Introduction

Closing a business in the US is relatively straightforward. Closing an Indian subsidiary works very differently. It involves two separate statutes, multiple regulatory bodies, and compliance obligations that stay active right up until the dissolution order is issued.

For US founders, investors, and companies that set up an Indian Private Limited Company, LLP, Branch Office, or Liaison Office, three laws shape the exit process: the Companies Act, 2013, the Insolvency and Bankruptcy Code (IBC), 2016, and FEMA regulations that govern how residual capital flows back to the US parent.

Many US business owners underestimate this complexity, especially the FEMA repatriation requirements and the need to clear all pending compliance before any dissolution application is accepted.

This guide covers the three closure paths available, the step-by-step process for each, key US-specific considerations around tax and foreign exchange, and the most common mistakes that derail applications.

Key Takeaways

- Two primary paths: Strike Off for inactive companies, or Voluntary Winding Up under IBC Section 59 for companies with assets or debts

- Compliance first: All ITR filings, GST returns, and ROC annual filings must be up to date before filing any application

- Timeline reality: Strike Off benchmarks around 100 days; Voluntary Winding Up averages 397 days in practice

- FEMA applies on exit: Residual capital repatriation to the US parent requires an Authorised Dealer (AD Category-I) bank

- GST cancellation is separate: Closing the company does not auto-cancel GST, PF/ESIC, or Shops & Establishments registrations

What Is Winding Up a Company in India?

Winding up is the formal legal process by which a company ceases operations, settles all outstanding obligations, and is officially removed from the Register of Companies maintained by the Registrar of Companies (ROC). Once dissolved, the entity ceases to exist as a legal person.

That definition matters because winding up is often confused with making a company dormant — but they are not the same. Section 455 dormancy preserves the company and its registration; it does not dissolve it. Dissolution is permanent, though Section 252 of the Companies Act does permit restoration on application within 20 years of Gazette publication in certain circumstances.

India offers three closure paths:

| Path | Governing Law | Best Suited For |

|---|---|---|

| Strike Off | Companies Act, Section 248 | Defunct companies with liabilities extinguished |

| Voluntary Winding Up | IBC, Section 59 | Solvent companies needing assets or claims administered |

| Compulsory Winding Up | Companies Act, Section 271 | Statutory misconduct, filing defaults, public-interest grounds |

For most US companies voluntarily exiting India — whether due to a change in business direction or a decision to exit the Indian market — the relevant choice is between Strike Off and Voluntary Winding Up.

Types of Company Winding Up in India

Strike Off (Fast Track Exit)

Strike Off under Section 248 of the Companies Act, 2013 is the fastest and least expensive closure route. It is available when a company has either failed to commence business within one year of incorporation, or has carried on no business during the two immediately preceding financial years without obtaining dormant company status.

Critical requirement: The company must have its liabilities fully extinguished before applying. A company with outstanding creditor claims, active bank transactions that contradict a nil-liability position, or unfiled returns is not eligible — regardless of how long it has been inactive.

The application is filed via Form STK-2 with the ROC, supported by:

- STK-3 (indemnity bond)

- STK-4 (affidavit)

- STK-8 (statement of accounts, dated no more than 30 days before STK-2 filing)

According to MCA's C-PACE system, the benchmark for Strike Off has improved to approximately 100 days, down from 180 days.

Voluntary Winding Up (IBC Section 59)

Voluntary Winding Up is the right path when the company has assets, liabilities, or creditor claims that need to be formally administered. The key requirement: the company must not be in default at the time of initiating the process.

Key features:

- A majority of directors sign a solvency declaration affirming the company can pay all debts in full from asset proceeds

- Members pass a special resolution within 4 weeks of the declaration

- If debt exists, creditors representing two-thirds in value must approve within 7 days

- An Insolvency Professional (IP) registered with the IBBI is appointed as liquidator

IBBI data as of September 2025 shows 2,417 voluntary liquidations initiated, with closed cases averaging 397 days from commencement to final report — nearly 4.5x the statutory target of 90 days (no creditor involvement), and 47% over the 270-day ceiling (with creditor approval).

Compulsory Winding Up (Section 271)

Compulsory Winding Up is tribunal-ordered and initiated by the NCLT on petition. Current grounds under Section 271 include:

- Company passes a special resolution to wind up

- Sovereignty or public-order concerns

- Fraudulent affairs or unlawful purpose

- Failure to file statements or returns for 5 consecutive financial years

- Just-and-equitable test (court's discretion)

Any of these grounds can expose a US parent company's India subsidiary to tribunal intervention with little warning. This route carries significant reputational and legal complications — and directors of defaulting companies face personal disqualification under Section 164(2). US companies with inactive Indian subsidiaries should act proactively, well before a petition becomes possible.

Step-by-Step Process to Wind Up Your Indian Company

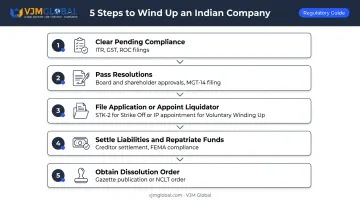

Both Strike Off and Voluntary Winding Up share the same mandatory pre-requisite: all pending compliance must be cleared before any application proceeds.

Step 1: Clear All Pending Compliance

The ROC and NCLT will reject applications from companies with outstanding:

- Income Tax Returns (ITRs)

- GST returns

- ROC annual filings — AOC-4 (financial statements) and MGT-7 (annual return) — up to the financial year in which business ceased

- Unpaid taxes or TDS obligations

This is the single most common reason wind-up applications stall for US-owned entities. Audit and clear all arrears with an Indian compliance partner before filing — delays here push back every subsequent step.

Step 2: Pass Board and Shareholder Resolutions

For Strike Off:

- Directors pass a board resolution approving closure

- Shareholders pass a Special Resolution (75% of paid-up share capital) or provide written consent

- File MGT-14 with the ROC within 30 days

For Voluntary Winding Up (IBC Section 59):

- Majority of directors sign the solvency declaration (affidavit-verified), attaching audited financials for the previous 2 years; include a registered valuer's report if assets exist

- Members pass a special resolution within 4 weeks and appoint an IP as liquidator

- If debt exists, creditor approval (two-thirds in value) must follow within 7 days

- File MGT-14 within 30 days of the special resolution

Step 3: File the Application or Appoint a Liquidator

For Strike Off, file Form STK-2 with the ROC. The ROC issues a public notice (STK-6) allowing 30 days for objections. If no valid objections are received, the ROC issues the final strike-off notice (STK-7), published in the Official Gazette.

For Voluntary Winding Up, the appointed IP:

- Publishes Form A (public announcement) within 5 days of commencement

- Invites creditor claims within 30 days

- Submits a preliminary report to the corporate person within 45 days

Step 4: Settle Liabilities, Distribute Assets, Repatriate Funds

The liquidator administers asset realisation and settles creditors in the legally prescribed priority order. Any remaining surplus is distributed to shareholders — in the case of a US parent, this triggers FEMA compliance obligations (covered in detail in the next section).

Section 178 of the Income Tax Act requires the liquidator to:

- Notify the Assessing Officer within 30 days of appointment

- Hold back the amount specified by the Assessing Officer for tax liabilities before making any distribution

Step 5: Obtain the Dissolution Order

For Voluntary Winding Up: The liquidator files the final report and dissolution application with the NCLT. The NCLT passes a dissolution order, which the liquidator must submit to the registration authority within 14 days.

For Strike Off: Dissolution occurs upon publication of STK-7 in the Official Gazette. The company's certificate of incorporation is cancelled at that point.

Special Considerations for US Business Owners

FEMA Compliance and Repatriation

When a US parent entity repatriates residual proceeds from winding up its Indian subsidiary, the Foreign Exchange Management (Non-debt Instruments) Rules, 2019 apply. The RBI permits repatriation of qualifying winding-up proceeds through an AD Category-I bank — which checks liquidation documents, tax payment evidence, and auditor confirmations before processing the remittance.

Key points:

- Blanket prior RBI approval is not required for standard cases; the AD bank handles eligible remittances

- Non-standard or non-compliant cases must be referred to RBI directly

- FEMA violations carry penalties of up to 3 times the quantifiable sum involved under Section 13, with continuing contraventions attracting up to ₹5,000 per day

Indian Tax Obligations

Liquidation distributions contain two components with different tax treatment:

- Deemed dividend under Section 2(22)(c) — attributable to accumulated profits

- Capital gains under Section 46(2) — on the remaining qualifying amount

For unlisted shares held more than 24 months, the long-term capital gains rate under Section 112 is 12.5% (plus applicable surcharge and cess) for disposals on or after July 23, 2024. Section 195 withholding applies only to the extent sums are chargeable to Indian tax — not automatically on every rupee remitted.

Note that transfer pricing obligations don't end with liquidation:

- Sections 92D and 92E documentation requirements apply for any year containing international transactions with the US parent

- Form 3CEB must be filed regardless of the liquidation status

US Tax Implications

US companies should consult their US CPA on how to characterise any loss or gain on the Indian investment — whether it qualifies as an ordinary loss or capital loss, and how Subpart F income, GILTI inclusions, or Previously Taxed Earnings and Profits (PTEP) accounts are affected. This guide does not constitute US tax advice; a US-India cross-border tax advisor is essential here.

Entity Type Matters

The closure path depends on how the US company is structured in India:

| Entity Type | Closure Route |

|---|---|

| Private Limited Company | Companies Act Section 248 (Strike Off) or IBC Section 59 (Voluntary Winding Up) |

| LLP | LLP Act Section 75; defunct LLP applies via Form 24 (separate from STK-2) |

| Branch Office | FEMA framework; closure application through designated AD Category-I bank |

| Liaison Office | Same FEMA route; annual/final activity and auditor compliance certificates required |

Branch Offices and Liaison Offices are not wound up through the ROC/NCLT route. Their closure involves the designated AD bank, with supporting documentation including auditor certificates confirming asset/liability position, remittable amounts, and litigation confirmations.

Working with the Right Advisors

Managing Indian regulatory requirements alongside US tax and FEMA obligations simultaneously is where most US business owners hit friction. VJM Global has guided 500+ American business owners through exactly this process, covering FEMA advisory, ROC compliance clearance, cross-border transaction advisory, and repatriation support.

For wind-up engagements, reach out at vjmglobal.com or email info@vjmglobal.com to discuss your entity's specific situation.

Common Mistakes to Avoid

Three mistakes consistently derail US-owned company wind-ups in India. Each one is avoidable with the right preparation.

Filing for Strike Off when the company is ineligible. US owners often assume that because their company "stopped operating," it qualifies for the fast-track exit. It doesn't. Outstanding GST liabilities, unfiled ITRs, active bank accounts with ongoing transactions, or pending legal proceedings will all cause the STK-2 application to be rejected.

A rejected application isn't just a delay. It can trigger compulsory strike-off notices from the ROC, which carries personal consequences for directors under Section 164(2).

Transferring funds without FEMA documentation. Some US companies move remaining cash without proper AD bank authorisation or supporting documentation. This constitutes a FEMA violation and can attract penalties of up to 3 times the amount transferred. Repatriation must follow the prescribed route — full documentation, correct form, correct bank channel.

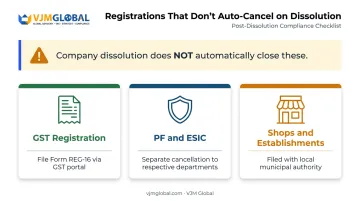

Assuming dissolution cancels all registrations. Company dissolution does not automatically close your other registrations. Each requires a separate cancellation filing:

- GST registration: Form REG-16 filed through the GST portal

- PF/ESIC: Separate cancellation applications to the respective departments

- Shops & Establishments: Filed with the local municipal authority

Many US business owners discover months later that these registrations remained active, triggering continued compliance obligations well after the company ceased to exist.

Frequently Asked Questions

How much does it cost to wind up a company in India?

Costs differ by method. Strike Off involves government filing fees (check the MCA portal for current STK-2 fees), professional fees, and compliance clearance costs. Voluntary Winding Up under IBC runs higher due to mandatory IP appointment and NCLT proceedings. Get a professional assessment for your entity's specific situation before committing to either route.

Can a foreign company be wound up in India?

Yes. A foreign company's Indian subsidiary, incorporated under Indian law, follows the same process under the Companies Act, 2013 or IBC, 2016. The US parent must additionally address FEMA/RBI compliance for repatriation. Branch Offices and Liaison Offices follow a separate RBI-approved closure path through the designated AD Category-I bank, not the ROC/NCLT route.

What are the types of company winding up in India?

Three main types: Strike Off (fast track exit under Companies Act Section 248), Voluntary Winding Up (IBC Section 59, for solvent companies with assets and liabilities to administer), and Compulsory Winding Up (tribunal-ordered under Companies Act Section 271, typically for filing defaults, fraud, or public-interest grounds).

What is the difference between strike off and winding up in India?

Strike Off removes a company's name from the ROC register administratively — it assumes liabilities are already extinguished and no formal asset administration is needed. Winding Up is a formal liquidation involving an IP, creditor settlement process, and NCLT dissolution order. Strike Off suits truly defunct companies; Voluntary Winding Up suits companies with remaining obligations to settle.

How long does it take to wind up a company in India?

Strike Off benchmarks at approximately 100 days under MCA's C-PACE system, assuming all compliance is current at the time of filing. Voluntary Winding Up averages 397 days based on IBBI data for processes closed by final report as of September 2025, though statutory targets are 90 or 270 days depending on creditor involvement.

Do US companies need RBI approval to repatriate funds after winding up their Indian subsidiary?

Prior RBI approval is not required for standard repatriation of original foreign investment proceeds — eligible amounts are processed through the designated AD Category-I bank. However, capital gains may require withholding tax clearance first, FEMA reporting obligations apply, and non-standard cases are referred to RBI. Professional guidance is strongly recommended before initiating any remittance.