Introduction

The belief that incorporating a Dubai Free Zone company guarantees zero taxes forever has become dangerously outdated for Indian entrepreneurs. Since June 1, 2023, the UAE's new Corporate Tax (CT) regime has changed the rules. While 0% tax remains achievable for Free Zone businesses, it now requires meeting strict qualifying conditions that many Indian owners misunderstand or overlook entirely.

Beyond UAE compliance, Indian business owners face a layer most guides ignore entirely: Indian tax laws, FEMA obligations, and the India-UAE Double Tax Avoidance Agreement (DTAA). Even if your Free Zone company qualifies for 0% UAE tax, you may still owe substantial taxes in India on dividends received.

The risk compounds further. If your company's management and control effectively operates from India, the entire UAE structure can collapse under India's Place of Effective Management (POEM) rules — triggering full Indian corporate tax liability at 25.168%.

This article covers who qualifies for the 0% UAE rate, what Indian-specific obligations apply, and the concrete steps to stay compliant on both sides of the border. The tax advantage is real — but only if you get both jurisdictions right.

Key Takeaways

- Dubai Free Zone companies must qualify as a Qualifying Free Zone Person (QFZP) by meeting all seven conditions—registration alone does not guarantee 0% tax

- Qualifying income includes transactions with other Free Zone persons and approved "qualifying activities" with non-Free Zone parties; everything else is taxed at 9%

- Exceeding the de minimis threshold (5% of revenue or AED 5 million) strips the entire entity of 0% status for five years

- Indian residents receiving dividends from a UAE Free Zone company still owe Indian income tax at slab rates up to ~42.7%; UAE's 0% rate does not eliminate Indian liability

- All Free Zone companies must register with the FTA and file annual CT returns with IFRS-compliant audited financial statements, even at 0% tax

What Is the UAE Corporate Tax and How Does It Apply to Free Zones?

The UAE introduced Federal Corporate Tax via Federal Decree-Law No. 47 of 2022, effective June 1, 2023, ending the Emirates' long-standing reputation as a zero-tax jurisdiction. The law established a two-tier rate structure:

| Taxable Income | CT Rate |

|---|---|

| Up to AED 375,000 | 0% |

| Above AED 375,000 | 9% |

Free Zone companies are not exempt from Corporate Tax. They are classified as "taxable persons" under the CT Law. Those meeting all Qualifying Free Zone Person (QFZP) criteria can access a 0% rate on qualifying income — with no upper limit — but non-qualifying income remains subject to the standard 9% rate.

Critical Compliance Requirements Even at 0% Tax

Indian entrepreneurs frequently assume that a 0% effective tax rate means zero filing obligations — that assumption is costly. Every Free Zone entity, regardless of tax liability, must:

- Register with the Federal Tax Authority (FTA) before applicable deadlines

- File annual CT returns within nine months of the tax period end

- Prepare audited financial statements in accordance with IFRS

- Maintain transfer pricing documentation for related-party transactions

Late registration alone carries a penalty of AED 10,000, though the FTA currently waives this penalty if you submit your first CT return within seven months from the end of the first tax period.

Maintaining QFZP status depends on ongoing compliance — not just initial registration. Failing to meet audit or filing requirements can trigger disqualification from the 0% rate for a minimum of five years.

Who Qualifies as a Qualifying Free Zone Person (QFZP)?

Only a juridical person (a corporation, LLC, or other registered legal entity incorporated in a UAE Free Zone) can qualify for QFZP status.

Sole proprietors and freelancers operating as natural persons in a Free Zone do not qualify — they are taxed under standard CT rules. This is a common blind spot for Indian sole proprietors who set up in Free Zones expecting full tax exemption.

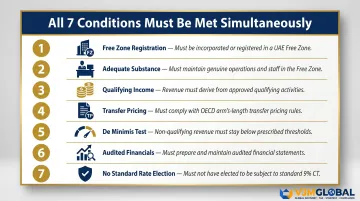

The Seven Mandatory Qualifying Conditions

A Free Zone entity must simultaneously satisfy all seven conditions to maintain QFZP status:

- Be a Free Zone Person: The entity must be incorporated, established, or registered in a Free Zone (including branches)

- Maintain adequate substance in the UAE: Core income-generating activities must occur within the Free Zone, with adequate physical assets, qualified employees, and operating expenditures in line with business scale

- Derive qualifying income: Income must come from approved sources and activities

- Not elect to be subject to standard 9% CT: The entity must not opt out of the QFZP regime

- Comply with transfer pricing rules: Full documentation and arm's length pricing required for related-party transactions

- Stay within the de minimis threshold: Non-qualifying revenue must not exceed 5% of total revenue or AED 5 million, whichever is lower

- Prepare IFRS-compliant audited financial statements: Annual audited financials are mandatory

Of these seven, the substance requirement (condition 2) is where most entities fall short. Here's what it actually requires.

What "Adequate Substance" Actually Means

The substance requirement is not satisfied by a virtual office or nominee director. The Free Zone entity must demonstrate that its core income-generating activities physically occur within the Free Zone. This means:

- Adequate physical office space and assets

- Sufficient qualified, full-time employees performing core functions

- Operating expenditures proportionate to the nature and scale of business

- Decision-making authority actively exercised from within the Free Zone

A registered-only "shell" entity with no real employees or operational presence will fail this test.

The Five-Year Disqualification Penalty

Failing even one qualifying condition triggers severe consequences. The entity loses QFZP status and is taxed at the standard 9% CT rate — not just for the current year, but for the current tax year plus the following four years.

Key rule: Ministerial Decision No. 265 of 2023, Article 5 states the person "shall cease to be a Qualifying Free Zone Person from the beginning of the relevant Tax Period and for the subsequent (4) four Tax Periods."

This creates a minimum five-year disqualification window before the entity can retest eligibility — making compliance a year-round discipline, not an annual checkbox.

Domestic Permanent Establishment Exception

If a QFZP operates a mainland branch or office outside the Free Zone within the UAE, that branch constitutes a Domestic Permanent Establishment (PE). Income attributable to a Domestic PE is calculated separately and taxed at 9%. Having a Domestic PE does not disqualify the Free Zone entity's qualifying income from the 0% rate — but separate books of accounts must be maintained for each.

What Counts as Qualifying Income and Qualifying Activities?

Qualifying income is income eligible for the 0% CT rate. It falls into three source-based categories:

- Income from transactions with other Free Zone persons (except excluded activities)

- Income from transactions with non-Free Zone persons, but only if the activity is a "qualifying activity"

- Any other income that passes the de minimis test

The 14 Approved Qualifying Activities

Ministerial Decision No. 265 of 2023 lists the specific activities that allow income from non-Free Zone parties to remain qualifying income:

- Manufacturing of goods or materials

- Processing of goods or materials

- Trading of qualifying commodities (metals, minerals, energy, agriculture traded on a recognized commodities exchange in raw form)

- Holding of shares and other securities for investment purposes

- Ownership, management, and operation of ships

- Reinsurance services

- Fund management services

- Wealth and investment management services

- Headquarter services to related parties

- Treasury and financing services to related parties

- Financing and leasing of aircraft

- Distribution of goods or materials in or from a Designated Zone

- Logistics services

- Ancillary activities to the above

Excluded Activities That Disqualify Income

Even if conducted in a Free Zone, the following activities disqualify income from the 0% rate:

- Transactions with natural persons – Income from individual consumers does not qualify, with limited exceptions for ships, fund management, wealth/investment management, and aircraft financing/leasing.

- Regulated banking, finance, leasing, and insurance – Banking, insurance (except reinsurance and captive/headquarters insurance), and finance/leasing (except ships, treasury services to related parties, and aircraft) are excluded.

- Immovable property outside Free Zones – Owning or exploiting property outside a Free Zone is excluded. Commercial Free Zone property transacted with another Free Zone person is an exception.

The De Minimis Rule Explained

Non-qualifying revenue must not exceed 5% of total revenue OR AED 5,000,000, whichever is lower.

Example: A Free Zone company earns AED 10 million in total revenue. It generates AED 400,000 from non-qualifying activities. This represents 4% of total revenue, staying within the 5% threshold. The entity still qualifies for QFZP status on its remaining income.

If that same company instead earned AED 600,000 from non-qualifying income (6%), it would breach the threshold and lose QFZP status entirely, triggering 9% CT on all taxable income for that tax year and the following four.

Warning for Indian-Owned Free Zone Businesses Serving Indian Clients

The de minimis calculation above is where many Indian-owned Free Zone businesses run into trouble. If your company primarily serves clients in India, map your activities against the approved qualifying activities list before assuming the 0% rate applies.

Income from Indian clients (non-Free Zone persons) is only qualifying income if the underlying activity is on that approved list. Trading general goods with Indian importers, for example, does not qualify unless the goods are qualifying commodities. Breaching the de minimis threshold through non-qualifying Indian client income is a common mistake that costs businesses their 0% status.

The India-UAE Angle: What Indian Business Owners Must Specifically Know

The India-UAE DTAA Does Not Eliminate Indian Tax Liability

The India-UAE Double Tax Avoidance Agreement, signed in 1993, prevents the same income from being taxed twice—but it does not shield Indian tax residents from Indian tax on foreign income.

Under Article 10 of the DTAA:

- India retains the right to tax dividends received by an Indian resident from a UAE company

- The UAE may impose withholding tax up to 10% on dividends, but since the UAE imposes no personal income tax and a QFZP pays 0% CT, the UAE side collects nothing

- Indian residents therefore pay full Indian income tax on UAE dividends with no foreign tax credit to offset it

Indian Tax Treatment of Foreign Dividends

Since April 1, 2020, dividends are taxable in the hands of shareholders at applicable slab rates as "Income from Other Sources." For an individual Indian resident in the highest tax bracket, this means:

| Tax Regime | Maximum Marginal Rate |

|---|---|

| Old regime | Approximately 42.74% (30% base + 37% surcharge + 4% cess) |

| New regime | Approximately 39% (30% base + 25% surcharge + 4% cess) |

The special 15% rate under Section 115BBD applies only to Indian companies holding 26%+ equity in a specified foreign company—not to individual shareholders.

A UAE Free Zone company paying 0% CT in the UAE does not reduce the Indian owner's personal tax bill. Dividends repatriated to India face full Indian slab rates.

NRI vs. Indian Resident: A Critical Distinction

NRIs (Non-Resident Indians) who have genuinely relocated to the UAE and meet non-residency conditions under FEMA and the Income Tax Act have significantly lower Indian tax exposure on UAE income.

Indian residents who simply register a UAE Free Zone company while living and managing the business from India trigger a critical risk: Place of Effective Management (POEM) rules.

Place of Effective Management (POEM): The Structural Collapse Risk

Section 6(3) of the Income Tax Act defines POEM as "a place where key management and commercial decisions that are necessary for the conduct of business of an entity as a whole are, in substance, made."

If the CBDT (Central Board of Direct Taxes) determines that a UAE Free Zone company's POEM is in India—because board meetings, key decisions, and day-to-day management all happen from India—the entire UAE company becomes an Indian tax resident.

At that point, all income is subject to Indian corporate tax at 25.168% under Section 115BAA, completely eliminating the Free Zone tax advantage.

POEM safe harbor: Companies with turnover below INR 500 million (Rs 50 crore) are exempt from POEM provisions. But most businesses aspiring to meaningful tax savings exceed this threshold quickly.

How to avoid POEM risk:

- Hold board meetings in the UAE, not India

- Ensure key decisions are documented as occurring in the UAE

- Employ qualified managers in the UAE who exercise genuine authority

- Maintain operational evidence that the UAE entity is not a shell

FEMA and RBI Compliance Obligations

Indian residents investing in a UAE Free Zone company must comply with the Foreign Exchange Management Act (FEMA) and RBI regulations:

Overseas Direct Investment (ODI) routing: Investments must be routed through an Authorised Dealer (AD) bank and reported to RBI under the Foreign Exchange Management (Overseas Investment) Directions, 2022.

Liberalised Remittance Scheme (LRS): Indian resident individuals can remit up to USD 250,000 per financial year under LRS. Amounts above this require the ODI route through an AD bank.

Repatriation requirements: Dividends and profits must be repatriated to India through proper banking channels. Late or improper repatriation is a FEMA breach carrying independent penalties.

FEMA penalties are separate from tax liability:

| Violation Type | Penalty |

|---|---|

| Quantifiable violations | Up to 300% of the sum involved |

| Non-quantifiable violations | Up to Rs 2 lakh |

| Criminal prosecution threshold | Up to 5 years imprisonment if foreign assets exceed Rs 1 crore |

Failure to comply with FEMA is a serious legal violation—distinct from and in addition to income tax non-compliance.

The Real Tax Comparison for Indian Entrepreneurs

India's corporate tax rates currently stand higher than the UAE's 9%:

| Jurisdiction | Rate |

|---|---|

| UAE QFZP qualifying income | 0% |

| UAE standard/non-qualifying income | 9% |

| India Section 115BAA (most common) | 25.168% |

| India Section 115BAB (new manufacturing) | 17.16% |

| India old regime (large companies) | Up to 34.94% |

The genuine tax advantage of a UAE Free Zone setup exists (approximately 25 percentage points lower than India's common corporate rate). But this advantage only materializes when:

- The owner actually relocates to the UAE and severs Indian tax residency

- The company maintains real UAE substance and management

- FEMA compliance is properly maintained

- The structure is not a paper entity controlled from India

Simply registering an offshore entity while continuing to live and operate from India does not deliver the tax benefit—and creates compounding compliance exposure across both jurisdictions.

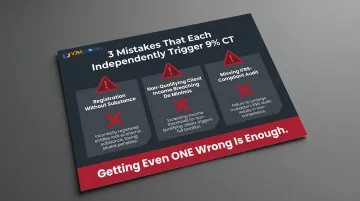

Common Mistakes Indian Business Owners Make in Free Zone Tax Planning

The "Registration = Exemption" Myth

Many Indian entrepreneurs assume that obtaining a Free Zone trade license automatically grants perpetual 0% corporate tax. Post-2023, you must actively meet and maintain all seven QFZP criteria — including real substance, correct income types, IFRS audits, and annual filings. Registration opens the door; sustained compliance keeps it open.

Building a Client Base of Indian Companies or Individuals

If the majority of your Free Zone entity's income comes from transactions with natural persons — or from activities not on the approved qualifying activities list — you will quickly breach the de minimis threshold.

Indian businesses serving their Indian client base through a UAE entity are particularly exposed here. Income from Indian clients only qualifies if the underlying activity is approved. If it isn't, that revenue counts as non-qualifying income and erodes your QFZP status.

Neglecting IFRS-Compliant Audited Financial Statements

Many small Indian-owned Free Zone businesses skip formal audits to save costs, unaware that audited financials are a mandatory condition for claiming the 0% CT rate. Missing this single requirement is enough to lose QFZP status entirely, triggering a 9% CT liability plus penalties.

This is non-negotiable. Ministerial Decision No. 265 of 2023, Article 5 explicitly mandates IFRS-compliant audited accounts as a condition of QFZP eligibility.

Each of these three mistakes is independently sufficient to trigger full 9% corporate tax liability — meaning you don't need to get all three wrong. Getting one wrong is enough.

How to Stay Compliant and Protect Your 0% Tax Status

Core Compliance Checklist for Indian-Owned QFZP Entities

- FTA registration before the applicable deadline (currently waivable if first CT return filed within seven months)

- Annual CT return filing within nine months of tax period end, even at 0% tax

- IFRS-compliant audited financial statements prepared annually

- Transfer pricing documentation maintained for all related-party transactions

- Documented evidence of adequate substance: employee headcount, physical office lease, payroll records, operating costs

Income Segregation and Record-Keeping

Free Zone companies with any mainland UAE operations (Domestic PE) must maintain separate books of accounts for Free Zone income and mainland income. Combining them exposes qualifying income to the 9% rate. Cross-border transactions with Indian group entities require arm's length pricing and full transfer pricing documentation.

VJM Global's transfer pricing services cover benchmarking studies, documentation (Master Files, Local Files, Country-by-Country Reporting), and risk assessment, ensuring compliance across both UAE and Indian regulations.

Professional Cross-Border Advisory

Navigating UAE corporate tax compliance and Indian tax/FEMA obligations at the same time is genuinely complex — the rules interact in ways that can cost you the 0% status you set up the structure to achieve. VJM Global's team of Chartered Accountants and international tax advisors has handled this dual-jurisdiction complexity for Indian entrepreneurs for over 30 years. The firm provides an integrated compliance solution covering:

- UAE CT registration and annual filing

- IFRS-compliant audit coordination

- Indian tax residency and DTAA analysis

- RBI/FEMA reporting for ODI and profit repatriation

- POEM risk assessment and mitigation strategies

- Transfer pricing documentation for cross-border transactions

Getting either jurisdiction wrong can trigger back-taxes, penalties, or a forced reclassification of your Free Zone income — making integrated advisory from the outset far less costly than remediation later.

Frequently Asked Questions

Frequently Asked Questions

How does UAE corporate tax impact free zones?

Free Zone companies are subject to UAE CT law and must register with the FTA, but those qualifying as QFZPs by meeting all seven conditions can enjoy a 0% rate on qualifying income. Non-qualifying income is taxed at 9%.

What is the 9% corporate tax in the UAE?

The UAE's 9% corporate tax applies to taxable income above AED 375,000 for mainland companies and for Free Zone entities that either fail to meet QFZP conditions or earn non-qualifying income.

Does Dubai really have 0% tax?

Yes — but only for Free Zone businesses that actively qualify as QFZPs. Non-qualifying income, mainland operations, and post-2023 compliance requirements all affect eligibility, so the 0% benefit must be earned and maintained, not assumed.

Can an Indian resident own a Dubai Free Zone company?

Yes, Indian residents can legally own a UAE Free Zone company through the RBI/FEMA-compliant Overseas Direct Investment (ODI) route. They must report the investment and comply with FEMA regulations. Dividends and income repatriated to India are taxable there under Indian slab rates, with partial relief available under the India-UAE DTAA.

Will income from a Dubai Free Zone company be taxed in India?

Indian tax residents pay tax on UAE company dividends at applicable slab rates (up to ~42.74%). The India-UAE DTAA reduces double taxation but does not eliminate the Indian liability. NRIs who have genuinely relocated outside India are treated differently.

What happens if a Dubai Free Zone company does business with clients in India?

Income from transactions with Indian clients (non-Free Zone persons) is only qualifying income if the underlying activity is an approved qualifying activity under UAE CT law. Otherwise it counts as non-qualifying income, and if it exceeds the de minimis threshold, the entire entity loses its 0% QFZP status.