Introduction

Many Indian business owners assume closing a UAE company is as simple as letting the trade license lapse. It isn't. Under Federal Decree-Law No. 32 of 2021 on Commercial Companies, every business closure requires formal liquidation — a structured legal process of settling liabilities and removing the company from the commercial register.

Letting a license expire without formal liquidation keeps the company legally alive, triggering accumulating fines and penalties.

For Indian business owners, the complexity doubles. Beyond UAE requirements, you must also manage Indian obligations — FEMA compliance, RBI reporting, and Schedule FA disclosure under the Income Tax Act.

Miss either side, and the consequences are serious: travel bans in the UAE, or penalties up to ₹10 lakh per year in India under the Black Money Act. This guide walks through both jurisdictions step by step, so you can close cleanly without surprises.

Key Takeaways

- Formal liquidation is legally mandatory — expired trade licenses create ongoing liability, not closure

- Penalties, fines, and director liabilities (including blacklisting risk) accumulate until formal deregistration is complete

- Indian residents must file Form FC-TRS with RBI within 30 days of fund repatriation

- Schedule FA disclosure in Indian tax returns is required until liquidation is complete

- Timelines vary by entity type: 2–3 months for dormant mainland companies, up to 12 months for active free zone entities

What Is Company Liquidation in the UAE?

Company liquidation (also called winding up) is the legal process of dissolving a company, selling assets, settling outstanding debts and employee dues, and deregistering the entity from the commercial register. Once complete, the company ceases to exist as a legal person.

Two main types exist:

- Voluntary liquidation — shareholders initiate this when closure is a deliberate business decision; it's the most common route for Indian owners exiting the UAE market

- Compulsory liquidation — a court orders this, typically when a company is insolvent or has breached regulatory obligations

For mainland companies, the legal basis for both types sits in Article 302 of Federal Decree-Law No. 32/2021, which recognises dissolution grounds including unanimous partner consent, term expiration, achievement of company objectives, and court-ordered dissolution due to asset loss.

Jurisdiction Matters

The liquidation process differs significantly by company type:

| Company Type | Governing Authority | Regulation |

|---|---|---|

| Mainland (LLC) | Department of Economy and Tourism (DET) | Federal Decree-Law No. 32/2021 |

| DMCC Free Zone | DMCC Authority | DMCC Company Regulations 2020 |

| JAFZA Free Zone | JAFZA Authority | JAFZA Company Regulations |

| RAK ICC Offshore | RAK International Corporate Centre | RAK ICC Regulations |

Creditor notice periods alone illustrate how much the rules diverge: mainland companies must wait 45 days, while DMCC requires just 14 calendar days. Documentation requirements and overall timelines vary just as significantly across these jurisdictions.

Why Proper Liquidation Is Legally Mandatory in the UAE

A company's legal obligations don't end when operations stop or a license expires. The UAE legal framework keeps imposing penalties until formal liquidation is complete.

Specific consequences of not formally liquidating:

- License renewal penalties, VAT non-filing fines, and Corporate Tax penalties (AED 10,000+) continue to accumulate

- Director liability — under Article 162 of Federal Decree-Law No. 32/2021, directors can be held personally liable for management errors

- Travel bans — founders who leave the UAE without proper liquidation may be denied future access into the country until all debts and penalties are repaid

- Employee dues and end-of-service gratuity payments remain legally owed regardless of whether the business is active

- Future business restrictions — unresolved closures block new UAE trade licenses and prevent opening any future entity

For Indian nationals, the consequences don't stop at UAE borders. Improper closures create a second layer of legal exposure back home.

The India Connection

Failing to formally liquidate a UAE company can trigger scrutiny under Indian tax and foreign exchange laws:

- Disclose unresolved foreign assets on Schedule FA — skipping this step violates Indian income tax law

- FEMA reporting failures and RBI scrutiny

- Income tax notices for undisclosed foreign shareholdings

- ₹10 lakh penalty per year under Section 43 of the Black Money Act for non-disclosure

- Potential imprisonment up to 7 years under Indian tax laws

The CBDT receives automated reports through CRS (Common Reporting Standard) and FATCA data exchange, making unreported foreign assets easier to detect than ever before.

How UAE Company Liquidation Works: Step-by-Step

UAE company liquidation follows a mandatory sequence: shareholder resolution → liquidator appointment → public notice → clearances → audit → deregistration. Every step must be completed in full — authorities do not recognize partial or incomplete liquidations.

Shareholder Resolution

The process begins with a formal board or shareholder resolution approving liquidation. This resolution must be:

- Notarized by a UAE public or private notary

- Include the name of the appointed liquidator

- Submitted to the relevant licensing authority (DET for mainland, specific free zone authority for free zones)

Appoint a Licensed Liquidator

Article 316 of Federal Decree-Law No. 32/2021 requires a licensed and registered liquidator — typically an approved audit firm — to oversee the winding up. The liquidator cannot be a current or recent auditor of the same company.

Liquidator responsibilities include:

- Asset inventory and valuation

- Debt settlement coordination

- Employee dues calculation and payment

- Preparation of final Statement of Affairs

- Government filing coordination

Publish Liquidation Notice

Mainland companies must publish a liquidation notice in two Arabic-language local newspapers, giving creditors 45 days to file claims. Publication costs range from AED 500–2,000 per newspaper.

During this period, the company must:

- Cease all new business activities

- Begin clearing outstanding liabilities

- Respond to any creditor claims filed

Free zone timelines differ — DMCC companies, for example, have a shorter 14-day publication window rather than the 45-day mainland requirement.

Obtain Clearance Certificates (NOCs)

No Objection Certificates must be secured from multiple government authorities before final deregistration:

- Federal Tax Authority (FTA) — VAT and Corporate Tax deregistration (approximately 20 business days)

- Ministry of Human Resources and Emiratisation (MOHRE) — labour card cancellations and employee gratuity settlements

- General Directorate of Residency and Foreigners Affairs (GDRFA) — visa cancellations

- Utility providers — DEWA, Etisalat, du account closures

- Landlord — lease termination and Ejari cancellation

- Dubai Customs — required for DMCC trading licenses

Each NOC must be obtained before the licensing authority will proceed — a single missing clearance puts the entire deregistration on hold.

Submit Final Audit Report

The liquidator prepares a final audit report (Statement of Affairs) covering:

- Complete asset inventory

- All liabilities and settlements

- Employee dues paid

- Debt repayments completed

- Remaining balances and distribution plan

This document must be verified and approved by the licensing authority before deregistration.

Obtain Final Liquidation Certificate

Once all clearances are verified and the audit report is approved, the licensing authority issues a Final Liquidation Certificate and cancels the trade license. The company is formally deregistered at this point. In Dubai mainland, the trade license cancellation fee is AED 520; free zone fees vary by authority.

Costs, Timelines, and Key Documents

Indicative Cost Ranges

Based on 2025–2026 industry data:

| Component | Cost (AED) |

|---|---|

| Mainland (LLC) total deregistration | 15,000 – 35,000 |

| Major free zones (DMCC, DIFC, ADGM) | 20,000 – 50,000+ |

| Northern Emirates free zones (RAKEZ, SHAMS) | 10,000 – 25,000 |

| RAK ICC offshore | 3,000 – 7,000 |

| Arabic newspaper advertisement (per paper) | 500 – 2,000 |

| Board resolution notarisation | 500 – 1,500 |

| Dissolution certificate (Dubai) | 520 |

The largest variable component is liquidator fees, which are negotiated privately based on company complexity.

Typical Timelines

| Company Type | Duration |

|---|---|

| Dormant company (no employees, no VAT) | 2–3 months |

| Active mainland (1–5 employees, VAT registered) | 4–6 months |

| Active free zone (JAFZA/DMCC, 6+ employees) | 6–12 months |

| Northern Emirates free zones | 3–5 months |

| DMCC summary winding-up | Up to 6 months |

These timelines assume documents are complete and liabilities are cleared upfront. Delays in NOC processing or pending employee visa cancellations are the most common causes of extended timelines.

Having the right documents ready before you begin is the single biggest factor in keeping your liquidation on schedule. Here is what Dubai Mainland LLC owners need to prepare.

Core Documents Required

Dubai Mainland LLC

Company & Legal Documents:

- Notarized minutes of the General Assembly meeting

- Liquidator's acceptance letter and license copy

- Notarized liquidator signature specimen

- Trade license copy

- Memorandum of Association (MOA) with all amendments

- Auditor registration certificate

Clearance & Compliance Documents:

- Original newspaper advertisement clippings

- Final Liquidation Report / Statement of Affairs

- Declaration letter (no objections received within 45 days)

- Visa cancellation proof from MOHRE and GDRFA

- Passport copies and Emirates IDs of all partners

- Lease termination documents

Free zone liquidations (DMCC, JAFZA, DIFC, ADGM) follow authority-specific checklists that differ from the mainland requirements above. Contact your free zone authority directly — or a licensed liquidation consultant — to obtain the current document list before starting the process.

India-Specific Considerations When Winding Up a UAE Company

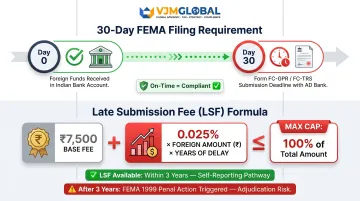

FEMA Reporting — The 30-Day Deadline

Under the Foreign Exchange Management (Overseas Investment) Directions, 2022 (A.P. DIR Series Circular No. 12):

Indian residents must file Form FC with their Authorised Dealer (AD) bank within 30 days of receiving disinvestment proceeds from the UAE liquidation.

Key requirements:

- Form FC must be certified by a Chartered Accountant for individuals where statutory audit is not applicable

- All disinvestment proceeds must be repatriated before filing

- Late Submission Fee (LSF) applies for delays: ₹7,500 + (0.025% × amount × years of delay), capped at 100% of amount

- LSF option available for up to 3 years from due date

- After 3 years, penal action under FEMA 1999 is triggered

- AD banks cannot facilitate further outward remittances until reporting delays are regularised

Critical: Coordinate UAE liquidation timelines with Indian filing deadlines. The 30-day clock starts when funds hit your Indian bank account, not when UAE deregistration is complete.

Schedule FA — Foreign Assets Disclosure

Under the Income Tax Act, 1961 and the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015, Resident and Ordinarily Resident (ROR) Indian taxpayers must disclose all foreign assets in Schedule FA (Foreign Assets) when filing ITR-2 or ITR-3.

What to disclose:

- Financial interests in any foreign entity (including UAE companies)

- Foreign bank accounts

- Immovable property outside India

- Capital assets located abroad

Foreign shareholdings in UAE entities must be reported every year until formal liquidation is complete and confirmed by UAE authorities.

Penalties for non-disclosure:

- ₹10 lakh penalty per year under Section 43 of the Black Money Act

- Undisclosed foreign income/assets taxed at flat 30% (no deductions or exemptions)

- Non-reporting treated as "wilful evasion of tax"

- Imprisonment up to 7 years under the Income Tax Act

2026 Update: Budget 2026 provides immunity from prosecution for non-disclosure of foreign movable assets up to ₹20 lakh (effective October 1, 2026), but penalties still apply.

Beyond disclosure obligations, the India-UAE tax treaty directly affects how your liquidation proceeds are taxed — and in some cases, can reduce that liability significantly.

India-UAE DTAA — Capital Gains Treatment

The Agreement for Avoidance of Double Taxation between India and UAE (signed April 29, 1992) governs how liquidation proceeds are taxed.

Article 13(5) — Residual Clause:

Gains from alienation of property not covered by paragraphs 1-4 are taxable only in the state of the alienator's residence.

Since the UAE levies no personal capital gains tax, UAE-resident Indian nationals can achieve 0% taxation on most liquidation distributions.

Compliance requirements to claim treaty benefits:

- Obtain Tax Residency Certificate (TRC) from UAE FTA

- File Form 10F electronically with Indian Income Tax Department

- For remittances to India exceeding ₹5 lakh, file Forms 15CA/15CB (15CB is a CA certificate)

Indian residents who have already returned to India will be taxed in India on capital gains; DTAA benefits apply primarily to UAE tax residents.

Practical Operational Challenges

Managing the process remotely from India:

- Most UAE liquidation steps require in-person notarizations or original documents

- Power of Attorney (POA) solution: A notarized POA allows a UAE-based representative to handle dissolution procedures, filings, asset management, and government submissions on your behalf

- POA must include company name, type, address, capital, number of partners, and purpose exactly as per Commercial Register

- POA can be initiated remotely through UAE notary offices

Coordination complexity:

- UAE liquidators need final instructions on fund distribution

- Indian CA needs UAE liquidation timeline to prepare Schedule FA and Form FC

- Indian AD bank needs proof of disinvestment and repatriation documentation

- Both processes must run in parallel, not sequentially

Running these two compliance tracks in parallel — UAE deregistration and Indian filings — is where most business owners hit delays. VJM Global coordinates both sides: managing UAE exit timelines alongside FEMA reporting, Schedule FA disclosures, and DTAA assessment so nothing falls through the gap.

Common Mistakes Indian Business Owners Make (and How to Avoid Them)

Assuming an Expired License Means Closure

Many Indian business owners assume that once a trade license lapses, the company is effectively closed. It isn't. RAK ICC explicitly confirms that struck-off companies "continue to exist until liquidated" and members/directors remain liable. Mainland companies continue accumulating license renewal fines, VAT penalties, and potential Corporate Tax fines until formal liquidation is completed.

How to avoid: Initiate formal liquidation before leaving the UAE, or execute a Power of Attorney enabling a representative to complete the process remotely.

Starting Liquidation with Outstanding Liabilities

Starting the liquidation process before clearing all liabilities is one of the most common—and costly—mistakes. Outstanding employee gratuity, unpaid VAT filings, or unresolved utility accounts will block NOC approvals from MOHRE, FTA, or service providers. Each unresolved item can extend your timeline by months.

How to avoid: Before notarizing the shareholder resolution:

- Settle all employee gratuity and outstanding salaries

- File all pending VAT returns and pay any outstanding amounts

- Close utility accounts (or transfer to new tenants)

- Clear any bank overdrafts or loans

Failing to Inform Indian Authorities

Indian business owners often focus entirely on UAE-side procedures and overlook their reporting obligations back home. Failing to notify RBI and Indian tax authorities of the entity closure and fund repatriation carries serious consequences:

- FEMA violations and LSF penalties (₹7,500 + 0.025% × amount × years)

- Income tax notices for undisclosed foreign assets

- ₹10 lakh penalty per year for Schedule FA non-disclosure

- Future overseas investment restrictions

To stay compliant on the Indian side:

- File Form FC with AD bank within 30 days of receiving disinvestment proceeds

- Continue filing Schedule FA in ITRs until UAE liquidation certificate is received

- Consult a CA experienced in cross-border compliance to coordinate UAE and Indian timelines

- Obtain and retain UAE Tax Residency Certificate if claiming DTAA benefits

Frequently Asked Questions

What is company liquidation in the UAE?

Company liquidation is the formal legal process of dissolving a UAE-registered business, settling all debts, liabilities, and employee dues, and removing the company from the commercial register. After completion, the company ceases to exist as a legal entity.

How much does it cost to liquidate a company in the UAE?

Costs vary by company size, jurisdiction, and number of employees. Mainland entities typically cost AED 15,000–35,000, major free zones AED 20,000–50,000+, and RAK ICC offshore entities AED 3,000–7,000. Key components include liquidator fees, newspaper advertisements, visa cancellations, and authority charges.

How long does it take to liquidate a company in the UAE?

Timelines vary by jurisdiction and document readiness. Dormant companies take 2–3 months, active mainland companies 4–6 months, and major free zone entities 6–12 months. The mandatory creditor notice period is 45 days (mainland) or 14 days (DMCC).

Can I liquidate a UAE company while living in India?

Yes, through a properly executed Power of Attorney. The POA must be notarized and authorize a UAE-based representative to handle dissolution procedures, filings, and government submissions. Most steps require in-person presence or original documents, so appointing a local representative is non-negotiable.

What happens if I just let my UAE trade license expire without formally liquidating?

The company remains legally active, fines and penalties continue to accumulate (license renewal, VAT, Corporate Tax), and directors/shareholders remain personally liable. You may be denied future entry into the UAE until all debts and penalties are repaid.

Do I need to report my UAE company's liquidation to Indian tax or regulatory authorities?

Yes. Indian residents have three key obligations:

- File Form FC with their AD bank within 30 days of receiving disinvestment proceeds (FEMA)

- Disclose the shareholding in Schedule FA of their ITR until liquidation is complete

- Assess capital gains implications under the India-UAE DTAA

Non-compliance triggers FEMA penalties and up to ₹10 lakh per year under the Black Money Act.