Introduction

India represents one of the most attractive expansion markets for UK businesses, offering a rapidly growing economy, a skilled workforce, and increasing consumer demand. Yet the regulatory reality catches many companies off guard.

A UK subsidiary incorporated in India is treated as a domestic Indian company under the Companies Act, 2013, not as a foreign branch. This means it is subject to the full spectrum of Indian compliance obligations across five major pillars: corporate law (MCA/ROC), tax (Income Tax Act), FEMA/RBI reporting, GST, and labour laws.

According to data from the Department for Promotion of Industry and Internal Trade, most sectors permit 100% FDI via the automatic route — entry is straightforward. Ongoing compliance is where UK companies most often stumble.

Missing deadlines across these five pillars can result in financial penalties ranging from ₹1 lakh to ₹3 lakh under Section 392 of the Companies Act, director disqualification for up to five years, or loss of operating licence through ROC strike-off.

VJM Global has assisted over 250 UK businesses in navigating India's regulatory landscape, from incorporation to ongoing compliance management. This guide covers each compliance pillar in practical terms, with the deadlines, penalties, and filing requirements your Indian subsidiary will need to manage from day one.

TLDR:

- UK subsidiaries in India are domestic companies subject to full Indian corporate, tax, FEMA, GST, and labour law obligations

- Key corporate filings: 4 Board Meetings/year, AGM within 6 months, AOC-4, MGT-7, and DIR-3 KYC by 30 September

- Tax covers corporate tax at 25.17% (Section 115BAA), TDS, advance tax, and Form 3CEB transfer pricing by 30 November

- FEMA reporting (FC-GPR within 30 days, FLA by 15 July) is frequently overlooked and carries penalties up to 3x the amount involved

- India-UK DTAA reduces withholding tax to 10-15% on dividends, royalties, and interest—but requires annual TRC and Form 10F submission

How UK Companies Set Up a Subsidiary in India

The most common structure for UK companies entering India is a Private Limited Company incorporated under the Companies Act, 2013. This provides limited liability protection and establishes a separate legal entity with its own PAN (Permanent Account Number) and tax filings.

Incorporation Process:

The key steps include:

- Obtain Digital Signature Certificates (DSC) for all proposed directors

- Secure Director Identification Numbers (DIN) through the Ministry of Corporate Affairs portal

- Reserve company name via the SPICe+ form—ensure the name complies with naming conventions and does not conflict with existing entities

- File Memorandum of Association (MoA) and Articles of Association (AoA) with the Registrar of Companies (ROC), along with incorporation documents

- Receive Certificate of Incorporation from the ROC

- Obtain PAN and TAN from the Income Tax Department—mandatory before commencing business operations

With complete documentation, this process typically takes 15-20 days. Incomplete filings or rejected name reservations are the most common causes of delay.

FDI Routes and Sector Restrictions:

Post-Brexit, UK companies are treated as standard non-resident investors under India's FDI policy. Press Note 3 (2020) restrictions—which apply to countries sharing a land border with India—do not apply to UK entities.

Most sectors permit 100% FDI via the automatic route — no prior government approval needed. This includes IT services, consulting, e-commerce, and most manufacturing. Sectors that require government-route approval are listed below:

| Sector | FDI Cap | Approval Required |

|---|---|---|

| Defence | 100% | Beyond 74% |

| Multi-Brand Retail Trading | 51% | Up to 51% |

| News Broadcasting (TV) | 49% | Up to 49% |

| Print Media (News & Current Affairs) | 26% | Up to 26% |

| Banking (Private Sector) | 74% | Beyond 49% |

| Pharmaceuticals (Brownfield) | 100% | Beyond 74% |

UK companies in IT, professional services, or consulting can proceed directly via the automatic route without prior approvals — no government application needed.

PAN and TAN Registration:

Before commencing business, the subsidiary must obtain:

- PAN (Permanent Account Number): mandatory for all tax filings and financial transactions

- TAN (Tax Deduction and Collection Account Number): mandatory for deducting and remitting TDS

Both are required before the subsidiary can open a corporate bank account or file the INC-20A Declaration for Commencement of Business.

Corporate Compliance Under the Companies Act, 2013

Immediate Post-Incorporation Filings

Once incorporated, the subsidiary faces several time-sensitive obligations:

| Filing/Action | Deadline | Legal Basis |

|---|---|---|

| INC-20A (Declaration of Commencement) | Within 180 days of incorporation | Section 10A |

| INC-22 (Registered Office verification) | Within 30 days | Section 12 |

| First Board Meeting | Within 30 days | Section 173 |

| Appointment of First Statutory Auditor | Within 30 days (until first AGM) | Section 139 |

Failure to file INC-20A within 180 days prevents the company from legally commencing business operations. VJM Global frequently encounters UK clients who overlook this deadline, resulting in late filings and penalty payments.

Ongoing Board Meeting Requirements

The subsidiary must hold a minimum of 4 Board Meetings per financial year, with no more than 120 days between consecutive meetings. For UK parent companies, director attendance via video conferencing is permitted under Section 173, though meeting minutes must be maintained in India.

Missing the 120-day gap requirement triggers penalties under the Act — UK-based directors should schedule all four meetings at the start of each financial year to avoid a compliance breach.

Beyond meeting cadence, a parallel set of annual filings runs to the Registrar of Companies (ROC) on fixed statutory deadlines.

Annual Filing Obligations with ROC

| Filing | Deadline | Notes |

|---|---|---|

| AGM (Annual General Meeting) | Within 9 months of FY close (first year); 6 months for subsequent years (by 30 September) | Section 96 |

| AOC-4 (Financial Statements) | Within 30 days of AGM | Section 137 |

| MGT-7 (Annual Return) | Within 60 days of AGM | Section 92 |

| DPT-3 (Return of Deposits) | 30 June annually | Rule 16 |

| ADT-1 (Auditor Appointment) | Within 15 days of AGM | Section 139 |

Missing these filings for three consecutive financial years triggers director disqualification under Section 164(2), affecting both Indian and UK-based directors serving on the board. This disqualification applies across all Indian companies where the individual holds directorship and lasts for five years.

Director-Level Annual Obligations

Every director on the Indian subsidiary board must complete:

- DIR-3 KYC: Annual KYC filing by 30 September

- MBP-1: Disclosure of Interest at the first Board Meeting of each financial year

- DIR-8: Non-disqualification declaration

UK-based directors must obtain a Digital Signature Certificate (DSC) registered in India to complete these filings — a step that's often overlooked until a deadline is imminent.

Statutory Registers and Records Maintenance

The Companies Act requires the subsidiary to maintain the following registers at its registered Indian office:

- Register of Members (MGT-1)

- Register of Directors and Key Managerial Personnel (Section 170)

- Minutes Books for Board and General Meetings

Without a physical India presence, UK-based management must appoint a local registered office to house these records — they must be available on-site for regulatory inspection at any time. VJM Global provides registered office services and ongoing compliance support to keep these obligations covered.

Tax Compliance: Corporate Tax, TDS, and Transfer Pricing

Corporate Income Tax Liability

A UK subsidiary incorporated in India is taxed as a domestic company on its global income. Under Section 115BAA, companies opting for the concessional regime pay an effective rate of 25.168% (22% base rate + 10% surcharge + 4% cess), compared to up to 34.944% under the normal regime for large companies.

Key benefit: Companies under Section 115BAA are exempt from Minimum Alternate Tax (MAT), which otherwise applies at 15% of book profits under the normal regime.

The trade-off: Section 115BAA requires permanent forfeiture of exemptions and deductions, including additional depreciation and SEZ benefits. UK subsidiaries should model both scenarios before making this irrevocable election at incorporation.

Advance Tax Payment Obligations

If estimated annual tax liability exceeds ₹10,000, the subsidiary must pay advance tax in four instalments:

| Instalment | Cumulative % Due | Due Date |

|---|---|---|

| 1st | 15% | 15 June |

| 2nd | 45% | 15 September |

| 3rd | 75% | 15 December |

| 4th | 100% | 15 March |

Non-payment attracts interest under Sections 234B (1% per month on total shortfall) and 234C (1% per month on instalment shortfall).

TDS (Tax Deducted at Source) Obligations

The subsidiary must deduct and deposit TDS on:

- Salary payments (Form 24Q, quarterly)

- Contractor and professional fees (Form 26Q, quarterly)

- Payments to non-residents, including the UK parent company (Form 27Q, quarterly)

Deposit deadline: 7th of the following month; March deductions by 30 April.

Critical for UK subsidiaries: TDS on payments to the UK parent for services, royalties, or interest is one of the most scrutinised compliance areas. Under Section 40(a)(i), failure to deduct TDS on payments to non-residents results in 100% disallowance of the expense in the subsidiary's tax assessment, directly inflating the subsidiary's taxable income.

Transfer Pricing Compliance

All international transactions between the Indian subsidiary and UK parent company must be conducted at arm's length under the Income Tax Act. This covers management fees, loan interest, royalties, IT services, and shared service charges.

Documentation requirements:

- Maintain transfer pricing documentation (Master File and Local File)

- File Form 3CEB (accountant's certificate) by 30 November of the following year

These requirements carry real audit risk. Indian tax authorities regularly issue notices for insufficient transfer pricing documentation, particularly around:

- Management fees charged by the UK parent

- Royalty and licence fee arrangements

- Interest rates on intercompany loans

- Shared service charges (IT, HR, finance)

VJM Global supports UK subsidiaries through this process, conducting benchmarking studies, preparing quarterly TDS returns, and maintaining contemporaneous documentation to defend intercompany arrangements during tax audits.

Annual Income Tax Return Filing

Once transfer pricing and TDS obligations are met, the subsidiary must file its annual income tax return.

ITR deadline: 31 October (if tax audit applies) or 30 November (if transfer pricing report required).

Tax audit threshold: ₹1 crore for business (enhanced to ₹10 crore if 95%+ transactions are through banking/digital modes); ₹50 lakh for professions.

FEMA and RBI Reporting Obligations

FEMA (Foreign Exchange Management Act) reporting is frequently overlooked by UK companies unfamiliar with RBI systems. Violations, however, carry penalties up to three times the amount involved.

Even if no fresh investments occurred during the year, the return is mandatory if previous FDI exists. If audited data is not available by 15 July, the entity may submit on a provisional/unaudited basis, with a revised return due once audited data is ready.

FC-TRS (Foreign Currency — Transfer of Shares)

Applicable when shares of the Indian subsidiary are transferred between the UK parent and an Indian resident—either by sale or gift—and must be reported within 60 days of the transfer. FC-TRS applies most often when UK companies restructure shareholding or bring in Indian co-investors.

FEMA Penalty Ceiling

For quantifiable violations, the penalty can reach three times the amount involved. A 2025 regulatory update introduced a reduced cap of ₹2 lakh (₹200,000) for certain technical violations, but intentional non-compliance remains heavily penalised.

VJM Global's FEMA compliance support, built on experience with 250+ UK businesses, helps UK parent companies manage RBI reporting timelines and structure remittances and share transactions correctly to avoid compounding penalties.

GST and Labour Law Compliance

GST Registration and Filing Requirements

GST registration is mandatory once turnover crosses the applicable threshold:

| Category | Regular States | Special Category States |

|---|---|---|

| Goods (intra-state) | ₹40 lakh | ₹20 lakh (most) / ₹10 lakh (Manipur, Mizoram, Nagaland, Tripura) |

| Services | ₹20 lakh | ₹10 lakh (Manipur, Mizoram, Nagaland, Tripura) |

GST Filing Deadlines:

- GSTR-1 (outward supply): 11th of the following month (monthly filers with turnover > ₹5 crore)

- GSTR-3B (summary return with tax payment): 20th of the following month

- GSTR-9 (annual return): 31 December of the following year (if turnover exceeds ₹2 crore)

Export of Services: UK subsidiaries in IT, consulting, or service sectors supplying to the UK parent may qualify for zero-rating under Section 16 of the IGST Act. To qualify, services must be supplied to a foreign entity with payment received in convertible foreign exchange — which allows the subsidiary to claim a refund of unutilised input tax credit.

VJM Global helps UK subsidiaries assess export classification eligibility and document zero-rating positions accurately under GST law.

Labour Law Compliance

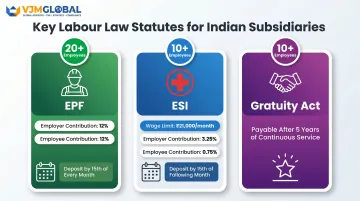

Beyond GST, UK subsidiaries with India-based staff must comply with three core central statutes — thresholds and contribution rates vary by headcount and payroll size:

| Statute | Threshold | Key Obligation | Deposit Deadline |

|---|---|---|---|

| EPF (Employees' Provident Fund) | 20+ employees | Employer and employee each contribute 12% of basic salary + Dearness Allowance (DA) | 15th of each month via ECR |

| ESI (Employees' State Insurance) | 10+ employees; wage limit ₹21,000/month | Employer 3.25%, Employee 0.75% | 15th of following month |

| Gratuity Act | 10+ employees | Payable after 5 years of continuous service | As per actuarial valuation |

Additional state-level obligations include Professional Tax registration (state-specific), Labour Welfare Fund (annual contributions), and the Shops and Establishments Act (state-wise registration).

UK businesses with Indian operations across multiple states face state-level variations in these obligations. VJM Global's payroll and compliance team manages these multi-state obligations on behalf of UK subsidiaries, reducing administrative burden across jurisdictions.

UK-Specific Considerations: DTAA and Profit Repatriation

India-UK Double Taxation Avoidance Agreement (DTAA)

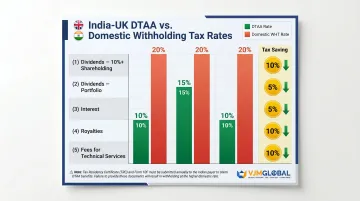

The India-UK DTAA provides reduced withholding tax rates on payments from the Indian subsidiary to the UK parent:

| Income Type | India-UK DTAA Rate | Indian Domestic Rate | Saving |

|---|---|---|---|

| Dividends (10%+ shareholding) | 10% | 20% | 10pp |

| Dividends (portfolio) | 15% | 20% | 5pp |

| Interest | 15% | 20% | 5pp |

| Royalties | 10% | 20% | 10pp |

| Fees for Technical Services | 10% | 20% | 10pp |

To claim DTAA benefits, the UK parent must provide:

- Tax Residency Certificate (TRC) from HMRC

- Form 10F filed electronically on the Indian e-filing portal

These are required annually. Missing these documents means the Indian subsidiary must apply the higher domestic withholding rate.

Dividend and Profit Repatriation

Since the abolition of Dividend Distribution Tax (DDT) in India (effective 1 April 2020), dividends paid to the UK parent are taxable in India at the point of payment, with TDS deducted at source. The lower DTAA rate (10% or 15%) applies provided the UK parent has submitted a valid TRC and Form 10F.

All outward remittances — dividends, loan repayments, and royalties — must comply with RBI/FEMA guidelines. A CA certificate (Form 15CA/15CB) is mandatory before the bank will execute any remittance.

Post-Brexit Context

The operational compliance picture above sits within a specific bilateral framework — one that shifted materially after Brexit. Two developments are directly relevant:

- UK-India BIT (1994): Terminated by India as part of a mass BIT termination covering 57–58 countries. UK investors no longer have treaty-level investment protection under that instrument.

- India-UK Free Trade Agreement: Signed on 24 July 2025, following negotiations that began in January 2022. Once ratified, the FTA is expected to affect tariff structures, professional services market access, and potentially certain withholding tax arrangements — though the full compliance implications will depend on the final ratified text.

UK subsidiaries operating in India should monitor FTA ratification closely, as provisions affecting cross-border payments or investment conditions may require updates to existing remittance and transfer pricing structures.

Consequences of Non-Compliance

Financial and Legal Penalties

Under Section 392 of the Companies Act, 2013:

- Company fine: ₹1 lakh to ₹3 lakh

- Continuing offence: Additional ₹50,000 per day

- Officers in default: Fine ₹25,000 to ₹5 lakh

FEMA violations: Penalties up to three times the amount involved; continuing violations attract ₹5,000 per day.

TDS non-deduction: Under Section 40(a)(i), 100% disallowance of payments to non-residents where TDS is not deducted; under Section 40(a)(ia), 30% disallowance for payments to residents.

These are concrete risks UK parent companies and their Indian directors personally face.

Broader Business Risks

Financial penalties are only part of the exposure. Missed filings and regulatory failures carry operational consequences that can be harder to reverse.

Director disqualification: Under Section 164(2), directors of a company that fails to file financial statements or annual returns for three consecutive financial years are disqualified for five years from holding directorship in any company. This applies equally to UK-based directors serving on the Indian board.

ROC strike-off: Under Section 248, the ROC may strike off a company not carrying on business for two consecutive financial years. Dormant subsidiaries must either apply for dormant status or maintain minimal compliance filings.

Reputational damage: Non-compliance affects relationships with Indian banks, customers, and regulators, undermining the subsidiary's credibility in the local market.

Loss of operating licence: In serious cases, compulsory strike-off by the ROC results in loss of the company's legal existence and all operating rights in India.

For UK subsidiaries, the cost of remediation — penalties, director reinstatement, ROC re-registration — consistently exceeds what structured compliance management would have cost. VJM Global's compliance retainer services handle deadline tracking, statutory filings, and direct regulatory representation, so these risks don't become emergencies.

Frequently Asked Questions

Can a foreign company be incorporated in India?

A foreign company cannot directly incorporate in India as a "foreign company" entity. However, it can establish an Indian-incorporated subsidiary (Private Limited Company) under the Companies Act, 2013, which operates as a separate legal entity subject to Indian laws.

What is a foreign wholly owned subsidiary in India?

A foreign wholly owned subsidiary (WOS) is an Indian-incorporated company in which 100% of equity shares are held by the foreign parent company. This structure is available in most sectors under the automatic FDI route, including for UK companies.

What is subsidiary compliance?

Subsidiary compliance covers the full set of regulatory obligations an Indian subsidiary must fulfil — corporate filings (ROC/MCA), tax returns (income tax, TDS, GST), RBI/FEMA reporting, and labour law contributions. These obligations apply regardless of the parent company's nationality.

How are subsidiary companies taxed?

An Indian subsidiary is taxed as a domestic company on its worldwide income at the applicable corporate tax rate (plus surcharge and cess). It must also comply with TDS, advance tax, and transfer pricing rules for any transactions with its UK parent.

How are foreign assets taxed in India?

Foreign assets held by an Indian-resident company are subject to Indian tax on income generated from those assets. Indian subsidiaries must disclose foreign assets in Schedule FA of their income tax return. Failure to disclose attracts steep penalties under the Black Money Act.

How does the UK-India Double Taxation Avoidance Agreement benefit UK subsidiaries in India?

The UK-India DTAA allows the UK parent to claim reduced withholding tax rates on payments received from the Indian subsidiary: dividends (10–15%), royalties (10%), interest (15%), and technical service fees (10%). It also prevents double taxation on the same income, provided the UK parent submits a valid TRC and Form 10F each year.