Introduction: UAE Corporate Tax Guide for Indian Businesses Operating in Dubai

For decades, Indian entrepreneurs viewed the UAE as a tax haven: profits flowed freely, with no corporate tax to manage. That changed on 1 June 2023, when the UAE introduced Federal Decree-Law No. 47 of 2022, implementing a federal Corporate Tax (CT) regime that fundamentally reshaped the operating environment for the nearly 4,000 Indian companies in Dubai and across the Emirates.

This shift creates unique challenges for Indian businesses. Unlike domestic UAE firms navigating a single new tax regime, Indian-owned entities must manage dual compliance — UAE CT rules alongside continuing Indian tax obligations.

That intersection creates pressure points across several areas:

- Remittances and repatriation of profits

- Transfer pricing documentation between related Indian and UAE entities

- Permanent Establishment (PE) risks in India

- Treaty access under the India-UAE Double Taxation Avoidance Agreement (DTAA)

Many Indian entrepreneurs mistakenly assume their free zone registration guarantees tax exemption, or that the 9% headline rate applies uniformly. This guide unpacks the UAE CT framework specifically for Indian businesses, covering the tiered rate structure, the conditional free zone 0% regime, Small Business Relief, DTAA implications, and the compliance steps that prevent costly penalties.

TLDR: Key Takeaways

- UAE CT applies at 0% up to AED 375,000 and 9% above — effective for financial years starting on or after 1 June 2023

- Free zone 0% requires QFZP status: adequate substance, qualifying activities, audited financials, and de minimis compliance

- Small Business Relief (revenue under AED 3 million) treats taxable income as zero — available through 31 December 2026

- The India-UAE DTAA reduces withholding tax on dividends (10%), interest (5–12.5%), and royalties (10%), but requires genuine substance to access treaty benefits

- FTA registration is mandatory for all taxable persons; late registration carries an AED 10,000 penalty and returns are due within 9 months of year-end

UAE Corporate Tax at a Glance: Rates and Who It Applies To

The UAE Corporate Tax Law applies to financial years starting on or after 1 June 2023, using a two-tier rate structure. It also aligns the UAE with the OECD Two-Pillar Solution, shielding the country's tax base from foreign top-up tax claims on UAE profits.

CT Rate Structure:

| Taxable Income Slab | CT Rate | Notes |

|---|---|---|

| Up to AED 375,000 | 0% | Threshold applies per entity, not per shareholder |

| Above AED 375,000 | 9% | Applied only to income exceeding threshold |

| Qualifying Free Zone Person (QFZP) qualifying income | 0% | Conditional; requires QFZP status each tax period |

| QFZP non-qualifying income | 9% | No AED 375,000 threshold benefit |

| Large MNEs (EUR 750M+ global revenue) | 15% | Domestic Minimum Top-up Tax (DMTT), effective 1 Jan 2025 |

Who Qualifies as a Taxable Person

Indian businesses operating in the UAE fall into CT scope if they are:

- Mainland LLCs, free zone entities (FZE, FZCO), or branches of Indian companies registered in the UAE

- Foreign entities whose trade or business is conducted in the UAE "in an ongoing or regular manner," or that are effectively managed and controlled from the UAE

- Individual business owners with annual turnover exceeding AED 1 million — registration deadline is 31 March of the following year, per FTA Decision No. 3 of 2024

Taxable income is calculated from accounting profit, adjusted for exemptions, reliefs, and non-deductible expenses under the CT Law.

Domestic Minimum Top-up Tax (DMTT) for Large Indian Conglomerates

Effective 1 January 2025, Cabinet Decision No. 142 of 2024 imposes a 15% DMTT on UAE constituent entities of MNEs with consolidated global revenues of EUR 750 million or more in at least two of the four preceding fiscal years.

This affects large Indian conglomerates with UAE operations. Groups such as Tata, Reliance, or Adani with UAE presence need to evaluate Pillar Two exposure alongside their standard UAE CT obligations.

Free Zone vs. Mainland: Tax Implications for Indian Business Structures

Most Indian entrepreneurs in Dubai operate through one of three structures: a mainland LLC, a free zone entity (FZE/FZCO), or a branch office — and each carries distinct CT implications that need to be understood before the first tax period begins, not during it.

Qualifying Free Zone Person (QFZP) Regime: 0% Is Conditional, Not Automatic

Simply being registered in a free zone does not guarantee tax exemption. The FTA's Free Zone Bulletin makes this explicit: a Free Zone Person must actively qualify as a QFZP for each tax period to benefit from the 0% rate on qualifying income.

QFZP Conditions (All Must Be Met):

- Maintain adequate assets, qualified employees, and operating expenditure in the Free Zone; Core Income-Generating Activities (CIGAs) must be performed there

- Earn income from qualifying activities conducted with other Free Zone Persons or from activities listed in Ministerial Decision No. 229 of 2025

- Keep non-qualifying revenue below the lower of AED 5 million or 5% of total revenue (de minimis threshold)

- Prepare and maintain audited financial statements — even if revenue falls below the AED 50 million audit threshold

- Apply arm's length pricing to all related-party transactions under Article 34

- Avoid excluded activities such as transactions with UAE natural persons or unregulated banking/insurance

Qualifying Activities Relevant to Indian Businesses

Per Cabinet Decision No. 100 of 2023 and Ministerial Decision No. 229 of 2025, qualifying activities include:

- Manufacturing or processing of goods

- Trading of qualifying commodities (metals, energy, agricultural products)

- Holding shares and securities (12-month holding period)

- Distribution of goods from a Designated Zone (JAFZA, DMCC, DIFC warehouses)

- Logistics services (freight forwarding, warehousing)

- Headquarter services to related parties

- Treasury and financing services to related parties

- Fund management and wealth management

- Ownership or exploitation of qualifying intellectual property

Not all income earned inside a free zone qualifies, however. The following are excluded activities — subject to 9% CT even for QFZPs:

- Retail sales directly to UAE individuals

- Provision of services to UAE natural persons

- Banking, insurance, and finance activities (unless the entity is appropriately regulated and licensed)

Mainland LLC Implications

A mainland LLC in Dubai is fully subject to the standard 0%/9% CT regime on all taxable income. There is no special free zone protection. Indian businesses with mainland operations—especially in retail, F&B, or professional services—should factor in a 9% effective rate on profits above AED 375,000 when planning pricing and margins.

If a mainland entity has a branch in a Free Zone, that branch is treated as a Domestic Permanent Establishment. Income attributable to the Domestic PE is excluded from qualifying income and taxed at 9%.

The Substance Requirement: Real Operations, Not Virtual Offices

The FTA Corporate Tax Guide on Free Zone Persons emphasises that adequate substance requires CIGAs to be performed within the Free Zone, with adequate assets, employees, and expenditure. Outsourcing is permitted to related parties or third parties within a Free Zone, provided the QFZP maintains adequate supervision.

For Indian trading companies operating from DMCC or JAFZA, the substance test poses real risk — particularly where inventory management, procurement decisions, or customer relationships are managed from India. Virtual offices, nominee directors, and minimal staffing will not satisfy QFZP substance requirements.

Common substance gaps that trigger disqualification:

- No employees physically present in the Free Zone

- Key decisions made by India-based management

- Core functions (procurement, sales, logistics) outsourced outside the Free Zone without adequate supervision

Key Exemptions and Reliefs Available to Indian Businesses

Small Business Relief: Transitional Zero-Tax Treatment

Ministerial Decision No. 73 of 2023 provides temporary relief for qualifying small businesses. Indian-owned UAE businesses with revenues of AED 3 million or less for the current and all previous tax periods are treated as having zero taxable income for tax periods ending on or before 31 December 2026.

Eligibility conditions:

- Must be a UAE resident person

- Revenue threshold of AED 3 million or less applies to both the current and all previous tax periods

- Cannot be a constituent entity of an MNE Group required to prepare Country-by-Country Reports (consolidated revenue exceeding AED 3.15 billion)

- Qualifying Free Zone Persons are excluded from Small Business Relief

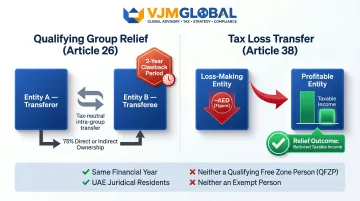

Qualifying Group Relief and Tax Loss Transfer

Article 26 of the CT Law allows tax-neutral transfer of assets and liabilities between group members at net book value, provided that:

- Both members must be UAE juridical residents (or non-residents with a PE in the UAE)

- One must own at least 75% of the other (or a third party owns 75% of both)

- Same financial year and accounting standards

- Neither can be an Exempt Person or QFZP

- 2-year clawback: Relief reversed if asset leaves the group or 75% ownership breaks

Tax loss transfer (Article 38) allows a company to transfer tax losses to offset another group company's taxable income, subject to 75% common ownership from the period the loss was incurred through the period it is used. This is separate from Qualifying Group Relief — practically, it means an Indian group with one loss-making UAE entity and one profitable one can reduce the profitable entity's taxable income by transferring those losses across.

Other Reliefs

Two additional reliefs are worth noting for Indian businesses with more complex structures:

Business restructuring relief (Article 27) eliminates the corporate tax impact of qualifying mergers and demergers carried out for valid commercial reasons. A 2-year clawback applies if the underlying conditions break down.

Realization basis election (Article 20) lets taxable persons elect to recognize gains and losses on certain assets only when realized — not on paper. This election must generally be made in the first tax return and applied consistently going forward.

India-UAE Double Taxation and Transfer Pricing: Critical Considerations for Indian Companies

The intersection of UAE CT and Indian tax law creates compliance complexity across three dimensions: treaty application, transfer pricing, and anti-avoidance rules.

India-UAE DTAA: Treaty Rates and Scope

The India-UAE DTAA provides relief from double taxation on key income types:

| Income Type | Treaty WHT Rate | Application |

|---|---|---|

| Dividends | 10% | Beneficial owner requirement; subject to Principal Purpose Test (PPT) |

| Interest (banks) | 5% | Includes financial institutions |

| Interest (others) | 12.5% | General rate for non-bank entities |

| Royalties | 10% | Covers patents, copyrights, trademarks, equipment |

| Fees for technical services | 10% | Specific provision in treaty |

| Business profits | Taxable only if PE exists | Only profits attributable to PE taxable in source state |

| Capital gains on shares | Taxable in source country | Per 2007 Protocol amendment |

The 2012 Protocol aligned the treaty with international transparency standards on Exchange of Information. Both India and the UAE are signatories to the Multilateral Instrument (MLI), which applies the Principal Purpose Test (PPT). A CBDT clarification issued in January 2025 enables denial of treaty benefits if the main purpose of an arrangement is to obtain tax benefits.

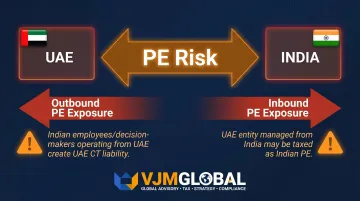

Permanent Establishment (PE) Risk

Article 5 of the India-UAE DTAA defines PE as "a fixed place of business through which the business of an enterprise is wholly or partly carried on," including a branch, office, factory, or construction site lasting more than 9 months.

Two-way PE risk for Indian businesses:

- Outbound PE exposure: Indian company employees or decision-makers operating from the UAE regularly can trigger a UAE PE, creating UAE CT liability on profits attributable to that presence

- Inbound PE exposure: A UAE entity whose management activities run from India — board meetings in Mumbai, key decisions made by Indian directors — may create a PE in India, exposing the entity to Indian tax liability

UAE CT Transfer Pricing (Article 34)

All transactions between related parties and connected persons must comply with the arm's length principle. Ministerial Decision No. 97 of 2023 sets disclosure thresholds:

| Requirement | Threshold |

|---|---|

| Related-party disclosure (aggregate) | AED 40 million per tax period |

| Related-party disclosure (individual) | AED 4 million per transaction |

| Master File and Local File (entity revenue) | AED 200 million or more |

| Master File and Local File (MNE group) | AED 3.15 billion consolidated revenue |

Documentation must be submitted within 30 days of FTA request. For Indian businesses transacting with their parent company or group entities in India — management fees, royalties, procurement payments, intercompany loans — transfer pricing documentation is mandatory.

VJM Global provides transfer pricing documentation services tailored to the India-UAE corridor, including FAR analysis, benchmarking studies, local file and master file preparation, and related-party disclosure form filing.

Indian Tax Treatment of UAE Income

Understanding UAE-side obligations is only half the picture — the Indian tax treatment of income flowing back from Dubai matters equally.

When a UAE subsidiary pays dividends to an Indian parent, Section 115BBD of the Income Tax Act imposes a concessional 15% tax (plus surcharge and cess) on dividends from a specified foreign company — applicable where the Indian company holds 26% or more of nominal share capital. The UAE's 10% DTAA withholding rate can be credited against this Indian liability. The Finance Act 2020's introduction of Section 80M also allows deduction of inter-corporate dividends to prevent cascading taxation.

Place of Effective Management (POEM) and GAAR

India's POEM test (Section 6(3), CBDT Circular No. 6 of 2017) can deem a UAE company tax-resident in India if key management and commercial decisions are made in substance from India. The safe harbor is narrow — POEM provisions do not apply where foreign company turnover is INR 500 million or less.

For larger UAE entities, the Active Business Outside India (ABOI) test applies. POEM is presumed to be outside India when all four conditions are met:

- Passive income does not exceed 50% of total income

- Less than 50% of assets are located in India

- Less than 50% of employees are based in India

- India-based payroll is less than 50% of total payroll

This presumption breaks down if the board functions as a rubber stamp for Indian holding company decisions rather than exercising independent judgment.

India's General Anti-Avoidance Rule (GAAR, Chapter X-A) can disregard arrangements lacking commercial substance where the tax benefit exceeds INR 30 million. UAE holding or trading companies controlled from India face dual risk: losing QFZP status under UAE CT and being treated as Indian tax residents under POEM.

VJM Global's cross-border tax advisory services help Indian businesses structure India-UAE operations in compliance with both UAE CT and Indian tax laws, including DTAA application, transfer pricing documentation, and POEM/GAAR compliance reviews.

UAE Corporate Tax Compliance: Registration, Filing, and Record-Keeping

FTA Registration

All taxable persons—including Indian-owned UAE entities—must register with the FTA and obtain a Corporate Tax Registration Number (CTRN). Late registration attracts an administrative penalty of AED 10,000, per Cabinet Decision No. 10 of 2024.

Registration timelines per FTA Decision No. 3 of 2024:

| Entity Type | Registration Deadline |

|---|---|

| Resident juridical persons (existing before 1 March 2024) | Staggered by month of license issuance (May–December 2024) |

| Resident juridical persons (incorporated after 1 March 2024) | 3 months from date of incorporation |

| Natural persons (turnover exceeding AED 1 million) | 31 March of the year following the calendar year threshold was exceeded |

| Non-resident juridical persons with PE | 9 months from date of PE existence (existing); 6 months (new) |

The FTA has announced a penalty waiver program for late registration, conditional on submission of the tax return within 7 months from the end of the tax period.

Filing and Payment

Once registered, businesses must meet ongoing filing obligations. CT returns and payment must be submitted within 9 months from the end of the financial year (for example, a company with a 31 December year-end must file by 30 September of the following year). CT is self-assessed, meaning the taxable person calculates and reports their own liability directly to the FTA.

Record-Keeping

Records must be retained for at least 7 years following the end of the tax period. Required records include:

- Documents supporting tax return information

- Records of transactions

- Records of assets (purchases and disposals)

- Records of liabilities and shares held

- Transfer pricing documentation

- Exempt Persons: documentation verifying exempt status

Managing these obligations—registration deadlines, self-assessed returns, and seven years of transfer pricing records—requires careful coordination. VJM Global supports Indian businesses through each stage: FTA registration, taxable income calculation, return filing, and transfer pricing disclosure forms.

Common Pitfalls Indian Businesses Must Avoid

Misunderstanding Free Zone Protections

Many Indian entrepreneurs assume their free zone entity is automatically exempt from corporate tax. The FTA Free Zone Bulletin is explicit on this point:

"A Qualifying Free Zone Person is not eligible to benefit from the 0% Corporate Tax rate applicable on Taxable Income up to the AED 375,000 threshold and is subject to the rate of 9% on its entire Taxable Income that is not Qualifying Income."

Failing to track and segregate qualifying versus non-qualifying income can trigger full 9% CT liability on all income. If non-qualifying revenue exceeds the de minimis threshold (lower of AED 5 million or 5% of total revenue), the entity loses QFZP status for that entire tax period and the subsequent four tax periods.

Ignoring Transfer Pricing Documentation

Free zone compliance is only part of the picture. Indian businesses transacting with related parties back home often overlook UAE transfer pricing requirements entirely — and the consequences are concrete.

Key risk areas include:

- Non-arm's length pricing with Indian group entities triggers CT adjustments and potential penalties

- Payments to connected persons (owners, directors, family members) at above-market rates are disallowed as deductions under UAE CT law

- Undocumented intercompany transactions leave no audit trail to defend pricing positions during FTA review

Missing the Substance Requirements

Transfer pricing problems often compound a deeper issue: thin substance. Indian businesses that rely on virtual offices or nominee directors while managing operations from India face two simultaneous risks:

- Loss of QFZP status under UAE CT law due to inadequate economic activity in the free zone

- Indian tax residency exposure under the Place of Effective Management (POEM) rules, triggering CT liability in India on the same income

The result is double taxation — in both jurisdictions at once.

With nearly 4,000 Indian companies in DMCC alone — 16% of its member base — operating within a USD 85 billion bilateral trade corridor, even one overlooked pitfall can expose a business to penalties across two tax systems simultaneously.

Frequently Asked Questions

How much is the UAE corporate tax?

UAE CT is 0% on taxable income up to AED 375,000 and 9% on taxable income above that threshold. A 15% Domestic Minimum Top-up Tax (DMTT) applies to large MNEs with global revenues of EUR 750 million or more, effective 1 January 2025.

Do Indian businesses in UAE free zones pay corporate tax?

Free zone entities fall within UAE CT scope but can qualify for a 0% rate on qualifying income by meeting QFZP conditions: adequate substance, qualifying activities, audited financials, and de minimis revenue limits. Non-qualifying income is taxed at 9%, with no AED 375,000 threshold benefit.

Does the India-UAE DTAA protect Indian businesses from double taxation?

The India-UAE DTAA limits withholding tax on dividends (10%), interest (5–12.5%), royalties (10%), and technical service fees (10%). To rely on these benefits, businesses must maintain genuine UAE substance and satisfy the Principal Purpose Test.

When is the UAE corporate tax return filing deadline?

CT returns must be filed within 9 months from the end of the financial year (e.g., 30 September 2025 for a 31 December 2024 year-end), with payment due on the same date. All returns are filed on a self-assessment basis.

Can Indian-owned UAE companies claim Small Business Relief?

Small Business Relief allows UAE resident businesses with revenue of AED 3 million or less to treat their taxable income as zero, available for tax periods ending on or before 31 December 2026. QFZPs and MNE constituent entities are excluded. Indian-owned UAE companies meeting the criteria may claim this relief.

What records must Indian businesses maintain for UAE corporate tax compliance?

All taxable persons must retain financial records, supporting documents, transfer pricing documentation, and records of transactions, assets, liabilities, and shares for 7 years after the end of the relevant tax period to facilitate potential FTA audits.