This guide explains the five core account categories, how to number and structure a UK-compliant CoA, UK-specific VAT and accounting standard requirements, real examples from Xero and Sage, and common setup mistakes to avoid. Whether you're a UK limited company, sole trader, or foreign entity operating in the UK, this article will help you build a CoA that supports clean reporting and HMRC compliance.

Key Takeaways

- A chart of accounts is a numbered list of every account your business uses to record financial transactions

- Five categories structure it — assets, liabilities, equity, revenue, and expenses — each mapping to either the Balance Sheet or Profit and Loss

- UK businesses must account for VAT codes, UK GAAP (FRS 102 or FRS 105), and Making Tax Digital requirements

- Numbering follows consistent logic (1000s for assets, 2000s for liabilities) across Xero, QuickBooks, and Sage UK

- A poorly structured CoA leads to inaccurate tax filings, unclear reports, and compliance risks

What Is a Chart of Accounts in the UK?

A chart of accounts is a complete index of all accounts available in your general ledger. Each account has a unique code, name, and type, used to categorise every financial transaction your business makes. It supports accurate financial statements—Profit and Loss and Balance Sheet—VAT reporting, and clear visibility into how money moves through your business.

The CoA is often confused with two related concepts. Here's how they differ:

- Chart of Accounts: The structure — a numbered index of every account category your business uses

- General Ledger: The detail — the full record of every transaction posted to those accounts

- Trial Balance: The snapshot — a period-end report listing all account balances at a specific date, derived from the CoA

In the UK, there's no single legally mandated CoA structure for private companies under the Companies Act 2006—section 396 mandates statement formats only. However, standard practice and accounting software defaults (Xero, QuickBooks UK, Sage 50) provide a framework the majority of UK businesses adopt by default.

The Five Core Categories of a UK Chart of Accounts

The five categories feed into two financial statements: the Balance Sheet (assets, liabilities, equity) and the Profit and Loss / Income Statement (revenue, expenses).

| Category | Financial Statement |

|---|---|

| Assets | Balance Sheet |

| Liabilities | Balance Sheet |

| Equity | Balance Sheet |

| Revenue | Profit & Loss |

| Expenses | Profit & Loss |

Balance Sheet Accounts

Assets are resources owned by the business, split into:

- Current assets: Cash, accounts receivable, stock/inventory, VAT reclaim receivable

- Fixed/non-current assets: Equipment, property, motor vehicles, intangible assets like goodwill

A UK-relevant example: VAT reclaim receivable is the amount HMRC owes you and is recorded as a current asset.

Liabilities are obligations the business owes, split into:

- Current liabilities: VAT payable to HMRC, accounts payable, PAYE liabilities, Corporation Tax provision

- Long-term liabilities: Business loans, director's loan accounts, hire purchase agreements

VAT payable is one of the most common UK-specific current liability accounts: it represents the net amount owed to HMRC after offsetting input VAT against output VAT.

Equity accounts represent the owner's stake in the business:

- Limited companies: Share capital, retained earnings, profit and loss reserves

- Sole traders: Capital account, owner's drawings

The structure matters for year-end reporting — retained earnings in a limited company accumulate differently from a sole trader's capital account.

Income Statement Accounts

Revenue accounts capture all income generated:

- Product sales and service fees

- Interest income and investment returns

- Other or miscellaneous income

VAT-registered businesses need to separate income by VAT treatment. For example, a retailer selling children's clothing (zero-rated) alongside adult clothing (standard-rated at 20%) must use distinct revenue accounts to report VAT correctly to HMRC.

Expense accounts record all costs incurred:

- Cost of sales/direct costs: Materials purchased, subcontractor fees, direct labour

- Operating overheads: Rent, salaries, utilities, insurance, professional fees

Keeping direct costs separate from overheads gives you a clear gross profit figure — which tells you whether the core business is viable before fixed costs enter the picture.

How to Number and Structure Your Chart of Accounts

Block numbering is the universal best practice: each category gets a numeric range so the account type is immediately identifiable from its code.

Standard UK numbering convention:

- 1000–1999 Assets

- 2000–2999 Liabilities

- 3000–3999 Equity

- 4000–4999 Revenue

- 5000–5999 Cost of Sales

- 6000–6999 Expenses

Note that UK software platforms apply their own conventions within this framework: Xero uses 3-digit codes (090–999 range), QuickBooks UK suggests 5-digit ranges (account numbers are off by default), and Sage 50 UK uses 4-digit codes starting from 0010.

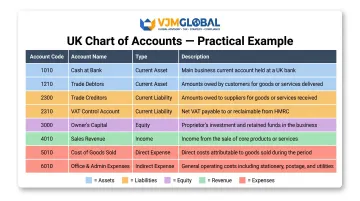

Practical UK Chart of Accounts Example

| Account Code | Account Name | Type | Description |

|---|---|---|---|

| 1010 | Business Bank Account | Current Asset | Main trading bank account |

| 1020 | Petty Cash | Current Asset | Cash on hand for small purchases |

| 1100 | Accounts Receivable | Current Asset | Money owed by customers |

| 1210 | VAT Reclaim | Current Asset | Input VAT recoverable from HMRC |

| 2100 | Accounts Payable | Current Liability | Money owed to suppliers |

| 2300 | VAT Payable (HMRC) | Current Liability | Output VAT owed to HMRC |

| 2310 | PAYE Liability | Current Liability | Income tax and NI owed to HMRC |

| 2400 | Director's Loan Account | Long-term Liability | Money owed to/from director |

| 3000 | Share Capital | Equity | Issued share capital |

| 4010 | Sales Revenue – Standard-rated | Revenue | Sales subject to 20% VAT |

| 5010 | Cost of Goods Sold | Cost of Sales | Direct cost of products sold |

| 6010 | Rent | Expense | Office or shop rent |

Once your structure is in place, consistent naming and careful setup keep it usable as your business grows.

Best Practices for Naming and Setup

When naming accounts:

- Keep names descriptive and consistent ("Utilities – Electricity" not just "Utilities")

- Avoid vague labels that create confusion later

- Use sub-account codes where needed (e.g., 6010 Rent, 6011 Rent – Office, 6012 Rent – Warehouse)

Setup steps in UK accounting software:

- Choose your business type on setup (limited company, sole trader, partnership)—this auto-generates a default CoA

- Review the default accounts and add, edit, or archive accounts to reflect your actual business activities

- Assign appropriate VAT codes to each account (critical for MTD compliance)

- Leave gaps in your numbering to add new accounts later without restructuring

Xero and QuickBooks UK both pre-load CoA templates tailored to common UK business types that can be customised during setup. For foreign-owned UK entities or businesses with cross-border operations, getting VAT coding and UK GAAP alignment right from the start often warrants input from an accounting specialist — mistakes in the initial structure tend to compound over time.

UK-Specific Considerations for Your Chart of Accounts

VAT Account Setup

UK VAT-registered businesses must assign the correct VAT rate to each account:

- Standard rate: 20%

- Reduced rate: 5% (energy-saving materials, children's car seats)

- Zero-rated: 0% (most food, children's clothing, books)

- Exempt: No VAT applies (insurance, finance, education)

Most UK accounting software attaches VAT codes to nominal accounts so VAT is calculated and reported automatically. This matters because all VAT-registered businesses must use MTD-compliant software for HMRC returns — a requirement in force since April 2022.

UK GAAP Compliance

Small UK companies filing under FRS 102 (or FRS 105 for micro-entities) must structure their CoA to produce accounts that meet these standards. This includes how fixed assets, depreciation, provisions, and deferred tax are classified.

Company size thresholds (effective April 2025):

- Micro-entities: Turnover ≤ £900k, assets ≤ £450k, employees ≤ 10

- Small companies: Turnover ≤ £15m, assets ≤ £7.5m, employees ≤ 50

IFRS applies to publicly listed companies only (section 403(1) Companies Act 2006), but most UK SMEs follow UK GAAP.

Companies House and HMRC Filing Requirements

Getting your CoA structure right directly affects how smoothly you can meet these obligations:

- Statutory accounts (Companies House): Due within 9 months of year-end; late penalties run from £150 to £1,500

- CT600 (Corporation Tax): Must be filed within 12 months of accounting period end

- CT payment: Due 9 months and 1 day after period end

- Accounts format: CoA must support abridged or full accounts as required

Sole traders use the same CoA logic for self-assessment, mapping income and expenses to HMRC categories.

Business Structure Impact on CoA Design

Sole traders:

- Simpler CoA with no share capital

- Uses owner's drawings account instead of dividends

- No Corporation Tax provision (uses Income Tax instead)

Limited companies:

- Requires share capital, retained earnings, director loan accounts

- Must track Corporation Tax provision

- Director's Loan Account (DLA) triggers section 455 tax at 33.75% if it remains overdrawn 9 months after year-end

Across the 250+ UK businesses VJM Global has supported, getting CoA structure right from the start has consistently reduced compliance risk and improved financial visibility — especially for foreign-owned UK entities working through unfamiliar regulations for the first time.

Common Mistakes and Best Practices

Creating Too Many or Too Few Accounts

Two opposite errors trip up most businesses when building a CoA:

- Too granular: Separate accounts for "Office Supplies – Pens," "Office Supplies – Paper," and "Office Supplies – Folders" add no decision-making value and make reports unreadable.

- Too broad: Grouping all utilities (electric, gas, water, internet) into one account makes it impossible to identify cost trends or claim specific reliefs.

Solution: Before adding a new account, ask: "Does this genuinely help me make better decisions or meet a compliance requirement?" If not, use an existing account.

Using Incorrect Account Types

Common errors:

- Recording loan repayments as an expense instead of a liability reduction—this overstates expenses and distorts profitability

- Recording owner drawings as a salary expense—creates incorrect PAYE liability and overstates wage costs

- Treating capital expenditure (equipment purchase) as an expense instead of a fixed asset—fails to spread depreciation correctly

These mistakes distort profitability figures and create mismatches in HMRC filings, triggering HMRC compliance checks or financial penalties.

Never Reviewing or Cleaning Up Your CoA

Recommended practice:

- Review your CoA annually, or when the business changes (new product lines, VAT registration, new financing)

- Archive unused accounts rather than deleting them—this preserves historical reporting integrity

- Check for duplicate or overlapping accounts

A scheduled CoA review keeps your financial structure accurate and audit-ready — so your reports reflect how the business actually operates, not how it was set up three years ago.

Frequently Asked Questions

What is the chart of accounts in the UK?

A chart of accounts in the UK is a structured list of all accounts used to record financial transactions in the general ledger, organised into assets, liabilities, equity, revenue, and expenses. It produces compliant financial statements for HMRC and Companies House.

What are the basic chart of accounts categories?

The five core categories are: assets (what the business owns), liabilities (what it owes), equity (the owner's stake), revenue (money earned), and expenses (costs incurred). Assets, liabilities, and equity feed the Balance Sheet; revenue and expenses feed the Profit and Loss.

What is an example of a chart of accounts?

A typical UK CoA includes account 1010 (Business Bank Account), 2300 (VAT Payable), 4010 (Sales Revenue), and 5010 (Cost of Goods Sold). The structure varies by business type and industry—e-commerce businesses need stock accounts, while service businesses may not.

How are accounts numbered in the chart of accounts?

Accounts are numbered in logical blocks by type: 1000s for assets, 2000s for liabilities, 3000s for equity, and so on. Different UK software platforms use slightly different ranges, so always leave gaps in your numbering to accommodate new accounts without restructuring.

What are common chart of accounts mistakes?

Top mistakes include over-complicating the CoA with too many accounts, using the wrong account type for a transaction (like coding a loan as an expense), and never reviewing or cleaning up unused accounts—all of which distort reports and risk compliance failures.

What accounting standards are used in the UK?

UK private companies follow UK GAAP — FRS 102 for most SMEs or FRS 105 for micro-entities. Publicly listed companies use IFRS. Your CoA structure must align with the applicable standard to ensure correct fixed asset classification and depreciation treatment.

Need help setting up a compliant UK chart of accounts? VJM Global's accounting team works with UK businesses and foreign-owned UK entities to build CoA structures that are VAT-coded correctly and HMRC-ready from day one. Reach out at info@vjmglobal.com or call +91 9891576441 to discuss your requirements.