Introduction

Fair value accounting represents a significant departure from traditional historical cost accounting and has become a central pillar of financial reporting under FRS 102 — the primary accounting framework for UK companies that do not use IFRS. With an estimated 3.4 million entities falling under UK GAAP standards, FRS 102 affects SMEs, subsidiaries of foreign-owned companies, and businesses across virtually every sector.

Many UK businesses struggle to identify which assets require fair value measurement, how to determine that value, and what the resulting impact is on their financial statements and tax position.

The FRC's Annual Review of Corporate Reporting 2024/25 consistently flags financial instruments as one of the top three problem areas — citing recurring failures in initial measurement, unclear accounting policies, and embedded derivatives that go unidentified.

This article breaks down the FRS 102 fair value framework — definition, scope, hierarchy, tax implications, and where most businesses go wrong — so you can stay compliant and avoid the disclosure failures the FRC flags most often.

TLDR:

- Fair value accounting under FRS 102 applies to specific asset classes, not all assets

- Financial instruments split into "basic" (Section 11) and "complex" (Section 12) categories, each with distinct measurement rules

- The 2024 amendments introduce a three-level fair value hierarchy aligned with IFRS 13

- Fair value movements on certain instruments flow through profit or loss, creating tax volatility

- Top compliance failures: misclassifying instruments and inadequate disclosure of valuation assumptions

What Is Fair Value Accounting and How Does FRS 102 Define It?

FRS 102 defines fair value as the amount for which an asset could be exchanged, a liability settled, or an equity instrument granted, between knowledgeable, willing parties in an arm's length transaction.

This differs from historical cost accounting, where assets are recorded at their original purchase price and remain at that value — less depreciation or impairment — until disposal.

Fair value accounting reflects the current economic reality of an asset or liability, giving investors, lenders, and other users a clearer picture of what those assets and liabilities are actually worth today.

Critical clarification: FRS 102 does not require all assets to be measured at fair value. It mandates fair value for specific categories — particularly certain financial instruments and investments — while requiring or permitting cost or amortised cost for others. This selective application is a common source of confusion and misclassification.

Financial Instrument Classification: Section 11 vs Section 12

Where fair value applies depends on how an instrument is classified. FRS 102 separates financial instruments into two categories that determine the measurement approach:

Section 11 (Basic Financial Instruments): Covers cash, demand deposits, trade receivables/payables, simple loans and bonds, and investments in non-convertible preference shares or non-puttable ordinary shares. To qualify as "basic," a debt instrument's contractual returns must be a fixed amount, a positive fixed or variable rate, or a combination of both.

Section 12 (Other/Complex Financial Instruments): Covers all remaining financial instruments, including all derivatives.

The 2024 Fair Value Amendments

The 2024 Periodic Review amendments — effective for periods beginning on or after 1 January 2026 — redefine fair value as "the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date." The definition is market-based, reflecting what participants would agree to, not what a specific entity estimates.

The revised definition is introduced via a new Section 2A of FRS 102, replacing the previous appendix on fair value measurement and bringing FRS 102 more closely in line with IFRS 13 Fair Value Measurement. Key concepts now incorporated include:

- Market participants (knowledgeable, willing, and able buyers/sellers)

- Principal market vs most advantageous market

- Highest and best use for non-financial assets

- Shift from "settlement" to "transfer" concept for liabilities

While FRS 102 entities are not directly required to apply IFRS 13, the concepts of market participants, principal markets, and the fair value hierarchy are now broadly consistent across both frameworks.

Which Assets and Liabilities Are Subject to Fair Value Measurement Under FRS 102?

FRS 102 applies different measurement bases across asset categories — fair value, amortised cost, and cost less impairment — depending on the nature of the instrument and the applicable section.

Section 11: Basic Financial Instruments

Measurement hierarchy for basic instruments:

- Debt instruments (loans, bonds): Measured at amortised cost using the effective interest method

- Short-term trade receivables/payables (due within one year): May be measured at undiscounted cash amounts where the arrangement does not constitute a financing transaction

- Financing transactions at non-market rates (e.g., interest-free loans, debts with below-market rates): Initially measured at the present value of future payments discounted at a market rate of interest

- Equity instruments (non-convertible preference shares, non-puttable ordinary shares): Measured at fair value through profit or loss (FVTPL) if fair value can be measured reliably; otherwise at cost less impairment

Section 12: Other Financial Instruments

Instruments under Section 12 are generally required to be measured at fair value with changes recognised in profit or loss (FVTPL).

Three key exceptions:

- Investments in equity instruments that are not publicly traded and whose fair value cannot be reliably measured — measured at cost less impairment

- Contracts linked to such instruments

- Certain hedging instruments designated in an eligible hedging relationship

Beyond financial instruments, two categories of non-financial assets also carry mandatory fair value requirements.

Investment Property (Section 16)

Investment property must be measured at fair value at each reporting date, with changes recognised in profit or loss. Where fair value cannot be determined reliably without undue cost or effort, the property falls under Section 17 (Property, Plant and Equipment) using the cost-depreciation-impairment model.

Following the Triennial Review, the "undue cost or effort" exemption was removed for properties rented to third parties — it had been misapplied as a discretionary accounting policy choice. For intra-group investment property, entities may still elect either the fair value model or the cost model.

Biological Assets (Section 34)

Biological assets related to agricultural activity are measured at fair value less costs to sell, with changes recognised in profit or loss. Agricultural produce harvested from biological assets is measured at fair value less costs to sell at the point of harvest.

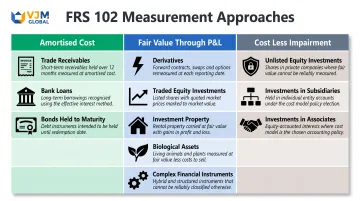

Summary Table: Fair Value vs Cost-Based Measurement

| Asset Category | Measurement Approach |

|---|---|

| Amortised Cost | |

| Trade receivables (>1 year) | Amortised cost using effective interest method |

| Bank loans, bonds (held to maturity) | Amortised cost using effective interest method |

| Fair Value Through Profit or Loss | |

| Derivatives (all types) | Fair value with changes in P&L |

| Traded equity investments | Fair value with changes in P&L |

| Investment property | Fair value with changes in P&L |

| Biological assets | Fair value less costs to sell |

| Complex financial instruments (Section 12) | Fair value with changes in P&L |

| Cost Less Impairment | |

| Unlisted equity investments (fair value unreliable) | Cost less impairment |

| Investments in subsidiaries (if policy chosen) | Cost less impairment |

| Investments in associates (if policy chosen) | Cost less impairment |

The Fair Value Hierarchy: How to Determine Fair Value in Practice

The 2024 amendments to FRS 102 introduce a three-level fair value hierarchy that determines how fair value is established, consistent with IFRS 13:

Level 1: Quoted Prices in Active Markets

The most reliable measure. Uses quoted prices in active markets for identical or comparable assets or liabilities.

For instance, if you hold ordinary shares in a FTSE 100 company, you use the closing market price on the reporting date — a straightforward, market-verified figure.

Level 2: Observable Market Inputs

Uses observable inputs other than Level 1 quoted prices, such as quoted prices for similar assets, interest rate yield curves, or observable market transactions.

In practice, a corporate bond with no active market can be priced using yield spreads over UK Gilts — drawing on observable data from similar bonds with comparable credit ratings and maturities.

Level 3: Unobservable Inputs

The least reliable and most judgement-heavy. Based on the entity's own assumptions where no active market exists.

Shares in a private unlisted company, for example, are typically valued using a discounted cash flow (DCF) model. You must assume future cash flows, growth rates, and discount rates — none of which are directly observable in the market.

Disclosure Requirements

Choosing the right level is only half the obligation — you also need to disclose how you got there. Entities must:

- Disclose the level used for each fair value measurement

- For Level 3 measurements, provide detailed information about the assumptions used and sensitivity of those values to changes in assumptions

These requirements carry real teeth. The FRC's Annual Review 2024/25 flagged inadequate fair value disclosure as one of the most common compliance failures, with recurring problems that include:

- Discount rates applied inconsistently regarding risk profiles

- Key inputs for valuation lacking external support

- Insufficient transparency about assumptions and methodologies

Fair Value Accounting for Investments Under FRS 102

Investment accounting under FRS 102 depends critically on the type of investment and the entity's relationship to the investee.

Investments in Subsidiaries, Associates, and Joint Ventures

Sections 9, 14, and 15 of FRS 102 provide specific treatment options for these investments in individual (standalone) financial statements. An entity may choose to measure these at:

- Cost less impairment

- Fair value through Other Comprehensive Income (OCI)

- Fair value through profit or loss

The chosen policy must be applied consistently. The fair value through profit or loss option creates volatility in the income statement, which may affect distributable reserves and dividend capacity.

Minority Equity Stakes (No Significant Influence)

For equity investments that do not confer significant influence:

- If publicly traded or fair value reliably measurable: Must be measured at fair value through profit or loss

- If fair value cannot be reliably measured (e.g., a small stake in a private company): Held at cost less impairment

Under old UK GAAP, entities could revalue investments to a director's estimated value via a revaluation reserve. FRS 102 closes that door: unrealised fair value gains on equity investments measured at FVTPL must now flow through the income statement, not through Other Comprehensive Income. This directly affects distributable profits and requires careful consideration before selecting the FVTPL policy.

Journal Entry Logic for Fair Value Movements

Initial recognition:

- Debit: Investment account (at transaction price/cost)

- Credit: Cash/Bank

Subsequent measurement (if at FVTPL):

- If value increases: Debit Investment account / Credit Fair value gain (profit or loss)

- If value decreases: Debit Fair value loss (profit or loss) / Credit Investment account

Because these gains are unrealised, entities may choose to ring-fence them within equity in a non-distributable reserve to prevent inappropriate distributions.

Impairment for Cost-Held Investments

For investments carried at cost rather than fair value, the measurement approach shifts from market-based assessment to an indicators-of-impairment review. At each reporting date, entities must assess whether impairment indicators exist — such as significant deterioration in the investee's financial position or adverse changes in the market environment.

If impairment exists:

- Reduce the carrying value to its recoverable amount

- Recognise the loss in profit or loss

- Note that impairment losses on cost-held investments generally cannot be reversed under FRS 102, unlike fair value movements through profit or loss

Tax Implications of Fair Value Accounting Under UK GAAP

HMRC's loan relationship and derivative contract rules broadly follow the accounting treatment under GAAP, meaning fair value gains and losses recognised in profit or loss under FRS 102 are generally brought into the corporation tax computation in the same period. This alignment creates potential tax volatility — and understanding where the rules diverge from accounting is critical for accurate tax planning.

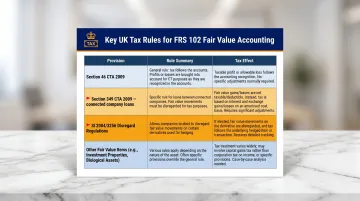

Key Tax Principles

| Provision | Rule | Effect |

|---|---|---|

| Section 46 CTA 2009 | Trading profits calculated in accordance with GAAP, subject to legal adjustments | Tax base follows accounting entries |

| Part 5 & Part 7 CTA 2009 | Loan relationships and derivative contracts follow accounting treatment | Fair value movements in P&L or OCI brought into corporation tax account |

| Section 349 CTA 2009 | Connected company loans taxed on amortised cost basis regardless of accounting policy | Prevents fair value volatility between related entities |

| SI 2004/3256 (Disregard Regulations) | Certain fair value movements on hedging derivatives can be "disregarded" for tax | Restores accruals-based treatment; avoids tax charge on unrealised hedging gains/losses |

Specific Risk: Derivatives and Complex Instruments

Entities that previously did not recognise derivatives under old UK GAAP (because they were not applying FRS 26) must now recognise and measure them at fair value under FRS 102. This can produce three distinct exposures:

- A significant one-off tax adjustment on transition to FRS 102

- Ongoing volatility in taxable profits from mark-to-market (period-end fair value) movements

- Potential mismatches where hedging relationships are economically effective but not tax-neutral without the Disregard Regulations

Investment Property Fair Value Movements

Fair value movements on investment property recognised in P&L are generally not taxable as income. Instead, disposal of the property typically gives rise to a chargeable gain (capital) for tax purposes. Tax law departs from accounting by not following P&L fair value movements for capital assets.

This capital/income distinction matters for cash flow planning — a property showing large annual fair value gains in the accounts may carry no current-year tax liability until disposal.

Transition Adjustments

HMRC has published specific transitional guidance for entities moving from old UK GAAP to FRS 102:

- Sections 315–319 and 613–615 CTA 2009 ensure no amounts fall out of account due to the change in accounting framework

- Chapter 14 Part 3 CTA 2009 provides "change of basis" adjustments so receipts and deductions are taxed exactly once

- COAP Regulations (SI 2004/3271): Transitional adjustments for loan relationships and derivatives are generally spread over 10 years, starting from the period of transition — spreading does not apply to instruments repaid or redeemed in the transition period

The 10-year spreading rule under COAP can significantly smooth the tax impact of transition — but it requires careful identification of qualifying instruments before the transition period closes.

Common Challenges and Practical Compliance Tips for UK Businesses

Most Common Practical Challenges

1. Identifying "basic" vs "other/complex" financial instruments

The distinction between Section 11 and Section 12 determines the measurement approach entirely. Many entities struggle to assess whether a debt instrument qualifies as "basic" under the Section 11.9(a) test (contractual returns that are a fixed amount, a positive fixed or variable rate, or a combination thereof). If it fails the test, the entire instrument falls to Section 12 and must be measured at FVTPL.

2. Determining fair value for Level 3 instruments

When no market exists, entities must develop robust documentation of assumptions and methodology. The FRC's findings show that many entities fail to provide adequate support for key inputs such as discount rates, growth assumptions, or valuation multiples.

3. Identifying embedded derivatives

Loan agreements may contain embedded derivatives (for example, interest rate swaps bundled into bank loan agreements, conversion features, early redemption penalties linked to market indices). Unlike FRS 26 or IAS 39, FRS 102 does not require bifurcation (separation) of embedded derivatives from a host contract.

Instead, the entire instrument is assessed as either basic (Section 11) or other (Section 12). If it fails the basic test, the whole contract is measured at fair value under Section 12.

Practical Compliance Tips

Maintain detailed documentation:

- Document the valuation methodology and inputs for every asset measured at fair value

- Keep records of market data sources, discount rate calculations, and sensitivity analyses

- Update documentation annually and retain evidence of reviews

Review loan agreements systematically:

- Review all loan contracts at the point of transition to FRS 102

- Conduct annual reviews to identify any new financing arrangements with non-market terms or embedded features

- Pay particular attention to interest-free loans, convertible debt, and vendor financing arrangements

Establish clear accounting policies:

- Document the accounting policy for investment classifications (cost, fair value, or equity method for subsidiaries and associates)

- Apply policies consistently across periods

- Disclose policies clearly in the notes to the financial statements

Ensure disclosures are specific, not boilerplate:

- Avoid generic disclosure language that could apply to any entity

- Provide specific information about valuation techniques, inputs, and assumptions used

- For Level 3 measurements, include sensitivity analysis showing the impact of changes in key assumptions

When to Seek Professional Support

Even with clear policies in place, FRS 102 compliance can be difficult to manage when cross-border transactions, complex instruments, or Level 3 valuations are involved. Professional support reduces the risk of misclassification and non-compliant disclosures before they become audit findings.

VJM Global supports UK-based businesses and foreign-owned UK entities in meeting their FRS 102 obligations accurately and on time. With experience serving over 250 UK businesses across 15+ industries, the firm handles cross-border accounting, international tax planning, and financial reporting compliance — particularly for entities with India-facing operations.

Frequently Asked Questions

Is fair value accounting allowed under GAAP?

Yes, fair value accounting is both permitted and required in specific cases under UK GAAP (FRS 102), particularly for complex financial instruments, certain investments in publicly traded shares, investment properties, and biological assets. Other instruments such as basic loans and trade receivables are measured at amortised cost or undiscounted amounts.

Does the UK use IFRS or GAAP?

The UK uses both: publicly listed companies on UK markets are required to use UK-adopted IFRS for consolidated financial statements, while most private companies and non-listed entities prepare accounts under UK GAAP (primarily FRS 102), which is overseen by the Financial Reporting Council.

Is FRS 102 the same as IFRS?

FRS 102 is not the same as IFRS, though it was developed with reference to the IFRS for SMEs standard and shares many concepts. Key differences include UK-specific provisions, simplified disclosure requirements, and distinct options for investment property and financial instrument classification.

Is FRS 102 the same as UK GAAP?

FRS 102 is the primary standard within UK GAAP and applies to most UK entities, but the full framework also includes FRS 100 (application guidance), FRS 101 (reduced disclosure for qualifying subsidiaries), and FRS 105 (micro-entities).

What is FRS 102 accounting for investments?

Under FRS 102, treatment depends on investment type. Subsidiaries, associates, and joint ventures in individual accounts may be held at cost, fair value through OCI, or fair value through profit or loss. Minority stakes in listed entities are measured at fair value through profit or loss; stakes in private companies where fair value is unreliable are carried at cost less impairment.

What is the journal entry for investment accounting?

On initial recognition, debit the investment account and credit cash/bank at cost. At subsequent reporting dates under fair value through profit or loss, debit the investment account and credit fair value gains in profit or loss — or reverse if the value has fallen. Actual entries vary by investment classification.