Introduction

With 4,032 construction insolvencies recorded in 2024—the highest of any UK sector—getting the numbers right is not a back-office concern. It's a survival requirement.

UK construction accounting is fundamentally different from standard business accounting. Long-term contracts, staged payments, CIS deductions, retention periods, and unpredictable cash flow create challenges that standard bookkeeping simply wasn't built for.

According to HMRC data, CIS deductions alone totalled £692.5 million in April 2024. Even a profitable project can destroy a business if cash flow isn't tracked correctly at the job level.

This guide covers the accounting methods UK contractors use, CIS compliance obligations, the VAT Domestic Reverse Charge, job costing and WIP schedules, and cash flow management tactics. It also includes 2025/26 regulatory updates so you know exactly what's changing and when.

Key Takeaways

- Construction accounting tracks finances project-by-project, not just at the business level

- CIS requires contractors to deduct tax (20% or 30%) from subcontractor payments each month

- The VAT Domestic Reverse Charge shifts VAT liability from subcontractor to contractor

- Job costing and WIP schedules differ significantly from standard accounting methods

- Making Tax Digital requirements are expanding, so verify your software meets the latest standards

Why Construction Accounting Differs from Standard Accounting

Most businesses operate on a simple buy-and-sell model: purchase inventory, sell it, record the transaction. Construction is fundamentally different. Projects involve multiple stakeholders, numerous subcontractors, timelines spanning months or years, staged payments tied to milestones, and costs committed long before income is received.

The practical consequences are severe:

- Profit and loss statements can look healthy overall while individual projects bleed money unnoticed

- A packed order book doesn't guarantee cash availability when payroll or supplier invoices are due

- PAYE obligations for direct employees and CIS deductions for subcontractors create parallel payroll complexities that multiply administrative burden

The regulatory environment is equally demanding. Contractors must simultaneously comply with:

- CIS registration and monthly return filing

- VAT Domestic Reverse Charge rules (since March 2021)

- GAAP/FRS 102 or IFRS 15 revenue recognition standards

Non-compliance with any one of these triggers HMRC penalties, and ignorance is not a defence.

These compliance demands make the choice of accounting method more consequential in construction than in almost any other sector.

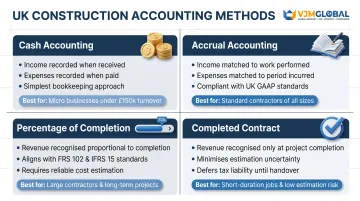

Key Accounting Methods Used in UK Construction

UK contractors typically use one of four methods:

1. Cash Accounting Income and expenses are recorded when money changes hands. It works for micro businesses with turnover below £150,000, but leaves committed costs and future liabilities invisible — a real risk on project-based work.

2. Accrual Accounting Income and expenses are recorded when invoiced, regardless of payment timing. This is the standard for most construction companies and provides a more accurate picture of financial position.

3. Percentage of Completion Revenue is recognised proportionally as a project progresses, based on costs incurred or physical completion. Common for larger contractors operating under FRS 102 Section 23 or IFRS 15. Requires detailed cost tracking and estimation.

4. Completed Contract All income is deferred until project completion. This reduces estimation risk on short jobs, though it creates large profit swings in annual accounts — a pattern that can catch directors off guard at year-end and distort Corporation Tax timing.

Your accounting method directly impacts Corporation Tax timing, financial reporting accuracy, and how Work in Progress (WIP) is presented to lenders or HMRC. Align your decision with project duration and turnover — and confirm the approach with a qualified accountant before your next financial year begins.

Job Costing, WIP, and Revenue Recognition

Job costing is the practice of assigning every cost to a specific project code. This includes:

- Materials (direct and indirect)

- Direct labour (site workers, foremen)

- Subcontractor fees

- Equipment depreciation

- Site-specific overheads (temporary utilities, site offices, permits)

Job costing allows profitability to be tracked at the job level, not just across the business. Without it, you're flying blind.

Getting job costing right means capturing two distinct types of expenditure:

- Direct costs: Easily attributable to a single project (for example, bricks ordered for a specific house)

- Indirect/overhead costs: Insurance, vehicle use, storage, head office salaries — must be apportioned fairly across projects

Common mistake: Failing to capture indirect costs. This is one of the most common reasons jobs appear profitable on paper but aren't in reality.

Work in Progress (WIP) Schedules

WIP schedules reconcile certified work against costs incurred to date. They:

- Flag over-billing (where invoices exceed work completed) and under-billing (where work exceeds invoices)

- Allow finance teams and quantity surveyors to spot margin erosion before it becomes unrecoverable

- Must be aligned with retention balances for accuracy

Retention (retainage): Typically 5–10% of contract value is withheld by clients until practical completion or defect remedy. Contractors track these as "retention receivable" in their ledgers.

New development: The UK Government has been consulting on an outright ban on retention in construction contracts as part of its wider late payment crackdown, with a phased transition period expected once legislation is confirmed. Construction businesses should monitor this closely and prepare retention accounting processes for potential reform.

Revenue Recognition

Revenue is recognised based on work completed, not invoices raised. Under IFRS 15 or FRS 102, contractors must:

- Identify the contract

- Define performance obligations

- Estimate transaction price

- Allocate price to obligations

- Recognise revenue only as obligations are satisfied

This makes record-keeping more demanding than in most industries. Done correctly, it gives you an accurate picture of where each project stands financially — before a problem becomes unrecoverable.

The Construction Industry Scheme (CIS): What UK Contractors Must Know

CIS is a HMRC scheme requiring contractors to deduct tax at source from payments to subcontractors. Deductions are:

- 20% for registered subcontractors

- 30% for unregistered subcontractors

- 0% for those with gross payment status

These deductions are remitted monthly and act as an advance against the subcontractor's income tax and National Insurance obligations.

Who Must Register?

Any business that pays subcontractors for construction work must register as a contractor—including limited companies (a common misconception). If a business both pays and receives construction payments, it must register as both contractor and subcontractor.

Monthly Obligations

Contractors must:

- Verify each subcontractor's CIS status with HMRC before the first payment

- Calculate the correct deduction rate

- Issue payment and deduction statements

- File monthly CIS returns by the 19th of each month

Penalties start from the first day a return is late:

- £100 for 1 day late

- £200 after 2 months

- £300 or 5% of deductions after 6 months

- £300 or 5% of deductions after 12 months

Cash Flow Opportunity

Subcontractors can offset CIS deductions against their Corporation Tax liability or reclaim overpaid amounts from HMRC. Prompt monthly claims—rather than waiting for year-end—can free up meaningful working capital throughout the year.

Errors carry real cost: incorrect deductions, missing verifications, or late filings can trigger financial penalties, HMRC investigation, or loss of gross payment status—which immediately reinstates a 20% deduction rate on all incoming payments.

For UK construction businesses managing monthly CIS returns alongside active project work, outsourced accounting support—such as that provided by VJM Global—ensures filings, verifications, and deduction calculations stay accurate and on time.

VAT in UK Construction: Domestic Reverse Charge, Rates & Compliance

Three VAT Rate Categories

Construction work falls into three categories:

- 0% (zero-rated): New build residential

- 5% (reduced rate): Residential conversions, renovations, certain energy-saving installations, social housing

- 20% (standard rate): Commercial work, repairs, and maintenance

Misapplying rates risks either overcharging clients or undercharging HMRC—both result in HMRC penalties or corrected returns.

VAT Domestic Reverse Charge

Introduced 1 March 2021, the Domestic Reverse Charge applies to most B2B construction services where a VAT-registered subcontractor works for a VAT-registered contractor within CIS.

How it works:

- The subcontractor no longer charges VAT on invoices

- The contractor accounts for both input and output VAT on their own VAT return

- Subcontractor invoices must state: "Reverse charge: customer to account for output tax"

Important: This applies to standard- and reduced-rate supplies, not zero-rated work.

Practical Impact

Cash flow: Subcontractors no longer receive VAT float from clients, which directly affects their cash position.

Both contractors and subcontractors need accounting software that handles reverse charge correctly — incorrect invoicing triggers HMRC penalties and creates reconciliation headaches that take time to untangle.

Making Tax Digital (MTD) for VAT

Getting the reverse charge right depends heavily on having compliant software — which brings MTD into the picture. The VAT registration threshold sits at £90,000 (as of April 2024, unchanged through 2025/26), and MTD-compliant software is mandatory for all VAT-registered businesses above it.

For construction firms, that means your software must handle reverse charge VAT treatment and CIS deduction recording in the same system — not as separate workarounds.

Cash Flow Management for Construction Businesses

Construction faces structural cash flow challenges:

- Upfront material and labour costs before client payment

- 30–90 day payment terms

- Retention withheld for months or years

- Seasonal slowdowns that don't reduce fixed costs

- CIS deductions reduce subcontractors' received payments immediately while refunds come later

The scale of the problem: UK construction businesses face an average payment wait of 83 days, with £30 billion in unpaid invoices owed to the sector. 77% of subcontract projects experience late payment.

Practical Cash Flow Tools

- 13-week rolling cash flow forecasts mapped against project payment schedules

- Retention release calendars to track when withheld funds become due

- Prompt invoicing and application for payment procedures

- Proactive debt management to minimise days sales outstanding

- Working capital facilities such as invoice finance or construction-specific factoring

Outsourced accounting support gives construction firms access to forward-looking financial analysis — identifying cash shortfalls before they hit — without the overhead of a full in-house finance function. For smaller contractors and subcontractors, this is often the most practical route to staying on top of retention tracking and payment forecasting simultaneously.

Construction Accounting Software and Making Tax Digital 2025

What to Look For

Construction-specific accounting software should include:

- Native CIS calculation and return filing

- Reverse-charge VAT handling

- Job costing modules

- WIP and retention dashboards

- Mobile timesheet capture for site teams

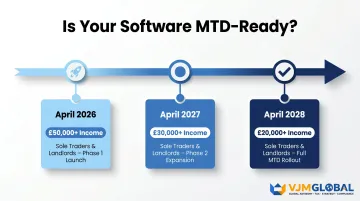

- MTD compatibility for both VAT and the forthcoming MTD for Income Tax

MTD for Income Tax extends to sole traders and landlords with income above:

- £50,000 from 6 April 2026

- £30,000 from 6 April 2027

- £20,000 from 6 April 2028

Software options: General-purpose software like Xero can work for smaller firms when configured correctly. Larger firms may need specialist construction platforms.

The Human Element

Software is only as effective as the people interpreting the data. A well-configured system producing accurate job cost reports, WIP reconciliations, and CIS returns is a strategic asset. Without proper oversight, even the best platform will produce unreliable numbers — and unreliable numbers create compliance risk.

That oversight is easier when your system is cloud-based. Since site teams rarely work from a fixed office, remote access to live job cost data and timesheets keeps everyone aligned — whether they're on-site or in the office.

Frequently Asked Questions

What type of accounting is used in construction in the UK?

UK construction businesses typically use accrual accounting or the percentage of completion method, as these best reflect the long-term, project-based nature of construction work. Smaller firms may use cash accounting, while larger contractors operating under FRS 102 or IFRS 15 use percentage of completion.

Who needs to register for the Construction Industry Scheme (CIS)?

Any business paying subcontractors for construction work must register as a contractor under CIS, including limited companies. If a business both pays and receives construction payments, it must register as both contractor and subcontractor.

What is the VAT Domestic Reverse Charge in construction?

Since March 2021, most B2B construction services between CIS-registered businesses fall under the reverse charge—meaning the contractor (not the subcontractor) accounts for VAT on their own return, and no VAT is charged on the invoice.

What is the difference between the percentage of completion and completed contract methods?

Percentage of completion recognises revenue proportionally as a project progresses, giving a more accurate ongoing picture. The completed contract method defers all revenue until the project is finished—which reduces estimation risk but creates more volatile annual profit figures.

What is job costing and why does it matter for construction businesses?

Job costing assigns all costs—labour, materials, subcontractors, overheads—to individual projects so profitability can be tracked per job. Without it, a construction business may appear profitable overall while specific projects are generating losses.

When does Making Tax Digital (MTD) apply to construction businesses?

MTD for VAT already applies to all VAT-registered businesses. MTD for Income Tax rolls out from April 2026 for sole traders and landlords earning above £50,000, dropping to £30,000 in 2027 and £20,000 in 2028. Check now that your accounting software is MTD-compatible.