions

Do I need to register for VAT as a UK ecommerce seller?

VAT registration becomes mandatory once UK taxable turnover exceeds £90,000 over any 12-month rolling period. You can also register voluntarily below the threshold to reclaim input VAT on business expenses.

Which accounting software is best for ecommerce?

Xero and QuickBooks Online are the most popular choices for UK ecommerce sellers due to their platform integrations and MTD compliance. A2X pairs well with both for automating Amazon and Shopify payout reconciliation.

How much do UK accountants charge?

UK outsourced bookkeeping typically costs between £200 and £500 per month for small ecommerce operations, depending on transaction volume and compliance needs. This is often more cost-effective than hiring in-house.

What is the most popular ecommerce platform in the UK?

Shopify leads UK ecommerce adoption with 239,051 UK websites, compared to 174,183 using WooCommerce. Platform choice affects bookkeeping setup, as each platform has different integration options with accounting software.

What is Making Tax Digital and how does it affect my ecommerce business?

MTD requires VAT-registered businesses to keep digital records and file returns via HMRC-approved software. From April 2026, sole traders earning over £50,000 must also submit quarterly income tax updates digitally.

Should I use cash or accrual accounting for my ecommerce store?

Cash accounting suits smaller, lower-volume businesses; accrual accounting is more accurate for inventory-heavy operations. HMRC permits cash accounting under the Cash Accounting VAT Scheme for businesses with turnover up to £1.35 million.

Final Thoughts

UK ecommerce bookkeeping carries real compliance stakes: VAT penalties, MTD filing obligations, and post-Brexit import VAT rules leave little margin for error. Missed deadlines or miscategorised transactions can trigger HMRC scrutiny that costs far more than clean bookkeeping would.

Whether you choose to manage it in-house with robust software or outsource to a firm like VJM Global — which supports 250+ UK businesses with bookkeeping and compliance — the foundation is the same: accurate records, maintained consistently from day one.