Introduction

HMRC completed 316,000 compliance checks in 2024-25, securing a record £48.0 billion in compliance yield. "Error and failure to take reasonable care" was the single most cited reason for incorrect tax. Many businesses implement double entry bookkeeping without fully understanding how or why it works — leaving them exposed to exactly these mistakes.

Double entry bookkeeping records every financial transaction in two accounts — one debit and one credit — so the books always balance. For UK business owners, finance managers, and accountants, it forms the foundation of accurate financial reporting, HMRC compliance, and sound business decisions.

This guide explains what double entry bookkeeping is, why it is required for UK businesses, how it works step by step, the golden rules governing it, and common mistakes to avoid.

Key Takeaways

- Double entry records every transaction as both a debit and a credit, keeping the books balanced

- The entire system rests on one equation: Assets = Liabilities + Equity — any transaction that breaks this balance signals an error

- UK limited companies must produce financial statements under the Companies Act 2006, making double entry the practical standard for compliance

- Which account to debit or credit depends on account type — the three golden rules tell you exactly which is which

- Common pitfalls include misclassification, unrecorded entries, and skipped reconciliations

What Is Double Entry Bookkeeping?

Double entry bookkeeping is a system where every financial transaction creates equal and opposite entries — a debit in one account and a credit in another — so that total debits always equal total credits. This dual recording maintains a permanently balanced set of books.

That balance enables accurate preparation of a balance sheet, profit and loss statement, and other financial reports required by Companies House and HMRC.

The system differs fundamentally from single entry bookkeeping, which records only one side of each transaction (typically income or expense). While simpler, single entry cannot produce a complete financial picture. It fails to track assets, liabilities, and equity simultaneously, making it unsuitable for UK limited companies subject to statutory reporting requirements.

ACCA defines the accounting equation as "Assets = Capital + Liabilities" and states it "is fundamental to the application of double entry bookkeeping where every transaction has a dual effect on the financial statements."

Why UK Businesses Use Double Entry Bookkeeping

Legal and Regulatory Requirements

Under Section 396 of the Companies Act 2006, UK limited companies must produce "a balance sheet as at the last day of the financial year" and "a profit and loss account" that together "give a true and fair view" of the company's financial affairs. These outputs can only be produced accurately using double entry accounting. HMRC expects records that support this true and fair view, and Companies House requires annual filing within nine months for private companies.

Failure to maintain adequate records carries serious consequences: HMRC can impose a £3,000 fine, and directors risk disqualification. HMRC's compliance yield reached £48.0 billion in 2024-25, a figure that signals how actively the department pursues underpayment and poor record-keeping.

Complete Financial Visibility

Double entry gives UK businesses a complete, real-time financial picture — tracking income, spending, assets, liabilities, and equity at once. That visibility supports faster decisions and clearer planning in ways single entry records simply cannot match.

HMRC Compliance and Audit Readiness

That financial clarity directly reduces compliance risk. When entries are consistently balanced and reconciled, discrepancies surface early — before they escalate into HMRC enquiries. Penalty rates range from 0% to 100% of extra tax due, depending on whether errors are careless (0–30%), deliberate (20–70%), or deliberate and concealed (30–100%).

Investor and Lender Confidence

Banks, investors, and potential buyers rely on financial statements generated from double entry to assess a business's financial health. Single entry records are widely regarded as insufficient for:

- Securing business loans or credit facilities

- Passing investor due diligence

- Supporting acquisition or sale valuations

Scalability Through Complexity

As businesses grow — adding employees, multiple bank accounts, VAT registration, and payroll — single entry quickly becomes inadequate. Double entry scales with that complexity. 62% of UK SMEs use accounting software and 70% work with a qualified accountant, which suggests most UK businesses already operate within a double entry framework.

At this stage, many businesses also bring in external support to maintain accuracy without stretching internal teams. VJM Global works with UK businesses on accounting outsourcing, handling bookkeeping and compliance so finance teams can focus on growth rather than record-keeping.

How Double Entry Bookkeeping Works: Step by Step

Conceptual Foundation

Every transaction has two sides: something is received, and something is given up. Double entry captures both sides using five core account types defined by FRS 102:

- Assets: Resources controlled by the entity from which future economic benefits are expected

- Liabilities: Present obligations expected to result in an outflow of resources

- Equity: The residual interest in assets after deducting liabilities

- Income: Increases in economic benefits resulting in increases in equity

- Expenses: Decreases in economic benefits resulting in decreases in equity

The accounting equation (Assets = Liabilities + Equity) must hold true after every entry.

Debit and Credit Rules

| Account Type | Debit (Increase) | Credit (Decrease) |

|---|---|---|

| Assets | ✓ | |

| Expenses | ✓ | |

| Liabilities | ✓ | |

| Equity | ✓ | |

| Income | ✓ |

With these rules as your reference, here is how each transaction moves through the system.

Step 1: Identify and Classify the Transaction

Every transaction begins with identifying what has occurred and which account types are affected. For example: a UK business receives £2,000 from a client. This affects the cash (asset) account and the sales income account. Correct classification is critical because misclassification distorts every financial report that follows.

Step 2: Record the Journal Entry

Once accounts are identified, the transaction is recorded as a journal entry: a debit to one account and a credit to another for the same amount.

Example: Receiving £2,000 in cash for services rendered:

- Debit: Cash Account £2,000 (asset increases)

- Credit: Sales Income £2,000 (income increases)

Most accounting software will flag the entry immediately if the two sides don't match — a built-in safeguard against recording errors.

Step 3: Post to the General Ledger and Run a Trial Balance

You post journal entries to the general ledger, where each account maintains a running balance. Over time, this ledger becomes the complete record of every financial movement in the business.

From the ledger, you prepare a trial balance: a two-column summary listing all debit and credit account balances. If the columns match, the books balance. Any discrepancy signals a recording error that must be resolved before producing financial statements.

Sage's help centre confirms: "Double-entry bookkeeping means that every transaction entered debits and credits different nominal codes. This means that your trial balance always balances."

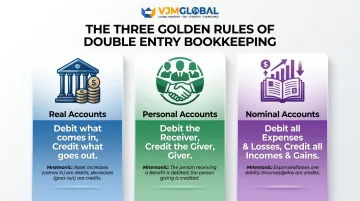

The Three Golden Rules of Double Entry Bookkeeping

The traditional British approach classifies all accounts into three types, each governed by its own rule:

- Real accounts — assets (property, equipment, cash)

- Personal accounts — debtors and creditors

- Nominal accounts — income, expenses, gains, and losses

Rule 1: Real Accounts

"Debit what comes in, credit what goes out."

Example: Purchasing equipment worth £5,000:

- Debit: Fixed Assets (Equipment) £5,000 (asset comes in)

- Credit: Bank Account £5,000 (cash goes out)

Rule 2: Personal Accounts

"Debit the receiver, credit the giver."

Example: Receiving a supplier invoice for £1,000 of stock:

- Debit: Purchases Account £1,000 (business is the receiver)

- Credit: Trade Creditors £1,000 (supplier is the giver)

Rule 3: Nominal Accounts

"Debit all expenses and losses, credit all incomes and gains."

Example: Two common nominal account entries:

- Debit: Rent Expense £800 (expense incurred)

- Credit: Interest Income £800 (income earned)

Every nominal account entry flows directly into your profit and loss statement — which is how HMRC-compliant accounts capture trading performance over a financial year.

Common Mistakes and Misconceptions in Double Entry Bookkeeping

Misclassification of Accounts

Placing a transaction in the wrong account type — such as recording a business loan as income — is one of the most frequent errors. It goes undetected in day-to-day records but distorts the balance sheet and profit and loss statement.

To prevent this, maintain a clear chart of accounts and review your categorisation consistently — ideally each month-end before closing the period.

Forgetting to Record Both Sides of a Transaction

Under double entry, each transaction must have a matching debit and credit. Missing one side creates an imbalance that the trial balance will reveal.

That said, skipping the trial balance check is its own mistake — one that lets errors compound silently over weeks or months.

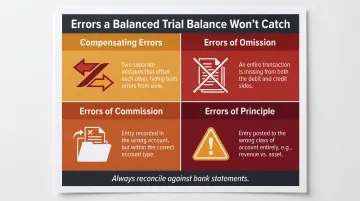

Confusing the Trial Balance with Error-Free Accounts

A common misconception is that a balanced trial balance means the books are correct. As noted in ACCA study materials: "A balanced trial balance does not guarantee that all the accounts contain the correct amounts."

The trial balance only confirms debits equal credits — it does not catch:

- Compensating errors: Two mistakes that offset each other

- Errors of omission: Transactions completely omitted from both sides

- Errors of commission: Recording in the wrong account of the correct type

- Errors of principle: Recording in the wrong class of account entirely

Accuracy requires reconciliation against bank statements and source documents, not just a balanced trial balance.

Frequently Asked Questions

What is double-entry bookkeeping in the UK?

Double-entry bookkeeping is the standard accounting method used by UK businesses in which every financial transaction is recorded as both a debit and a credit across two accounts, keeping the books balanced. UK limited companies are legally required to maintain records sufficient to produce accurate financial statements under the Companies Act 2006.

What is an example of double-entry bookkeeping?

If a business pays £500 in office rent, the rent expense account is debited by £500 (expense increases) and the bank account is credited by £500 (asset decreases). Both entries are equal and opposite, keeping the ledger balanced.

Is double-entry bookkeeping still used?

Yes, double-entry bookkeeping remains the universal standard for business accounting worldwide, including in the UK. It is the method underlying all major accounting software (Xero, QuickBooks, Sage) and is required for producing the financial statements demanded by HMRC, Companies House, investors, and lenders.

Is double-entry bookkeeping hard?

The concept is straightforward: every transaction has two equal and opposite effects. Consistent, accurate application does require practice and familiarity with account classifications. Many UK businesses use accounting software or outsourced bookkeeping services to manage this reliably without needing deep technical expertise in-house.

What are the three golden rules of double-entry bookkeeping?

The three golden rules follow the traditional British approach to account classification:

- Real accounts: Debit what comes in, credit what goes out

- Personal accounts: Debit the receiver, credit the giver

- Nominal accounts: Debit all expenses and losses, credit all incomes and gains

Do sole traders in the UK need to use double-entry bookkeeping?

Sole traders are not legally required to use double entry. From April 2024, cash basis became the default method with no turnover cap. However, double entry is strongly recommended as the business grows, and is essential for VAT-registered businesses (mandatory above £90,000 turnover) and those who want accurate financial reporting for growth or lending purposes.