Introduction

An HMRC tax audit — formally called a compliance check — is a review of your financial records and tax returns by HM Revenue & Customs to verify you've paid the correct amount of tax. For UK businesses, from SMEs and limited companies to sole traders, this isn't a remote possibility. HMRC completed 316,000 compliance checks in 2024-25, generating £48 billion in additional tax revenue.

Many business owners assume audits only happen when something's obviously wrong. That's a misconception. HMRC's Connect platform processes 22 billion lines of data, cross-referencing your returns against bank records, Companies House filings, and data from 106 international jurisdictions.

Even minor discrepancies can trigger a review — and some checks are entirely random.

Knowing what triggers a check — and what HMRC expects to find — is the most practical way to reduce your exposure. This guide walks you through the types of audits, common triggers, what happens during a compliance check, and how to prepare.

Key Takeaways

- An HMRC compliance check examines your financial records and tax returns to confirm correct tax payment

- Triggers include inconsistent figures, late filings, and high-risk industry flags — random checks can hit any business too

- HMRC can look back 4 years for honest errors, 6 years for careless mistakes, and 20 years for deliberate fraud

- Expect written notification, document requests, and possibly a site visit; outcomes range from no further action to financial penalties

- Your strongest protection: clean bookkeeping, timely filings, and qualified tax representation

What Is an HMRC Tax Audit?

An HMRC tax audit is a formal compliance check where HMRC examines your tax affairs to ensure the correct tax has been declared and paid. The official term is "compliance check" — you'll see this on any letter from HMRC. It covers Corporation Tax, VAT, PAYE, Self Assessment, and other taxes.

Most businesses encounter compliance checks, not criminal investigations. HMRC's policy is to deal with fraud using civil procedures wherever possible. Criminal investigation is reserved for cases requiring a strong deterrent message or where conduct is so serious that only a criminal charge is suitable.

The Three Types of HMRC Audit

HMRC uses three internal classifications to organise compliance work, though legally all enquiries are treated the same:

| Audit Type | Scope | Typical Trigger |

|---|---|---|

| Full enquiry | All business records; director-level accounts for limited companies | Suspected widespread inaccuracies or serious underpayment |

| Aspect enquiry | Single area only — e.g. a large VAT reclaim, unusual expense, or property disposal | One specific discrepancy, not systemic issues |

| Random check | Same scope as a risk-based enquiry — officers cannot treat it as low priority | No fault or suspicion; selected by HMRC's KAI team to measure the tax gap |

Random checks are less common but handled identically to targeted enquiries. If you receive one, the response process is the same regardless of how clean your records are.

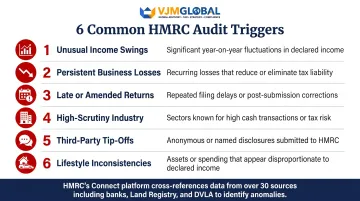

What Triggers an HMRC Tax Audit?

HMRC uses sophisticated data analytics to compare your returns against industry norms, peer groups, and historical data. The Connect system makes unusual figures easier to detect than most businesses realise.

Common risk triggers include:

Unusual figures or sudden swings in income, expenses, or profit margins — especially discrepancies between successive years or different sections of the same return. Connect benchmarks your numbers against thousands of similar businesses.

Persistent losses across multiple years, which prompt HMRC to question commercial viability and whether expenses are genuinely "wholly and exclusively" for business use.

Recurring late or amended returns across Self Assessment, Corporation Tax, VAT, or PAYE. Each amendment builds a data trail — especially if corrections consistently reduce your liability.

Operating in a high-scrutiny sector — hospitality, construction (particularly under CIS), retail, hair and beauty, and financial services all face elevated review rates due to cash-heavy transactions and complex supply chains.

Tip-offs and third-party data: HMRC received 164,670 fraud reports in 2024-25, paying out £852,438 in informant rewards. Ex-employees, competitors, and business partners are common sources — even vague reports can trigger a review when other risk factors are present.

Two further triggers catch many businesses off guard:

- Lifestyle inconsistent with declared income — luxury purchases, vehicles, or property that don't align with reported earnings, especially where Connect cross-references Land Registry and social media data

- Prior audit findings — previous compliance issues raise the likelihood of follow-up scrutiny, particularly where earlier errors were classified as careless or deliberate

What Happens During an HMRC Tax Audit?

HMRC almost always notifies businesses in advance — typically by letter to you or your registered accountant. The notification outlines what's being reviewed, which tax years are in scope, and what documents are required.

HMRC must open an enquiry within 12 months of a return being filed (or by the next quarter day — 31 January, 30 April, 31 July, or 31 October — if filed late). Miss that window and HMRC generally loses the right to open an enquiry — though separate powers exist for suspected fraud.

How Far Back Can HMRC Audit?

Three review windows apply depending on the nature of any errors:

- 4 years: Normal time limit for innocent errors or standard checks (applies to all taxes)

- 6 years: Where HMRC suspects careless behaviour or human error (Income Tax, CGT, Corporation Tax, IHT, SDLT, SDRT, Petroleum Revenue Tax — note VAT remains 4 years)

- 20 years: Cases involving deliberate tax fraud or evasion

These windows matter for record-keeping, too. HMRC expects businesses to retain records for at least 6 years (5 years for self-employed individuals) — meaning a 6-year audit window can cover periods where your records may already be gone.

The Audit Process Step by Step

Step 1 — Information gathering

HMRC specifies required records, typically including:

- Tax returns and calculations

- Business bank statements

- Sales and purchase invoices

- PAYE and RTI records

- VAT documentation

The audit may be conducted remotely (document submission) or involve an in-person visit to your business premises, home address, or accountant's office.

Step 2 — Review and clarification

HMRC asks clarifying questions about how figures were calculated, how your business operates, or how specific transactions were treated. You have the right to bring an accountant or legal adviser to any meeting. Refusing a reasonable request without valid excuse can result in a penalty.

Step 3 — Outcome and resolution

Three possible outcomes exist:

| Outcome | When It Applies | What Happens Next |

|---|---|---|

| No further action | Records are clean and HMRC is satisfied | Audit closes — no liability |

| Correction notice | Underpayment identified | Tax owed within 30 days, plus interest |

| Penalty notice | Negligent or deliberate errors found | 0%–100% of underpaid tax, based on behaviour and disclosure timing |

In complex cases, HMRC may agree a contract settlement. You have the right to appeal a decision or apply for Alternative Dispute Resolution (ADR) if you disagree. ADR uses a trained HMRC mediator to find common ground — and choosing it doesn't forfeit your right to escalate to an independent tribunal later.

How to Prepare Your Business for an HMRC Audit

The businesses that handle HMRC audits smoothly are rarely the ones who prepared at the last minute. Audit readiness is built through consistent habits long before any enquiry letter arrives.

Keep Records Organised Year-Round

HMRC expects records to be organised and immediately accessible on request. Poor recordkeeping is itself a red flag — and one of the most controllable audit risk factors.

Maintain:

- Digital copies of receipts, invoices, and bank statements

- Up-to-date payroll and RTI data

- Correctly categorised and evidenced business expenses

- VAT return records with full supporting documentation

- Accurate mileage and travel logs

File on Time and Review Before Submitting

Late or amended submissions are among the most common — and preventable — audit triggers. Review figures carefully before submission rather than rounding or estimating. A few extra hours of checking before the deadline can meaningfully lower your audit exposure.

Get Ready for Making Tax Digital

From April 2026, businesses and sole traders above the £50,000 turnover threshold must comply with mandatory digital record-keeping and quarterly updates. The threshold drops to £30,000 in April 2027 and £20,000 in April 2028.

MTD IT requires:

- Compatible accounting software

- Digital storage of income and expense records (amount, date, and category)

- Quarterly digital updates to HMRC

Getting ahead of MTD IT compliance — rather than waiting for the deadline — builds the kind of clean, structured records that make any future audit far less disruptive.

Work with a Qualified Tax Adviser

Professional representation does more than improve filing accuracy. When a registered agent is on record, HMRC contacts them first — giving you time to respond properly rather than reactively. Expert advisers can also narrow the scope of an enquiry and shorten its duration.

VJM Global has supported 250+ UK businesses with tax compliance and HMRC correspondence, drawing on 30+ years of cross-border advisory experience. Their team helps businesses maintain audit-ready records and manages representation during compliance checks.

Common Misconceptions UK Businesses Have About HMRC Audits

Several widely-held assumptions about HMRC audits lead businesses to either panic unnecessarily or underprepare. Here's what the evidence actually shows.

"Only large businesses or those with obvious errors get audited"

Random checks mean any compliant, well-run business can be selected. HMRC's Connect system flags minor discrepancies that business owners may not notice — a £200 expense coded to the wrong category can trigger a review if it creates an industry benchmark anomaly.

"An audit letter means I'm under criminal investigation"

Most businesses face aspect or random checks, not criminal investigations. Overreacting to a routine compliance letter delays resolution. Cooperating promptly and transparently typically leads to faster closure.

"Correcting an error voluntarily makes things worse"

HMRC considers whether taxpayers disclosed errors as soon as they could when determining penalties. Getting ahead of HMRC contact almost always reduces what you owe:

- Careless errors (unprompted disclosure): penalty reduced to 0%

- Careless errors (HMRC discovers first): minimum 15% penalty applies

- Deliberate errors (unprompted disclosure): minimum penalty drops from 35% to 20%

Frequently Asked Questions

What is a tax audit in the UK?

A UK tax audit (formally called an HMRC compliance check) is a review of your financial records and tax returns to verify correct tax payment. It covers Corporation Tax, VAT, PAYE, and Self Assessment, examining whether declared figures match supporting documentation.

What happens when you get audited in the UK?

HMRC notifies you by letter, specifies which records and tax years are under review, and conducts the audit remotely or via site visit. It concludes with a clean outcome, a tax correction and repayment demand (typically within 30 days), or a penalty notice.

What triggers a tax audit in the UK?

Common triggers include inconsistent figures, late or amended filings, operating in a high-risk industry (hospitality, construction, retail), tip-offs from third parties, or figures deviating significantly from industry benchmarks. HMRC's analytics team also selects businesses entirely at random to measure compliance across all sectors.

How likely is a tax audit in the UK?

The probability rises sharply when businesses file late, operate in scrutinised sectors, or show unexplained anomalies — though random checks can affect any business. With 316,000 checks completed in 2024-25, consistent recordkeeping is your best defence.

What income is most likely to get audited?

Self-employed income, cash-intensive business income (hospitality, trades, retail), and income with large or unexplained fluctuations attract the most scrutiny. These are harder to verify through third-party data, making them natural targets for compliance checks.

What is the 60% tax trap in the UK?

The 60% tax trap affects individuals earning between £100,000 and £125,140, where the Personal Allowance tapers away at a rate that creates an effective 60% marginal tax rate. While this is a personal tax issue rather than a direct audit trigger, unusual income management strategies in this bracket can attract HMRC attention.