Introduction

Many Singapore companies applying for GST registration in India hit delays — or outright rejections — because they follow guides written for Indian domestic businesses. The rules for foreign entities are fundamentally different, and that gap causes real problems.

The core difference: foreign businesses have zero turnover threshold for mandatory GST registration, while Indian resident companies enjoy a ₹20–40 lakh exemption. If you're a Singapore company planning to sell products in India, provide B2B services to Indian clients, or participate in a trade exhibition, this guide covers the two registration pathways available to non-residents, the documents you'll need, and the compliance obligations that follow once you're registered.

Key Takeaways

- GST is India's unified indirect tax; Singapore businesses must register from their first taxable supply, with no minimum turnover threshold for non-residents

- Two routes exist: Non-Resident Taxable Person (NRTP) for temporary operations, or regular GST registration via an incorporated Indian entity

- NRTP registration is valid for 90 days, requires advance tax deposit, and mandates GSTR-5 monthly filing

- Registration is fully online at gst.gov.in and requires an authorised signatory plus foreign-entity documentation

- Post-registration compliance covering return filing, invoice formats, and record retention begins from the first taxable supply date

What Is GST in India and Why It Matters for Singapore Businesses

India's Goods and Services Tax is a unified, destination-based indirect tax that replaced a fragmented set of central and state taxes (VAT, excise, service tax) and applies to most supplies of goods and services across India.

Why this matters to Singapore companies:

Any Singapore business selling into India — products, B2B services, e-commerce, or even a temporary pop-up presence — likely has a GST obligation. This applies even without a permanent office or physical presence in India.

Understanding India's GST Components

India's GST operates through four distinct components:

- CGST (Central GST) - Collected by the central government on intrastate supplies

- SGST (State GST) - Collected by state governments on intrastate supplies

- IGST (Integrated GST) - Applies to interstate and cross-border transactions

- UTGST (Union Territory GST) - Collected by union territories on local supplies

For Singapore businesses, IGST is the most relevant component — it's the rate type non-resident foreign companies encounter most often when billing Indian clients or making interstate supplies.

When Does a Singapore Business Need to Register for GST in India?

**Foreign businesses have no threshold exemption** for GST registration in India. Unlike Indian resident businesses, which qualify for a ₹20–40 lakh turnover threshold (varying by business type and state), Singapore companies must register from the first taxable supply made in India.

Scenarios Triggering GST Registration for Singapore Companies

Singapore businesses must register when:

- Selling physical goods imported and sold in India

- Providing digital or online services to Indian customers

- Operating a temporary exhibition or trade stall

- Supplying through an Indian e-commerce marketplace

- Making interstate supplies of goods or services

- Providing B2B professional or consulting services to Indian clients

Exception: Registration Through an Indian Entity

Singapore companies operating through a formally incorporated Indian entity — a private limited company, LLP, or branch office — register as regular GST taxpayers under the turnover thresholds applicable to Indian resident businesses. This distinction fundamentally changes both the registration pathway and ongoing compliance obligations.

Voluntary Registration Benefits

A Singapore company not yet required to register can still do so voluntarily to:

- Claim input tax credit on purchases and business expenses

- Build credibility with Indian B2B buyers who require GST invoices

- Participate in the Indian supply chain

- Issue compliant tax invoices for interstate transactions

Risks of Non-Registration

The voluntary benefits above also underscore what's at stake when registration is skipped. Operating without required GST registration carries serious penalties:

- Penalty: 10% of tax due for unintentional non-registration

- Penalty: 100% of tax due in cases of deliberate evasion

- Inability to issue valid tax invoices, which blocks Indian clients and vendors from claiming input tax credit on transactions with your business

- Potential business disruption and reputational damage

Two Registration Pathways for Singapore Businesses

Singapore businesses entering India choose between two distinct registration routes based on the nature and duration of their operations.

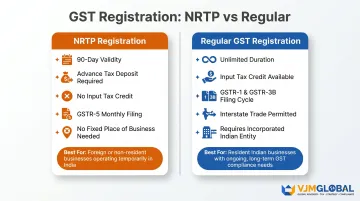

Pathway 1: Non-Resident Taxable Person (NRTP) Registration

NRTP status is designed for foreign businesses making occasional or time-limited supplies in India (such as participating in a trade fair or executing a short-term service contract) without a fixed place of business in India.

Key characteristics:

- Registration valid for 90 days (extendable for another 90 days)

- Requires estimating total tax liability for the period

- Advance tax deposit must be paid before registration approval

- Must file GSTR-5 monthly return

- Cannot claim input tax credit on purchases

- Registration lapses automatically after 90 days unless extended

These constraints — advance tax deposit, no input tax credit, and a hard 90-day ceiling — make NRTP registration impractical for sustained India operations.

Pathway 2: Regular GST Registration via an Indian Entity

Singapore companies establishing a subsidiary, wholly owned entity, branch office, or LLP in India register for GST as regular Indian taxpayers.

This route unlocks:

- Input tax credit (ITC) on business purchases and expenses

- Ability to conduct interstate trade without restrictions

- Ongoing compliance under the normal GSTR-1/GSTR-3B return cycle

- Credibility as a formally established Indian business

- No 90-day validity limitation

A Singapore company planning sustained India operations — selling products regularly, running a service delivery centre, or building an Indian customer base — should strongly consider the regular registration route. It reduces long-term compliance burden and opens more commercial opportunities.

Choosing the right pathway before applying for registration matters — the wrong structure can create avoidable compliance costs. VJM Global works with Singapore businesses to assess their entry structure and confirm which route fits their operational plans before the process begins.

Step-by-Step GST Registration Process for Foreign Businesses

The entire registration process happens online through gst.gov.in. Foreign or non-resident businesses without an Indian Aadhaar must appoint either an Indian-resident authorised signatory or a registered GST practitioner (tax agent) to submit and sign the application on their behalf. The five steps below walk through the full process.

Step 1: Determine Registration Type and Gather Documents

- Confirm which registration type applies (NRTP or regular via Indian entity)

- Prepare the full document checklist (detailed in the next section)

- For NRTPs: Calculate estimated GST liability for the registration period — this amount must be deposited upfront

Step 2: Create a Temporary Reference Number (TRN)

- Visit gst.gov.in → Services → Registration → New Registration

- Select applicable taxpayer type (e.g., Non-Resident Taxable Person)

- Enter basic details: foreign entity's legal name, country of origin, contact information

- Complete OTP-based verification of email and mobile number

- A 15-digit TRN is generated, valid for 15 days

Critical deadline: If Part B is not completed within 15 days, the process must restart from scratch.

Step 3: Complete Part B of Form GST REG-01

Log in using the TRN to complete the detailed application:

- Business constitution and legal structure

- Nature of business activities

- Principal place of business in India (or the address of the Indian tax agent)

- Authorised signatory details

- Bank account information (can be updated post-registration)

- Upload all required documents

- For NRTPs: Submit advance tax deposit challan reference

Step 4: Aadhaar Authentication and Verification

Key distinction for Singapore businesses: Aadhaar-based e-KYC is designed for Indian nationals. Foreign company applicants without Aadhaar proceed via:

- Biometric verification, or

- GST officer inspection (physical or document-based verification of the place of business, particularly for NRTP applications)

Practical tip: Engaging a registered GST practitioner (tax agent) handles the biometric or officer verification on your behalf — removing the main friction point for foreign applicants unfamiliar with the process.

Step 5: Receive ARN and GSTIN

- An Application Reference Number (ARN) is issued by SMS and email

- Track status: Services → Track Application Status on the GST portal

- Upon approval (typically 7–10 working days; potentially 3 days for simplified scheme-eligible businesses), a GSTIN — a unique 15-digit number — is issued

- Download the GST registration certificate from the portal

GSTIN structure: The 15-digit GSTIN includes the state code (first 2 digits), PAN-based identification (next 10 digits), entity number, and check digit — understanding this format helps verify registration authenticity.

Documents Required for GST Registration (Singapore Business Perspective)

The document requirements for foreign companies differ significantly from domestic applicants.

Core documents for Singapore businesses:

- Certificate of incorporation or registration from Singapore (apostilled if required)

- Proof of principal place of business in India (registered address provided by an Indian representative, office lease, or tax agent's address)

- PAN of the Indian entity (if incorporated locally) or equivalent identification document for NRTPs

- Bank account details (foreign currency account or Indian bank account opened for the entity)

- Letter of authorisation naming the authorised signatory

Documents Commonly Overlooked by Singapore Businesses

Digital Signature Certificate (DSC)

DSC is mandatory for companies and LLPs. A Class 3 DSC must be obtained in India for the authorised signatory, issued by a certifying authority in token form and valid for 1-2 years.

PAN Requirement

Foreign entities without PAN cannot use the standard PAN-based GSTIN and must work with the NRTP pathway or obtain PAN through incorporating an Indian entity.

Address Proof for Indian Registered Place of Business

Address proof for the registered place of business in India is required even if operations are remote — many Singapore companies miss this when planning virtual presence operations.

VJM Global's business setup team helps Singapore companies prepare and apostille required documents, obtain DSC, and verify the complete package meets current CBIC requirements before submission, reducing the risk of rejection or delays.

Post-Registration Compliance and Common Mistakes

Obtaining your GSTIN is the starting point, not the finish line. Compliance obligations begin immediately, and the requirements differ significantly depending on your registration type.

Key Ongoing Obligations

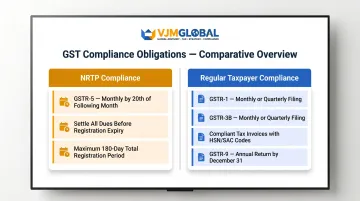

For NRTPs:

- File GSTR-5 monthly (by the 20th of the month following the tax period)

- Settle all tax dues before registration expires

- Cannot extend registration beyond 180 days total (initial 90 days + one 90-day extension)

For regular taxpayers (via Indian entity):

- File GSTR-1 (outward supplies) monthly or quarterly depending on turnover

- File GSTR-3B (summary return and tax payment) monthly or quarterly

- Maintain compliant tax invoices including GSTIN, HSN/SAC codes, and tax breakup in every invoice issued

- File GSTR-9 (annual return) by December 31 of the following financial year

Common Mistakes Singapore Businesses Make

1. Assuming threshold exemption applies

Many Singapore companies incorrectly assume their India operations fall below the ₹20–40 lakh threshold and skip registration. The zero-threshold rule for non-residents makes this a costly error — it results in penalties and business disruption.

2. Using NRTP for long-term business

Choosing NRTP registration when regular entity registration would be more appropriate creates unnecessary compliance burdens, prevents input tax credit claims, and requires frequent renewal applications.

3. No valid authorised signatory

Failing to appoint a valid authorised signatory before the application causes rejections and delays. Foreign businesses must designate either an Indian resident or engage a registered GST practitioner.

4. Missing document apostille or notarisation

Submitting documents without apostille or notarisation where required leads to verification failures and application rejection.

GST and the India-Singapore Tax Treaty

The India-Singapore tax treaty (DTAA) reduces or eliminates double taxation on income — but it does not exempt Singapore businesses from India's GST obligations on domestic supplies. The two regimes operate independently. DTAA governs income tax treatment; GST is a consumption tax on domestic supplies and applies regardless of any treaty provisions.

Understanding this distinction early helps Singapore businesses avoid the common assumption that treaty protections cover all Indian tax obligations — they don't.

Frequently Asked Questions

Who is eligible for GST registration in India?

Resident businesses must register once turnover crosses ₹20–40 lakh (varies by state and business type). Non-resident and foreign businesses must register from their first taxable supply in India, regardless of turnover. E-commerce operators, interstate suppliers, and online information service providers also face mandatory registration with no turnover threshold.

Can an NRI register for GST in India?

Yes. NRIs and OCIs can register for GST in India by incorporating an Indian entity or registering as a non-resident taxable person. The right pathway depends on whether they have a fixed place of business in India and the nature of their operations.

What are the 4 types of GST?

CGST (Central GST), SGST (State GST), IGST (Integrated GST for interstate and cross-border transactions), and UTGST (Union Territory GST). Singapore businesses supplying into India will most frequently encounter IGST on cross-border and interstate transactions.

Does a Singapore company need a PAN card to register for GST in India?

PAN is required for companies incorporated in India (including Indian subsidiaries of Singapore firms), but non-resident taxable persons (NRTPs) without an Indian PAN can use their foreign registration/identification documents. However, incorporating an Indian entity to obtain PAN is recommended for long-term operations as it simplifies compliance and unlocks additional business benefits.

How long does GST registration take for a foreign company in India?

The standard processing time is 7–10 working days after a complete application is submitted. A simplified fast-track process introduced in November 2025 allows eligible businesses to receive GSTIN within 3 working days. NRTP applications requiring officer inspection may take longer.

Ready to register your Singapore business for GST in India? VJM Global's team of GST specialists and business setup professionals provides end-to-end support — from determining the right registration pathway to post-registration compliance. Contact us at +91 9213397070 or info@vjmglobal.com to discuss your India market entry strategy today.