Introduction

Since 1 January 2021, UK businesses importing goods valued over £135 have faced a persistent cash flow problem: import VAT applies to all goods entering the UK from anywhere in the world. Paying this VAT upfront at customs — then waiting weeks or months to reclaim it on a VAT return — creates a real working capital burden.

According to HMRC statistics, non-postponed import VAT receipts fell from £32 billion in 2019-20 to just £9 billion in 2024-25, reflecting how widely UK importers have adopted Postponed VAT Accounting since its introduction.

That solution is Postponed VAT Accounting (PVA) — a system allowing UK VAT-registered importers to declare and reclaim import VAT on the same VAT return, rather than paying upfront at the border. This eliminates the cash flow gap entirely.

This guide covers how PVA works, who qualifies, how to complete a VAT return using monthly import statements, and where businesses commonly go wrong. Whether you're importing from China, the EU, or anywhere else, understanding PVA can free up working capital that would otherwise sit tied up in upfront customs payments.

Key Takeaways

- PVA lets UK VAT-registered businesses avoid paying import VAT upfront by declaring and reclaiming it on the same VAT return

- Applies to imports from any country outside the UK, covering goods valued over £135 (Northern Ireland businesses follow slightly different rules)

- No application process required — any VAT-registered business can start using PVA immediately

- Businesses must register with the Customs Declaration Service (CDS) and report PVA in Boxes 1, 4, and 7 of their VAT return

- The net cash VAT impact is zero: Box 1 declares VAT due, Box 4 reclaims it

What Is Postponed VAT Accounting?

Postponed VAT Accounting is a method introduced by HMRC on 1 January 2021 that allows UK VAT-registered businesses to account for import VAT on their VAT return instead of physically paying it at customs. The VAT appears as both payable (output tax) and reclaimable (input tax) on the same return, resulting in zero net cash outflow.

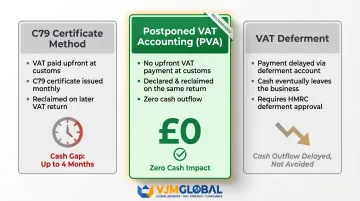

Before PVA, businesses paid import VAT at the border, received a C79 certificate as proof of payment, and recovered the VAT on a later return. For quarterly filers, this created a cash flow gap of up to four months. HMRC's official guidance confirms that PVA allows businesses to "declare and recover import VAT on the same VAT Return, rather than paying it upfront when the goods are imported and recovering it later."

PVA is distinct from two commonly confused mechanisms:

- C79 certificate method: VAT is paid upfront at customs and reclaimed via a C79 certificate on a later return, creating a temporary cash gap

- VAT deferment: Physical payment is deferred to a later date, but cash eventually leaves the business through a customs duty deferment account

PVA eliminates physical payment entirely for eligible businesses. The import VAT is an accounting entry on your VAT return.

Who Can Use Postponed VAT Accounting?

Any UK VAT-registered business can use PVA immediately without applying or seeking permission. There are no eligibility thresholds beyond being registered for VAT.

Geographic eligibility rules:

- England, Scotland, and Wales: Use PVA for imports from anywhere outside the UK

- Northern Ireland: Use PVA for imports from outside the UK and EU; goods from EU countries into Northern Ireland continue to be treated as intra-community acquisitions and do not use PVA

Non-Established Taxable Persons (NETPs): Foreign businesses importing into the UK without a UK establishment must appoint a UK-based intermediary or fiscal representative to handle customs declarations and select PVA on their behalf.

Flat Rate Scheme (FRS) businesses: Can use PVA but must account for it outside the FRS turnover calculation. Revenue and Customs Brief 3 (2022) clarifies that "the value of imported goods must be excluded from the Flat Rate Scheme calculation." It also confirms that "the full amount of import VAT should be added to Box 1 following the flat rate calculation." This rule became effective for VAT return periods starting on or after 1 June 2022.

How Postponed VAT Accounting Works: Step-by-Step

PVA operates through a monthly accounting cycle that substitutes upfront customs payment with structured record-keeping. The importer instructs their customs agent to apply PVA on the declaration, HMRC records the postponed VAT centrally, and the importer downloads a monthly statement to complete their VAT return. At no point does money change hands at the border.

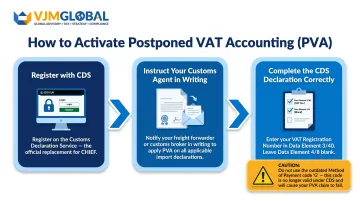

Step 1: Notify Your Customs Agent and Register with CDS

Before using PVA, businesses must register with the Customs Declaration Service (CDS) — the system that replaced CHIEF and now serves as the UK's sole customs platform. HMRC announced the transition on 3 August 2021, with import declarations closing on CHIEF on 30 September 2022.

Inform your freight forwarder or customs agent that PVA should be applied. According to HMRC, you must provide this instruction in writing before they can proceed.

How PVA is triggered on CDS declarations:

A common mistake is referencing outdated guidance. Many third-party sources still reference entering code 'G' in Box 47e, which applied only under the now-retired CHIEF system. The CDS Import Declaration Completion Guide confirms that method of payment code G was removed on 25 May 2023 and is no longer in use.

Current method (as of 2024):

- Enter your UK VAT registration number (VRN) in Data Element 3/40 (Additional Fiscal References Identification Number) at header level

- Leave Data Element 4/8 (Method of Payment) blank

Your customs agent must also provide your EORI number on the declaration. Failure to comply with these instructions may result in PVA being disallowed and a demand for payment issued.

Step 2: Download Your Monthly Postponed Import VAT Statement (MPIVS)

HMRC generates a Monthly Postponed Import VAT Statement (MPIVS) showing the total import VAT postponed in the previous month. These statements are available through the CDS financial dashboard and are usually accessible by the 10th working day of the following month.

Statements are only available online for 6 months from publication. Download and retain each one immediately — missing the window requires a separate retrieval process and creates record-keeping compliance exposure.

If a customs declaration was deferred:

If your customs agent delayed submitting the import declaration, the corresponding import will not appear on the current MPIVS. In that case:

- Estimate the VAT due based on goods value plus duty and other costs

- Report the estimated amount on the current VAT return

- Correct it on the next return once the delayed declaration appears on the following month's statement

Step 3: Complete Your VAT Return Using the MPIVS

The MPIVS figures feed directly into three specific boxes on the VAT return, covered in detail below. Unlike standard VAT return boxes, your accounting software must record these values under Making Tax Digital (MTD) — you cannot manually adjust them in the return boxes directly. This matters because MTD rules require a complete digital audit trail from source data to submission.

How to Account for Postponed VAT on Your VAT Return

HMRC's guidance specifies a three-box reporting structure for PVA:

- Box 1 (VAT due on sales and other outputs): Include the VAT due in this period on imports accounted for through PVA, sourced from the MPIVS

- Box 4 (VAT reclaimed on purchases and other inputs): Include the same VAT amount as a reclaim (subject to normal input tax recovery rules)

- Box 7 (Total value of purchases and all other inputs excluding VAT): Include the total value of all imports on the MPIVS, excluding VAT

The net VAT effect of Boxes 1 and 4 cancels out, leaving zero cash impact.

Worked Example

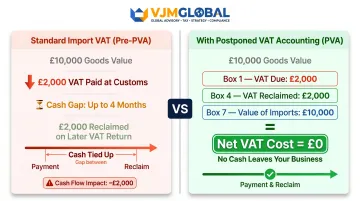

A UK business imports £10,000 of goods from outside the UK.

Under standard import VAT (pre-PVA):

- Pay £2,000 (20% VAT) at customs

- Wait to reclaim £2,000 on a later VAT return

- Cash flow gap of £2,000 for up to 4 months

Under PVA:

- Box 1: £2,000 (VAT due on imports)

- Box 4: £2,000 (VAT reclaimed on imports)

- Box 7: £10,000 (goods value excluding VAT)

- Net VAT cost: £0

- No cash leaves the business at any point

C79 Certificate vs. MPIVS

If you choose to pay VAT upfront at customs rather than using PVA, HMRC issues a C79 (Import VAT Certificate) monthly instead of an MPIVS. In this case, only Boxes 4 and 7 need to be completed on the VAT return (not Box 1, since the VAT was already paid).

Cross-check all imports against either the MPIVS or C79 to ensure HMRC holds accurate records.

Import VAT Calculation Rule

Getting the customs value right directly affects how much VAT you declare. Import VAT is calculated on the customs value of goods after adding duty, freight, insurance, and other costs — not simply on the supplier invoice value. HMRC's valuation guidance requires businesses to base import VAT on the customs value for duty, even if no duty is payable.

Items to add to customs value include:

- Customs duty or levy payable on importation

- Excise duty or other charges (except VAT itself)

- Commission, packing, transport, and insurance costs up to the goods' first destination in the UK

- Customs clearance charges, quay rent, entry fees, demurrage, handling, loading, and storage costs

HMRC will not accept estimates based on invoice value alone — always use the full customs value when calculating import VAT.

Key Benefits of Postponed VAT Accounting for UK Importers

Cash Flow Relief

The most significant benefit is eliminating the upfront VAT payment. Businesses can receive and use their goods without waiting to recover VAT, keeping working capital available for operations.

With 251,000 UK businesses importing goods in 2024 — 67% of them SMEs — the aggregate cash flow relief is substantial. Border-collected import VAT dropped from £32 billion in 2019-20 to £9 billion in 2024-25, pointing to PVA's widespread adoption across UK importers.

Simplified Administration

Before Brexit, businesses importing from the EU used the reverse charge mechanism. PVA broadly replicates this approach for all global imports, meaning less interaction with freight handling companies for VAT processing and fewer separate payment processes to manage.

Operational Speed

Goods are not held at customs pending VAT payment, which speeds up supply chains — particularly valuable for time-sensitive or perishable goods imports.

Taken together, these three benefits make a strong case for adoption. In practice, businesses gain the most when PVA processes are set up correctly from the outset:

- Cash flow: VAT is declared and recovered in the same return period, with no upfront payment at the border

- Administration: A single monthly import VAT statement replaces multiple payment processes

- Speed: Goods clear customs faster, reducing delays for time-critical shipments

VJM Global's VAT compliance advisory services help UK importers structure PVA correctly from day one — avoiding setup errors and ensuring the process fits within existing accounting workflows.

Common Mistakes and When Postponed VAT Accounting May Not Apply

Misconception 1: "PVA is the same as VAT deferment"

Deferred VAT was a temporary post-Brexit measure allowing businesses to postpone physical payment of import VAT into a separate monthly payment. PVA is permanent and requires no payment at all — the VAT is offset within the same return.

It should not be confused with a customs duty deferment account, which is still required for customs duty (not VAT).

Misconception 2: "The MPIVS shows all imports"

The MPIVS only reflects imports for which customs declarations have been submitted with PVA selected. If a declaration was delayed or deferred, the import will not appear on the statement. Businesses must estimate the VAT and correct it in the following return. Many businesses incorrectly assume the MPIVS is a complete picture of all imports.

Common Error: Failing to Download and Store Statements

Because MPIVS statements are only available online for 6 months from the date of publication, businesses that miss downloading a statement risk losing access to it. Archived statements require a separate retrieval process. This is a serious record-keeping compliance risk.

When PVA May Not Apply or Needs Adjustment

Beyond common errors, there are four specific scenarios where PVA either does not apply or requires adjustment:

Partially exempt businesses — Businesses making exempt supplies (financial services, insurance, residential real estate) cannot fully reclaim import VAT. Box 1 must still show the full import VAT amount, but Box 4 reflects only the recoverable portion under their partial exemption method — meaning a real cash cost remains.

Northern Ireland imports from EU countries — These are treated as intra-community acquisitions under EU VAT rules, not imports. PVA does not apply.

Consignments valued at £135 or less — HMRC confirms that these are subject to supply VAT charged at point of sale, not import VAT. Note that the threshold applies to the consignment value, not to individual items within it.

Postal imports via Royal Mail — Goods received through Royal Mail over £135 cannot use PVA. The exception is where Royal Mail provides the service through a commercial non-postal arrangement.

Frequently Asked Questions

How does postponed VAT accounting work in the UK?

PVA allows UK VAT-registered importers to account for import VAT on their VAT return rather than paying it at the border. Box 1 records VAT due on imports, Box 4 reclaims it, and Box 7 records the goods value — resulting in no net cash payment.

How do you account for postponed VAT on a VAT return?

Retrieve your Monthly Postponed Import VAT Statement (MPIVS) from the Customs Declaration Service, then use the figures to complete Boxes 1, 4, and 7 of your VAT return. Because the same amount appears in both Box 1 (output) and Box 4 (input), the entries cancel out with no net VAT payment due.

What is the postponed VAT accounting threshold?

There is no minimum value threshold for using PVA itself, but import VAT only applies to goods entering the UK valued above £135. Below that threshold, supply VAT rules apply instead, so PVA is not relevant.

Is postponed VAT accounting mandatory in the UK?

PVA is optional for most VAT-registered importers. However, it becomes mandatory when a business opts to defer its customs declarations, and it is also mandatory for B2B imports into Northern Ireland from outside the EU valued below £135.

Can businesses in Northern Ireland use postponed VAT accounting?

Northern Ireland businesses can use PVA for imports from non-EU countries. Goods arriving from EU member states are treated as intra-community acquisitions and fall outside the PVA framework entirely.

What is the difference between postponed VAT accounting and VAT deferment?

VAT deferment (via a customs duty deferment account) delays when payment is made but still requires a physical cash payment. PVA involves no physical payment at all — the import VAT is declared and reclaimed on the same VAT return, resulting in zero cash outflow.