Introduction

Many UK businesses share a surprisingly common problem: their chart of accounts doesn't align with what Companies House and HMRC actually require. Thousands of businesses face late filing penalties every year (ranging from £150 to £1,500), often because their accounting structure fails to produce compliant financial statements. The root cause is usually a poorly designed chart of accounts that doesn't map to UK GAAP requirements.

This guide covers how COA structure aligns with UK GAAP reporting obligations under FRS 102 or FRS 105 — relevant for UK limited companies, sole traders, foreign businesses operating in the UK, and finance professionals. In tools like Sage and Xero, a chart of accounts is easy to set up but easy to get wrong. Its specific requirements under UK GAAP are frequently misunderstood or conflated with US GAAP or IFRS. Getting it wrong leads to non-compliant accounts, HMRC scrutiny, and costly corrections.

Key Takeaways

- A chart of accounts lists every financial account in a general ledger across five categories: assets, liabilities, equity, income, and expenses

- UK GAAP requires COA alignment with FRS 102 (standard entities) or FRS 105 (micro-entities) for Companies House compliance

- Nominal codes, used by Sage and Xero, are the standard numbering system for organising UK accounts

- Updated April 2025: Micro-entity thresholds now sit at turnover under £1,000,000 and balance sheet under £500,000

- No single COA structure is mandated in the UK, but the FRS framework governs how accounts are categorised and reported

What Is a Chart of Accounts Under UK GAAP?

A chart of accounts is a complete, indexed list of every account a business uses to categorise financial transactions. This covers everything from sales revenue and fixed assets to employee wages and shareholder equity. Each account receives a unique nominal code (the UK term for numeric identifiers) for consistent recording and retrieval across your accounting system.

UK GAAP refers to accounting standards issued by the Financial Reporting Council (FRC), primarily FRS 102 (The Financial Reporting Standard applicable in the UK and Republic of Ireland) and FRS 105 (for micro-entities). A compliant chart of accounts must map directly to the financial statement line items these standards require.

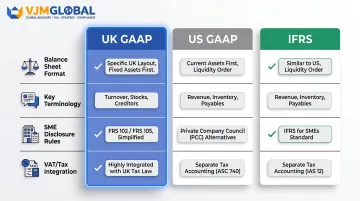

UK GAAP vs US GAAP vs IFRS

The five core account categories (assets, liabilities, equity, income, expenses) appear similar across frameworks, but crucial differences exist:

- Balance sheet formats: The Companies Act 2006 prescribes specific presentation formats (Format 1 vertical, Format 2 horizontal) with mandatory headings like "Creditors: amounts falling due within one year" (terminology absent from US GAAP)

- Terminology divergence: UK GAAP uses debtors, creditors, and stocks; US GAAP uses accounts receivable, accounts payable, and inventory

- Disclosure requirements: FRS 102 Section 1A (small entities) has no equivalent in IFRS for SMEs, creating different COA granularity needs

- VAT integration: UK COAs require separate input and output VAT tracking , which has no equivalent in US GAAP structures

UK listed companies must use UK-endorsed IFRS for consolidated accounts, while private companies typically follow UK GAAP (FRS 102 or 105). A COA built for US GAAP reporting is not directly transferable to UK statutory filings.

The Five Core Categories of a UK GAAP Chart of Accounts

Every UK GAAP chart of accounts is built around five fundamental categories — three feeding the balance sheet, two feeding the profit and loss (P&L) statement. Understanding each one determines how your nominal codes are structured and in what order they appear.

Assets

Asset accounts cover everything the business owns or controls with economic value, split into:

Fixed assets (appearing first in Format 1 balance sheet):

- Tangible: property, plant, equipment, motor vehicles

- Intangible: goodwill, patents, trademarks, software licences

Current assets:

- Cash at bank and in hand

- Trade debtors (receivables)

- Prepayments

- Stock (inventory)

Under the Companies Act 2006 Format 1, fixed assets appear above current assets — this statutory order determines your nominal code sequence.

Liabilities

Liability accounts record what the business owes, divided per statutory requirements:

Creditors falling due within one year (current liabilities):

- Trade creditors

- VAT payable

- PAYE and National Insurance payable

- Accruals

- Bank overdrafts

Creditors falling due after more than one year (long-term):

- Bank loans

- Debentures

- Hire purchase obligations

The statutory split between "within one year" and "after more than one year" is mandatory — your COA must support this categorisation.

Equity

Equity accounts represent the residual interest after liabilities are deducted from assets.

For limited companies, this includes share capital, share premium, retained earnings, and revaluation reserves. For sole traders and partnerships, capital accounts and drawings replace share capital and dividends.

Income and Expenses

These accounts feed your profit and loss statement.

Income accounts:

- Turnover/sales revenue

- Other operating income

- Interest receivable

Expense accounts follow one of two classification methods under UK GAAP — by function or by nature — and you must apply whichever you choose consistently across all reporting periods.

By function (Formats 1 & 3):

- Cost of sales

- Distribution costs

- Administrative expenses

By nature (Formats 2 & 4):

- Raw materials and consumables

- Staff costs

- Depreciation

- Other operating charges

The method you select shapes every expense account in your COA — switching mid-year requires restating prior period comparatives, so the decision carries real practical weight.

How UK GAAP Standards Shape Your Chart of Accounts

FRS 102 vs FRS 105: Different Standards, Different COAs

FRS 102 applies to most UK companies (small, medium, and large), requiring a full balance sheet and P&L with specific line items and disclosure notes.

FRS 105 (micro-entities regime) permits substantially simplified financial statements. Critical update: From 6 April 2025, thresholds increased approximately 50%:

| Criterion | Threshold (from 6 April 2025) |

|---|---|

| Turnover | Not more than £1,000,000 |

| Balance sheet total | Not more than £500,000 |

| Number of employees | Not more than 10 |

Companies must meet at least two of three criteria. Micro-entities can use a much leaner COA with fewer income and expense sub-accounts.

FRS 102 Section 1A (small companies regime) creates a middle tier: simpler accounts than full FRS 102 entities but more detailed than FRS 105.

The VAT Dimension Unique to UK COAs

VAT-registered businesses must have accounts or sub-accounts that separately capture:

- Input VAT (recoverable VAT on purchases)

- Output VAT (VAT charged on sales)

Many UK accounting software solutions split sales and purchases by VAT rate:

- Standard rate: 20%

- Reduced rate: 5%

- Zero-rated: 0%

- Exempt

This granularity is specific to UK bookkeeping and has no direct equivalent in US GAAP COAs.

Making Tax Digital (MTD) Requirements

That VAT structure feeds directly into Making Tax Digital compliance — HMRC's digital reporting mandate requires businesses to maintain and submit precisely these records electronically.

MTD for VAT: Mandatory for all VAT-registered businesses since 1 April 2022. Businesses must:

- Keep digital records of all supplies and purchases

- Maintain separate input and output VAT tracking

- Transfer data between software via digital links (no manual cut-and-paste)

- File VAT returns using MTD-compatible software

MTD obligations extend beyond VAT. Sole traders and landlords face mandatory digital income tax reporting on a rolling timeline:

MTD for Income Tax Self Assessment (sole traders and landlords):

| Effective Date | Income Threshold |

|---|---|

| 6 April 2026 | Over £50,000 |

| 6 April 2027 | Over £30,000 |

| 6 April 2028 | Over £20,000 |

A loosely structured COA without proper income and expense categorisation creates MTD compliance problems. Your accounts must map directly to HMRC's digital reporting categories.

For foreign companies entering the UK market, getting this structure right from day one matters. VJM Global has worked with 250+ UK businesses on COA setup aligned to FRS 102/105 and HMRC's digital reporting requirements.

How to Set Up and Number a UK GAAP Chart of Accounts

Understanding Nominal Code Conventions

UK accounting practice uses numeric range systems where each category receives a number range. The most common Sage convention:

| Category | Sage Code Range |

|---|---|

| Assets | 0001 – 1999 |

| Liabilities | 2000 – 2999 |

| Capital (Equity) | 3000 – 3999 |

| Income | 4000 – 4999 |

| Direct Expenses | 5000 – 5999 |

| Overheads | 6000 – 9999 |

Xero uses different conventions (090–999 ranges), but the underlying logic of grouping by category remains consistent. Once you understand the structure, applying it is straightforward.

Practical Setup Steps

- Determine whether FRS 102, FRS 102 Section 1A, or FRS 105 applies to your business.

- List the balance sheet and P&L line items your reporting standard requires.

- Allocate nominal code ranges to each account category following your software's conventions.

- Add sub-accounts for UK-specific needs:

- VAT control accounts (input VAT, output VAT)

- Payroll accounts (PAYE, National Insurance, pension)

- Industry-specific categories (stock sub-categories for retail, WIP for manufacturing)

- Import or manually create accounts in your MTD-compatible accounting software.

Design for Scalability

Leave gaps in your numbering sequence to accommodate new accounts as your business grows. A slightly broader structure upfront beats recoding transactions later — for example, if you assign 4000–4099 to product sales, keep 4100–4199 free for service revenue you might add.

Software Default Templates

Sage 200, Xero, and QuickBooks provide default UK COA templates that follow UK GAAP conventions and include pre-mapped VAT codes. These are useful starting points but should be reviewed against your reporting needs and FRS obligations before using them as-is.

Common Mistakes and Misconceptions in UK GAAP COA Setup

Setting up a chart of accounts correctly from the start prevents costly compliance problems later. These are the most common mistakes UK businesses make.

Any Template Will Be UK GAAP Compliant

Many businesses assume generic "chart of accounts" templates found online or bundled with international software will automatically comply with UK GAAP. In reality, many templates are built for US GAAP (FASB) or IFRS and do not reflect:

- Companies Act 2006 balance sheet formats

- FRS 102 presentation requirements

- UK-specific items like VAT control accounts and PAYE/NI payables

Companies House can reject financial statements built on non-UK templates, resulting in late-filing penalties.

Under-Categorisation Problems

Many small UK businesses use oversimplified COAs with a single "expenses" account or fail to separate cost of sales from overheads. This:

- Prevents accurate gross profit calculation

- Makes P&L analysis meaningless

- Triggers HMRC scrutiny when tax returns lack expected breakdown of trading income and allowable expenses

- Fails to meet statutory presentation requirements

Confusing COA with Financial Statements

The COA is the structural framework from which reports are generated, not the reports themselves. Changes to the COA mid-year — renaming, merging, or deleting accounts — can:

- Distort comparative figures in year-end accounts

- Create reconciliation problems during audit

- Complicate HMRC reviews

To avoid these problems, make account changes only at year-start or with professional guidance.

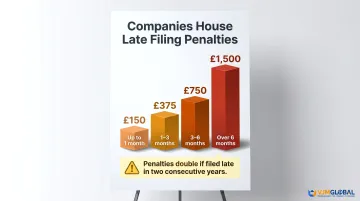

Compliance Penalties

Each of the above mistakes can ultimately feed into late or rejected filings. Companies House late filing penalties for private companies are:

| Period Late | Penalty |

|---|---|

| Not more than 1 month | £150 |

| More than 1 month but not more than 3 months | £375 |

| More than 3 months but not more than 6 months | £750 |

| More than 6 months | £1,500 |

Penalties double if accounts are filed late in two successive years. Not filing is a criminal offence that can result in director prosecution.

Frequently Asked Questions

What is the standard chart of accounts GAAP?

There is no single universally mandated "standard" COA under GAAP. Both UK GAAP and US GAAP define categories and presentation requirements for financial statements, but each business structures its own COA to meet those requirements. In the UK, the COA must align with FRS 102 or FRS 105 and the Companies Act 2006 formats rather than following one prescribed list.

Does the UK use GAAP accounting?

Yes — UK GAAP is a set of accounting standards issued by the Financial Reporting Council (FRC), primarily FRS 102 and FRS 105. It is separate from both US GAAP and IFRS, and governs how most UK private companies prepare and file their accounts.

What are the 7 basic accounting categories?

The foundational model uses five categories: assets, liabilities, equity, income, and expenses. Some frameworks expand this to seven by separating cost of sales from operating expenses and splitting out non-operating income or contra accounts. UK GAAP COAs typically start with the five core categories, with sub-categories added for business complexity.

What is FRS 102 and how does it affect the chart of accounts?

FRS 102 is the primary UK GAAP standard, covering most UK companies that are neither micro-entities nor listed. It sets required formats for the balance sheet and profit and loss account, which directly shapes how accounts must be structured and categorised in the COA.

What are nominal codes in UK accounting?

Nominal codes are numeric identifiers assigned to each COA account, used by software such as Sage, Xero, and QuickBooks to categorise and retrieve transactions. Each number range maps to a category (assets, liabilities, income, expenses), and consistent use ensures accurate reporting and audit readiness.

Do micro-entities need a different chart of accounts under FRS 105?

Yes. FRS 105 allows simplified financial statements with fewer required line items, so the COA can be leaner with fewer income and expense sub-accounts. Eligibility requires meeting all three thresholds: turnover under £1,000,000, balance sheet under £500,000, and fewer than 10 employees (from April 2025). The COA must still support VAT and tax reporting.