Introduction

Many foreign business owners assume that stopping operations is enough to close a Singapore company. It isn't. ACRA and IRAS continue to hold directors personally accountable until the company is formally deregistered — and failing to follow the correct procedure triggers penalties, tax complications, and ongoing legal liability that can follow you well after the business stops trading.

Directors who leave a company registered without meeting filing obligations face fines up to SGD 5,000 each, late annual return penalties of up to SGD 600 per filing, and potential prosecution for persistent non-compliance. These obligations don't pause when business stops — they run until deregistration is complete.

This guide is for foreign business owners, directors of private limited companies, and multinationals with Singapore-based entities weighing closure. The right path depends on your company's financial position and entity type — and choosing the wrong method can set the process back by months.

Key Takeaways

- Singapore companies close through striking off (solvent, no debts) or winding up (insolvent or asset distribution required)

- Striking off is free and takes 4–6 months; winding up requires a licensed liquidator and can take 6 months to 3 years

- Before applying, settle IRAS tax clearance, CPF contributions, employee payouts, licence cancellations, and final accounts

- Applications submit via ACRA's BizFile+ portal, triggering a gazette process with objection windows

- Applications fail when debts remain unpaid, litigation is pending, or director consent is missing

What "Closing a Company" Actually Means in Singapore

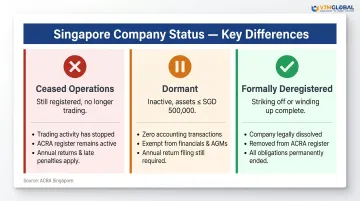

Formally closing a company in Singapore means deregistering the entity with ACRA so it no longer legally exists. This is fundamentally different from simply ceasing operations or going dormant — each status carries distinct obligations.

The three statuses differ significantly:

- Ceasing operations: Trading stops, but the company stays live on ACRA's register. Annual returns, financial statements, and director notifications still apply — penalties accumulate if ignored.

- Becoming dormant: No accounting transactions occur during the period. Under Section 205B of the Companies Act, qualifying dormant companies (private, non-listed, assets ≤ SGD 500,000) are exempt from financial statements and AGMs, but must still file annual returns.

- Formal deregistration: Striking off or winding up removes the company entirely, ending all obligations.

The closure process also varies by entity type:

- Representative Office: Must notify Enterprise Singapore upon closure

- Branch Office: Must file cessation via BizFile+ within 7 days of business ceasing in Singapore

- Private Limited Company (Pte Ltd): Must complete either striking off or winding up

This guide focuses on Pte Ltd closure — the most complex structure and the one most foreign companies use when operating in Singapore.

Striking Off vs Winding Up: Which Route Is Right for You?

Striking Off: The Faster Route for Clean Exits

Striking off is ACRA's streamlined closure process for companies that have genuinely ceased operations. It's free, requires no liquidator, and typically completes within 4-6 months. However, eligibility is strict.

Your company qualifies for striking off only if it meets all six criteria:

- Has stopped trading or never commenced business since incorporation

- Has no unpaid debts or unresolved issues with any government agency

- Has no registered charges (loans) in the charge register

- Is not involved in any legal cases (ongoing or pending) in Singapore or overseas

- Is not subject to regulatory action or disciplinary proceedings

- Owns nothing and owes nothing (no property, debts, or potential future claims)

All directors (or a majority) must consent, and there can be no outstanding court summons.

Winding Up: When Formal Liquidation Is Required

Winding up involves appointing a licensed liquidator to formally dissolve the company through a structured asset distribution and debt settlement process. It's required when a company cannot pay its debts, or when directors choose to formally dissolve a solvent company that still holds assets.

Three types of winding up exist:

| Type | When It Applies | Key Requirement |

|---|---|---|

| Members' Voluntary Winding Up (MVL) | Company is solvent and can pay all debts within 12 months | Directors must file a Declaration of Solvency under IRDA Section 163 |

| Creditors' Voluntary Winding Up (CVL) | Company is insolvent and cannot continue due to debts | Creditors' meeting required; creditors appoint the liquidator |

| Compulsory Winding Up | Court orders winding up (e.g., unpaid debts, fraudulent activity, failure to file documents) | Court petition required |

For MVL, directors making a false solvency declaration face fines up to SGD 5,000 or imprisonment up to 12 months, or both.

The Decision Rule

Use the following to identify your path before proceeding.

Choose striking off if:

- Company is completely debt-free

- No assets remain

- Business has stopped trading

- No registered charges exist

- No legal proceedings are pending

Choose Members' Voluntary Winding Up if:

- Company is solvent but holds assets to distribute to shareholders

- You want a structured, formal dissolution process

- Company can pay all debts within 12 months

If the company is insolvent or facing creditor pressure, the voluntary route is no longer available.

Choose Creditors' Voluntary or Compulsory Winding Up if:

- Company cannot pay debts as they fall due

- Total liabilities exceed total assets

- A creditor has served a statutory demand for SGD 15,000+ that remains unpaid for 3 weeks

Most Singapore companies use striking off — it's faster, costs nothing, and works cleanly when there are no outstanding obligations.

How to Close a Company in Singapore: Step-by-Step

The striking off process involves six key stages from eligibility assessment through gazette notification and final dissolution. The timeline depends largely on IRAS tax clearance (typically 2-6 months) and whether objections arise during the gazette period.

Step 1: Assess Your Company's Financial Position

Before choosing a closure method, directors must determine whether the company is solvent. Singapore insolvency law applies two tests:

- Cash Flow Test: Can the company pay its debts as and when they fall due?

- Balance Sheet Test: Do total liabilities exceed total assets?

The Singapore Court of Appeal has held that the cash flow test is the sole determinative test for deemed insolvency under IRDA Section 125(2)(c).

Critical threshold: Under IRDA Section 125(2)(a), a company is deemed unable to pay its debts if a creditor owed more than SGD 15,000 serves a written demand at the registered office. If the company fails to pay (or secure/compound it to the creditor's satisfaction) within 3 weeks of service, this can trigger compulsory winding up proceedings.

Settle all debts exceeding this threshold as a priority during pre-closure planning.

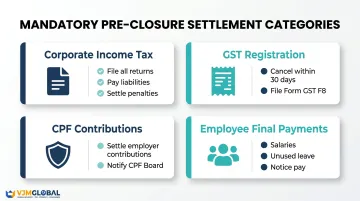

Step 2: Settle All Outstanding Liabilities and Notify Relevant Parties

No striking off application will proceed until all obligations are cleared. ACRA and IRAS coordinate closely, and any outstanding matter will trigger an objection.

Mandatory settlements include:

- Corporate Income Tax: File all returns (Form C-S/C-S Lite/Form C) up to cessation date; pay all liabilities and penalties in full

- GST Registration: Cancel within 30 days of business cessation if registered; file final Form GST F8 within one month; account for output tax on business assets exceeding SGD 10,000 total value

- CPF Contributions: Settle all outstanding employer contributions; inform CPF Board of business termination

- Employee Salaries: Pay all final salaries, unused annual leave, and notice pay on the employee's last day of work

Critical CPF distinctions for final payments:

| Payment Type | CPF Payable? |

|---|---|

| Compensation in lieu of notice (employer to employee) | No |

| Wages during notice period (employee working through notice) | Yes |

| Encashment of unused annual leave | Yes |

| Retrenchment benefits | No |

Budget accurately: CPF contributions are required on leave encashment but not on compensation in lieu of notice or retrenchment benefits.

One more step often overlooked: do not close corporate bank accounts yet. The account must stay open until all debts are settled and pending tax refunds or final receipts are received. Premature closure can block IRAS refunds and prevent you from settling remaining obligations.

Step 3: Prepare Final Financial Statements and File for Tax Clearance

The company must prepare final management accounts and file its last tax return with IRAS using the digital service titled "Apply for Waiver/ File last Form C-S/ C (Dormant/ Striking Off)" (effective from 1 August 2026).

IRAS tax clearance timeline:

- Straightforward cases (approximately 80%): Assessment completed by the 2nd month

- Complex cases (approximately 20%): Assessment completed by the 6th month (queries issued by 2nd month, response required by 4th month)

- Payment due: Within 30 days of Notice of Assessment

Critical warning: Settle all outstanding tax matters with IRAS before applying for strike off with ACRA. If IRAS objects and the matter is not resolved within 2 months, the entire application lapses. You will then need to submit a new ACRA application from scratch after clearance.

GST deregistration process:

- Apply via mytax.iras.gov.sg within 30 days of cessation

- Most online applications approved same day; some take 1-10 working days

- File final GST return (Form GST F8) within one month from end of accounting period

- Retain business records for at least 5 years after deregistration

In practice, starting IRAS clearance 3-6 months before your intended ACRA filing date gives you enough buffer to handle queries without disrupting your timeline.

Step 4: Submit the Striking-Off Application via BizFile+

Directors (or a Corporate Service Provider acting on their behalf) submit the application through ACRA's BizFile+ portal at no cost.

Application requirements:

- Majority of directors must consent to striking off

- Applicant must confirm the company meets all six eligibility criteria

- Declaration that all information provided is accurate and complete

- If multiple directors exist, co-directors must endorse the application within 14 days or it lapses

Consequence of false declarations: Applying without meeting eligibility criteria constitutes a false declaration, which can lead to investigation and prosecution.

Corporate Service Provider applications: If a CSP applies on behalf of the company, endorsements through BizFile+ are not required, though the CSP must ensure majority director consent was obtained beforehand.

Step 5: Navigate the Gazette Notification and Objection Period

After ACRA approves the application, the gazette process begins:

- ACRA approval: Immediate or after the 14-day endorsement period

- Striking-off letter: ACRA sends notification to the company's registered office and officers

- Officer objection window: Company officers have 30 days from the letter date to submit objections

- First Gazette Notification: Published within 30 days of approval

- Public objection period: 60 days following the First Gazette during which any interested party may object

- Objection resolution window: If an objection is filed, the company has 2 months to resolve it with the objector

- Application lapse: If objection not resolved within 2 months, the striking-off application lapses

- Final Gazette Notification: If no objections received, ACRA publishes the Final Gazette and the company is officially dissolved

Common objectors include:

- IRAS (outstanding tax matters)

- CPF Board (unpaid contributions)

- Creditors (unpaid debts)

- Government agencies (unresolved regulatory matters)

Step 6: Confirmation of Dissolution

Once the Final Gazette Notification is published, the company is removed from ACRA's register and ceases to exist as a legal entity. Any remaining tax credits transfer to the Insolvency and Public Trustee's Office upon dissolution.

Restoration possibility: A struck-off company can be restored within 6 years of being struck off via Court Order.

For Members' Voluntary Winding Up: Under IRDA Section 180(6), dissolution occurs 3 months after the liquidator lodges the final return with ACRA and the Official Receiver. The court can void the dissolution within 2 years under Section 208(1).

Any unresolved liabilities or pending claims should be addressed before the liquidator files the final return — once the 3-month window closes, unwinding the dissolution requires a court application.

What to Do Before You Apply: A Pre-Closure Checklist

Cancel All Business Licences and Permits

Licences cannot be transferred and failing to cancel them delays closure. Key licensing bodies include:

- MAS (Monetary Authority of Singapore): Cancel all financial services licences

- Ministry of Manpower: Cancel Employment Passes and work permits tied to the company

- Industry-specific regulators: Cancel sector-specific licences and permits

Contact each regulatory body well in advance of your ACRA application.

Communicate Closure to Employees with Adequate Notice

Employers with at least 10 employees must:

- Submit Mandatory Retrenchment Notification to MOM within 5 working days of informing employees

- Non-compliance results in SGD 1,000 penalty for first offence, SGD 2,000 for subsequent contraventions

Retrenchment benefit norms:

- 2 weeks to 1 month's salary per year of service (depending on company financial position and industry)

- Unionised companies: typically 1 month per year

- Eligibility: employees with at least 2 years of service

Final payment requirements:

- Pay all salaries, unused annual leave, and notice pay on the employee's last day of work

- Include CPF contributions for wages during notice period and leave encashment

Terminate Contracts with Suppliers, Service Providers, and Landlords

Review all contractual obligations and serve notice as required by written agreements. Failing to provide contractual notice periods can result in compensation claims that complicate the ACRA application. Notify customers of the closure date as well — this manages expectations and helps preserve business relationships through the wind-down.

For Foreign Companies: Coordinate Cross-Border Obligations

Foreign companies closing Singapore entities face additional coordination requirements:

- Inform parent company or head office of intended closure

- Notify home-country tax authorities of the Singapore entity's dissolution (may trigger capital repatriation or intercompany debt settlement requirements)

- Clear all intercompany balances before the strike-off application

- Resolve intercompany loans, transfer pricing settlements, and foreign exchange positions before filing

Coordinating these obligations across tax jurisdictions and regulatory regimes carries significant compliance risk. A cross-border advisory firm with Singapore and home-country expertise can reduce that risk considerably.

Common Mistakes and When to Consider Alternatives

Don't Close the Corporate Bank Account Too Early

The bank account should remain open until all debts are paid and any pending tax refunds or final receipts are cleared. Premature closure prevents the company from receiving IRAS refunds or settling final obligations that arise during the gazette period.

Stopping Operations Is Not the Same as Closing the Company

Many directors stop trading but fail to file for striking off, leaving the company "live" on ACRA's register. The consequences of inaction pile up quickly:

- Annual filing obligations and late fees continue to accrue

- ACRA may initiate its own striking-off proceedings

- Persistent non-compliance can lead to prosecution of directors

Common Misconception: Outstanding Annual Returns Block Striking Off

ACRA permits striking-off applications even if the company has outstanding Annual Returns, provided all other eligibility criteria are met and no summons are pending. However, the company must resolve any summons before applying.

Alternative to Consider: Dormancy

If your company is temporarily inactive but may resume business, keeping it dormant avoids re-incorporation costs and brand loss if you revive it later.

Dormant company requirements:

- No accounting transactions during the dormant period

- Total assets not exceeding SGD 500,000 (for private companies)

- Exempt from preparing financial statements and holding AGMs

- Must still file annual returns with ACRA

In short, dormancy keeps the door open with minimal upkeep — a practical choice if there's any realistic chance you'll restart operations within the next few years.

Frequently Asked Questions

How to close down a company in Singapore?

Choose between striking off (for solvent, inactive companies with no assets or liabilities) or winding up (for insolvent companies or those with assets to distribute). Clear all debts and tax obligations with IRAS, CPF, and other agencies, then submit your application to ACRA via BizFile+.

How much does it cost to close a company in Singapore?

The striking-off application is free via ACRA. Professional fees for a Corporate Service Provider typically run SGD 500–2,000, while liquidator fees for a Members' Voluntary Liquidation range from SGD 8,000–15,000. Outstanding tax clearance and compliance filing fees add to the total.

How long does it take to close a company in Singapore?

Striking off typically takes 4-6 months, subject to IRAS tax clearance (2-6 months depending on complexity) plus the gazette objection period. Liquidation timelines vary from 6 months for straightforward cases to 2-3 years for complex situations involving multiple creditors or disputed assets.

How to close a sole proprietorship in Singapore?

Sole proprietorships deregister through ACRA's BizFile+ portal under a simpler process than company closure. The sole proprietor settles all outstanding obligations, notifies IRAS, cancels GST registration if applicable, and files the cessation online. Processing is immediate with no gazette period — much faster than closing a Pte Ltd.

How long before a debt is written off in Singapore?

Under Singapore's Limitation Act, most unsecured debts carry a 6-year limitation period, after which creditors cannot sue to recover them. Debts are not automatically written off, though — unresolved liabilities can still block a company's striking-off eligibility with ACRA.